Auto Insurance Companies In Washington State

Auto insurance is a legal requirement for all drivers in Washington State, providing financial protection against property damage, liability, and personal injury resulting from traffic accidents.

With no state-mandated personal injury protection, residents must carefully evaluate coverage options to ensure adequate protection. Washington’s unique no-fault adjacent system allows drivers to file claims with their own insurers for certain benefits, emphasizing the importance of selecting a reliable insurance provider.

Numerous companies operate in the state, offering a range of policies and pricing structures. Understanding the differences among these providers helps consumers make informed decisions and secure optimal coverage tailored to their needs and budget.

Cheap home insurance los angeles ca

Cheap home insurance los angeles caTop Auto Insurance Companies in Washington State

Washington State drivers have access to a competitive auto insurance market, with numerous providers offering a range of coverage options, pricing models, and customer service experiences.

The state operates under a guaranteed availability program, ensuring that all drivers, regardless of their driving history, can obtain minimum liability coverage through the Washington Automobile Insurance Plan (WAIP) if they are unable to secure a policy in the private market.

Major national insurers like State Farm, Geico, Progressive, and Allstate maintain a strong presence in Washington, often offering competitive rates, online tools, and 24/7 claims support. Regional carriers such as Erie Insurance and Farmers Insurance also serve Washington policyholders, sometimes providing better localized service or bundling options. When choosing an insurer, Washington residents should evaluate factors such as financial stability, customer satisfaction ratings from sources like J.D.

Power or the National Association of Insurance Commissioners (NAIC), and the availability of discounts like safe driver, multi-policy, and good student incentives. Additionally, Washington law requires every registered vehicle to carry liability insurance, personal injury protection (PIP), and uninsured/underinsured motorist coverage unless formally rejected in writing.

Cheap home insurance missouri

Cheap home insurance missouriRegulatory Framework for Auto Insurance in Washington

The Washington State Office of the Insurance Commissioner (OIC) regulates all auto insurance providers operating in the state, ensuring compliance with mandated coverage requirements, fair pricing practices, and consumer protection laws.

Insurers must file their rates and policy forms with the OIC, which reviews them for reasonableness and non-discrimination. Washington follows a no-fault auto insurance system, meaning drivers typically turn to their own insurance first to cover medical expenses and lost wages, regardless of who caused the accident, through Personal Injury Protection (PIP).

However, drivers retain the right to sue the at-fault party if injuries meet a legal threshold, such as significant disfigurement or over $3,000 in medical costs. The OIC also maintains a database of insurer complaints and complaint ratios, helping consumers compare companies based on responsiveness and fairness in handling claims, a critical factor when selecting a reliable provider.

Auto insurance premiums in Washington vary significantly based on insurer, location, driving record, and vehicle type.

Churchill insurance home insurance

Churchill insurance home insuranceOn average, Washingtonians pay slightly above the national median for full coverage insurance. According to recent data from sources like Insurify and NerdWallet, Geico and State Farm frequently rank among the most affordable options for drivers with clean records, often offering average annual rates between $1,200 and $1,500.

Progressive competes aggressively with customizable coverage and usage-based programs like Snapshot, which can reduce premiums for low-mileage or safe drivers. In contrast, Allstate and Nationwide tend to be more expensive but may offer enhanced service features, such as accident forgiveness or better repair guarantees.

Urban areas like Seattle, Bellevue, and Tacoma generally have higher premiums due to increased traffic density and accident rates, while rural drivers may benefit from lower costs. Shopping around and requesting personalized quotes remains essential to securing the best value.

Discounts and Coverage Options for Washington Drivers

Auto insurance companies in Washington offer a variety of discounts designed to reduce premiums for responsible and low-risk drivers. Common available discounts include multi-vehicle, bundling home and auto policies, electronic billing, paperless statements, and safe driver rewards for those with no accidents or violations over several years.

Common exclusions in home insurance policies

Common exclusions in home insurance policiesSome insurers, like Progressive and Allstate, provide defensive driving course discounts and anti-theft device incentives. Additionally, many companies offer pay-in-full discounts or auto-pay savings for choosing convenient payment methods.

