Auto Insurance In Dallas

Auto insurance in Dallas is a crucial consideration for drivers navigating the bustling streets of one of Texas’ largest cities. With heavy traffic, frequent road construction, and a high rate of uninsured motorists, having reliable coverage is more than just a legal requirement—it’s a financial safeguard. Dallas drivers face unique risks influenced by urban density, weather conditions, and accident rates, making it essential to understand policy options. From liability and collision to comprehensive and personal injury protection, selecting the right plan depends on individual needs and vehicle usage. Many insurers offer tailored plans, but shopping wisely can lead to significant savings.

Understanding Auto Insurance in Dallas: Coverage, Costs, and Requirements

Auto insurance in Dallas is a critical necessity for every driver navigating the city’s bustling roads and highways. With a growing population and high traffic density, Dallas presents unique risks that make reliable coverage essential. Texas law mandates all drivers to carry a minimum level of liability insurance, commonly referred to as 30/60/25 coverage, which includes $30,000 for injury per person, up to $60,000 per accident, and $25,000 for property damage. However, these minimums may not be sufficient in the event of a serious accident, prompting many Dallas residents to opt for enhanced policies that include uninsured motorist coverage, personal injury protection (PIP), and comprehensive or collision coverage. Insurance premiums in Dallas are influenced by multiple factors, such as driving history, vehicle type, credit score, and even ZIP code, with higher rates typically found in areas with increased accident frequency or auto theft. Working with local insurance agents or using online comparison tools can help drivers find affordable and well-suited policies. Choosing the right auto insurance in Dallas involves understanding not only the legal requirements but also the potential financial risks of being underinsured in an urban environment.

Minimum Legal Requirements for Auto Insurance in Dallas

In Dallas, as in the rest of Texas, drivers are required to meet the state’s minimum auto insurance requirements to legally operate a vehicle. These requirements consist of liability coverage with limits of $30,000 for injuries per person, $60,000 for total injuries per accident, and $25,000 for property damage—commonly known as 30/60/25 coverage. While this is the legal baseline, it's important to note that this level of coverage only pays for damages the policyholder causes to others and does not cover their own vehicle repairs or medical bills. Drivers who finance their vehicles are typically required by lenders to carry additional collision and comprehensive coverage. Furthermore, Texas allows drivers to opt out of insurance by posting a cash bond with the state, though this is rarely practical. Failing to maintain proper insurance can result in steep fines, license suspension, or even vehicle impoundment. Therefore, understanding and complying with Dallas’s minimum insurance mandates is the first step toward responsible vehicle ownership.

Compare home insurance in bryan county

Compare home insurance in bryan countyAverage Costs of Auto Insurance in Dallas Compared to State and National Averages

