Disability Insurance Policies Covering Mental Health Conditions

Disability insurance plays a critical role in protecting individuals when health issues prevent them from working, yet mental health conditions have historically faced significant limitations in coverage.

As awareness grows around mental wellness, more policies are beginning to include comprehensive provisions for conditions like depression, anxiety, and bipolar disorder.

However, challenges remain in eligibility, benefit duration, and the definition of total disability. Understanding how disability insurance addresses mental health is essential for policyholders seeking financial protection.

Aarp Auto Insurance Reviews Finance

Aarp Auto Insurance Reviews FinanceThis article explores the evolving landscape of disability insurance policies that cover mental health conditions, highlighting key considerations, common limitations, and recent advancements in the industry.

How Disability Insurance Policies Address Mental Health Conditions

Disability insurance plays a crucial role in providing financial protection to individuals who are unable to work due to medical conditions, including mental health disorders. Historically, mental health conditions were either excluded from coverage or subject to more restrictive terms compared to physical disabilities.

However, in recent years, regulatory changes and increased awareness of mental health issues have led many insurers to expand their policies to include conditions such as depression, anxiety, bipolar disorder, and PTSD. Despite this progress, coverage for mental health often comes with specific limitations, such as shorter benefit periods or stricter eligibility requirements.

Understanding how disability insurance policies cover mental health conditions is essential for individuals seeking protection, as it allows them to make informed decisions and advocate for appropriate care and income support during periods of disability.

Aig Auto Insurance Reviews

Aig Auto Insurance ReviewsCommon Mental Health Conditions Covered by Disability Insurance

Many disability insurance policies now include coverage for a range of diagnosed mental health disorders, though the scope can vary significantly between providers and policy types.

Conditions such as major depressive disorder, generalized anxiety disorder, bipolar disorder, schizophrenia, and post-traumatic stress disorder (PTSD) are commonly recognized as qualifying disabilities when they prevent an individual from performing their job duties.

Coverage usually requires documentation from a licensed mental health professional, including diagnosis, treatment plans, and functional assessments demonstrating the severity and duration of impairment.

While some group policies through employers offer broader inclusion, individual policies may impose limitations, such as caps on benefit duration—often limiting mental health claims to 24 months, even if the policy provides longer benefits for physical disabilities.

Alfa Insurance Auto Quote

Alfa Insurance Auto QuoteLimitations and Exclusions in Mental Health Coverage

Despite growing recognition of mental health conditions, many disability insurance policies still impose more restrictive terms for claims related to psychological impairments compared to physical ones.

A common limitation is the 24-month benefit cap, which restricts the length of time individuals can receive benefits solely due to mental health conditions, regardless of ongoing disability. Additionally, insurers may require extensive documentation, including psychiatric evaluations and proof of treatment compliance, to validate a claim.

Pre-existing condition clauses and exclusions for substance use disorders, unless treated alongside a primary mental health diagnosis, can further complicate coverage. These restrictions reflect historical biases and challenges in objectively measuring functional impairment in mental health, but consumer advocacy and legal standards are gradually pushing for more equitable treatment.

Short-Term vs. Long-Term Disability Insurance for Mental Health

Both short-term disability (STD) and long-term disability (LTD) insurance plans can provide coverage for mental health conditions, but they differ in duration, eligibility, and level of support.

America's Best Auto Insurance Carrollton

America's Best Auto Insurance CarrolltonSTD policies typically cover mental health issues for a limited period—usually up to six months—with benefits beginning after a short waiting period of a few days to a week. In contrast, LTD policies offer longer-term income replacement, often extending several years or until retirement age, but commonly apply the aforementioned 24-month limitation for mental health-related claims.

