Advantages Of Group Health Insurance Plans Usa

Group health insurance plans in the United States offer a vital safety net for employees and employers alike.

By pooling risk across a larger population, these plans provide more affordable premiums, broader coverage options, and access to extensive healthcare networks. For businesses, offering group health insurance enhances employee recruitment and retention while fostering a healthier, more productive workforce.

Employees benefit from reduced out-of-pocket costs, pre-negotiated rates with providers, and protection against high medical expenses. Additionally, group plans often include preventive care services and wellness programs, promoting long-term health. With tax advantages and regulatory protections, group health insurance remains a cornerstone of financial and medical security in the U.S. workforce.

Auto Owners Insurance Phone Number Claims

Auto Owners Insurance Phone Number ClaimsKey Advantages of Group Health Insurance Plans in the USA

Group health insurance plans in the United States offer a wide range of benefits for both employers and employees, making them a cornerstone of comprehensive employee benefits packages.

These plans are typically offered through employers, professional associations, or labor unions and provide participants with access to medical coverage at a lower cost than individual plans. One of the primary reasons businesses opt for group coverage is cost efficiency, as premiums are generally more affordable due to risk sharing across a larger pool of individuals.

Additionally, group plans often come with simplified underwriting, meaning employees may not need to undergo individual medical exams to qualify, increasing accessibility for those with pre-existing conditions. These plans also enhance employee satisfaction, improve workplace morale, and help attract and retain top talent in competitive job markets.

One of the most compelling benefits of group health insurance plans in the USA is the reduction in premium costs due to shared risk among members.

Auto Quotes Insurance New Jersey

Auto Quotes Insurance New JerseyInsurance providers assess risk based on the overall health of the group rather than individuals, which typically results in more favorable rates for employers and employees. Since the risk of high medical claims is distributed across a larger population, insurers can offer lower monthly premiums compared to individual health policies.

Employers often contribute a significant portion—sometimes 50% or more—of the premium, further decreasing the financial burden on employees. This cost-sharing model not only increases affordability but also promotes equitable access to quality healthcare services for a broader segment of the workforce.

Access to Comprehensive Coverage Options

Group health insurance plans in the U.S. typically offer broader and more comprehensive benefits than individual plans, including preventive care, hospitalization, prescription drugs, mental health services, and maternity care.

These plans are designed to meet the diverse healthcare needs of a workforce, often providing multiple plan tiers such as HMO, PPO, and EPO networks, allowing employees to choose coverage that best suits their medical needs and preferred providers.

Auto Repair Insurance Massachusetts

Auto Repair Insurance MassachusettsEmployers may also offer value-added benefits like dental, vision, wellness programs, and telemedicine services as part of the group package. Such comprehensive offerings not only enhance employee well-being but also encourage proactive health management, ultimately leading to reduced absenteeism and increased productivity.

Tax Advantages for Employers and Employees

Both employers and employees enjoy significant tax benefits with group health insurance plans in the United States.

Employer contributions toward employee health premiums are generally tax-deductible as a business expense, lowering the company’s taxable income. For employees, the value of health insurance coverage is typically excluded from gross income, meaning they do not pay federal or state income taxes on the portion of premiums paid by their employer.

Additionally, many group plans allow employees to pay their share of premiums through pre-tax payroll deductions, further reducing their taxable income. These tax incentives make group health insurance a financially sound decision for businesses of all sizes while increasing the net take-home pay and purchasing power of employees.

| Advantage | Description | Key Benefit |

|---|---|---|

| Lower Premiums | Costs are distributed across a large group, reducing individual financial burden. | Employers and employees pay less per person compared to individual plans. |

| No Medical Underwriting | Employees are not required to pass individual health assessments to enroll. | Guaranteed acceptance for all eligible employees, including those with conditions. |

| Tax Savings | Employer contributions are tax-deductible; employee benefits are tax-free. | Reduces taxable income for both parties, increasing overall value. |

| Enhanced Employee Retention | Health benefits increase job satisfaction and perceived value of compensation. | Employers gain a competitive edge in talent acquisition and retention. |

Benefits of Group Health Insurance Plans in the USA

What are the key advantages of group health insurance plans in the US?