Washington-specific options also include low-mileage discounts, ideal for those working remotely or using public transportation, and good student discounts for young drivers maintaining high GPAs. Comprehensive and collision coverages are optional but recommended for newer vehicles, while uninsured motorist protection is mandatory unless formally declined.

| Insurance Company | Average Annual Premium (Full Coverage) | Notable Features | Discounts Offered |

|---|---|---|---|

| Geico | $1,275 | 24/7 customer service, mobile app, quick claims process | Safe driver, military, federal employee, multi-policy |

| State Farm | $1,310 | Local agents, strong financial rating, bundled savings | Good student, defensive driving, multi-car, home bundling |

| Progressive | $1,420 | Snapshot program, price comparison tool, accident forgiveness | Usage-based, multi-policy, home bundling, continuous insurance |

| Allstate | $1,550 | Enhanced repair guarantees, digital claims, local agents | Safe driving rewards, new car replacement, bundle discounts |

| Farmers Insurance | $1,480 | Customizable policies, ride-sharing coverage available | Multi-policy, loyalty, claim-free, low-mileage discounts |

Top Auto Insurance Companies in Washington State: A Comprehensive Guide

Which auto insurance company offers the lowest rates in Washington state?

Top Auto Insurance Providers with the Lowest Rates in Washington

Several auto insurance companies consistently offer competitive rates in Washington state, making them top choices for cost-conscious drivers. Among these, Progressive, State Farm, and Geico stand out for providing affordable premiums while maintaining reliable coverage options.

Corpus christi home insurance

Corpus christi home insuranceProgressive often leads in price comparison tools due to its extensive use of personalized pricing models and safe driver discounts. State Farm benefits from a large network of local agents and bundled policy incentives, which can reduce overall costs.

Geico’s low rates are supported by its direct-to-consumer model, minimizing overhead and passing savings to customers. These insurers balance affordability with strong financial ratings and customer service, making them dependable options across diverse driver profiles.

- Progressive uses advanced telematics and personalized risk assessment to offer among the lowest quotes in Washington.

- State Farm frequently ranks high for affordability, especially for drivers who qualify for loyalty or multi-policy discounts.

- Geico provides consistently low base premiums, particularly for drivers with clean records and low annual mileage.

Factors That Influence Insurance Rates Across Washington

Auto insurance pricing in Washington varies significantly based on multiple factors that insurers evaluate when issuing quotes. Location plays a crucial role, with urban areas like Seattle and Tacoma typically facing higher premiums due to increased traffic density and higher rates of accidents and theft.

A driver’s age, driving record, and credit score are also key determinants—drivers with prior accidents or violations can expect substantially higher rates. Additionally, the type of vehicle insured, coverage levels selected, and annual mileage directly impact premium costs. Insurers use these variables to calculate risk, meaning two drivers in the same city might receive vastly different quotes based on personal circumstances.

- Residing in high-risk ZIP codes with frequent claims history increases premiums regardless of the insurance provider.

- Drivers with an at-fault accident or DUI on record may see their rates double or even triple compared to clean records.

- Choosing higher deductibles and limiting optional coverages such as rental reimbursement can lower monthly premiums.

How to Find and Compare the Best Rates in Washington

To identify the insurer offering the lowest rate for your specific situation, it's essential to compare multiple quotes using reliable methods. Online comparison tools allow side-by-side evaluation of premiums from various companies based on identical coverage levels and personal data.

It's recommended to gather at least three to five quotes to ensure you're getting a competitive rate. Additionally, contacting local independent agents can provide access to lesser-known companies or regional insurers that may offer lower prices not visible through national platforms. Always ensure the coverage limits and deductibles are the same across quotes to make an accurate comparison.

- Use state-approved comparison websites like the Washington Office of the Insurance Commissioner's rate tool to find transparent pricing data.

- Ask insurers about available discounts such as safe driver, student, or pay-in-full reductions to maximize savings.

- Reevaluate your policy annually and switch providers if a competitor offers a significantly lower rate for comparable coverage.

What are the top-rated auto insurance companies in Washington State?