Approval for either type of claim hinges on the individual’s ability to demonstrate a significant and medically documented impairment that prevents them from working in their occupation. Employer-sponsored LTD plans governed by ERISA regulations may also impose additional procedural hurdles, making thorough documentation and persistent appeals essential for claim success.

| Feature | Short-Term Disability | Long-Term Disability |

|---|---|---|

| Typical Benefit Period | 3–6 months | Years to retirement age (with mental health cap) |

| Benefit Cap for Mental Health | Usually not capped at 24 months | 24-month limit common |

| Waiting Period | 0–14 days | 90–180 days |

| Documentation Required | Doctor’s note, diagnosis, functional limitations | Psychiatric evaluation, treatment history, work incapacity proof |

| Coverage for Conditions Like Depression or Anxiety | Yes, widely included | Yes, but often subject to restrictions |

Comprehensive Guide to Disability Insurance Policies Covering Mental Health Conditions

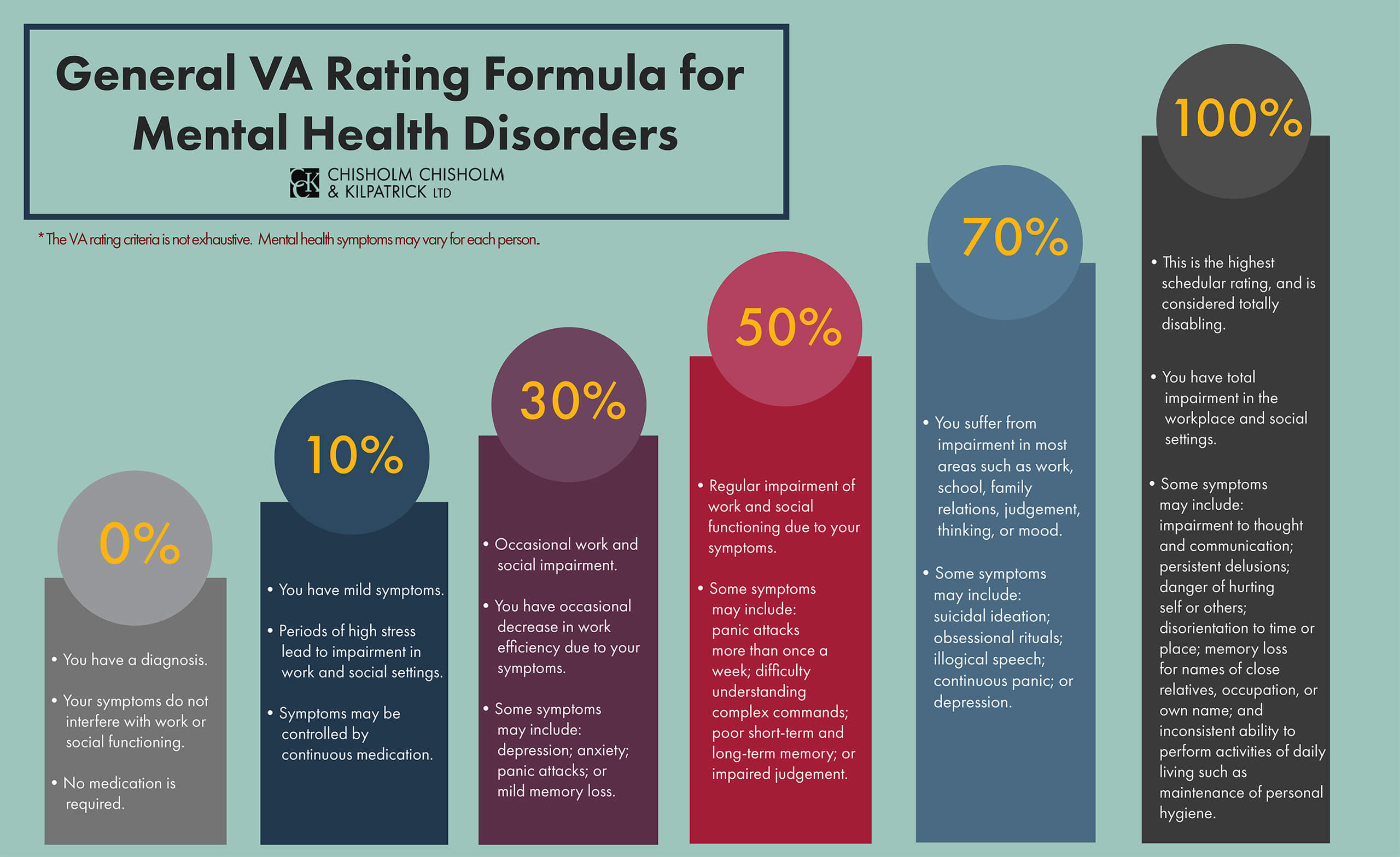

Can mental health conditions qualify for 100% disability under insurance policies?

Yes, mental health conditions can qualify for 100% disability under certain insurance policies, depending on the severity of the condition, the type of insurance, and the specific policy terms. Many long-term disability (LTD) insurance plans, as well as government programs like Social Security Disability Insurance (SSDI), recognize severe mental health disorders as valid bases for total disability claims.

To qualify, individuals must demonstrate through medical documentation and often functional assessments that their condition significantly impairs their ability to perform essential job duties or any substantial gainful activity. Conditions such as major depressive disorder, bipolar disorder, schizophrenia, and severe anxiety disorders are commonly considered, especially when they result in prolonged inability to work.

Criteria for Qualifying with a Mental Health Condition

- The primary requirement is a formally diagnosed mental health disorder supported by a licensed mental health professional, such as a psychiatrist or clinical psychologist. This diagnosis must align with established diagnostic criteria, typically from the DSM-5 (Diagnostic and Statistical Manual of Mental Disorders).

- Individuals must show that their symptoms severely limit their capacity to function in a work environment—this includes difficulties with concentration, social interaction, persistence in tasks, and emotional regulation. Insurance providers assess these limitations using functional capacity evaluations or reports from treating clinicians.

