Covid-19 Impact On Travel Insurance Policies 2025

The global travel insurance landscape has undergone significant transformation since the onset of the COVID-19 pandemic, and by 2025, its lasting impact remains evident.

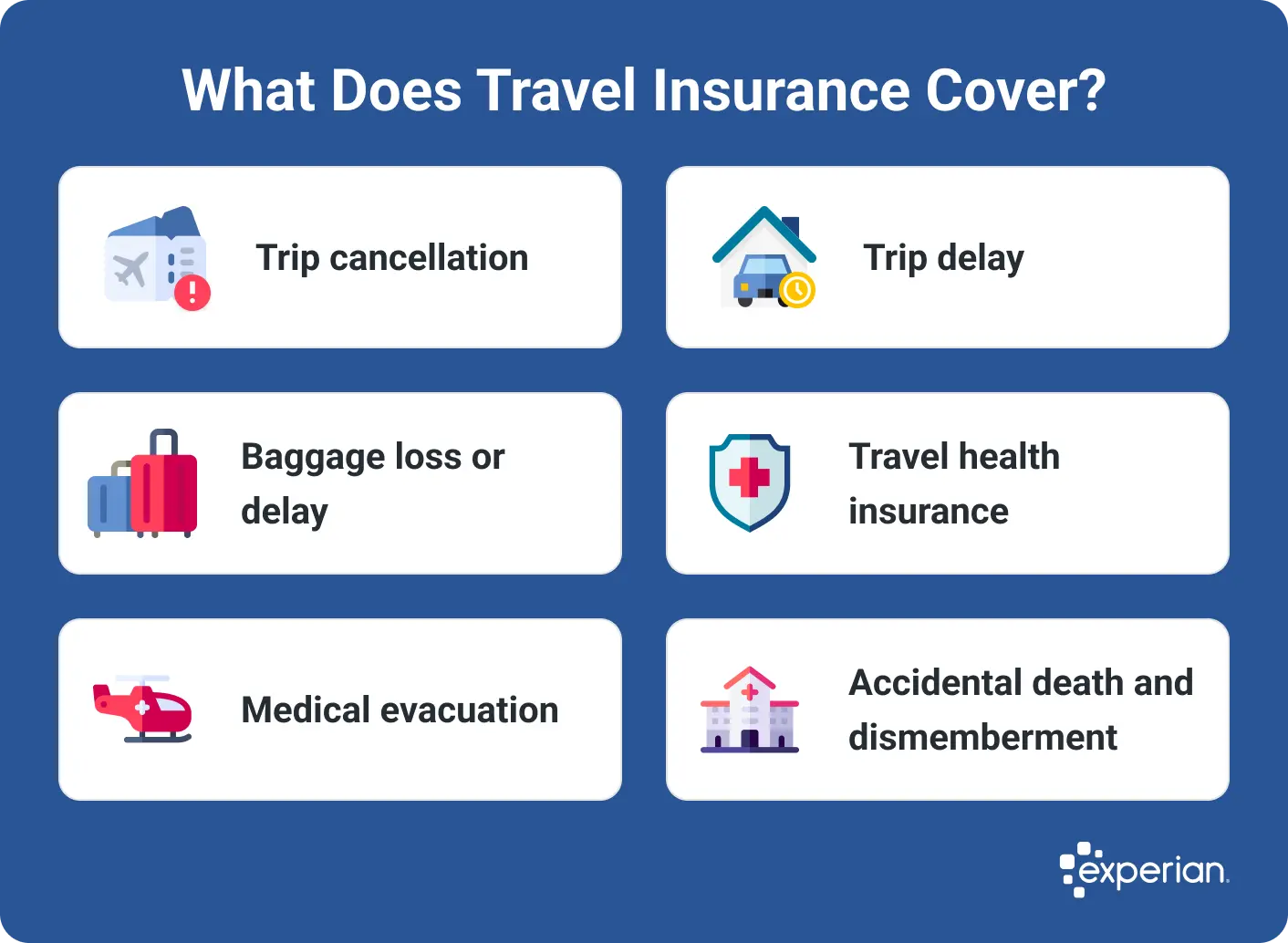

Insurers have restructured policies to address pandemic-related uncertainties, introducing enhanced coverage for trip cancellations, medical emergencies abroad, and unexpected quarantines. As travelers regain confidence, insurance providers are balancing comprehensive protection with sustainable pricing models.

New clauses specifically addressing infectious diseases, vaccine requirements, and government travel advisories have become standard. Technology-driven solutions, such as real-time risk assessment and digital claims processing, are now integral. The evolution of travel insurance in 2025 reflects a more resilient, transparent, and traveler-centric industry shaped by lessons learned during the pandemic era.

