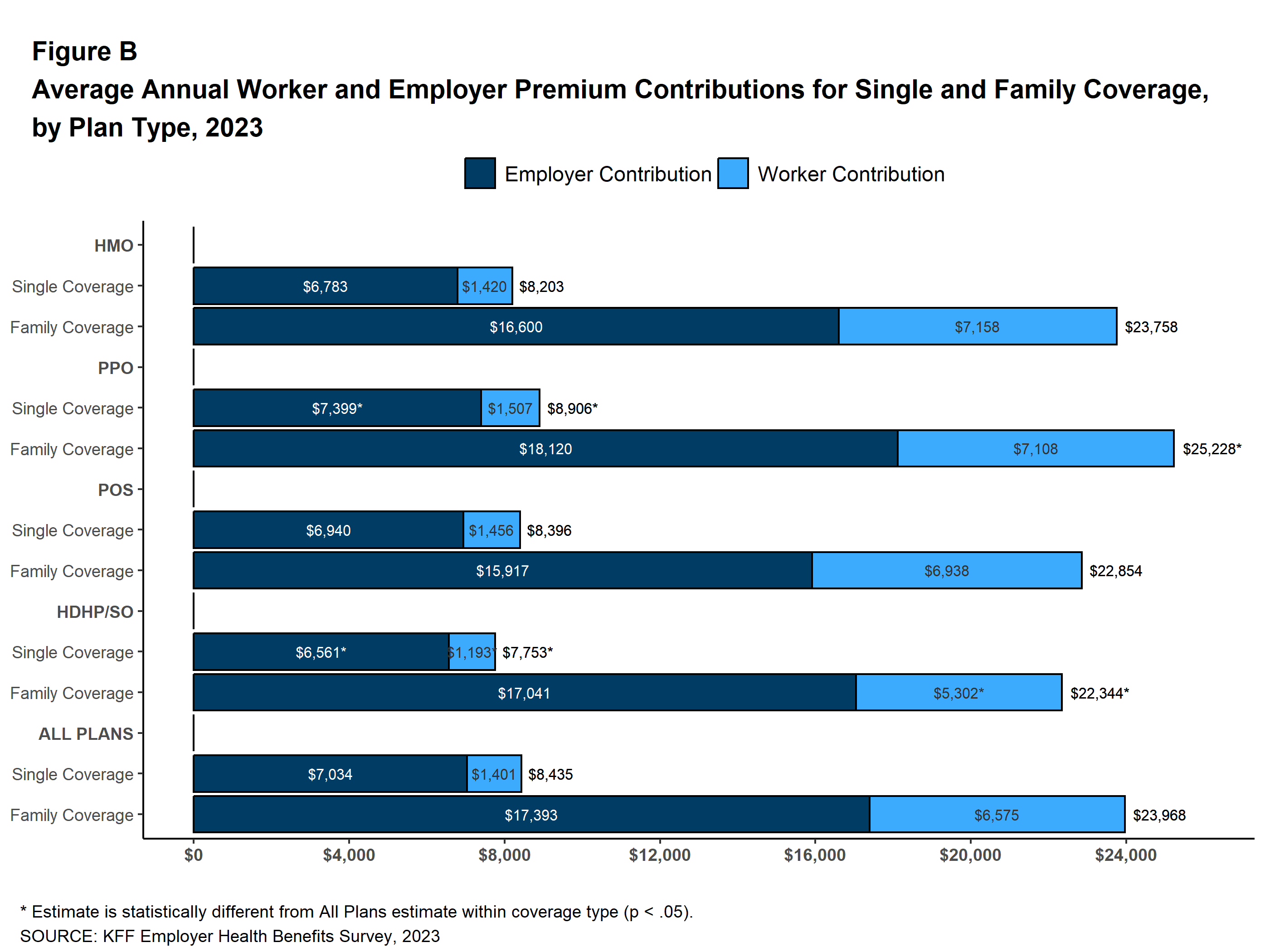

Cobra Cost Health Insurance

Health insurance costs continue to strain household budgets across the United States, with premiums, deductibles, and out-of-pocket expenses rising steadily year after year. Among the various factors driving these increases, the Cobra Cost Health Insurance program remains a significant concern for many Americans.