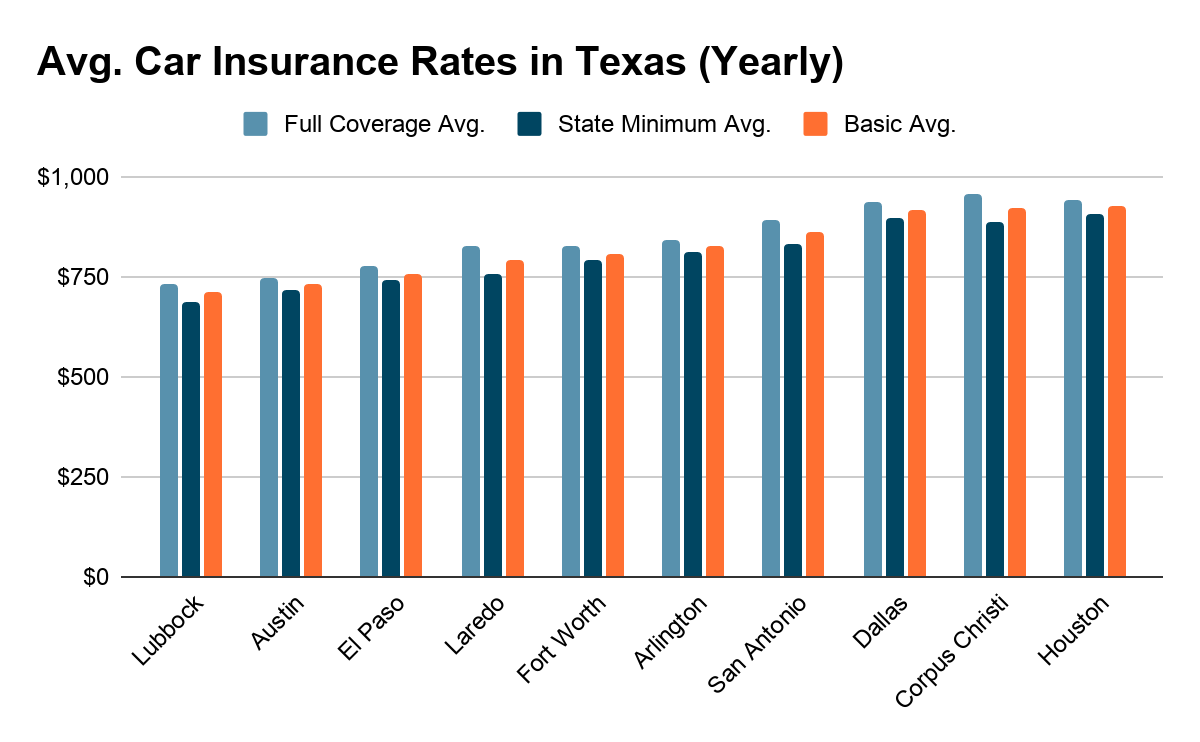

Auto insurance rates in Dallas tend to be higher than both the Texas state average and the national average due to factors like heavy traffic, high rates of uninsured drivers, and elevated auto theft and accident statistics. On average, Dallas drivers pay between $1,600 and $2,000 annually for full coverage insurance, compared to the Texas average of around $1,800 and the U.S. national average of approximately $1,700. Several variables influence these rates, including the driver's age, driving record, credit history, chosen coverage limits, and the type of vehicle insured. For example, a young driver with a history of traffic violations will likely face significantly higher premiums than an older driver with a clean record. Geographic location within Dallas also matters—areas with higher crime or congestion typically have pricier premiums. To reduce costs, many residents shop around, take advantage of discounts (such as multi-policy or safe driver discounts), and maintain good credit, which insurers in Texas are legally permitted to consider when pricing policies.

Common Optional Coverages Dallas Drivers Should Consider

While Texas mandates only basic liability coverage, many drivers in Dallas enhance their protection with optional coverages tailored to local risks. Uninsured/underinsured motorist coverage is highly recommended, especially since Texas ranks among the highest states for uninsured drivers—nearly 15% of motorists on Dallas roads may lack adequate insurance. This coverage helps pay for medical expenses and vehicle repairs if you're involved in a crash with an uninsured or underinsured driver. Personal injury protection (PIP) is another valuable option, covering medical bills, lost wages, and funeral costs regardless of fault. For those concerned about vehicle damage from incidents other than collisions—such as hailstorms, theft, or vandalism—comprehensive coverage is essential, particularly in a city prone to severe weather. Collision coverage pays for repair costs after an accident, regardless of fault, and is typically required by lenders. Lastly, gap insurance is beneficial for drivers who lease or finance new vehicles, as it covers the difference between the car’s value and the outstanding loan amount if the vehicle is totaled.

| Insurance Coverage Type | Description | Recommended For |

|---|---|---|

| Liability (30/60/25) | Mandatory in Texas; covers injury and property damage to others you cause in an accident. | All drivers; meets legal minimum. |

| Uninsured Motorist Coverage | Covers medical and repair costs if hit by a driver without insurance. | Drivers in high-risk areas with many uninsured motorists. |

| Comprehensive Coverage | Covers non-collision damage like theft, vandalism, or weather events. | Owners of newer or valuable vehicles; those in hail-prone zones. |

| Collision Coverage | Pays for repairs to your car after an accident, regardless of fault. | Financed or leased vehicles; high-traffic commuters. |

| Personal Injury Protection (PIP) | Covers medical expenses, lost wages, and other costs regardless of fault. | Families seeking broader medical coverage. |

Comprehensive Guide to Auto Insurance in Dallas: Coverage Options and Cost Factors

What factors influence auto insurance rates in Dallas, Texas?

Demographics and Population Density in Dallas

Several demographic factors contribute to auto insurance rates in Dallas, Texas. The city's large and growing population increases traffic congestion, raising the likelihood of accidents. Insurance companies analyze statistical data related to age, gender, marital status, and population density when determining risk. Urban areas like Dallas generally see higher premiums due to greater exposure to accidents, theft, and vandalism.

