Best Auto Insurance In Michigan Finance

Choosing the best auto insurance in Michigan requires careful consideration of coverage options, pricing, and financial stability. As one of the few states with no-fault insurance, Michigan mandates personal injury protection, making it essential for drivers to understand how policies impact their finances. With some of the highest auto insurance rates in the nation, finding affordable yet comprehensive coverage is a priority for residents. Top providers balance competitive premiums, strong customer service, and flexibility in payment options. This guide explores leading insurers in Michigan, evaluating their value, financial strength, and ability to meet the unique demands of the state’s auto insurance landscape.

Top Auto Insurance Providers for Michigan Drivers: Financial Safety and Coverage Options

Choosing the best auto insurance in Michigan involves more than simple price comparisons—it requires a deep understanding of financial stability, coverage benefits, and state-specific regulations. Michigan has long followed a no-fault insurance system with unique provisions, including unlimited personal injury protection (PIP) as a mandatory coverage, though recent reforms allow residents to choose lower limits based on their healthcare coverage. This shift has made it essential for drivers to evaluate insurers not only by premium costs but also by their ability to provide strong financial protection, fast claims processing, and flexible plans tailored to Michigan’s complex legal framework. Leading providers such as Michigan Citizens Insurance Agency, Erie Insurance, and Auto-Owners stand out due to their high financial strength ratings, consistent customer satisfaction, and strong local presence. When assessing the best options, policyholders must weigh affordability against reliability, ensuring coverage aligns with both legal requirements and personal financial risk.

Understanding Michigan’s Unique No-Fault Insurance System

Michigan's no-fault insurance model differs significantly from other states, primarily due to its lifetime personal injury protection (PIP) coverage, which historically paid for unlimited medical expenses resulting from auto accidents. While reforms enacted in 2019 now allow drivers to choose lower PIP limits—from $250,000 to $50,000 or even opting out with proof of qualified health insurance—the core principle of prioritizing medical cost coverage over legal fault remains. This system is designed to ensure that injured drivers receive prompt medical care regardless of who caused the crash, but it has contributed to some of the highest auto insurance premiums in the nation. Understanding this framework is critical when selecting a policy, as it influences both coverage scope and long-term financial exposure. Consumers should carefully review how different insurers handle PIP claims, coordinate benefits with health insurance, and support retroactive changes under the new law.

Best homeowner insurance for luxury homes

Best homeowner insurance for luxury homesTop-Rated Insurance Companies for Financial Strength and Customer Service

When selecting the best auto insurance in Michigan, financial stability and customer service quality are as important as premium rates. Insurers like Erie Insurance consistently earn top marks from AM Best for their excellent financial strength (rated A+) and high JD Power satisfaction scores. Similarly, Auto-Owners Insurance is renowned for its personalized service and stable pricing, particularly valuable in a market prone to fluctuation. State Farm and Progressive also rank highly due to extensive digital tools, broad coverage options, and strong claims handling networks. Michigan drivers should look for insurers that not only offer competitive pricing but also demonstrate reliability during claims events, especially given the state’s history of high bodily injury costs. A company’s ability to pay large medical claims without financial strain is a key factor in long-term policyholder security.