Designed to allow individuals to maintain their employer-sponsored coverage after job loss, COBRA often comes with steep price tags, making it unaffordable for some. This article explores the true cost of COBRA, how it compares to other insurance options, and the financial implications for those forced to rely on it during transitional periods in their lives.

Understanding the True Cost of COBRA Health Insurance

The Consolidated Omnibus Budget Reconciliation Act (COBRA) allows former employees, retirees, and their dependents to continue their employer-sponsored health coverage after job loss, reduction in hours, or other qualifying life events. While COBRA provides a valuable safety net, the cost can be a major consideration for individuals.

Where To Find Cheap Auto Insurance

Where To Find Cheap Auto InsuranceUnlike active employees who typically share premium costs with their employer, COBRA participants are responsible for paying the full premium, plus up to a 2% administrative fee. This often leads to significantly higher monthly payments, sometimes exceeding $500 to over $1,200 depending on coverage level and location.

Although COBRA ensures continuity of care, network access, and avoids coverage gaps, its expense may make it unsustainable for some, prompting exploration of alternatives like marketplace plans through the ACA or spousal coverage.

What Determines the Cost of COBRA Coverage?

Several key factors influence the total COBRA cost, with the most significant being the type of health plan previously held (e.g., single, family, or multi-state coverage) and the geographic region where the individual resides.

The base premium reflects the full cost that the employer was paying for the health insurance policy, as COBRA requires participants to cover the entire amount. Employers are no longer subsidizing a portion of the premium for former employees, so someone who previously paid only 25% of a $800 monthly premium as an active worker could now face a COBRA bill of $800 plus a 2% administrative surcharge.

21 St Auto Insurance

21 St Auto InsuranceAdditionally, if the employer offers multiple plan options, the cost will vary accordingly, and individuals must choose a plan they were enrolled in prior to the qualifying event. Rates can also fluctuate if the employer adjusts its group health plan pricing annually, meaning the COBRA cost may increase even during a single continuation period.

How COBRA Compares to Marketplace and Other Insurance Options

When evaluating COBRA cost vs. alternatives, prospective participants should compare it to health plans available through the Health Insurance Marketplace.

One of the main advantages of marketplace plans is the potential eligibility for premium tax credits and cost-sharing reductions, which can drastically lower monthly payments and out-of-pocket costs—benefits not available with COBRA.

A person with lower post-employment income might qualify for substantial subsidies under the Affordable Care Act (ACA), making a marketplace plan more affordable than COBRA, even if the latter offers identical network access. Additionally, Medicaid may be an option for those with very low income.

Aarp Auto Insurance Reviews Finance

Aarp Auto Insurance Reviews FinanceWhile COBRA offers continuity of care with existing doctors and ongoing medical treatments, the financial burden is typically greater, so individuals must weigh network stability against long-term affordability when making a decision.

Duration and Payment Responsibilities Under COBRA

COBRA coverage can last up to 18 months for employees who leave their job voluntarily or involuntarily (excluding gross misconduct), and in certain cases such as disability or a dependent child aging out, coverage can be extended to 29 or 36 months respectively.

During this period, the former employee must make timely premium payments directly to the employer or plan administrator, usually within a 45-day initial payment window after electing COBRA. Subsequent payments are due monthly, and late payments beyond a 30-day grace period can result in permanent termination of coverage.

Because the individual is now responsible for the entire insurance premium, budgeting is essential, especially during transitional phases of employment. Employers are required to provide detailed election notices, but it is the participant’s responsibility to understand billing schedules, payment methods, and coverage details to avoid unintended lapses.