- The disability must be expected to last for a minimum duration, often at least 12 months, as stipulated in most insurance contracts. Temporary or mild conditions that allow for partial work performance usually do not meet the threshold for 100% disability benefits.

Types of Insurance That May Cover 100% Disability for Mental Health

- Private long-term disability insurance policies often include mental health conditions in their coverage, though some impose limitations such as shorter benefit periods (e.g., 24 months) for psychiatric diagnoses compared to physical conditions. However, if the policy does not have such exclusions, a mental health condition can indeed lead to full 100% disability benefits.

- Social Security Disability Insurance (SSDI) evaluates mental disorders using a set of listings in its Blue Book, specifically Section 12—Mental Disorders. Meeting or medically equaling one of these listings, such as 12.04 for depressive disorders or 12.03 for psychotic disorders, can result in full disability benefits.

- Employer-sponsored group disability plans may also cover mental health conditions at 100%, but the terms vary widely. Some plans differentiate between physical and mental health categories, so understanding the policy details is critical to determining eligibility for full benefits.

Documentation and Evidence Required for Approval

- Comprehensive medical records from mental health providers are essential, including treatment history, medication regimens, therapy notes, and hospitalization records if applicable. Consistent treatment strengthens the claim by demonstrating the ongoing nature and severity of the condition.

- Functional assessments, such as a Mental Residual Functional Capacity (MRFC) form completed by a psychiatrist or psychologist, detail how symptoms impact daily activities and job performance—information that insurers closely examine when evaluating claims.

- In some cases, third-party statements from family members, coworkers, or employers may support the claim by providing real-world examples of how the mental health condition has impaired functioning. These narratives can help corroborate the clinical evidence submitted.

What mental health conditions are covered under disability insurance policies with Blue Cross Blue Shield?

Common Mental Health Conditions Covered

Disability insurance policies offered by Blue Cross Blue Shield (BCBS) typically cover a range of diagnosed mental health conditions that significantly impair an individual's ability to perform their job duties.

The eligibility for benefits depends on the severity and documented impact of the condition, not just the diagnosis itself. Coverage is generally aligned with criteria from the Diagnostic and Statistical Manual of Mental Disorders (DSM-5) and requires medical verification from a licensed mental health professional.