Factors That Influence Auto Insurance Rates Across Michigan Cities

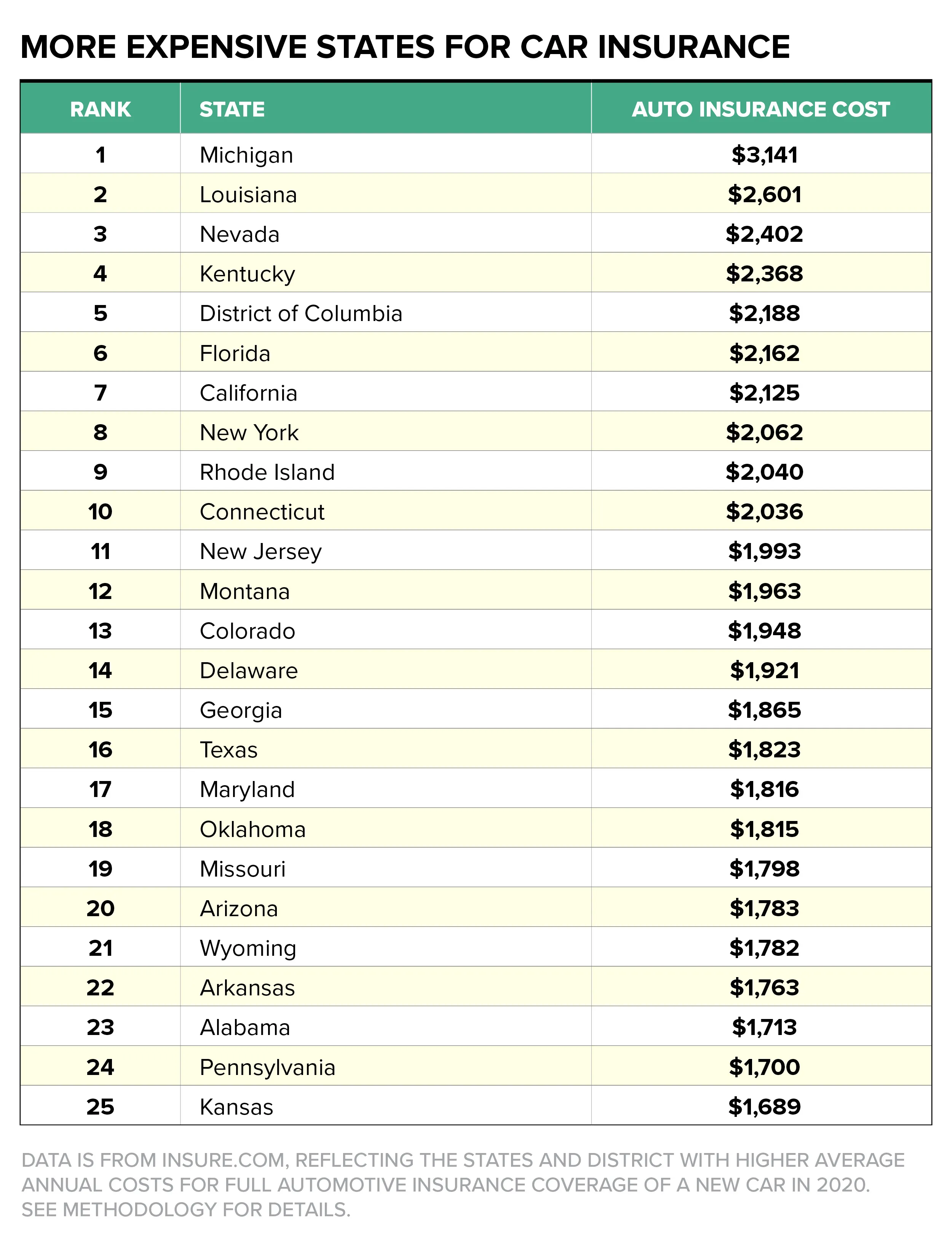

Auto insurance premiums in Michigan vary significantly depending on location, with urban areas such as Detroit, Flint, and Lansing typically facing higher costs due to elevated rates of accidents, theft, and insurance fraud. Insurers consider local crime statistics, traffic congestion, and even ZIP code-specific claims history when setting rates. For example, a driver in Ann Arbor may pay substantially less than an identical driver just 30 miles away in Highland Park, despite similar driving records. Other key rate factors include the driver’s age, credit score, vehicle type, and claims history. Bundling policies, maintaining continuous coverage, and qualifying for usage-based discounts (such as safe driving programs via mobile apps) can help mitigate these regional disparities. By understanding how these variables impact pricing, Michigan residents can make more informed decisions and potentially lower their annual insurance expenses while maintaining robust protection.

| Insurance Provider | AM Best Financial Rating | Avg. Annual Premium in Michigan | Notable Features |

|---|---|---|---|

| Erie Insurance | A+ (Excellent) | $2,400 | Low rate increases, lifetime loyalty rewards, strong local agents |

| Auto-Owners Insurance | A++ (Superior) | $2,600 | Personalized service, multiple discount options, high stability |

| State Farm | A++ (Superior) | $2,800 | Extensive agent network, mobile claims support, bundling discounts |

| Progressive | A+ (Excellent) | $3,100 | Snapshot usage-based program, price comparison tool, 24/7 claims |

| Michigan Citizens (Reinsurance Group) | B++ (Good) | $4,500+ | Assigned-risk provider, last-resort option, higher premiums |

Best Auto Insurance Options in Michigan: A Comprehensive Financial Guide

What is the best auto insurance in Michigan for competitive rates and financial reliability?

