Auto Glass Insurance Deductible

When it comes to auto glass repairs or replacements, understanding your insurance deductible is essential. An auto glass insurance deductible is the amount you pay out of pocket before your insurance coverage kicks in. Depending on your policy, this deductible can vary significantly, impacting how much you'll owe for services like windshield or window fixes.

Some plans offer full coverage with no deductible, while others require payments ranging from $100 to $500 or more. Knowing your deductible helps you make informed decisions, avoid unexpected costs, and choose between repair options wisely. This guide explores how deductibles work, factors influencing them, and tips for minimizing expenses.

Understanding Auto Glass Insurance Deductible: What You Need to Know

An auto glass insurance deductible is the amount you're responsible for paying out-of-pocket when repairing or replacing your vehicle’s windshield or other glass components before your insurance coverage kicks in. Depending on your policy, this deductible can vary significantly—typically ranging from $100 to $1,000 or more—and influences how much you'll pay during a claim.

Home inspector insurance california

Home inspector insurance californiaSome auto insurance policies offer full coverage for glass repairs with no deductible, especially for minor fixes like cracks or chips, making it cost-effective to address damage early. However, if your policy includes a deductible, you'll need to decide whether filing a claim is worth the out-of-pocket expense and potential impact on future premiums. Understanding the terms of your deductible is essential to making informed decisions about when and how to use your coverage.

How Does an Auto Glass Deductible Work?

When you experience windshield damage, such as a crack or chip from road debris, your auto glass deductible determines how much you pay toward the repair or replacement.

If your policy has a $250 deductible and the total repair cost is $350, you’ll pay $250 and the insurance company covers the remaining $100. However, many insurers offer exceptions: if the repair cost is below the deductible amount—for example, a $100 repair with a $250 deductible—the insurer may waive the deductible and cover the entire cost, as long as it's a repair rather than a full replacement.

Additionally, some states have laws or insurance companies have policies that allow for zero-deductible coverage specifically for windshield repairs, promoting timely fixes that prevent more costly replacements later. This structure encourages drivers to address small damages early without financial hesitation.

2 home insurance claims in one year

2 home insurance claims in one yearFactors That Influence Your Auto Glass Deductible Amount

Several factors determine the amount of your auto glass deductible, including the terms of your insurance policy, the type of coverage you have (comprehensive vs. collision), and the laws in your state. Drivers who choose a higher deductible typically pay lower monthly premiums, but they'll owe more at the time of a claim.

Conversely, a lower deductible means higher premiums but less out-of-pocket expense when damage occurs. Some insurance providers offer deductible waivers for glass claims, especially if you have comprehensive coverage, which can substantially reduce or eliminate your responsibility.