One of the most significant benefits of group health insurance plans in the US is the cost savings it offers to both employers and employees. Because these plans cover a large number of individuals, insurance companies can spread the risk across a broader population, which often leads to lower premiums compared to individual health insurance policies.

Employers typically contribute a portion of the premium, further reducing the financial burden on employees. Additionally, group plans benefit from economies of scale in administrative costs, which helps keep overall expenses down.

- Group health plans usually have lower per-person premiums due to shared risk among a larger pool of insured individuals.

- Employers often subsidize a considerable percentage of the premium, decreasing out-of-pocket costs for employees.

- Lower administrative fees and streamlined billing processes reduce overhead for insurers, translating into more affordable rates.

Broader Access to Coverage and Reduced Underwriting Restrictions

Group health insurance plans are generally available to all eligible employees regardless of their health status, thanks to guaranteed issue provisions under regulations like the Affordable Care Act.

This means individuals with pre-existing conditions can gain coverage without being charged higher rates or denied altogether. Such accessibility makes group plans a more inclusive option compared to individual market policies, where medical underwriting could result in exclusions or increased premiums.

- Employees are typically guaranteed coverage without medical underwriting, ensuring inclusivity for those with health issues.

- Pre-existing conditions do not affect eligibility or pricing, aligning with federal healthcare protections.

- Higher participation rates in healthy and less healthy individuals balance the risk pool, maintaining plan stability.

Enhanced Benefits and Comprehensive Coverage Options

Group health insurance plans often offer more robust and diverse benefits than individual plans. Employers can select from various plan designs, including HMOs, PPOs, and high-deductible health plans paired with Health Savings Accounts.

These plans frequently include coverage for preventive care, prescription drugs, mental health services, maternity care, and wellness programs. The collective bargaining power of a group enables access to expansive provider networks and favorable service terms.

- Employers can choose from multiple coverage tiers and benefit structures to meet diverse employee needs.

- Routine screenings, vaccinations, and wellness visits are commonly covered at no additional cost under preventive care mandates.

- Integrated benefits such as telehealth, dental, vision, and behavioral health services enhance the overall value of the plan.