Top Auto Insurance Providers in Michigan for Competitive Rates

- State Farm is consistently recognized for offering some of the most competitive auto insurance rates in Michigan. With a broad network of local agents and customizable policy options, State Farm provides tailored coverage that fits various driver profiles, including those with clean records and those managing past infractions. Their usage-based program, Drive Safe & Save, allows Michigan drivers to reduce premiums by demonstrating safe driving habits through telematics.

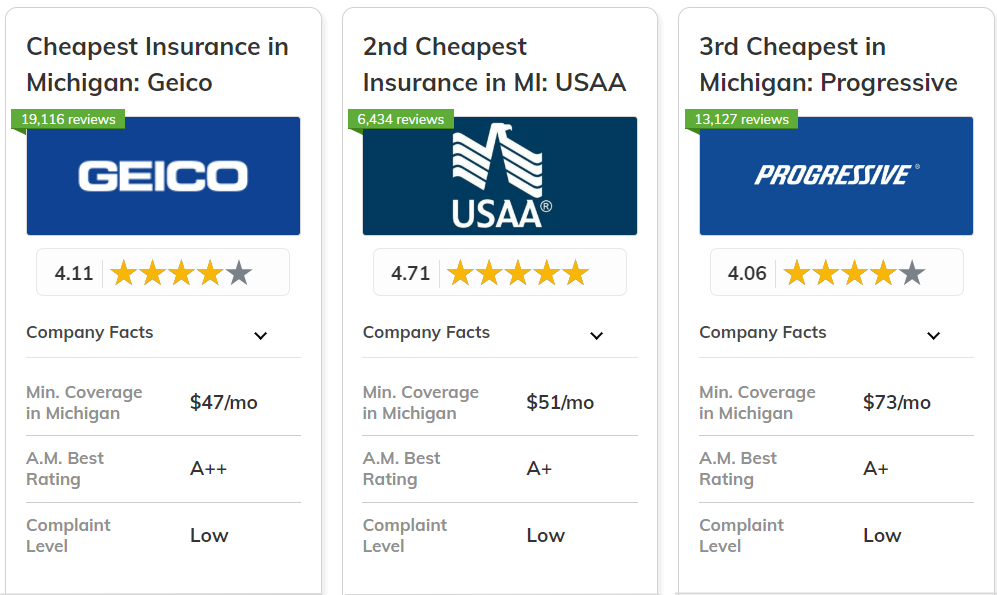

- Geico is another top choice for low-cost auto insurance in the state, appealing to budget-conscious drivers. Its online tools and mobile app make it easy to compare quotes and manage policies. Geico often features exclusive discounts for Michigan residents, such as multi-policy, good student, and federal employee discounts, contributing to its reputation for affordability.

- Progressive stands out due to its price comparison tool, Snapshot, which helps drivers find the most cost-effective rates based on actual driving behavior. The company frequently offers competitive bundled policies and has strong customer satisfaction ratings for transparency in pricing, making it a reliable option for Michigan residents seeking both value and flexibility.

Financial Reliability and Rating Agencies' Insights for Michigan Insurers

- When assessing financial reliability, it's important to consult ratings from agencies like AM Best, Standard & Poor's, and Moody's. Insurers such as Auto-Owners and USAA maintain 'A++' ratings from AM Best, indicating exceptional financial strength and their ability to meet policyholder obligations, even during economic downturns. These ratings are crucial for Michigan drivers who want assurance their insurer will be there when claims arise.

- Esurance, a subsidiary of Allstate, also holds solid financial ratings and offers transparent claims processes, which is a key indicator of reliability. Its digital-first approach ensures fast service and efficient claim settlements, backed by the financial stability of its parent company. This combination makes Esurance an excellent blend of innovation and trustworthiness.