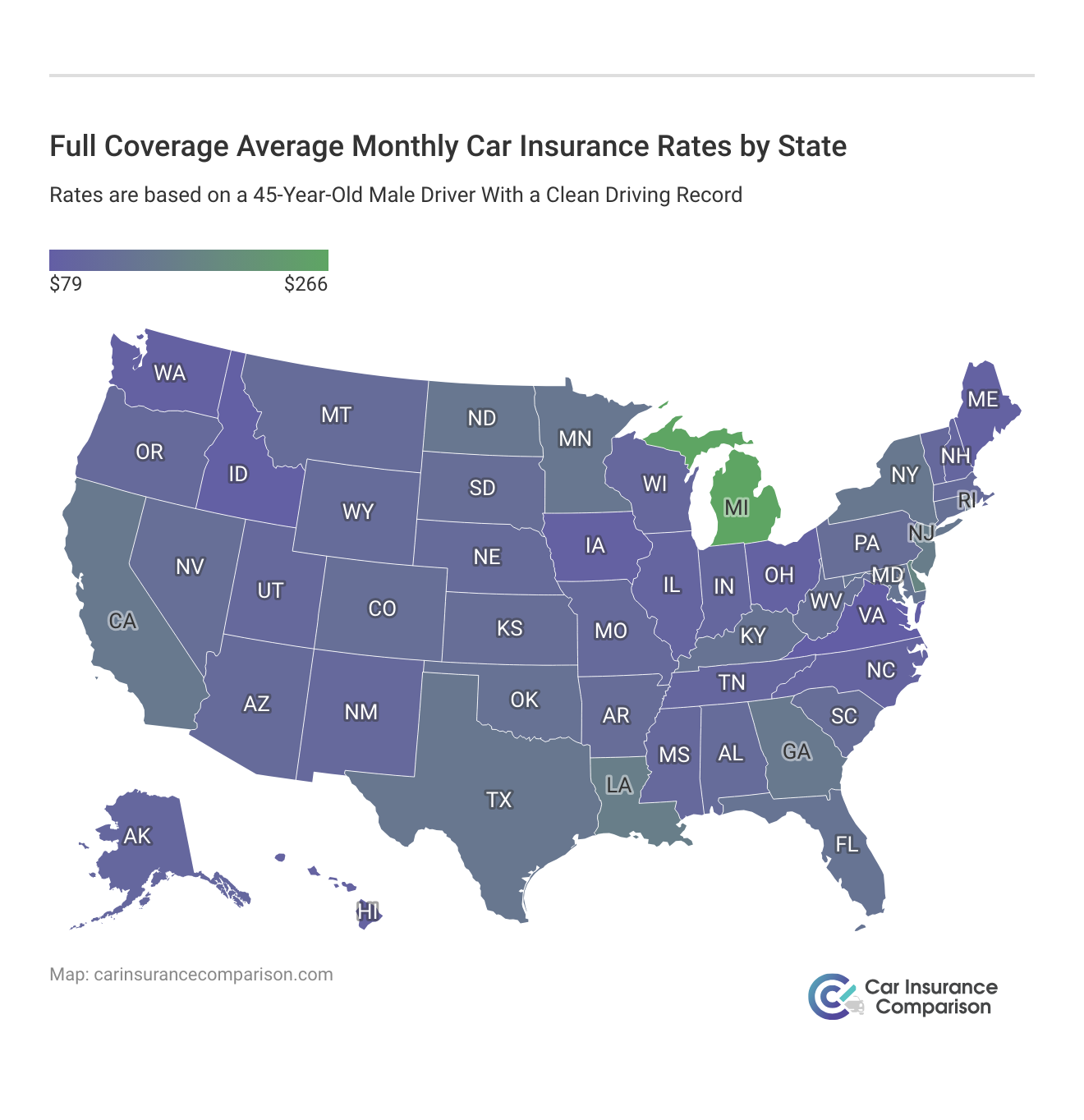

Additionally, where you live matters—states like Florida, Kentucky, and South Carolina mandate zero-deductible coverage for windshield replacements under certain conditions, making it easier and more affordable for residents to maintain safe, clear visibility while driving.

Repair vs. Replacement: How It Affects Your Deductible

The distinction between glass repair and glass replacement significantly impacts how your deductible applies. Most insurance companies do not apply a deductible for windshield repairs because fixing small chips or cracks is cost-effective and helps prevent the need for a full replacement. In many cases, repairs are fully covered under comprehensive coverage with no out-of-pocket cost to the policyholder.

Affordable home insurance claim assistance services

Affordable home insurance claim assistance servicesOn the other hand, windshield replacement usually triggers the deductible since the process is more expensive and labor-intensive. For side windows or rear glass, deductibles typically apply regardless of repair or replacement. Knowing this difference helps drivers make economical decisions: getting a crack repaired quickly not only restores structural integrity but also avoids the higher costs and deductible obligations associated with full replacements.

| Service Type | Typical Cost Range | Deductible Usually Applies? | Insurance Coverage Common? |

|---|---|---|---|

| Windshield Repair (crack/chip) | $50 – $150 | No (often waived) | Yes, often 100% covered |

| Windshield Replacement | $200 – $600+ | Yes (depends on policy) | Yes, minus deductible |

| Side/Rear Window Repair | $100 – $300 | Sometimes | Limited coverage |

| Side/Rear Window Replacement | $200 – $500+ | Yes | Yes, minus deductible |

Understanding Auto Glass Insurance Deductibles: A Comprehensive Guide

What Is an Auto Glass Insurance Deductible and Do You Have to Pay It?

What Is an Auto Glass Insurance Deductible?

- An auto glass insurance deductible is the amount you are required to pay out of pocket before your insurance coverage kicks in for repairing or replacing damaged auto glass, such as a windshield or side window.

- This deductible is typically part of your comprehensive or collision insurance policy, and the amount can vary depending on your specific policy terms—common deductible amounts include $100, $250, or $500.

- For example, if your windshield repair costs $300 and your deductible is $100, you would pay $100 and your insurance company would cover the remaining $200.

When Do You Have to Pay the Deductible?

- You are usually required to pay the deductible when filing a claim for auto glass damage under comprehensive or collision coverage, particularly if the damage resulted from an incident like a rock chip, vandalism, or an accident.

- However, some insurance companies offer full glass coverage as an add-on or built-in benefit, which may waive the deductible for windshield repairs specifically, making repairs free of charge to the policyholder.

- It’s important to check your policy details or contact your insurer, as deductible rules vary by state, insurance provider, and type of service—repair versus full replacement may also be treated differently.