Costco home insurance rates

Costco home insurance rates- The high population density in central Dallas leads to more vehicles on the road, increasing the probability of collisions and claims.

- Young drivers, who are statistically more prone to accidents, are a significant demographic in the Dallas metro area, affecting overall risk assessment.

- Insurance providers use zip code-level data to assess crime and accident rates, with certain neighborhoods carrying higher premiums due to above-average incidents.

Local Crime and Accident Statistics

Auto insurance rates in Dallas are heavily influenced by local crime and accident data. Areas with higher incidences of vehicle theft, vandalism, and hit-and-run accidents are considered higher risk by insurers. Dallas has reported above-average rates for auto theft compared to national figures, which directly impacts comprehensive coverage costs. Additionally, the frequency and severity of traffic accidents contribute to claim histories that insurers use to adjust premiums.

- Dallas consistently ranks among Texas cities with the highest number of uninsured drivers, increasing the risk for insured drivers and leading to higher rates for uninsured motorist coverage.

- High-accident intersections and well-traveled corridors, such as those near I-35E and LBJ Freeway, contribute to claims frequency, prompting insurers to apply risk-based pricing.

- Vehicle break-ins and thefts in densely populated or low-income neighborhoods are factored into comprehensive premium calculations.

Driving History and Personal Behavior

An individual’s driving record plays a critical role in determining auto insurance costs in Dallas. Insurance companies evaluate past behavior, including traffic violations, at-fault accidents, and license suspensions, to predict future risk. Drivers with clean records typically qualify for lower premiums, while those with citations for speeding, DUI, or reckless driving face significant rate increases. Insurers also consider behavioral factors like annual mileage and usage patterns.

- Drivers with a history of traffic violations, such as speeding tickets or red-light camera infractions, are seen as higher risk and are charged correspondingly higher premiums.

- Accidents and insurance claims within the past 3 to 5 years can substantially raise rates, particularly if the driver was at fault.

- Annual mileage and commuting patterns are assessed—those who drive longer distances or during peak hours are viewed as more exposed to potential accidents.

What is the most affordable auto insurance in Dallas, Texas?