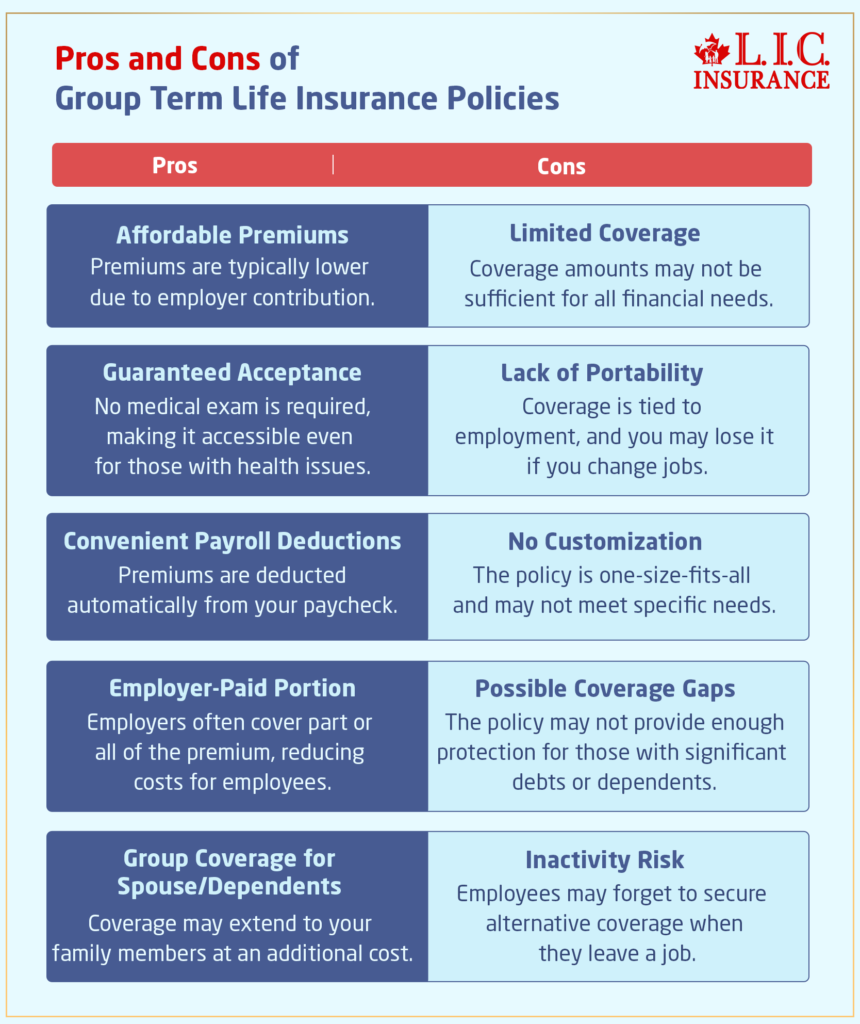

What are the benefits and drawbacks of GTL insurance in relation to group health plans in the US?

What Are the Key Benefits of GTL Insurance in Relation to Group Health Plans?

- One major benefit of Group Term Life (GTL) insurance is its cost-effectiveness for employees. Since the policy is offered through the employer, premiums are typically lower than if individuals were to purchase life insurance independently, thanks to group rate structures and reduced administrative costs.

- GTL insurance often requires no medical underwriting for standard coverage amounts, making it accessible to all eligible employees regardless of health status. This inclusivity ensures broader participation and supports employee well-being initiatives without additional barriers.

- Employers can use GTL as a strategic component of their benefits package to enhance overall job satisfaction and retention. Offering life insurance alongside group health plans signals employer investment in employees' financial and personal security, contributing to a more comprehensive benefits strategy.

What Are the Main Drawbacks of GTL Insurance Compared to Group Health Coverage?

- A significant drawback is the limited coverage amount provided by GTL insurance. Most employer-sponsored policies offer a flat amount or a multiple of salary (e.g., one or two times annual salary), which may be insufficient to meet long-term financial needs of beneficiaries, especially for higher-income employees.

- GTL coverage is generally not portable; employees lose their coverage upon leaving the company unless they convert the policy to an individual plan, which can be much more expensive. This lack of continuity contrasts with health savings accounts or certain health plan options that allow for greater flexibility after employment ends.

- The death benefit from GTL insurance may be partially or fully taxable if the coverage exceeds $50,000 and the employee pays no premium or a discounted premium for the excess. This tax implication creates an additional financial burden for highly compensated employees and requires careful planning and communication from employers.

How Does GTL Insurance Complement or Differ from Group Health Plans in Employee Benefits?

- GTL insurance and group health plans serve different, though complementary, purposes. While group health insurance covers medical expenses related to illness or injury, GTL provides a financial safety net to beneficiaries upon the employee’s death, addressing long-term financial stability for families.

- Integration within the benefits portfolio allows employers to offer a holistic approach to employee security. While health plans support immediate physical health needs, GTL extends protection beyond the employee’s life, reinforcing a culture of care and responsibility.

- Administrative management of both types of coverage often occurs through the same vendor or platform, simplifying enrollment, communication, and HR oversight. However, compliance requirements differ—group health plans are heavily regulated under laws like the ACA and HIPAA, whereas GTL falls under IRS tax code and ERISA, necessitating distinct reporting and monitoring procedures.

What are the key benefits of group health insurance plans through private insurers in the US?

Group health insurance plans offered through private insurers in the United States often result in lower costs for both employers and employees. Because the risk is spread across a larger pool of individuals, private insurers can offer lower premiums compared to individual health plans. Additionally, employers typically contribute a significant portion of the premium, further reducing the financial burden on employees. These plans also benefit from economies of scale, where administrative and operational costs are distributed across the group, resulting in greater efficiency.