Top-Rated Auto Insurance Companies in Washington State

Washington State drivers have access to a range of highly rated auto insurance providers known for their financial strength, customer service, and competitive rates.

Among the top-rated companies are Progressive, PEMCO, and Nationwide, all of which consistently earn high marks from trusted sources like J.D. Power, AM Best, and the National Association of Insurance Commissioners (NAIC).

Progressive stands out for its broad range of coverage options and digital tools, making it easy for drivers to manage policies online. PEMCO, a regional insurer based in the Pacific Northwest, is widely praised for its exceptional customer service and loyalty discounts tailored to Washington residents.

Nationwide offers strong roadside assistance and accident forgiveness features, appealing to drivers seeking comprehensive protection. These companies also maintain favorable complaint ratios, indicating reliable claim handling and responsive support.

- Progressive offers usage-based insurance programs like Snapshot, which can reduce premiums for low-risk drivers.

- PEMCO provides exclusive discounts for members of certain organizations and communities in Washington.

- Nationwide scores high in customer satisfaction due to its customizable policies and strong financial ratings.

Factors That Influence Insurance Ratings in Washington

Insurance ratings are determined by a combination of financial stability, customer satisfaction, claims processing efficiency, and affordability. In Washington, companies are evaluated based on how promptly and fairly they handle claims, which is crucial during accidents or emergencies.

The Washington State Office of the Insurance Commissioner (OIC) monitors insurers’ performance, including complaint volumes and rate approvals. AM Best assesses financial strength, ensuring companies can pay out claims even during widespread events. J.D.

Power surveys customers on overall satisfaction, interaction quality, and digital experience. Lower NAIC complaint index scores indicate fewer complaints relative to the company’s market share, a sign of reliability. Insurers that perform well across these metrics typically rank higher in statewide comparisons.

- Financial strength ratings from AM Best reflect an insurer’s ability to meet ongoing obligations to policyholders.

- Customer satisfaction scores from J.D. Power consider ease of use, agent support, and claims resolution.

- The NAIC complaint index compares the number of complaints an insurer receives against industry averages.

How Washington Drivers Can Choose the Best Auto Insurance

Selecting the best auto insurance in Washington involves comparing multiple factors beyond just premiums. Drivers should review coverage options, available discounts, and local agent availability. It’s also important to check if an insurer offers specific benefits like rideshare coverage, custom equipment protection, or accident forgiveness.

Reading customer reviews and checking the OIC’s consumer complaint database can help identify reliable providers. Obtaining quotes from at least three top-rated companies ensures a balanced view of cost versus service quality.

Additionally, drivers with clean records may qualify for preferred pricing tiers, while those with past incidents should look for insurers with supportive reinstatement policies. Tailoring a policy to individual needs leads to better long-term satisfaction.

- Compare coverage limits and deductible options to find a balance between affordability and protection.

- Look for local discounts such as safe driver rewards, multi-policy bundles, or paperless billing reductions.

- Verify the insurer’s claims process, including 24/7 reporting options and mobile app support.