- Michigan Basic Perfection insurance policies require certain minimum coverages, including unlimited personal injury protection (PIP), making insurer stability especially important. Companies like Frankenmuth Insurance have deep roots in the state and demonstrate long-term financial resilience, with consistent performance even in high-claim environments, ensuring they can support extensive medical payouts required under Michigan law.

Customer Satisfaction and Claims Experience in Michigan

- According to the J.D. Power U.S. Auto Insurance Study, Auto-Owners consistently receives high marks for customer satisfaction in the Midwest region, including Michigan. Drivers praise its agent responsiveness, straightforward claims filing, and minimal delays in settlements. Its regionally focused model allows for more personalized service compared to national giants.

- USAA, while limited to military members and their families, is frequently rated at the top for claims satisfaction. Michigan-based military families benefit from USAA’s fast claims processing, mobile claim reporting, and high first-contact resolution rates. The company's commitment to service aligns well with the complexities of Michigan’s no-fault insurance system.

- farmers insurance has invested heavily in improving its customer experience, particularly in claims support. Through its 24/7 claims hotline and GPS-assisted accident reporting, Farmers helps Michigan drivers get back on the road faster. Although historically seen as more expensive, its recent upgrades in digital tools and customer care have improved overall satisfaction scores significantly.

Is $300 Monthly a High Cost for Auto Insurance in Michigan?

Bundling home and auto insurance florida cost savings

Bundling home and auto insurance florida cost savingsYes, $300 per month for auto insurance in Michigan is considered a high cost, especially when compared to the national average, which is significantly lower. Michigan has historically had some of the most expensive auto insurance rates in the United States due to its unique no-fault insurance system, which guarantees unlimited personal injury protection (PIP) benefits to accident victims, regardless of fault. While recent reforms have made efforts to bring down premiums by allowing drivers to choose lower PIP coverage levels, many drivers still face high costs. At $3,600 annually, a $300 monthly rate exceeds both the state and national averages, indicating that this price point may be high for most drivers, particularly those with clean records or who live in low-risk areas.

Why Is Auto Insurance So Expensive in Michigan?

- Michigan’s no-fault insurance system previously mandated unlimited PIP coverage, leading to high medical billing and fraud, which significantly drove up premiums across the board.

- Urban areas like Detroit have high rates of uninsured drivers, vehicle theft, and accidents, increasing risk for insurers who pass those costs onto policyholders.

- Even after the 2019 auto insurance reforms that allowed tiered PIP coverage options, many drivers remain on older, more expensive plans or live in high-risk ZIP codes that keep premiums elevated.

How Does $300 Monthly Compare to Michigan's Average Insurance Rates?

- The average annual cost of auto insurance in Michigan is approximately $2,900, or about $240 per month, making $300 monthly notably above this benchmark.

- While some high-risk drivers or those with poor credit may pay rates around $300, most standard drivers with good records can often find policies well below this amount.

- Comparison shopping can reveal significant differences between insurers, and many residents are able to lower their premiums by switching companies or adjusting coverage levels after the no-fault reform.

- Drivers with past accidents, traffic violations, or DUI convictions are considered high-risk and typically face much higher premiums, potentially reaching or exceeding $300 per month.

- Carrying full coverage on luxury or high-performance vehicles can lead to increased premiums due to higher repair and replacement costs.

- Location plays a major role—residents in densely populated cities with high claim rates may see elevated prices, especially if they have not yet taken advantage of PIP coverage options introduced in recent reforms.

What is the most cost-effective auto insurance in Michigan for financial savings?

Top Affordable Auto Insurance Providers in Michigan

When seeking the most cost-effective auto insurance in Michigan, several providers consistently offer competitive rates without compromising essential coverage. These companies balance affordability with strong customer service and financial stability. Consumers often find savings through insurers like Auto-Owners, State Farm, and Frankenmuth Insurance, all of which maintain below-average premiums in the state. Michigan’s unique no-fault insurance system, which includes unlimited medical coverage by default, typically raises costs, making the choice of provider crucial for financial savings. By comparing quotes from multiple reputable insurers, drivers can identify policies that align with their budget while meeting legal requirements.