Do I Need Special Insurance For Instacart

Do I Need Special Insurance For InstacartCovid-19 Impact On Travel Insurance Policies 2025

The global travel insurance landscape has undergone significant transformation due to the lasting effects of the Covid-19 pandemic, with policies in 2025 reflecting a more adaptive, health-conscious, and risk-aware approach.

As borders reopened and international mobility resumed, insurers recalibrated coverage parameters to address emerging concerns such as vaccine mandates, quarantine costs, and last-minute cancellations driven by public health fluctuations. Unlike early 2020, when widespread exclusions caused confusion and claim denials, 2025 policies now typically include pandemic-related protections as standard or optional add-ons.

Insurers have also integrated real-time health alerts, digital medical verification systems, and enhanced refund protocols to meet traveler expectations for flexibility and security. This evolution marks a shift from reactive crisis management to proactive risk mitigation, aligning policy frameworks with the unpredictable nature of global health events.

In 2025, most comprehensive travel insurance plans explicitly cover Covid-19-related interruptions, including trip cancellations, interruptions, and medical expenses incurred abroad due to infection.

Do I Need Special Insurance For Lyft

Do I Need Special Insurance For LyftThese updates emerged from consumer demand and regulatory pressure, compelling insurers to eliminate blanket exclusions that once rendered policies ineffective during outbreaks. Now, policyholders can file claims if they test positive before or during travel, are placed under mandatory quarantine, or face sudden border closures.

Some insurers also cover the cost of temporary accommodation and return flights when travelers are stranded. This shift reflects a broader industry commitment to traveler protection in high-uncertainty environments, setting a precedent for handling future public health emergencies.

Integration of Vaccination and Health Status Verification

Insurers in 2025 increasingly require or incentivize proof of vaccination status and digital health documentation as part of the policy activation or claims process. While not universally mandated, many plans offer lower premiums or broader coverage to travelers who can verify full vaccination or recent recovery from Covid-19.

This integration is supported by interoperable digital health passes such as EU Digital Covid Certificates or private health apps linked to insurance providers. The goal is to reduce risk exposure and streamline medical claims processing. However, this trend has sparked debate over privacy concerns and equitable access, especially for travelers from regions with limited vaccine availability or unreliable digital infrastructure.

Gold Amex Travel Insurance

Gold Amex Travel InsuranceDynamic Pricing and Real-Time Risk Assessment Models

A major innovation in 2025 is the use of AI-driven risk modeling to adjust travel insurance premiums in real time based on global health data, regional infection rates, and government travel advisories. These models allow insurers to offer personalized pricing that reflects the actual risk level of a destination at the time of purchase.

For instance, traveling to a country experiencing a surge in respiratory illness may trigger higher premiums or specific exclusions unless additional coverage is purchased. This dynamic approach improves transparency and enables travelers to make informed decisions. The integration of big data analytics not only benefits insurers financially but also enhances customer trust through tailored and timely policy options.

| Policy Feature | Pre-Pandemic (Before 2020) | 2025 Standard Coverage |

|---|---|---|

| Covid-19 Medical Expenses Abroad | Typically not covered | Routinely included, up to policy limits |

| Trip Cancellation Due to Illness | Limited to non-pandemic illnesses | Explicitly covers positive Covid-19 tests |

| Quarantine Coverage | Excluded or capped | Includes daily benefits for lodging & meals |

| Flexible Rebooking or Refunds | Strict non-refundable terms | Free or low-cost changes within 24–48 hours |

| Real-Time Risk Alerts | Not available | Integrated via mobile apps and policy portals |

Covid-19 Impact on Travel Insurance Policies in 2025: A Comprehensive Guide

How will COVID-19 influence travel insurance policies in 2025?

Enhanced Coverage for Pandemic-Related Disruptions

Travel insurance policies in 2025 are expected to offer more robust coverage for pandemic-related events, largely as a direct response to the gaps exposed during the initial phases of the COVID-19 crisis.

Health Insurance When You Travel

Health Insurance When You TravelInsurers have recognized the need to clearly define what constitutes a covered event during global health emergencies, ensuring travelers are protected against unforeseen cancellations, medical emergencies abroad, and quarantine requirements. This evolution aims to reduce ambiguity and increase consumer trust in insurance products.

- Many policies will explicitly include coverage for trip cancellations or interruptions due to government-imposed travel bans related to infectious diseases.

- Medical coverage extensions will likely encompass treatment for viral infections contracted during travel, including COVID-19 variants prevalent in 2025.

- Quarantine expenses, such as additional accommodation and return flight changes, may be standard inclusions rather than optional add-ons.