Can You Avoid Paying the Deductible?

- In certain cases, you may not have to pay the deductible, especially if your policy includes zero-deductible windshield repair coverage, which is common in no-fault states like Florida, Kentucky, and South Carolina.

- Insurance companies often waive the deductible for minor repairs (such as fixing small cracks or chips) because it’s more cost-effective for them to fix the issue early rather than pay for a full replacement later.

- Additionally, if you have a luxury vehicle or specific auto policy endorsements, you might receive deductible-free glass services as part of your coverage benefits—always verify your plan’s terms to understand your financial responsibility.

Which states offer $0 deductible for auto glass windshield replacement under insurance policies?

States That Allow $0 Deductible for Windshield Replacement

- Florida is one of the states where insurance policies often include a $0 deductible for windshield replacement. This is due to state regulations that classify windshield repair or replacement under comprehensive coverage, allowing drivers to benefit from full coverage without out-of-pocket costs if their policy includes this provision.

- Kentucky also permits zero-deductible windshield replacement under certain insurance plans. The state does not mandate free windshield replacement, but insurers commonly offer it as part of comprehensive coverage, especially since Kentucky allows drivers to opt for full glass coverage without raising premiums significantly.

- Mexico is not a U.S. state and therefore not applicable, but among U.S. states, South Carolina stands out as another location where zero-deductible glass replacement is widely available. While not required by law, many insurance companies in South Carolina voluntarily waive the deductible for windshield claims as a competitive benefit.

How No-Deductible Glass Coverage Works by State

- In Florida, no-deductible windshield replacement is supported by state law when comprehensive coverage is active. This means that if a driver has comprehensive insurance, the repair or replacement of a cracked or shattered windshield must be provided without applying a deductible, making it one of the most driver-friendly policies in the nation.

- Kentucky operates under a choice system where drivers can select either full glass coverage with no deductible or standard coverage that may require a deductible. Insurance providers in Kentucky are not obligated to offer $0 deductibles, but competition among companies has led many to include it as an attractive policy feature.

- Other states like Massachusetts and Connecticut do not require insurers to offer $0 deductibles for glass, but several major carriers provide this option as an add-on or included benefit. In these states, it’s essential for policyholders to review their specific policy details or consult with their insurer to determine whether their plan includes deductible-free windshield services.

Insurance Providers Offering $0 Deductible Windshield Services

- Geico prominently offers $0 deductible windshield replacement in states like Florida and Kentucky, where regulations or market practices support no-cost glass claims. Their comprehensive policies often include this benefit automatically, reducing financial burden on drivers needing urgent repairs.

- State Farm provides windshield replacement with no deductible in multiple states, especially in regions where customers frequently file glass claims. While not universal across all states, State Farm allows policyholders to add full glass coverage that waives the deductible, particularly beneficial in areas prone to severe weather or road debris.

- Progressive Insurance offers a glass coverage option with zero deductible in several states, including South Carolina and Florida. They promote this feature as part of their comprehensive protection plans, encouraging customers to repair minor damage promptly to avoid full replacements later.

Frequently Asked Questions

What is an auto glass insurance deductible?

An auto glass insurance deductible is the amount you pay out of pocket when repairing or replacing your vehicle's windshield or other glass. It applies before your insurance covers the remaining cost. Deductibles vary by policy, commonly ranging from $100 to $500. Some plans offer full coverage with no deductible, especially for repairs, helping reduce your immediate expenses.

When do I have to pay my deductible for windshield repair?

You pay your deductible for windshield repair when the service is completed, unless your policy waives it. Many insurers cover repairs at no cost to you if the damage is fixable, promoting safety and preventing larger issues. However, for full windshield replacements, the deductible typically applies. Always verify your plan details to understand when and how much you'll need to pay upfront.

Can I avoid paying my auto glass deductible?

Yes, you may avoid paying your deductible if your insurance policy includes full glass coverage or a zero-deductible clause for glass repairs. Some states require insurers to waive the deductible for windshield repairs. Additionally, certain insurance plans cover replacements without a deductible. Check your policy or contact your provider to confirm whether you qualify for a full or partial waiver on glass-related claims.

Does my deductible affect the quality of the replacement glass?

No, your deductible does not affect the quality of the replacement glass. Insurance companies typically use high-quality, OEM (Original Equipment Manufacturer) or equivalent aftermarket glass, regardless of your deductible amount. The repair facility must meet industry standards. Your out-of-pocket cost only influences how much you pay, not the materials or workmanship used. Always choose a certified installer to ensure safety and durability.

Leave a Reply