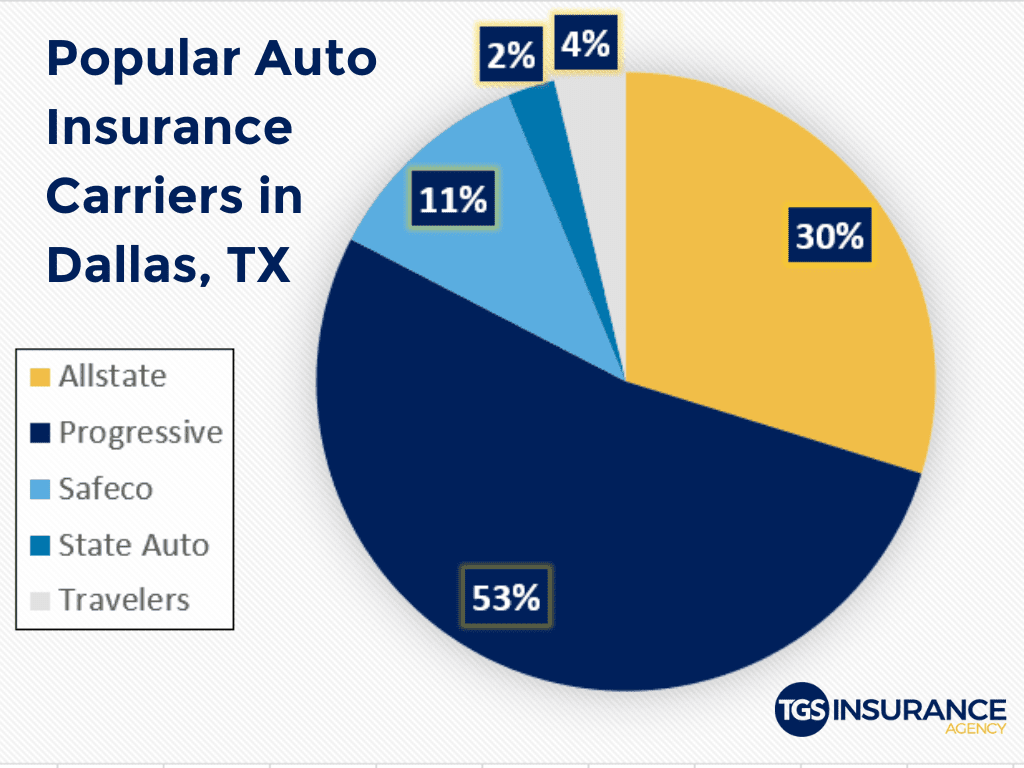

Top Budget-Friendly Auto Insurance Providers in Dallas

When searching for the most affordable auto insurance in Dallas, Texas, several insurers consistently offer competitive rates for drivers. Companies like State Farm, USAA (for military members and their families), and Geico are often ranked at the top for low premiums without sacrificing essential coverage. State Farm frequently offers discounts for safe driving, home and auto bundling, and paperless billing, which can reduce monthly costs significantly. USAA, known for its excellent customer service and pricing, typically provides some of the lowest rates in Dallas but is limited to active and former military personnel and their families. Geico stands out with straightforward pricing and a wide range of discounts, particularly for federal employees and educators. Drivers in Dallas should also consider Progressive and Dairyland, as both insurers offer flexible payment plans and special programs for high-risk drivers who may struggle to find affordable options elsewhere.

Difference between home insurance endorsements and exclusions

Difference between home insurance endorsements and exclusions- State Farm offers localized rate advantages in Dallas due to its extensive agent network and multiple discount opportunities.

- USAA’s average premiums are among the lowest, but eligibility is restricted to military-affiliated individuals and their families.

- Geico provides scalable online tools and personalized quotes, making it easy for Dallas drivers to find low-cost plans quickly.

Factors That Influence Auto Insurance Costs in Dallas

Auto insurance rates in Dallas are influenced by a combination of personal, geographic, and vehicle-related factors. Personal elements such as age, driving history, credit score, and coverage needs play a significant role in determining premiums. For instance, young drivers or those with past traffic violations will typically pay more. The city’s high population density and traffic congestion contribute to increased accident and theft rates, which insurance companies factor into pricing. Additionally, where you park your car—whether in a secure garage or on a busy downtown street—can affect your premium. Vehicle type is another crucial element; cars with higher repair costs or poor safety ratings usually attract higher insurance prices. Lastly, the amount of coverage chosen, including liability limits and optional protections like comprehensive and collision, directly impacts the overall cost.

- Traffic density in Dallas leads to more frequent claims, pushing up average premiums compared to less congested areas.

- Insurance companies use credit-based insurance scores, so individuals with lower credit may pay higher rates.

- Choosing higher deductibles can lower monthly premiums but increases out-of-pocket costs during a claim.

Ways to Save on Car Insurance in Dallas, Texas

Dallas drivers have multiple strategies available to reduce their auto insurance expenses without compromising necessary coverage. One of the most effective methods is shopping around and comparing quotes from at least three different insurers annually. Many drivers overlook renewal opportunities to switch providers for better rates. Bundling home or renters insurance with auto coverage through the same company often unlocks substantial discounts. Safe driving habits are also rewarded; maintaining a clean record can qualify drivers for accident-free and loyalty discounts. Usage-based insurance programs, such as Geico’s DriveEasy or Progressive’s Snapshot, track driving behavior and can lead to lower premiums for cautious drivers. Additionally, completing a state-approved defensive driving course may result in reduced rates and even traffic ticket dismissal in some cases.

- Annual comparison shopping ensures you're not overpaying, as rates can change based on company risk models and competition.

- Bundling policies can reduce total insurance costs by 10% to 25%, depending on the provider and coverage types.

- Participating in telematics programs allows insurers to assess real driving behavior, often benefiting safe drivers with lower premiums over time.

Why Does Auto Insurance Cost More in Dallas Compared to Other Cities?

Traffic Congestion and High Accident Rates

The cost of auto insurance in Dallas is significantly influenced by the city's heavy traffic congestion and high frequency of traffic accidents. As one of the largest metropolitan areas in Texas, Dallas experiences constant vehicle volume on major highways such as I-35E, I-635, and US-75, where bottlenecks and rush hour gridlock are common. This congestion increases the likelihood of collisions, including fender benders, rear-end crashes, and multi-vehicle pileups. Insurance companies analyze historical claims data and recognize Dallas as a high-risk area due to the sheer number of reported incidents, which directly affects premium pricing. Drivers in densely populated urban zones are more likely to file claims, prompting insurers to raise rates to offset potential losses.