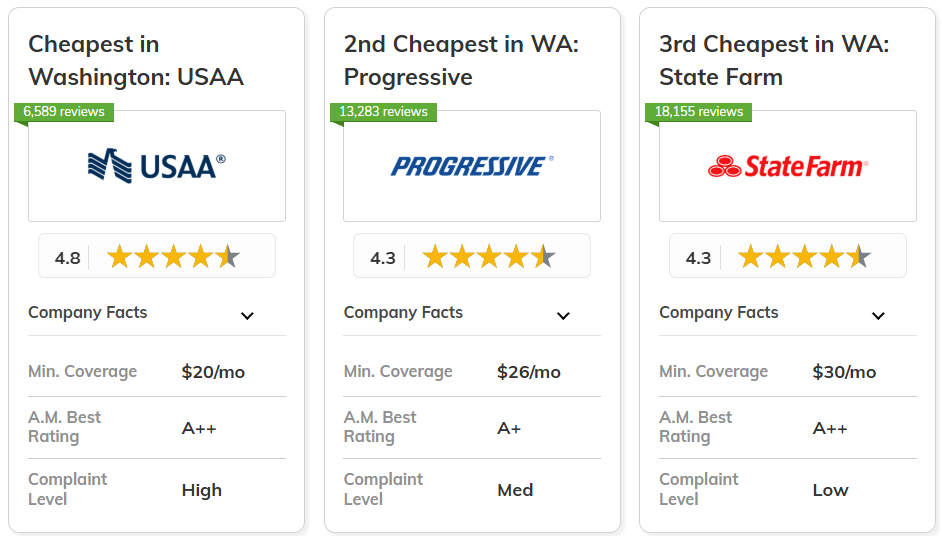

Is Pemco more affordable than Progressive for auto insurance in Washington State?

When evaluating whether PEMCO is more affordable than Progressive for auto insurance in Washington State, examining average premiums is a critical starting point. Multiple comparative studies and consumer reports consistently show that PEMCO generally offers lower base rates for standard drivers across various cities in Washington, especially in urban areas like Seattle and Tacoma.

This regional focus allows PEMCO to tailor pricing more precisely to local driving conditions, claims history, and theft rates. In contrast, Progressive, as a national insurer, applies broader risk models that may not account for localized factors as effectively.

- PEMCO's deep regional expertise in the Pacific Northwest enables it to price policies more competitively for Washington residents.

- Progressive’s national footprint means its algorithms are less sensitive to state-specific driving behaviors, which can result in higher premiums for some drivers.

- Independent rate analyses from sources like NerdWallet and Insurify show that PEMCO typically undercuts Progressive by 10% to 20% for similar coverage levels among low-risk drivers.

Impact of Individual Factors on Pricing

Affordability between PEMCO and Progressive can vary significantly based on personal factors such as driving history, credit score, vehicle type, and annual mileage.

While PEMCO tends to reward safe drivers with loyalty discounts and low-mileage incentives, Progressive often competes with usage-based programs like Snapshot, which can reduce rates for drivers who exhibit cautious behavior monitored via telematics. However, drivers with minor infractions may find PEMCO’s underwriting more forgiving, particularly if they have longstanding ties to the Pacific Northwest.

- Drivers with clean records and strong local residency history often qualify for PEMCO’s regional discounts, including multi-policy and homeowner bundling.

- Progressive may offer better deals for high-risk drivers or those seeking flexible payment plans and accident forgiveness, though base rates may start higher.

- Young drivers or those shopping for their first policy may benefit from Progressive’s broader digital tools and instant quotes, but PEMCO frequently offers better long-term value once eligibility requirements are met.

Discount Availability and Policy Customization

The affordability of an auto insurance policy is not solely determined by base premiums but also by the availability of discounts and the flexibility of coverage options.

PEMCO provides a structured yet generous set of discounts tailored to Washington residents, including claims-free rewards, paperless billing, and discounts for insuring newer vehicles with advanced safety features. Progressive, by comparison, offers a wider array of customizable coverage add-ons and dynamic discount opportunities based on real-time driving data.

- PEMCO offers a claims-free discount that increases over time, rewarding consistent safe driving with progressively larger savings each year.

- Progressive’s Snapshot program can yield substantial savings—up to 30%—for drivers who drive less frequently or avoid high-risk hours, though participation is optional and results vary.

- Both insurers offer multi-car and bundling discounts, but PEMCO often integrates these more seamlessly for homeowners in Washington, especially when combined with property insurance through the same provider.

Which auto insurance company in Washington State typically offers the lowest rates?

Which Auto Insurance Companies Offer the Most Competitive Rates in Washington State?

Several auto insurance providers consistently rank among the most affordable in Washington State based on industry data and consumer reports.

Companies like Progressive, GEICO, and State Farm are frequently cited for offering competitive base premiums, especially for drivers with clean records and strong credit histories. Progressive often uses advanced quote tools and usage-based programs like Snapshot to customize pricing, which can significantly reduce costs for low-mileage or safe drivers.

GEICO maintains low overhead due to its direct-to-consumer model, helping keep premiums affordable. State Farm, with its large network of local agents, offers personalized service while still remaining cost-competitive for many customer profiles. It's important to note that while these insurers commonly offer low initial rates, final pricing depends on numerous individual factors.

