Auto Insurance Sd

Auto insurance in South Dakota is a legal requirement for all drivers, designed to provide financial protection in the event of accidents, property damage, or injuries.

The state follows a traditional at-fault system, where the driver responsible for a collision is held liable for resulting damages. South Dakota mandates minimum coverage levels, including bodily injury and property damage liability, ensuring drivers can cover third-party claims.

While these minimums offer basic protection, many residents opt for additional coverage such as uninsured motorist protection, comprehensive, and collision insurance for greater security. Insurance rates vary based on factors like driving history, vehicle type, and location.

Fort worth home insurance cost

Fort worth home insurance costUnderstanding Auto Insurance in South Dakota: Coverage and Requirements

Auto insurance in South Dakota is regulated by the state's Division of Insurance and is mandatory for all drivers operating a vehicle on public roads. South Dakota follows an at-fault (tort) system, meaning the driver who causes an accident is responsible for covering the damages and injuries.

The state requires all drivers to carry minimum liability insurance coverage to ensure financial responsibility in the event of a crash. These minimum requirements include $25,000 for bodily injury per person, $50,000 for bodily injury per accident, and $25,000 for property damage per accident (commonly referred to as 25/50/25). Drivers must be able to provide proof of insurance upon request during traffic stops, vehicle registration, or after an accident.

Failure to maintain insurance can result in fines, license suspension, or even vehicle impoundment. In addition to liability coverage, drivers may opt for optional protections such as comprehensive, collision, personal injury protection (PIP), and uninsured/underinsured motorist coverage to enhance their policy and provide broader financial security.

Minimum Insurance Requirements in South Dakota

South Dakota law mandates that all vehicle owners hold a minimum level of liability coverage to legally operate a vehicle.

Geico home insurance reviews 2025

Geico home insurance reviews 2025This includes $25,000 in coverage for injuries per person, $50,000 per accident for total injuries, and $25,000 for property damage, collectively known as the 25/50/25 rule. These amounts are the legal minimum, but they may not fully cover expenses after a serious accident, prompting many drivers to purchase higher limits.

The state also requires insurance companies to offer uninsured motorist coverage, although drivers can reject it in writing. Proof of insurance must be carried at all times while driving, and insurers are required to report policy status to the Department of Motor Vehicles (DMV), ensuring accountability and reducing the number of uninsured drivers on the road.

Factors That Affect Auto Insurance Rates in South Dakota

Several variables influence the cost of auto insurance premiums in South Dakota, including the driver’s age, driving record, location, vehicle type, and credit history.

Younger and inexperienced drivers typically face higher premiums due to increased risk, while those with a history of accidents or traffic violations may also see rate increases. Urban areas such as Sioux Falls and Rapid City often have higher premiums due to increased traffic density and accident rates.

Quote home and auto insurance

Quote home and auto insuranceInsurers also consider annual mileage and how the vehicle is used (e.g., commuting vs. pleasure). Additionally, credit-based insurance scores are commonly used in rate determination, as statistical data show a correlation between creditworthiness and claim likelihood. Shopping around and comparing quotes can help drivers find the most competitive rates based on their individual profiles.

Optional Coverages and Endorsements for South Dakota Drivers

While South Dakota only requires liability insurance, drivers are encouraged to consider additional coverages for more comprehensive protection. Comprehensive and collision coverage help pay for vehicle repairs due to accidents, theft, vandalism, or natural events.

Personal Injury Protection (PIP), though not mandatory, can cover medical expenses, lost wages, and other related costs regardless of fault. Uninsured/underinsured motorist coverage is particularly valuable in protecting against drivers who lack sufficient insurance.

Additional endorsements like rental reimbursement, roadside assistance, and gap insurance can further enhance a policy. These options allow South Dakota drivers to customize their insurance plans according to their needs, offering greater financial security in diverse accident scenarios.

