Fort Worth Group Health Insurance

Access to comprehensive and affordable health insurance is a cornerstone of financial and medical security, especially for businesses and employees in Fort Worth. Group health insurance provides a practical solution, offering coverage that supports employee well-being while helping employers attract and retain top talent.

In a growing city with a dynamic workforce, Fort Worth group health insurance plans are designed to meet the diverse needs of businesses, from small startups to large corporations. These plans often include benefits such as preventive care, specialist visits, hospitalization, and prescription drug coverage, all structured to promote long-term health and reduce out-of-pocket expenses for employees and their families.

Understanding Fort Worth Group Health Insurance Options for Employers and Employees

Fort Worth businesses seeking to provide competitive benefits packages often turn to group health insurance as a strategic solution to attract and retain talent while managing healthcare costs. Group health insurance refers to health coverage offered by an employer to its employees, typically at lower premiums than individual plans due to shared risk across a larger pool.

Cheap Auto Insurance Joliet

Cheap Auto Insurance JolietIn Fort Worth, companies of all sizes can access flexible plans through carriers such as Blue Cross Blue Shield of Texas, Cigna, UnitedHealthcare, and regional providers. These plans often include a range of options, including PPOs, HMOs, and High-Deductible Health Plans (HDHPs) paired with Health Savings Accounts (HSAs), allowing employers to tailor coverage to their workforce’s needs.

Additionally, under the Affordable Care Act (ACA), businesses with 50 or more full-time equivalent employees may be subject to the employer mandate, requiring them to offer affordable coverage or face potential penalties. Navigating this landscape requires understanding plan costs, employee eligibility, provider networks, and compliance obligations.

Benefits of Offering Group Health Insurance in Fort Worth

Providing group health insurance offers significant advantages for both employers and employees in the Fort Worth area.

For employers, offering health benefits enhances employee recruitment and retention, improves morale, and increases workplace productivity. From a financial perspective, businesses can take advantage of tax deductions on premiums paid for employee coverage, and employees benefit from pre-tax payroll deductions, reducing their taxable income.

Cheap Auto Insurance Quotes Pa

Cheap Auto Insurance Quotes PaFort Worth organizations also gain access to broader provider networks, including major hospitals like JPS Health Network and Baylor Scott & White, ensuring employees receive quality care. Furthermore, group plans often include preventive services at no additional cost, supporting a healthier workforce and potentially lowering long-term healthcare expenses for both parties.

Key Considerations When Choosing a Group Health Plan

Selecting the right group health insurance plan in Fort Worth requires careful evaluation of several critical factors. Employers must assess the size of their workforce, overall budget constraints, and employee demographics to determine the most suitable coverage level.

It’s crucial to compare monthly premiums, deductibles, co-pays, and out-of-pocket maximums across different plans and insurers. Employers should also consider the network of healthcare providers—ensuring key Fort Worth clinics and hospitals are included—and whether employees value flexibility in choosing specialists without referrals, a hallmark of PPO plans.

Other important considerations include prescription drug coverage, telehealth availability, and wellness programs that promote employee health. Engaging a licensed insurance broker familiar with the North Texas market can help navigate these options effectively.

Cheap Full Coverage Auto Insurance Az

Cheap Full Coverage Auto Insurance AzSmall Business Health Options Program (SHOP) in Texas

The Small Business Health Options Program (SHOP) is a valuable resource for Fort Worth-based small businesses with fewer than 25 employees seeking affordable group health coverage.

Administered by the federal government, SHOP allows employers to compare and enroll in certified health plans through the Health Insurance Marketplace or directly with insurers. One major incentive is the Small Business Health Care Tax Credit, which can cover up to 50% of premium costs (35% for nonprofit employers) for companies paying average wages below a certain threshold.

SHOP plans offer flexibility—businesses can choose to contribute a fixed percentage toward employee premiums or offer different levels of coverage based on employee roles. Additionally, SHOP supports annual plan changes, enabling employers to adapt coverage as business needs evolve, making it a dynamic and scalable option for growing Fort Worth enterprises.

| Plan Feature | Group Health Insurance | Individual Health Insurance |

|---|---|---|

| Monthly Premiums | Typically lower due to shared risk and employer contribution | Generally higher, dependent on individual age and health status |

| Tax Advantages | Employer premiums are tax-deductible; employee contributions are pre-tax | Limited tax benefits unless eligible for subsidies |

| Enrollment Period | Open throughout the year with qualifying events | Limited to annual Open Enrollment or special enrollment periods |

| Provider Network Access | Broad networks often include major Fort Worth hospitals | Varies by plan; may be more limited than group networks |

| Affordable Care Act (ACA) Mandate | Applies to employers with 50+ full-time employees | Does not apply to individual plan holders |

Comprehensive Guide to Fort Worth Group Health Insurance Options

What group health insurance plans does Fort Worth offer employees?

