Auto Insurance Policy Terms

Understanding auto insurance policy terms is essential for every driver. These terms define the coverage, responsibilities, and limitations of both the insured and the insurance provider.

From liability and collision coverage to deductibles and premiums, each element plays a crucial role in determining protection and cost. Misinterpreting key clauses can lead to unexpected expenses or insufficient coverage during a claim. Policies often include exclusions, limits, and conditions that require careful review.

Being familiar with common terminology helps drivers make informed decisions, compare policies effectively, and ensure they have the right protection for their needs, ultimately providing peace of mind on the road.

Health insurance coverage at-home allergy test kits

Health insurance coverage at-home allergy test kitsUnderstanding Auto Insurance Policy Terms: What You Need to Know

Auto insurance policies are legal contracts between drivers and insurance providers that define the terms, conditions, and coverage options available in the event of an accident, theft, or other vehicle-related incidents.

Understanding the key terminology used in these policies is essential to ensure you are adequately protected and not caught off guard when filing a claim. These terms dictate everything from the amount of coverage you receive to your financial responsibility in various scenarios.

Policyholders should be familiar with components such as liability limits, deductibles, premiums, and coverage types to make informed decisions when purchasing or renewing a policy. Misinterpreting these terms can result in insufficient coverage, higher out-of-pocket costs, or even claim denials.

Types of Auto Insurance Coverage Explained

Auto insurance policies typically include several types of coverage, each designed to protect against different risks.

Home and auto insurance in los angeles

Home and auto insurance in los angelesLiability coverage is often required by law and helps pay for damages or injuries you cause to others in an accident. It is usually broken down into two parts: bodily injury liability and property damage liability. Collision coverage assists in repairing or replacing your vehicle after a crash, regardless of fault, while comprehensive coverage protects against non-collision incidents such as theft, vandalism, fire, or natural disasters.

Uninsured/underinsured motorist coverage safeguards you if you're hit by a driver with no or insufficient insurance. Finally, medical payments (MedPay) or personal injury protection (PIP) covers medical expenses for you and your passengers, regardless of fault. Selecting the right combination of coverages depends on your state's requirements, driving habits, and financial situation.

Two of the most fundamental terms in any auto insurance policy are deductibles and premiums, which directly impact your out-of-pocket costs. A premium is the amount you pay—usually monthly or biannually—to maintain active coverage with your insurer.

It's calculated based on factors like driving history, vehicle type, location, and chosen coverage limits. On the other hand, a deductible is the amount you must pay out of pocket before your insurance kicks in when making a claim. For example, if your deductible is $500 and you incur $3,000 in repairs from an accident, you pay the first $500 and the insurer covers the remaining $2,500.

Home care providers insurance

Home care providers insuranceGenerally, policies with higher deductibles come with lower premiums, but this means you’ll pay more at the time of a claim. Choosing the right balance between premiums and deductibles involves weighing your ability to handle unexpected expenses against your monthly budget.

Policy Limits and Coverage Maximums

Policy limits refer to the maximum amount an insurance company will pay for a covered loss during the policy period. These limits are usually expressed in specific dollar amounts and can vary by coverage type.

For instance, a liability policy might be structured as 25/50/25, meaning $25,000 per person for bodily injury, $50,000 per accident for bodily injury, and $25,000 for property damage. Once these coverage maximums are reached, the policyholder is responsible for any additional costs. It's crucial to select limits that adequately protect your assets, especially in high-liability situations.

While state minimums may seem sufficient, they often fall short in serious accidents. Increasing your policy limits can offer better financial protection and peace of mind. Understanding where your coverage ends helps avoid potentially devastating out-of-pocket expenses.

| Term | Definition | Why It Matters |

|---|---|---|

| Premium | The regular payment made to keep the insurance policy active. | Higher coverage or risk factors can increase your premium, affecting your monthly budget. |

| Deductible | The amount you pay out of pocket before insurance covers a claim. | Choosing a higher deductible lowers premiums but increases costs during claims. |

| Policy Limits | The maximum amount the insurer will pay for a covered loss. | Exceeding policy limits means you’re responsible for the remaining expenses. |

| Liability Coverage | Covers costs if you're at fault in an accident involving injury or property damage. | Required in most states and essential for protecting against lawsuits. |

| Comprehensive Coverage | Covers non-collision incidents like theft, fire, or natural disasters. | Protects your vehicle from a wide range of unpredictable risks. |