- Employers usually cover 50% to 80% of the premium costs, making coverage more affordable for employees.

- Group plans avoid the higher risk-based pricing common in individual insurance, which can be influenced by pre-existing conditions or age.

- Bulk purchasing power allows businesses to negotiate better rates and coverage options with private insurers.

Broader Access to Healthcare Services

One of the primary advantages of group health insurance is expanded access to a comprehensive network of healthcare providers and services. Private insurers provide structured networks including physicians, specialists, hospitals, and clinics, allowing employees and their dependents to receive timely medical care. These plans often include preventive services, mental health coverage, prescription drugs, and wellness programs at little or no out-of-pocket cost, promoting early detection and improved health outcomes.

- Members gain access to large provider networks, increasing options for specialist care and reducing wait times.

- Preventive care benefits such as vaccinations, annual check-ups, and screenings are commonly covered at 100% under the Affordable Care Act mandates.

- Many group plans include telehealth services, offering convenient and cost-effective virtual consultations.

Enhanced Employee Attraction and Retention

Offering group health insurance is a powerful tool for employers seeking to attract and retain skilled workers in a competitive job market. Comprehensive health benefits signal organizational stability and employee care, increasing job satisfaction and loyalty. Employees are more likely to stay with employers who provide reliable healthcare coverage, reducing turnover rates and associated hiring and training costs.

- Health benefits are consistently ranked among the top factors employees consider when evaluating job offers.

- Providing group insurance fosters a sense of security, leading to higher morale and improved productivity.

- Small and mid-sized businesses can leverage group plans to compete with larger companies in talent acquisition efforts.

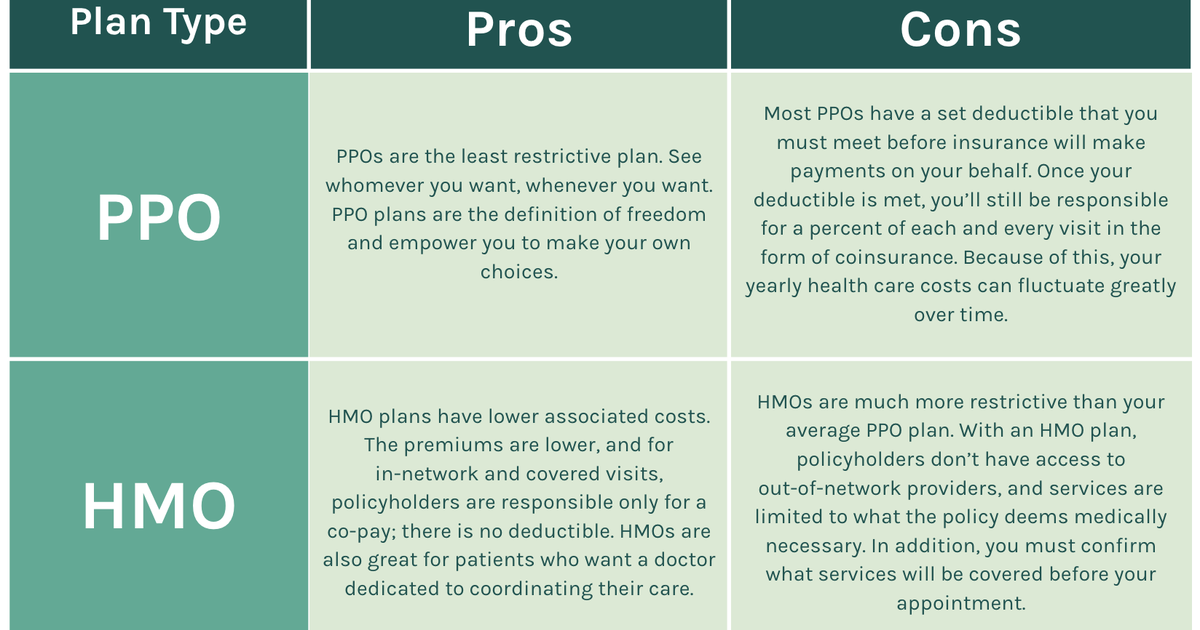

What Are the Key Differences Between PPO and HMO Plans in U.S. Group Health Insurance?