.png)

Medical Insurance Coverage Options

The City of Fort Worth provides its employees with comprehensive medical insurance plans designed to meet a variety of healthcare needs.

These group health plans are offered through well-established insurance carriers and include options such as Health Maintenance Organization (HMO) plans, Preferred Provider Organization (PPO) plans, and high-deductible health plans (HDHPs) paired with Health Savings Accounts (HSAs).

Employees can select the plan that best fits their medical requirements, budget, and preferred network of healthcare providers. Coverage typically includes preventive care, hospitalization, prescription drugs, mental health services, and emergency care.

- Employees may choose from multiple medical plan tiers, allowing customization based on family size and desired level of coverage.

- PPO plans offer greater flexibility in selecting specialists and out-of-network providers, though at a higher cost.

- HMO options emphasize cost-efficiency by requiring the selection of a primary care physician and referrals for specialists.

Dental and Vision Benefits

In addition to medical coverage, Fort Worth offers group dental and vision insurance plans as part of its employee benefits package. These ancillary plans help reduce out-of-pocket expenses related to routine care and unexpected dental or vision issues.

The dental plan typically covers preventive services such as cleanings and exams, as well as basic and major procedures like fillings, root canals, and crowns. The vision plan includes coverage for eye exams, prescription eyeglasses, contact lenses, and discounts on LASIK surgery. These benefits support long-term health and wellness by promoting regular preventive care.

- Dental coverage includes both in-network and out-of-network options, with higher reimbursement rates when using preferred providers.

- Vision benefits are available annually and often include allowances for frames or contact lens purchases.

- Employees can enroll in dental and vision plans independently or in combination with their medical insurance selection.

Flexible Spending and Wellness Programs

The City of Fort Worth enhances its group health offerings through flexible spending accounts (FSAs) and wellness initiatives. Employees can contribute pre-tax dollars to a Dependent Care FSA or a Healthcare FSA to pay for qualified medical, dental, vision, and childcare expenses.

These accounts help lower taxable income while increasing disposable income for health-related costs. Additionally, the city promotes employee well-being through wellness programs that may include fitness challenges, health screenings, smoking cessation support, and educational seminars.

- Healthcare FSAs allow employees to set aside up to the IRS annual limit for eligible out-of-pocket medical expenses.

- Wellness program participation can lead to premium reductions or incentives under certain insurance plans.

- Resources are provided year-round to encourage healthy lifestyle choices and preventive healthcare practices.

Which group health insurance provider is the top choice for businesses in Fort Worth, Texas?

The top choice for group health insurance providers for businesses in Fort Worth, Texas is often considered to be UnitedHealthcare (UHC). This ranking stems from UHC’s extensive provider network, flexible plan options, and strong reputation for customer service within the employer solutions market. Fort Worth businesses benefit from UHC’s broad access to hospitals and clinics across North Texas, including relationships with major health systems like Baylor Scott & White and Cook Children’s.

Additionally, UnitedHealthcare offers scalable plans suitable for small, mid-sized, and large companies, with wellness programs, telehealth services, and digital tools that enhance employee engagement. The company’s local support teams and responsive claims processing further bolster its standing as a preferred provider in the region.

Key Factors That Make UnitedHealthcare a Leading Provider in Fort Worth

- UnitedHealthcare's expansive network includes thousands of in-network physicians and medical facilities throughout Tarrant County and the Dallas-Fort Worth metroplex, ensuring employees have ready access to care without excessive travel or out-of-network costs.

- The provider offers a variety of customizable health plan designs, such as HMOs, PPOs, high-deductible health plans paired with HSAs, and value-based insurance options, allowing employers to match coverage with their workforce’s needs and budget.

- Employers gain access to advanced digital tools like the UnitedHealthcare app and online portals that simplify benefits administration, claims tracking, and employee health management, contributing to higher satisfaction and lower administrative burdens.

Alternative Group Health Insurance Providers Popular Among Fort Worth Employers

- Blue Cross and Blue Shield of Texas (BCBSTX) is a strong contender due to its well-established regional presence, comprehensive benefits, and robust preventive care coverage, making it a reliable option for businesses that prioritize long-term stability and local support.

- Humana offers competitive group plans with features like mental health support, wellness incentives, and integrated care management, appealing to companies focused on holistic employee well-being and chronic condition management.