Understanding Auto Insurance Policy Terms: A Comprehensive Guide

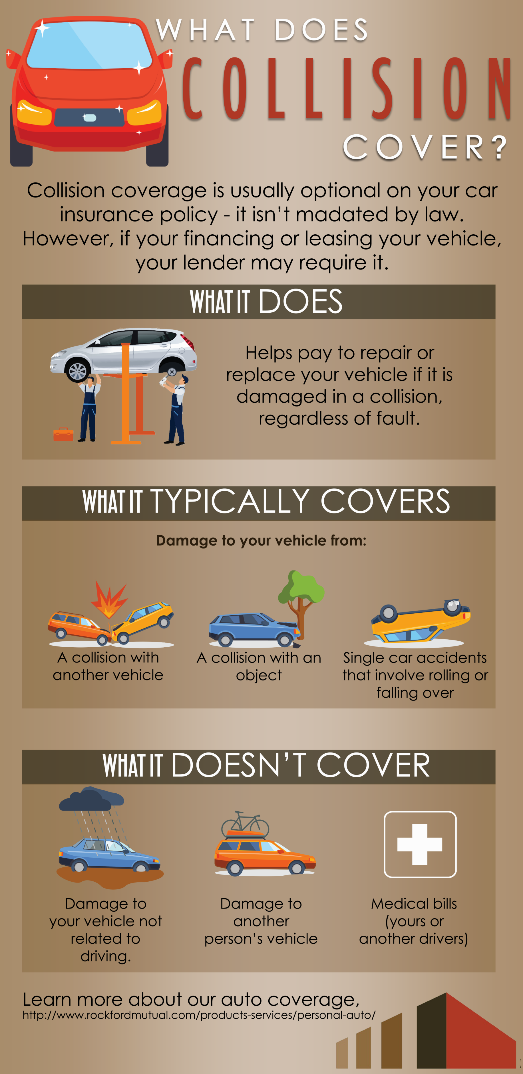

Do I need comprehensive and collision coverage in my auto insurance policy?

What Are Comprehensive and Collision Coverage?

Comprehensive and collision coverage are two optional components of an auto insurance policy that provide financial protection for damage to your own vehicle. While most states only require liability insurance, these additional coverages help cover repair or replacement costs when your car is damaged, regardless of who is at fault.

- Collision coverage pays for damage to your car resulting from an accident with another vehicle or object, such as hitting a tree or a guardrail.

- Comprehensive coverage, sometimes called other than collision, covers non-accident-related damages like theft, vandalism, fire, falling objects, natural disasters, and animal-related incidents.

- Unlike liability coverage, both comprehensive and collision are optional if you own your car outright, but they may be required by lenders or leasing companies.

When Should You Consider Dropping Comprehensive and Collision Coverage?

There are specific financial and practical circumstances under which maintaining comprehensive and collision coverage may no longer be cost-effective. As vehicles age and depreciate in value, the cost of these coverages might outweigh the potential benefits.

- One key factor is the actual cash value of your car; if the annual premium for both coverages totals more than 10% of your car’s current market value, it might be time to reconsider.

- Another consideration is your personal financial ability to absorb repair or replacement costs; if you can comfortably afford to pay for vehicle damages out of pocket, the coverage may not be necessary.

- Vehicles that are older or have high mileage often do not justify the cost of these coverages, especially if extensive repairs would exceed the car’s worth.

When Is It Wise to Keep Comprehensive and Collision Coverage?

Retaining comprehensive and collision coverage is generally advisable when your vehicle holds significant value or when financial protection is critical in the event of an accident or unexpected incident. This is especially true if replacing your car would be a financial burden.

- If your vehicle is relatively new, financed, or leased, lenders typically require both coverages to protect their investment.

- Living in areas prone to extreme weather, high rates of theft, or frequent animal collisions increases the risk of damage, making comprehensive and collision coverage more valuable.