- High vehicle density leads to more frequent accidents, increasing the number of insurance claims filed annually.

- Rush hour traffic in central Dallas and surrounding suburbs elevates stress and distracted driving, contributing to higher collision rates.

- Insurance providers use local accident statistics to assess risk, and Dallas consistently ranks above average for per capita claims.

Vehicle Theft and Property Crime Trends

Another major factor driving up auto insurance costs in Dallas is the elevated rate of vehicle theft and property crimes related to automobiles. Compared to many other cities in Texas and the U.S., Dallas reports a higher incidence of car theft, break-ins, and vandalism. Neighborhoods within the city limits, as well as adjacent areas like South Dallas and parts of West Dallas, have been historically prone to these crimes. Comprehensive coverage, which protects against non-collision incidents such as theft and glass damage, becomes more expensive as insurers adjust rates to reflect the increased likelihood of such claims. Additionally, the cost of replacing high-theft vehicles or repairing damaged ones adds financial pressure on insurance companies, which is then passed on to policyholders.

- Dallas consistently ranks among the top U.S. cities for auto thefts per capita, according to FBI crime data.

- Popular models like full-size pickup trucks and luxury SUVs are frequent targets, increasing claim payouts for insurers.

- Higher crime rates mean increased risk exposure, leading insurers to charge more for comprehensive and personal property protection.

Population Growth and Urban Expansion

Rapid population growth and ongoing urban sprawl in the Dallas-Fort Worth metroplex contribute to rising auto insurance premiums. The region has seen a significant influx of new residents over the past decade, driven by job opportunities, affordable housing (in some areas), and business development. However, this population surge has led to more vehicles on the road, expanded road networks, and increased construction zones—all of which create new hazards for drivers. As the number of licensed drivers rises, so does the probability of accidents and claims. Furthermore, infrastructure often struggles to keep pace with growth, resulting in poorly lit streets, confusing interchange designs, and higher congestion in developing suburbs, all of which insurers consider when calculating risk.

- The DFW metro area is one of the fastest-growing in the U.S., with over 7 million residents and rising, increasing roadway density.

- Urban expansion leads to more inexperienced drivers and longer commutes, both associated with higher accident risk.

- Insurance companies factor in long-term risk trends, and sustained growth in Dallas signals ongoing claims pressure, warranting higher premiums.

Frequently Asked Questions

What does auto insurance in Dallas typically cover?

Auto insurance in Dallas generally includes liability coverage for bodily injury and property damage, which is legally required. Most policies also offer optional coverages like collision, comprehensive, uninsured/underinsured motorist, and medical payments. Additional protections may cover rental car fees, roadside assistance, or personal injury protection. Coverage limits and inclusions vary by provider and policy tier, so reviewing your options carefully ensures adequate protection based on your driving habits and vehicle value.

Why is car insurance more expensive in Dallas compared to other cities?

Car insurance rates in Dallas tend to be higher due to factors like population density, traffic congestion, and a higher incidence of accidents and vehicle theft. Insurance companies also consider local crime rates, weather-related risks, and the cost of medical care and vehicle repairs. Urban areas like Dallas typically see more claims, leading insurers to adjust premiums accordingly. Drivers with clean records can still find competitive rates by shopping around and taking advantage of available discounts.

You can reduce your auto insurance costs in Dallas by maintaining a clean driving record, bundling policies, and qualifying for discounts such as safe driver, multi-vehicle, or military benefits. Raising your deductible can also lower premiums, though it increases out-of-pocket costs in case of a claim. Completing a defensive driving course may qualify you for further savings. Regularly comparing quotes from different insurers ensures you’re getting the best rate for the coverage you need.

Is minimum liability coverage enough for driving in Dallas?

While minimum liability coverage meets Texas legal requirements, it may not provide sufficient protection in Dallas due to high traffic volumes and expensive repair and medical costs. Minimum coverage limits could leave you responsible for paying large out-of-pocket expenses after an accident. Experts recommend purchasing higher liability limits and adding collision and comprehensive coverage for better financial protection. Evaluating your risk and assets can help determine the right level of coverage for your needs.

Leave a Reply