- BCBS LocalPlus, a localized offering from BCBSTX, is tailored specifically for Texas employers, providing cost-effective plans with access to the Blue Access PPO network and favorable rates for in-state medical services, which is particularly advantageous for regionally based businesses.

How Fort Worth Businesses Can Choose the Right Group Health Insurance Plan

- Employers should evaluate the size of their workforce and expected healthcare utilization, as plan flexibility and premium costs vary significantly between small group and large group markets in Texas.

- Conducting a needs assessment by surveying employees about preferred doctors, telehealth usage, prescription drug needs, and mental health services helps align the selected plan with actual employee expectations.

- Partnering with a licensed, local insurance broker who understands the Fort Worth business landscape and has direct access to multiple carriers enables companies to compare rates, network strength, and service quality to make an informed decision.

What sets Fort Worth group health insurance apart from individual health insurance plans?

One of the most significant advantages of Fort Worth group health insurance compared to individual health insurance plans is cost efficiency. Employers typically contribute a substantial portion of the monthly premiums, which reduces the financial burden on employees.

This shared-cost model makes comprehensive coverage more affordable than purchasing individual plans, where the entire premium falls on the policyholder. Additionally, group plans benefit from the insurer’s ability to spread risk across a larger pool of individuals, which often leads to lower rates.

- Employers in Fort Worth commonly cover 50% to 80% of employee premiums, making coverage significantly more accessible.

- Group plans leverage collective bargaining power, allowing businesses to negotiate better rates with insurers.

- Lower per-person administrative costs in group insurance contribute to reduced overall premiums for participants.

Coverage Stability and Guaranteed Issue

Fort Worth group health insurance offers greater stability in coverage, especially for individuals with pre-existing conditions. Unlike individual plans, which may require medical underwriting and can deny coverage or charge higher premiums based on health history, group plans are generally guaranteed issue.

This means employees cannot be denied coverage due to health status as long as they meet eligibility criteria such as employment status. This provides a more reliable and inclusive option for employees seeking consistent healthcare access.

- Group policies do not require health questionnaires or medical exams for enrollment in most cases.

- Employees transitioning from individual plans benefit from uninterrupted coverage without exclusions for pre-existing conditions.

- Renewability is typically not contingent on individual claims history, protecting employees with higher medical needs.

Broad Network Access and Enhanced Benefits

Another key differentiator is the breadth of provider networks and the range of benefits included in Fort Worth group health plans. Insurers often design group policies with extensive networks of doctors, specialists, and hospitals to meet the diverse needs of employee populations. These plans also frequently include value-added benefits such as mental health services, preventive care with no out-of-pocket costs, dental and vision coverage, and wellness programs—features that may be limited or require extra costs in individual plans.

- Group plans typically offer access to regional or national provider networks, increasing convenience for employees.

- Preventive services like annual checkups, vaccinations, and screenings are commonly covered at 100% under group policies.

- Employers can customize benefit packages, adding ancillary options such as telehealth, prescription discounts, and disability coverage.

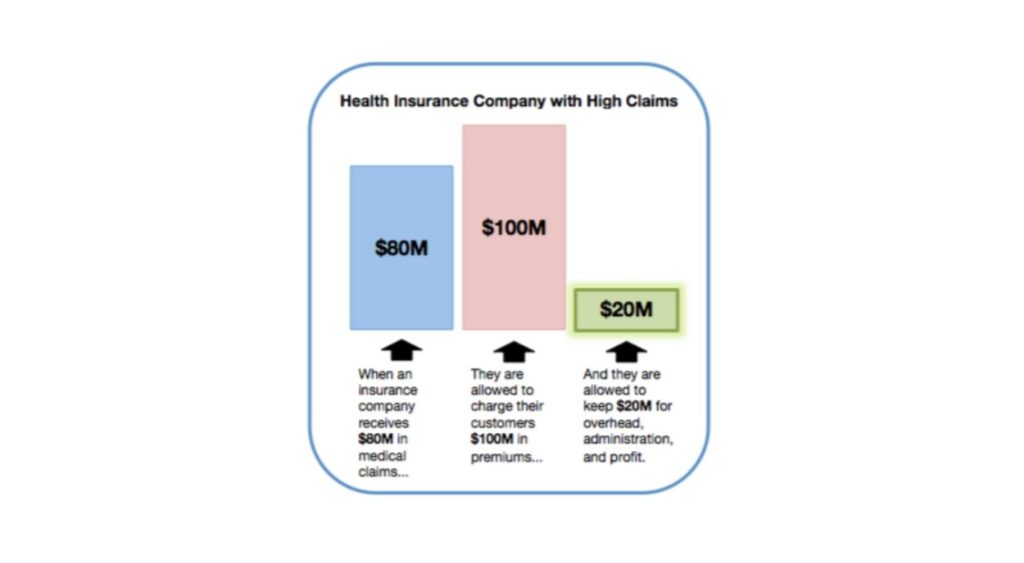

What is the 80/20 rule in Fort Worth group health insurance plans?