- Drivers who use their cars frequently or in high-risk environments benefit from the added protection these coverages offer, helping avoid large out-of-pocket expenses after an incident.

What are key terms to know in an auto insurance policy?

Coverage Types in Auto Insurance Policies

Understanding the different types of coverage included in an auto insurance policy is essential for making informed decisions. Each type of coverage protects against specific scenarios and financial risks related to vehicle ownership and operation. Knowing what each provides helps policyholders select appropriate limits and avoid unexpected out-of-pocket expenses.

- Liability Coverage – This includes both bodily injury liability and property damage liability. It pays for injuries or damage you cause to others in an at-fault accident and is required by law in most states.

- Collision Coverage – This pays for repairs or replacement of your vehicle if it’s damaged in a collision with another vehicle or object, regardless of fault.

- Comprehensive Coverage – Also known as other than collision coverage, it covers non-collision incidents such as theft, vandalism, fire, natural disasters, or hitting an animal.

Key Policy Limits and Deductibles

Policy limits and deductibles directly influence how much you pay in premiums and how much financial protection you receive after a claim. These terms define the maximum amount your insurer will pay and your initial out-of-pocket cost before coverage applies.

- Policy Limits – These are the maximum amounts your insurance company will pay for a covered loss, typically listed in dollar amounts per incident. For example, a liability limit written as 100/300/100 means $100,000 per person for bodily injury, $300,000 per accident for bodily injury, and $100,000 for property damage.

- Deductibles – This is the amount you must pay out of pocket before your insurance coverage kicks in. Higher deductibles generally mean lower premiums, but also higher out-of-pocket costs when filing a claim.

- Split vs. Combined Limits – Some policies use split limits (separate amounts for different types of liability) while others use a single combined limit that covers all damages up to a total amount.

Additional Terms Affecting Your Policy

Beyond coverage and limits, several other terms influence how your auto insurance policy functions, including eligibility for discounts, claim processing, and potential premium adjustments. Familiarity with these terms helps policyholders manage costs and understand their responsibilities.

- Personal Injury Protection (PIP) – Also called no-fault coverage, PIP helps pay for medical expenses, lost wages, and other costs for you and your passengers, regardless of who caused the accident. It is mandatory in some states.

- Uninsured/Underinsured Motorist Coverage – This covers your damages and injuries if you're in an accident with a driver who has no insurance or insufficient coverage to pay for your losses.

- Endorsements or Riders – These are optional additions to a policy that customize coverage, such as rental reimbursement, roadside assistance, or gap insurance for leased or financed vehicles.

Frequently Asked Questions

What does an auto insurance policy typically cover?

An auto insurance policy typically covers liability for bodily injury and property damage, collision and comprehensive damage to your vehicle, and medical payments or personal injury protection. It may also include uninsured/underinsured motorist coverage. Coverage specifics vary by state and provider, so it's important to review your policy details. Optional coverages like rental reimbursement or roadside assistance can also be added based on individual needs.

What is the minimum required auto insurance coverage?

The minimum required auto insurance coverage varies by state but generally includes liability insurance for bodily injury and property damage. This covers costs if you're at fault in an accident. Some states also require personal injury protection or uninsured motorist coverage. While minimum coverage meets legal requirements, it may not provide sufficient protection in serious accidents. Drivers should consider higher limits or additional coverage for better financial security.

How does a deductible work in auto insurance?

A deductible is the amount you pay out of pocket before your insurance coverage kicks in for a claim. For example, with a $500 deductible and $3,000 in damages, you pay $500 and the insurer covers $2,500. Higher deductibles usually mean lower premiums, but you'll pay more when filing a claim. Deductibles apply to collision and comprehensive coverage, not liability. Choose a deductible amount you can afford in case of an accident.

Can my auto insurance policy be canceled for a traffic violation?

Yes, your auto insurance policy can be canceled or not renewed due to serious or repeated traffic violations, such as DUIs, reckless driving, or multiple speeding tickets. Insurers view these as higher risk, which may lead to cancellation or increased premiums. While a single minor violation typically won't result in cancellation, it could affect your rates. Always check with your provider about their specific policies regarding violations and risk assessment.

Leave a Reply