Network Flexibility and Provider Choice

- PPO (Preferred Provider Organization) plans offer greater flexibility in choosing healthcare providers. Enrollees can visit any doctor or specialist without needing a referral, both in and out of the network, although out-of-network care costs more.

- HMO (Health Maintenance Organization) plans require members to use a specific network of providers and typically do not cover services received from out-of-network doctors, except in emergencies. This restriction helps keep costs lower but limits freedom of choice.

- With HMOs, individuals must select a primary care physician (PCP) who coordinates all their care and provides referrals to see specialists. In contrast, PPO members can see specialists directly without going through a PCP or obtaining a referral, offering more convenience for those seeking specialized treatment.

Cost Structure and Out-of-Pocket Expenses

- PPO plans generally come with higher monthly premiums compared to HMOs. This increased cost reflects the broader network access and flexibility offered to members.

- HMO plans usually feature lower premiums and predictable out-of-pocket costs, making them attractive for individuals and employers focused on cost control. However, they require members to stay within the plan’s network to maintain coverage.

- While PPOs cover some out-of-network services, patients pay a higher percentage of the cost through coinsurance and have higher deductibles. HMO enrollees often face lower deductibles and copayments but receive little to no coverage when accessing care outside the network, which increases financial risk if network rules are not followed.

Coverage Scope and Plan Administration

- PPO plans are administered with less oversight, allowing members to manage their healthcare decisions independently. There is no requirement for pre-authorization for most specialist visits, streamlining access to care.

- HMO plans emphasize preventive care and coordinated treatment through the primary care physician. Most services require adherence to the network structure, and procedures often need prior approval to be covered, which can delay care but helps manage overall healthcare spending.

- The administrative framework of HMOs focuses on cost containment and efficiency by centralizing care within a closed network. PPOs, while more expensive, support a decentralized approach that prioritizes patient autonomy and expanded access to providers across regions.

Frequently Asked Questions

What are the main benefits of group health insurance plans in the USA?

Group health insurance plans in the USA offer lower premiums due to shared risk among members, making coverage more affordable. Employers often pay a portion of the premiums, increasing employee savings. These plans provide access to comprehensive benefits like doctor visits, prescriptions, and preventive care. Additionally, they simplify enrollment and guarantee coverage regardless of individual health status, promoting financial security and better healthcare access for employees and their families.

How do group health insurance plans reduce costs for employees?

Group health insurance reduces costs by spreading financial risk across a large pool of people, which lowers premiums. Employers typically cover a significant percentage of the premium, reducing employees' out-of-pocket expenses. Because insurers face less risk with group plans, they offer better rates. Employees also benefit from tax advantages, as premiums are often paid with pre-tax dollars, increasing take-home pay while ensuring access to quality healthcare services at reduced overall costs.

Can small businesses offer group health insurance plans effectively?

Yes, small businesses can effectively offer group health insurance through programs like the Small Business Health Options Program (SHOP). These plans provide flexibility in coverage options and may qualify employers for tax credits of up to 50% of premiums. Offering health insurance helps small businesses attract and retain talent, promotes employee wellness, and enhances competitiveness. With proper planning and provider selection, even small firms can provide valuable, affordable health coverage to their employees.

Are pre-existing conditions covered under group health insurance in the USA?

Yes, group health insurance plans in the USA must cover pre-existing conditions without waiting periods or denials, thanks to the Affordable Care Act. Unlike individual plans, group policies cannot exclude or charge more for conditions like diabetes or asthma. This ensures employees get immediate access to necessary treatments. Employers play a key role in facilitating this inclusive coverage, providing peace of mind and promoting equitable healthcare access for all team members regardless of medical history.

Leave a Reply