- Progressive leverages technology and real-time data to provide dynamic pricing models, which can lead to lower premiums for cautious drivers.

- GEICO’s focus on digital efficiency and large-scale operations enables savings that are often passed on to customers in the form of lower base rates.

- State Farm combines affordability with accessibility, using agent-driven assessments to tailor coverage and pricing to specific regional risks in Washington.

What Factors Influence Auto Insurance Rates in Washington?

Auto insurance pricing in Washington State is shaped by a combination of regulatory policies, driver behavior, and geographic risk. Washington is a tort state, meaning drivers must carry liability coverage to pay for damages they cause in an accident, which impacts how insurers calculate risk exposure.

Key factors that influence individual premiums include driving history, age, vehicle type, credit score, annual mileage, and where the vehicle is primarily parked or driven. Urban areas like Seattle and Tacoma tend to have higher rates due to increased traffic density, theft risks, and higher claim frequencies.

Insurance companies also consider data from past claims in specific ZIP codes when setting premiums. As a result, even the most competitively priced insurers may offer different quotes to seemingly similar drivers based on location and personal circumstances.

- Driving record is a primary determinant—drivers with accidents or violations typically face higher premiums across all insurers.

- Geographic location within the state plays a major role, with city dwellers often paying more due to congestion and higher incident rates.

- Vehicle specifics such as make, model, safety features, and repair costs influence premiums significantly, especially for newer or high-performance cars.

How Can Washington Drivers Secure the Lowest Possible Auto Insurance Rates?

Securing the lowest auto insurance rate in Washington involves a strategic approach beyond choosing a single insurer. Drivers should actively compare quotes from at least four to five providers, as pricing algorithms and risk tolerance vary widely between companies.

Taking advantage of available discounts—such as multi-policy, safe driver, low-mileage, or student discounts—can also reduce costs. Completing defensive driving courses or enrolling in telematics programs that monitor driving behavior may result in long-term savings.

Additionally, adjusting coverage limits and deductibles to match one’s financial situation, while still meeting state minimums, can optimize premium cost. Maintaining a strong credit history is particularly beneficial, as Washington law allows insurers to use credit-based insurance scores in pricing decisions.

- Regularly shopping around every 6 to 12 months ensures drivers do not miss better offers that may become available due to shifting market conditions.

- Combining auto insurance with home or renters policies under the same provider often unlocks multi-policy discounts that substantially lower overall costs.

- Using usage-based insurance programs allows safe drivers to demonstrate responsible habits and receive personalized rate reductions over time.

Frequently Asked Questions

What are the minimum auto insurance requirements in Washington State?

Washington State requires drivers to carry liability insurance with minimum coverage of $25,000 for bodily injury per person, $50,000 per accident, and $10,000 for property damage. Drivers must also have personal injury protection and uninsured motorist coverage unless they formally reject it in writing. Proof of insurance must be carried at all times while driving.

Which auto insurance companies operate in Washington State?

Major auto insurance companies in Washington State include Progressive, State Farm, Geico, Allstate, Liberty Mutual, and Nationwide. Local providers such as Safeco and the Washington Automobile Insurance Company (WAIC) also serve residents. These companies offer various coverage options, discounts, and customer service tailored to state regulations and regional driving conditions.

How can I find affordable auto insurance in Washington State?

To find affordable auto insurance in Washington, compare quotes from multiple providers online, take advantage of discounts like safe driving or bundling, and consider raising deductibles. Maintaining a clean driving record and good credit score also helps lower premiums. Some insurers offer pay-per-mile plans ideal for low-mileage drivers seeking cost savings.

Does Washington State require personal injury protection (PIP) insurance?

Yes, Washington requires personal injury protection (PIP) as part of auto insurance policies unless the driver explicitly rejects it in writing. PIP covers medical expenses, lost wages, and essential services regardless of fault after an accident. It ensures quick payment of benefits without waiting for liability determinations, providing immediate financial support to injured drivers and passengers.

Leave a Reply