- Major Depressive Disorder: This is one of the most commonly covered conditions, especially when it results in prolonged inability to work due to symptoms like persistent sadness, lack of energy, and impaired concentration.

- Anxiety Disorders: Includes generalized anxiety disorder, panic disorder, and social anxiety disorder, particularly when symptoms such as excessive worry, avoidance behaviors, or physical manifestations interfere with daily functioning.

- Bipolar Disorder: Coverage applies during acute episodes (manic or depressive) where the individual is unable to maintain regular work performance due to mood swings, impulsivity, or hospitalization.

Eligibility and Documentation Requirements

To qualify for benefits under a BCBS disability insurance policy for a mental health condition, policyholders must meet specific eligibility criteria and provide thorough documentation.

The insurance review process focuses on objective evidence showing that the condition prevents the individual from performing the material duties of their occupation. Pre-existing condition clauses and policy waiting periods also apply in most cases.

- Medical Records: Comprehensive records from psychiatrists, psychologists, or therapists are required, including diagnosis, treatment history, medication use, and notes on functional limitations.

- Functional Capacity Evaluation: Some policies may require a detailed assessment explaining how the mental health condition limits cognitive or emotional functioning in a work context, such as difficulty concentrating, handling stress, or interacting with others.

- Proof of Continuous Treatment: Insurers often require evidence of ongoing treatment, such as regular therapy sessions or medication management, to validate the persistence and severity of the condition.

Limitations and Variations in Coverage

While Blue Cross Blue Shield provides coverage for many mental health conditions, there are limitations that vary by specific policy, state regulations, and whether the plan is employer-sponsored or individual. Not all policies offer the same duration or percentage of benefits for mental health-related disabilities, and some include caps on benefit periods for non-physical conditions.

- Benefit Duration Caps: Many policies limit mental health disability benefits to 24 months, even if the physical disability benefits last longer, depending on the plan’s terms.

- Plan-Specific Exclusions: Certain conditions, such as personality disorders or substance use disorders, may have restricted coverage or require additional criteria to qualify for benefits.

- State and Employer Variability: Coverage details can differ significantly based on the state of residence and whether the policy is part of a group plan through an employer, impacting access and approval rates.

Frequently Asked Questions

What mental health conditions are typically covered by disability insurance policies?

Most disability insurance policies cover a range of diagnosed mental health conditions, including depression, anxiety disorders, bipolar disorder, PTSD, and schizophrenia. Coverage depends on the policy's specific terms and the severity of the condition. Some policies may limit benefits for mental health-related claims to a shorter duration than physical disabilities. Always review your policy details or consult with your provider to understand what conditions and treatment plans are included.

How long does disability insurance pay for mental health conditions?

Disability insurance typically pays benefits for mental health conditions up to a specified period, often 24 months for non-physical disabilities. Some long-term policies may extend beyond this, especially if the condition prevents sustained work. The duration depends on the specific policy terms and medical documentation proving ongoing disability. Check your plan’s limitations and work with a healthcare provider to ensure continued eligibility for benefits.

Do I need a doctor’s diagnosis to claim disability for a mental health condition?

Yes, a formal diagnosis from a licensed mental health professional—such as a psychiatrist or psychologist—is required to file a disability claim. Insurers also require ongoing treatment records and medical evidence demonstrating that the condition significantly impairs your ability to work. Regular evaluations and documentation from your provider increase the likelihood of claim approval and continued benefit payments throughout the disability period.

Can I receive disability benefits if I’m undergoing therapy for a mental health condition?

Yes, you can receive disability benefits while undergoing therapy if your mental health condition prevents you from performing your job duties. Therapy records often serve as crucial evidence in your claim. However, receiving therapy alone doesn’t guarantee benefits—you must prove functional impairment through medical documentation and meet your policy’s definition of disability. Always keep your insurer updated with treatment progress.

Leave a Reply