Higher Premiums and Tiered Policy Options

As insurers adapt to the long-term risks associated with global pandemics, travelers can anticipate adjusted pricing structures and a broader range of policy tiers. The financial impact of widespread claims during the pandemic has prompted companies to reevaluate risk models, leading to more nuanced premium calculations based on destination risk levels, vaccination status, and traveler health profiles. This shift allows for personalized policies but may result in increased costs for comprehensive coverage.

- Base policies may exclude pandemic coverage unless upgraded, requiring travelers to opt into higher-tier plans for full protection.

- Premiums could vary significantly depending on the destination's healthcare infrastructure and current disease outbreak status.

- Insurers may offer dynamic pricing models, adjusting rates in real-time based on global health alerts and infection rates.

Integration of Health Verification and Digital Documentation

By 2025, travel insurance frameworks are likely to integrate more closely with digital health credentials and verification systems, a trend accelerated by the necessity of vaccine passports during the pandemic. Insurers may require proof of vaccination, recent testing, or use health-tracking apps to assess risk before issuing policies. This digital integration not only streamlines claims processing but also allows for proactive risk management.

- Insurance providers may partner with health platforms to verify travelers’ medical status automatically upon policy purchase.

- Claims related to illness abroad could require digital submission of test results or medical records through secure portals.

- Real-time data from wearable devices might be used to monitor traveler health, potentially influencing coverage eligibility or claim outcomes.

Does travel insurance cover cancellations due to unforeseen events like COVID-19 in 2025?

- As of 2025, most standard travel insurance policies continue to treat pandemics as a generally excluded event unless explicitly stated otherwise. While lessons from the initial waves of COVID-19 led some insurers to revise their offerings, widespread automatic coverage for pandemics is still not the norm. Policyholders must review the specific terms to determine whether infectious disease-related cancellations are included.

- Many travel insurance providers now offer optional add-ons or upgraded plans that do cover pandemics, including COVID-19, under certain conditions. These may include coverage if a traveler is diagnosed with the virus, is quarantined, or if official travel bans are imposed by governments. Coverage often depends on the timeline of policy purchase relative to travel advisories or outbreak declarations.

- It’s important to note that coverage eligibility frequently hinges on when the policy was purchased in relation to public knowledge of the health threat. For example, policies bought after a pandemic is formally recognized by the World Health Organization or after the issuance of a government travel warning may exclude claims related to that event. Always ensure the policy is purchased before any public alerts are issued.

What Types of Unforeseen Events Are Typically Covered Under Modern Travel Insurance Policies?

- Modern travel insurance plans typically cover a defined list of unforeseen events, including sudden illness or injury (of the traveler or a close family member), hospitalization, death, natural disasters affecting travel routes, terrorist attacks at the destination, and airline bankruptcies. These are considered valid reasons for trip cancellation or interruption.

- Some policies extend coverage to unexpected events such as jury duty, mandatory military deployment, or a home becoming uninhabitable due to fire or severe weather. However, coverage varies significantly between providers and policy tiers, so careful comparison is necessary.

- Events that are considered foreseeable or within the traveler’s control—such as choosing not to travel due to personal anxiety about health risks or general news reports about an illness—are typically not covered. Insurers evaluate claims based on documented unpredictability and severity, requiring medical certification or official documentation to support most claims.

- To maximize protection, travelers should select a comprehensive plan that explicitly includes “Cancel for Any Reason” (CFAR) coverage or pandemic-specific riders. CFAR allows cancellation for reasons not listed in standard policies, usually refunding 50% to 75% of the trip cost, and must be purchased within a short window after the initial trip deposit.

- It is essential to read the policy’s definitions of covered illnesses and required documentation. For COVID-19 or similar conditions, insurers may require a positive test result, a doctor’s note, or proof of isolation orders. Keeping detailed medical and travel records improves the chances of a successful claim.

- Travelers are advised to purchase insurance as early as possible—ideally within 7 to 21 days of booking—to qualify for time-sensitive benefits and pre-existing condition waivers. Early enrollment often increases eligibility for enhanced protections, including coverage related to emerging health crises that were not yet declared at the time of purchase.

How did Martin Lewis address the impact of Covid-19 on travel insurance policies in 2025?

Clarification on Policy Coverage During Ongoing Travel Disruptions

- Martin Lewis emphasized the importance of understanding exactly what travel insurance policies covered in the context of lingering Covid-19 disruptions, particularly in 2025 when some regions still experienced localized outbreaks and travel advisories.

- He advised travelers to review their policy documents thoroughly, highlighting that many standard policies did not automatically cover cancellations due solely to fear of infection or government travel warnings unless explicitly stated.