The 80/20 rule in Fort Worth group health insurance plans refers to a regulation established under the Affordable Care Act (ACA) that requires health insurance companies to spend at least 80% of the premiums collected from policyholders on actual medical care and healthcare quality improvement activities.

This means that for every dollar paid in premiums, at least 80 cents must go toward clinical services such as doctor visits, hospital stays, prescriptions, preventive care, and initiatives that improve patient outcomes.

The remaining 20% can be used for administrative costs, marketing, profit, and overhead. If an insurance company fails to meet this medical loss ratio (MLR), it must issue rebates to policyholders. This rule applies to group health plans in Fort Worth and across the United States, ensuring greater accountability and value for employers and employees who purchase group coverage.

Understanding the Medical Loss Ratio (MLR) in Group Health Insurance

- The Medical Loss Ratio is a key metric used to measure how efficiently an insurance company uses premium dollars. For group health plans in Fort Worth with fewer than 51 employees, insurers must meet an 80% MLR, meaning 80% of collected premiums must fund healthcare services.

- If an insurer spends less than 80% on medical claims and quality improvements, they are required to refund the difference to policyholders in the form of rebates. These rebates are typically issued annually and provide tangible financial benefits to employers and employees.

- The MLR standard promotes transparency and incentivizes insurance companies to prioritize patient care over excessive administrative spending, helping Fort Worth businesses ensure they receive fair value from their group health coverage.

How the 80/20 Rule Affects Employers in Fort Worth

- Employers sponsoring group health plans in Fort Worth benefit from the 80/20 rule because it ensures that a significant portion of premium payments directly supports employee healthcare rather than insurer profits or overhead.

- When insurance companies fail to meet the MLR threshold, employers may receive rebates that can be reinvested into the business, used to reduce future premiums, or distributed to employees, depending on compliance guidelines.

- This rule also encourages employers to evaluate insurance carriers based on efficiency and value, fostering competition among insurers to offer more cost-effective and medically focused plans tailored to Fort Worth’s workforce needs.

Implications for Employees Covered Under Fort Worth Group Health Plans

- Employees benefit indirectly from the 80/20 rule because it ensures that their employer’s healthcare spending prioritizes actual medical services, leading to better access to care, prescription coverage, preventive screenings, and hospitalizations.

- While employees do not typically receive rebates directly, employers who get rebates may choose to pass savings on through lower premiums, enhanced benefits, or direct payments, improving overall employee satisfaction with their health coverage.

- The regulation increases trust in health insurance providers by holding them accountable for how premiums are spent, giving employees confidence that their healthcare dollars are being used appropriately within the Fort Worth group insurance market.

Frequently Asked Questions

What is Fort Worth Group Health Insurance?

Fort Worth Group Health Insurance offers health coverage to employees of businesses in the Fort Worth area. It allows employers to provide medical, dental, and vision benefits to their staff at lower costs due to group rates. These plans are typically more affordable and comprehensive than individual policies, improving employee satisfaction and retention. Employers can choose from various plans tailored to their workforce’s needs through providers and brokers serving the North Texas region.

Who qualifies for a group health insurance plan in Fort Worth?

Businesses with at least one full-time employee besides the owner qualify for group health insurance in Fort Worth. Most insurers require that the employer contribute a certain percentage toward employee premiums and that coverage be offered to all eligible employees. Small businesses with 2–50 employees often use the Small Business Health Options Program (SHOP), while larger companies may access fully insured or self-funded group plans through private carriers or brokers.

What are the benefits of offering group health insurance to employees?

Offering group health insurance in Fort Worth helps attract and retain top talent, increases employee productivity, and enhances workplace morale. Employers often enjoy tax advantages and can deduct premium contributions. Group plans provide access to comprehensive coverage with lower out-of-pocket costs for employees, including preventive care and prescription drugs. Additionally, participating in group plans can lead to better health outcomes and reduced absenteeism across the organization.

How can a Fort Worth business choose the right group health insurance plan?

A Fort Worth business should assess its budget, employee needs, and desired level of coverage when selecting a group health plan. It's wise to consult a licensed insurance broker who specializes in group benefits and knows local market options. Comparing premiums, provider networks, deductibles, and covered services across multiple insurers helps identify the best fit. Employers should also gather employee feedback and consider offering multiple plan choices to accommodate diverse healthcare needs.

Leave a Reply