Walmart home insurance phone number

Walmart home insurance phone number| Coverage Type | Minimum Requirement in South Dakota | Description |

|---|---|---|

| Bodily Injury Liability (per person) | $25,000 | Covers medical expenses for others injured in an accident you cause. |

| Bodily Injury Liability (per accident) | $50,000 | Pays up to $50,000 total for all injuries in a single accident. |

| Property Damage Liability | $25,000 | Covers repair or replacement costs for damaged property, such as vehicles or structures. |

| Uninsured Motorist Coverage | Offered (opt-out available) | Protects you if hit by a driver with no or insufficient insurance. |

| Comprehensive & Collision | Optional | Covers damage to your vehicle from accidents, theft, weather, or other non-collision events. |

Comprehensive Guide to Auto Insurance in South Dakota: Coverage Options and Requirements

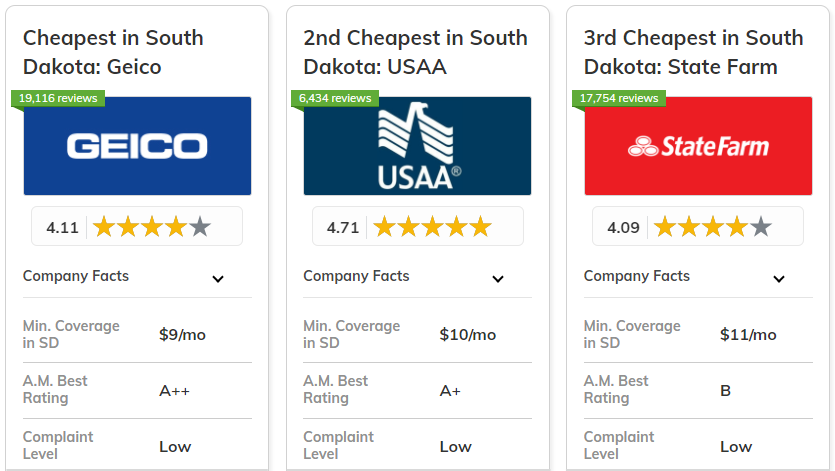

What is the most affordable auto insurance in South Dakota?

The most affordable auto insurance in South Dakota varies depending on individual factors such as driving history, age, vehicle type, and coverage needs. However, among the providers consistently offering competitive rates statewide, companies like State Farm, USAA (for military members and their families), and Farmers Insurance frequently rank as some of the most budget-friendly options.

According to data from sources like NerdWallet and Bankrate, State Farm generally offers the lowest average premiums for minimum and full coverage in South Dakota. It's important to note that while cost is a major factor, policyholders should also evaluate customer service ratings, coverage options, and financial stability when selecting an insurer.

Factors That Influence Auto Insurance Rates in South Dakota

- Driving Record: A clean driving history significantly lowers insurance premiums, as insurers view drivers with fewer accidents or violations as lower risks. In South Dakota, a single at-fault accident or traffic ticket can increase rates substantially depending on the provider.

- Credit Score: Most insurers in the state use credit-based insurance scores to determine premiums. Drivers with higher credit scores typically qualify for lower rates, while poor credit may lead to higher quotes, even for otherwise responsible drivers.

- Location and Mileage: Urban areas like Sioux Falls or Rapid City often have higher premiums due to increased traffic density and accident risks. Additionally, the more miles driven annually, the higher the chances of an accident, which can raise insurance costs.

Top Low-Cost Auto Insurance Providers in South Dakota

- State Farm: Known for offering some of the most competitive rates in South Dakota, State Farm benefits from an extensive network of local agents and tailored discounts such as safe driver, multi-policy, and good student programs.

- USAA: Exclusively available to active military members, veterans, and their families, USAA regularly provides the lowest premiums in the state. Its strong customer satisfaction and comprehensive coverage make it a top choice for eligible drivers.

- Farmers Insurance: Offering a blend of affordability and flexible policy options, Farmers is especially popular in rural areas. It provides unique discounts for bundling home and auto policies and maintaining continuous coverage.

How to Save More on Auto Insurance in South Dakota

- Compare Quotes Regularly: Rates can vary dramatically between insurers. Using online comparison tools to review quotes from at least three providers annually ensures you're getting the best deal available based on your current profile.

- Take Advantage of Discounts: Many companies offer premium reductions for defensive driving courses, vehicle safety features, low annual mileage, and electronic billing. Always ask insurers about available discounts when getting a quote.

- Adjust Coverage Levels Wisely: While South Dakota requires only minimum liability coverage (25/50/25), slightly increasing liability limits or opting for higher deductibles on comprehensive and collision can enhance protection without drastically increasing costs.

What factors determine the lowest auto insurance rates in South Dakota?