Aig Auto Insurance Reviews

Aig Auto Insurance Reviews| Plan Type | Average Monthly Cost (Employee Only) | Average Monthly Cost (Family) | Employer Subsidy? | Subsidies Available? |

|---|---|---|---|---|

| COBRA | $500 – $750 | $1,200 – $2,000+ | No – participant pays full premium | No – not eligible for tax credits |

| ACA Marketplace (Bronze) | $300 – $600 (before subsidies) | $900 – $1,800 (before subsidies) | N/A | Yes – based on income |

| Medicaid | $0 – $50 | $0 – $100 | N/A | Yes – for low-income individuals |

Comprehensive Guide to COBRA Health Insurance Costs and Coverage Options

What is the average monthly cost of COBRA health insurance?

The average monthly cost of COBRA health insurance in the United States typically ranges from $400 to $700 per month, though this amount can vary significantly depending on the specific health plan, geographic location, number of people covered, and the percentage of premiums previously subsidized by the employer.

COBRA (Consolidated Omnibus Budget Reconciliation Act) allows individuals to continue their employer-sponsored health coverage after losing their job, quitting, or experiencing certain qualifying events. Since the individual is responsible for paying the full premium that the employer and employee previously shared—plus up to a 2% administrative fee—the cost is often much higher than what employees paid while working.

For example, if an employer-sponsored family plan cost $1,200 per month with the employer covering $800, the former employee would need to pay the remaining $400 plus fees under COBRA, totaling approximately $408 monthly. However, if no employer contribution existed or the plan was more comprehensive, costs could easily exceed $800 per month.

- One of the primary factors affecting COBRA costs is the original health insurance plan’s structure. Plans with lower deductibles and broader networks, such as PPOs, typically have higher monthly premiums, which means the COBRA continuation fee will also be higher compared to more restrictive HMO plans.

- Geographic location plays a significant role as healthcare costs vary across states and regions. For instance, premiums in urban areas like New York City or San Francisco are generally higher than in rural regions due to the increased cost of medical services and provider rates.

- The number of people covered under the plan directly impacts the total COBRA cost. An individual coverage plan is less expensive than family or spousal coverage. Someone switching from employer-subsidized family coverage may face a sharp increase in out-of-pocket expenses when paying the full premium via COBRA.

- COBRA premiums are based on the total cost of the group health insurance plan that the employer offers to active employees. This includes both the portion previously paid by the employer and the portion deducted from the employee's paycheck, ensuring that the coverage remains identical in scope and benefits.

- Federal law allows former employers or plan administrators to charge an additional 2% to cover administrative costs. This fee is added to the full premium, which means individuals typically pay 102% of what the plan costs the employer.

- In cases where an individual qualifies for an extended COBRA period due to a disability ruling by the Social Security Administration, the administrative fee can increase to 150% of the premium cost for months 19 through 29. This temporary spike significantly raises the monthly burden during those months.

Alternatives to COBRA and Their Cost Comparison

- One common alternative to COBRA is purchasing coverage through the Health Insurance Marketplace established under the Affordable Care Act. Depending on income, individuals may qualify for federal subsidies that reduce monthly premiums, often making marketplace plans more affordable than COBRA, especially if employer contributions were substantial.

- Short-term health insurance plans offer lower-cost, temporary coverage that can span several months. While these plans are generally cheaper, they often come with limited benefits, exclusions for pre-existing conditions, and no compliance with ACA standards, making them unsuitable for those needing comprehensive care.

- Some individuals may qualify for Medicaid or CHIP (Children’s Health Insurance Program) based on income and household size. These government programs offer free or low-cost coverage and can be a more economical option than shouldering the full COBRA premium, particularly for unemployed individuals or those with reduced incomes.

What are the cost-saving loopholes in COBRA health insurance coverage?

Opting for Alternative Coverage During Open Enrollment

While COBRA allows individuals to maintain their current health insurance after leaving a job, it does not necessarily offer the most cost-effective solution.

A major cost-saving opportunity lies in using the special open enrollment window that occurs outside of the standard annual marketplace period. When COBRA coverage begins, individuals gain eligibility to enroll in new health plans through the Health Insurance Marketplace without waiting for the usual enrollment cycle.