- Lewis recommended looking for policies with comprehensive disruption due to pandemics clauses, which were becoming more common among providers adapting to post-pandemic travel trends.

Guidance on Claiming for Cancellations and Medical Expenses Abroad

- Martin Lewis provided clear direction on how to file claims if a trip was canceled due to a positive Covid-19 diagnosis, stressing the need for official documentation such as PCR or rapid test results and medical confirmation.

- He outlined steps travelers should follow, including immediate notification to both the insurer and the travel provider, and keeping detailed records of all communications and expenses.

- Lewis also addressed medical coverage abroad, urging travelers to verify that their policy included treatment costs for Covid-19, which varied significantly between providers and sometimes required additional riders or upgrades.

Promotion of Government and Industry Resources

- In 2025, Martin Lewis actively promoted the use of official resources, such as the Foreign, Commonwealth & Development Office (FCDO) travel advice pages, to help individuals assess whether travel to specific destinations was advised, which influenced insurance validity.

- He collaborated with insurance comparison platforms to highlight providers that had adapted their terms to be more traveler-friendly in the wake of the pandemic, sharing direct links and updates through his website and social channels.

- Lewis also encouraged consumers to check the Insurance Repository and ombudsman services if disputes arose with insurers over Covid-related claims, helping to empower individuals with tools to challenge unfair denials.

Does travel insurance cover trip cancellation due to COVID-19 in 2025?

- As of 2025, most comprehensive travel insurance plans do provide coverage for trip cancellation due to confirmed cases of COVID-19, provided the policy was purchased before the trip was canceled and before any symptoms appeared or diagnosis was made.

- Insurers typically require documented proof, such as a positive PCR or rapid antigen test result, a doctor’s note, or a government-issued quarantine order, to validate the claim for cancellation.

- It is essential to read the policy’s specific wording, as not all plans treat pandemics or infectious diseases the same way — some may have exclusions or limitations based on the destination or the traveler's vaccination status.

Vaccination Status and Its Impact on Coverage

- Many insurance providers now consider vaccination status when evaluating claims related to COVID-19; being up to date with recommended vaccines may be a condition for coverage of illness-related cancellations.

- If a traveler chooses not to be vaccinated and contracts COVID-19, some policies may deny coverage on the grounds that the illness was preventable and resulted from known risk exposure.

- Travelers should confirm whether their policy contains clauses related to vaccine requirements and understand how their personal health decisions could influence the outcome of a potential claim.

Emerging Variants and Government Restrictions in 2025

- If a new variant of the virus emerges in 2025 leading to renewed travel bans or mandatory quarantines, coverage depends on whether the policy includes provisions for government-mandated trip interruptions.

- Some Cancel For Any Reason (CFAR) add-ons allow greater flexibility, reimbursing a portion of non-refundable expenses even if the reason for cancellation isn’t explicitly covered, including fear of contracting the virus.

- Travelers should monitor updates from health authorities and insurers, as sudden policy changes or destination-specific exclusions may be implemented in response to evolving public health conditions.

Frequently Asked Questions

Does travel insurance cover trip cancellations due to COVID-19 in 2025?

Yes, most travel insurance policies in 2025 cover trip cancellations due to COVID-19 if you're diagnosed before departure or require quarantine. Coverage depends on policy terms, timing of purchase, and whether the destination has travel restrictions. Always check for a “cancel for any reason” add-on and ensure you meet documentation requirements such as medical proof or official orders.

Are medical expenses from COVID-19 covered during international travel?

Yes, many travel insurance plans in 2025 include medical coverage for illnesses like COVID-19 while abroad. This typically covers hospitalization, doctor visits, and necessary treatments. However, coverage limits and exclusions vary by provider. Some plans may require proof of vaccination or exclude high-risk regions. Always review your policy details and confirm coverage with your insurer before traveling.

Will travel insurance cover quarantine costs if I test positive abroad?

Yes, several travel insurance policies in 2025 provide coverage for quarantine-related expenses such as extended hotel stays and return flight changes if you test positive for COVID-19 while traveling. Coverage amounts and conditions vary. Documentation like a positive test result and official quarantine orders are usually required. Always verify your policy’s specifics to ensure eligibility for reimbursement.

Yes, the lasting impact of COVID-19 has influenced travel insurance premiums in 2025, though rates have stabilized compared to earlier years. Insurers now better assess pandemic-related risks, and premiums reflect destination, trip duration, and coverage level. Policies with enhanced medical or cancellation coverage may have higher costs. Shopping around and comparing plans helps find balanced pricing and protection.

Leave a Reply