Driver Profile and Personal Characteristics

Insurance providers in South Dakota evaluate numerous personal attributes of the driver when calculating premiums. These characteristics significantly influence the perceived risk of insuring an individual, thus impacting the final cost of coverage.

- Age and driving experience play a crucial role, with younger and less experienced drivers typically facing higher premiums due to statistically higher accident rates, while older, more experienced drivers often benefit from lower rates.

- Gender can be a factor, as insurers may consider statistical trends showing differences in accident frequency and claim severity between male and female drivers, although this varies by company and is not universally applied.

- A clean driving record with no accidents, traffic violations, or DUI offenses results in more favorable rates, as it demonstrates responsible driving behavior and reduced risk to the insurer.

Vehicle Type and Usage Patterns

The kind of vehicle driven and how it is used on a daily basis contribute heavily to insurance costs in South Dakota. Insurers assess risk based on the potential repair costs, safety features, and likelihood of theft or accidents associated with a specific vehicle.

- Cars with higher market values, powerful engines, or those frequently targeted by thieves tend to have higher premiums, while reliable, low-performance, and widely owned models usually come with lower insurance costs.

- The annual number of miles driven is factored in; individuals who drive less—such as those with short commutes or who work from home—often receive lower rates due to reduced exposure to accidents.

- Using a vehicle for business purposes or ridesharing may increase premiums compared to personal use, as commercial driving generally presents greater risk and more time on the road.

Location and Coverage Selection

Where a policyholder lives within South Dakota and the types of coverage they choose are fundamental in determining auto insurance affordability. Geographic and policy design elements directly affect risk exposure and claim potential.

- Urban areas like Sioux Falls or Rapid City tend to have higher insurance rates due to increased traffic density, higher accident frequency, and greater risk of theft or vandalism compared to rural regions with lower population and traffic volume.

- Choosing higher deductibles lowers monthly premiums, as the policyholder assumes more financial responsibility in the event of a claim, reducing the insurer’s immediate payout risk.

- Opting for only state-minimum liability coverage can yield the lowest rates, but drivers selecting additional protections like comprehensive, collision, or uninsured motorist coverage will see higher premiums based on the expanded scope of protection.

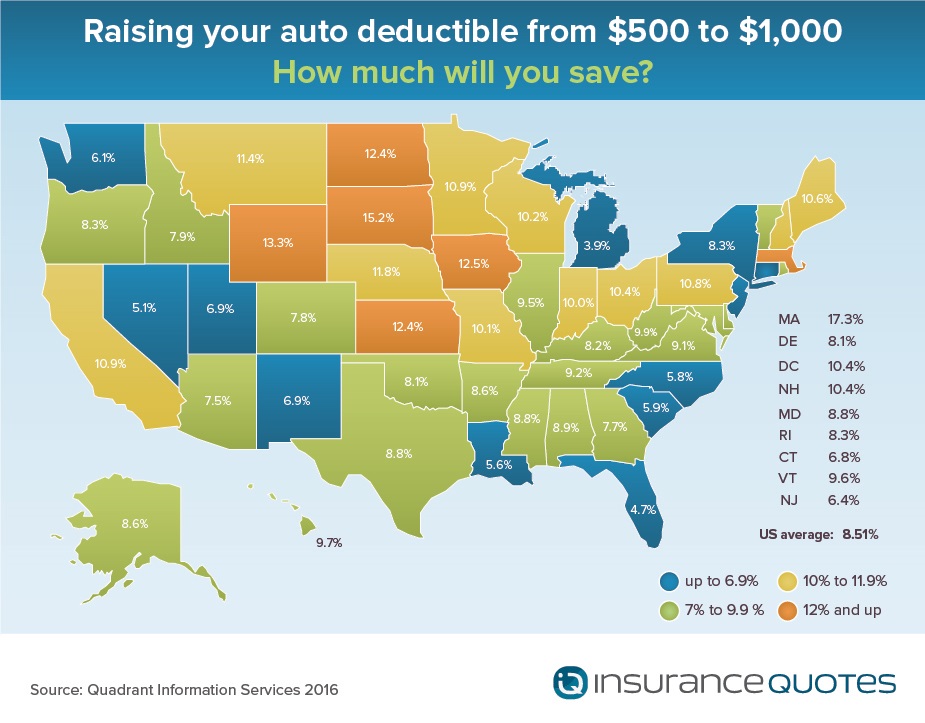

Is a $500 or $1,000 deductible more cost-effective for auto insurance in SD?