- Auto-Owners Insurance is frequently rated as one of the most affordable and reliable insurers in Michigan, offering personalized policies and multi-policy discounts.

- State Farm provides accessible pricing, especially for drivers with clean records, and offers various tools for managing policies online.

- Frankenmuth Insurance, a regional favorite, often delivers some of the lowest premiums in the state, particularly for low-risk drivers with strong credit histories.

Factors That Influence Auto Insurance Costs in Michigan

Understanding the variables that affect auto insurance premiums in Michigan is essential for finding the most cost-effective option. The state’s no-fault system, which mandates personal injury protection with unlimited medical benefits, is a major cost driver. However, recent reforms allow drivers to opt for lower PIP levels, directly reducing premiums. Other significant factors include driving history, credit score, location, type of vehicle, and annual mileage. Urban areas like Detroit often see higher rates due to increased accident and theft risks. Adjusting coverage limits and selecting higher deductibles can also lead to meaningful cost reductions.

Common issues with home insurance claims

Common issues with home insurance claims- Drivers who opt into lower Personal Injury Protection (PIP) tiers under Michigan’s no-fault reform can save hundreds annually on their premiums.

- A clean driving record free of accidents and violations significantly lowers insurance costs, as providers view these drivers as low risk.

- Insurers use credit-based insurance scores to determine rates, meaning maintaining good credit can directly result in lower monthly payments.

Money-Saving Strategies for Michigan Drivers

Michigan drivers can adopt various strategies to reduce their auto insurance expenses while still maintaining adequate protection. Proactively shopping for insurance every year allows consumers to capitalize on competitive offers and better deals. Bundling auto policies with home or renters insurance often triggers multi-policy discounts. Completing a defensive driving course may qualify drivers for additional reductions, especially those over 55. Taking advantage of usage-based insurance programs, which monitor driving behavior through mobile apps or devices, can also result in lower rates for safe driving habits.

- Annual comparison shopping ensures that drivers are not stuck with renewals at higher rates when cheaper options are available from other carriers.

- Choosing to bundle insurance policies with the same provider typically yields discounts of 10% to 25%, enhancing overall affordability.

- Enrolling in telematics programs like Progressive’s Snapshot or Allstate’s Drivewise rewards safe driving patterns with long-term premium reductions.

Frequently Asked Questions

What factors determine the best auto insurance rates in Michigan?

Your driving record, credit score, vehicle type, and coverage level influence auto insurance rates in Michigan. Insurers also consider your age, location, and annual mileage. Comparing quotes from multiple providers helps identify the best value. Michigan's no-fault system impacts pricing, so understanding personal injury protection (PIP) options is essential. Choosing higher deductibles and bundling policies may lower premiums while maintaining reliable coverage.

How does Michigan’s no-fault insurance system affect my coverage?

Michigan's no-fault insurance requires drivers to carry personal injury protection (PIP) coverage, which pays for medical expenses regardless of fault in an accident. This system aims to ensure prompt treatment and reduce lawsuits. While it increases coverage reliability, it can also raise premiums. Drivers can now choose lower PIP options to manage costs. Understanding your PIP selection is critical when choosing the best auto insurance plan for your financial needs.

Can I lower my auto insurance costs without sacrificing coverage?

Yes, you can reduce auto insurance costs in Michigan by increasing deductibles, maintaining a clean driving record, and qualifying for discounts like safe driver or multi-policy bundles. Opting for a lower PIP level under Michigan’s reformed no-fault law also helps. Comparing quotes regularly ensures you’re getting competitive rates. Ensuring adequate liability and collision coverage protects your finances while keeping overall premiums affordable and sustainable.

Compare san antonio home insurance

Compare san antonio home insuranceWhich auto insurance companies offer the best value in Michigan?

Top insurers in Michigan include State Farm, Geico, Auto-Owners, and Frankenmuth Insurance, known for competitive rates and strong customer service. Frankenmuth often ranks highest for overall value due to lower premiums and local expertise. When selecting a provider, evaluate not only price but also claims satisfaction, financial strength, and available discounts. Reading customer reviews and checking ratings from sources like J.D. Power helps identify the best balance of cost and service.

Leave a Reply