This lets them compare premiums, deductibles, and benefits across a range of plans, many of which may be subsidized based on income. By switching early and canceling COBRA, individuals can secure lower monthly premiums and avoid overpaying for benefits they may not need.

- Check eligibility for Advanced Premium Tax Credits (APTC) on healthcare.gov, which can drastically reduce monthly payments for marketplace plans.

- Compare essential health benefits across plans to determine whether COBRA’s broader network or brand-name providers are truly necessary or worth the higher cost.

- Enroll promptly during the 60-day special enrollment window triggered by COBRA initiation to avoid coverage gaps and lock in lower rates.

Strategic Use of COBRA for Short-Term Medical Needs

Rather than maintaining COBRA coverage for the full 18-month duration, individuals can use it selectively to cover specific medical treatments or procedures immediately following job loss. This strategy allows people to access care under their familiar plan with known provider networks and predictable co-pays, especially when transitioning between life events.

Once a major medical service—such as surgery, ongoing treatment, or maternity care—is completed, individuals can terminate COBRA and switch to a more affordable alternative. Since COBRA coverage is retroactive to the date of job loss, enrolling only when needed and canceling once critical care is delivered can save hundreds or thousands of dollars in premiums.

- Delay COBRA enrollment until a medical need arises to preserve the right to elect coverage later during the 60-day election window.

- Use COBRA exclusively for high-cost treatments where provider continuity or pre-existing condition coverage is essential.

- Transition to a lower-cost plan such as a marketplace plan or Medicaid as soon as major care is completed and coverage stability is regained.

Leveraging State-Sponsored Continuation Programs

In certain states, mini-COBRA laws provide continuation coverage options that are more affordable and flexible than federal COBRA. These state programs apply to employers with fewer than 20 employees, who are not covered under federal COBRA guidelines.

Premiums under state continuation plans are often lower because they may be capped or partially subsidized, and some states offer extended coverage periods. Individuals should investigate whether their former employer’s state has such provisions, as these programs frequently allow people to maintain similar benefits at a fraction of the cost. When available, state continuation is typically a smarter financial move than federal COBRA.

- Research whether your former employer is located in a state with mini-COBRA laws such as California, New York, or Illinois.

- Contact your state’s Department of Insurance to confirm eligibility and application procedures for state-level continuation options.

- Compare total costs—including premiums, co-insurance, and out-of-pocket maximums—between federal COBRA and state programs to determine long-term savings potential.

Frequently Asked Questions

What is Cobra Cost Health Insurance?

COBRA health insurance allows workers and their families to continue their group health coverage temporarily after losing employment or experiencing certain life events. It is not a cost but a U.S. law that lets individuals pay to maintain their existing plan. While comprehensive, COBRA can be expensive since employees cover the full premium plus an administrative fee, typically up to 102% of the cost.

How much does COBRA health insurance cost?

COBRA costs vary based on the original group health plan. On average, individuals pay 100% of the premium plus a 2% administrative fee, often totaling $400 to $700 monthly. Since employers no longer contribute, costs are significantly higher than during employment. Prices depend on coverage level, location, and plan type, making COBRA an expensive option compared to marketplace or Medicaid plans.

Who qualifies for COBRA health insurance?

Employees at companies with 20+ workers, along with their spouses and dependent children, qualify for COBRA after qualifying events like job loss (except gross misconduct), reduced hours, divorce, or death of a covered employee. Beneficiaries must act quickly, as they have 60 days to elect COBRA coverage after receiving the election notice, and must enroll within that window to maintain uninterrupted health benefits.

How long can you stay on COBRA health insurance?

Most individuals can keep COBRA coverage for up to 18 months after a qualifying event like job loss or reduction in hours. Certain events, such as disability or a covered employee’s death, may extend coverage to 29 or 36 months. After the maximum period ends, individuals must transition to alternative health insurance through an employer, the marketplace, or government programs.

Leave a Reply