Average Auto Insurance Costs with $500 vs $1,000 Deductibles in South Dakota

- On average, South Dakota drivers who choose a $1,000 deductible pay lower monthly premiums compared to those with a $500 deductible. The difference can range from $10 to $25 per month depending on the insurer, driving history, and vehicle type. This reduction occurs because insurers assume less financial risk when policyholders agree to cover more out-of-pocket costs in the event of a claim.

- For a driver with a clean record insuring a mid-range sedan, a policy with a $500 deductible may cost approximately $1,200 annually, whereas switching to a $1,000 deductible could reduce the total to around $1,050 per year. While this represents a 12.5% decrease in the premium, it also means the driver must be prepared to pay an additional $500 in the event of a claim.

- It’s important to consider that these savings accumulate over time, but they only become cost-effective if the policyholder avoids filing claims. Drivers who frequently file comprehensive or collision claims may end up paying more overall due to the higher out-of-pocket expense each time, negating the annual premium savings.

Claim Frequency and Financial Risk in South Dakota

- South Dakota experiences moderate rates of auto insurance claims, influenced by winter driving conditions, rural roadways, and wildlife collisions—particularly with deer. These factors make claim frequency higher than in some neighboring states, which affects the practicality of choosing a higher deductible.

- Drivers who face a higher likelihood of filing a claim—such as those who commute long distances or live in areas with frequent ice and snow—might find a $500 deductible more practical. The lower out-of-pocket cost after an accident can prevent financial strain, especially if multiple incidents occur over time.

- Conversely, safe drivers with several years of accident-free history and an emergency fund may benefit more from a $1,000 deductible. By covering minor damages out of pocket, they avoid claim filings that could trigger premium increases, while also enjoying lower base rates over the long term.

Long-Term Savings vs Immediate Out-of-Pocket Costs

- Selecting a $1,000 deductible offers greater long-term savings potential for drivers who do not anticipate needing to file collision or comprehensive claims. Over a 5-year period, the accumulated premium savings could exceed $900, making the higher deductible financially advantageous if no claims are made.

- However, if a driver with a $1,000 deductible experiences even one at-fault accident requiring $3,000 in repairs, they pay $1,000 upfront versus $500 with the lower deductible. This results in $500 more in immediate expenses, which may be burdensome without accessible savings.

- The decision ultimately hinges on individual financial stability. Drivers with reliable savings should consider the $1,000 deductible to maximize savings over time. In contrast, those living paycheck to paycheck may find a $500 deductible more manageable, avoiding potential debt or delays in vehicle repairs after an incident.

Frequently Asked Questions

What does Auto Insurance SD cover?

Auto Insurance SD covers damages and liabilities resulting from car accidents, including bodily injury, property damage, and medical expenses. It also offers protection against theft, vandalism, and natural disasters if comprehensive coverage is included. Policies can be customized with additional options like roadside assistance and rental reimbursement, ensuring drivers in South Dakota have flexible, reliable protection tailored to their needs and budget.

Is auto insurance mandatory in South Dakota?

Yes, auto insurance is mandatory in South Dakota. Drivers must carry minimum liability coverage, including $25,000 for bodily injury per person, $50,000 per accident, and $25,000 for property damage.

Proof of insurance must be carried at all times while driving. Failing to maintain valid coverage can result in fines, license suspension, or vehicle registration cancellation, making it essential to stay insured to comply with state laws and avoid penalties.

You can lower your auto insurance premium in South Dakota by maintaining a clean driving record, bundling policies, and taking advantage of discounts for safety features or defensive driving courses.

Increasing your deductible can also reduce costs, though it raises out-of-pocket expenses after a claim. Comparing quotes from multiple insurers and adjusting coverage based on your vehicle’s value helps ensure you’re getting the most affordable, suitable rate available.

What should I do after a car accident in South Dakota?

After a car accident in South Dakota, ensure everyone’s safety and call emergency services if needed. Exchange insurance and contact information with the other driver, take photos, and gather witness statements if possible.

Report the accident to your insurer promptly to start the claims process. South Dakota is a fault-based state, so determining liability is crucial. Cooperate with your insurer and keep records of all related expenses and communications.

Leave a Reply