Health Insurance And Hiv

Access to health insurance plays a critical role in the management and treatment of HIV. For individuals living with HIV, consistent medical care, antiretroviral therapy, and regular monitoring are essential to maintaining health and preventing transmission.

However, navigating health insurance systems can be complex and challenging, particularly for marginalized populations. Coverage disparities, high out-of-pocket costs, and stigma remain significant barriers.

In recent years, policy changes and expanded insurance options under initiatives like the Affordable Care Act have improved access for many. Still, gaps persist, underscoring the need for continued reform to ensure equitable, affordable, and comprehensive health coverage for all people affected by HIV.

Cheap Small Business Auto Insurance

Cheap Small Business Auto InsuranceUnderstanding the Intersection of Health Insurance and HIV Care

Access to comprehensive health insurance is a critical factor in managing HIV effectively and improving long-term health outcomes for people living with the virus. With the advent of advanced antiretroviral therapies, HIV has transformed from a fatal diagnosis into a manageable chronic condition—provided that individuals can access consistent medical care and prescribed medications.

However, disparities in health insurance coverage can significantly affect treatment adherence, viral suppression rates, and overall quality of life. In the United States and many other countries, health insurance plans vary widely in their coverage of HIV-related services, including testing, specialist visits, lab monitoring, and prescription drugs like antiretrovirals.

Navigating these systems often requires awareness of patient rights, available public programs such as Medicaid or the Ryan White HIV/AIDS Program, and protections provided by laws like the Affordable Care Act (ACA), which prohibits denial of coverage based on pre-existing conditions such as HIV. Ensuring equitable access to health insurance is therefore not only a medical necessity but a public health imperative to reduce transmission and promote health equity.

How Health Insurance Coverage Impacts HIV Treatment Access

Health insurance plays a pivotal role in determining how quickly and effectively individuals with HIV can access life-saving treatments. Without insurance, the cost of antiretroviral therapy (ART) can exceed $20,000 per year, placing it out of reach for many.

Cheap Auto Insurance Jacksonville Fl

Cheap Auto Insurance Jacksonville FlInsured individuals are more likely to initiate ART soon after diagnosis, adhere to treatment regimens, and achieve viral suppression, reducing both disease progression and transmission risk. Private insurance, Medicaid, and Medicare all offer varying levels of coverage for HIV care, but patients may face challenges such as high deductibles, limited provider networks, or prior authorization requirements.

Moreover, those who are uninsured or underinsured can turn to federal assistance programs like the Ryan White HIV/AIDS Program, which fills coverage gaps by providing medications, medical care, and support services. Expanding insurance coverage through policy initiatives and reducing administrative barriers are essential steps in ensuring uninterrupted access to HIV care for all populations.

Legal Protections for People with HIV in Health Insurance

Individuals living with HIV are protected under several key legal frameworks that prevent discrimination in health insurance.

In the United States, the Affordable Care Act (ACA) bans insurers from denying coverage or charging higher premiums based on pre-existing conditions, including HIV. Additionally, the Americans with Disabilities Act (ADA) recognizes HIV as a disability, offering protections in healthcare settings and employment-based insurance.

Cheap Auto Insurance Lakeland Fl

Cheap Auto Insurance Lakeland FlThe Health Insurance Portability and Accountability Act (HIPAA) safeguards patient privacy by restricting the unauthorized disclosure of HIV status. These laws collectively ensure that people with HIV can seek treatment without fear of stigma or financial penalties.

However, awareness of these protections remains uneven, and enforcement can vary—especially in regions with limited access to legal or medical advocacy resources. It is crucial for patients and providers alike to understand these rights to advocate effectively for fair and equitable insurance practices.

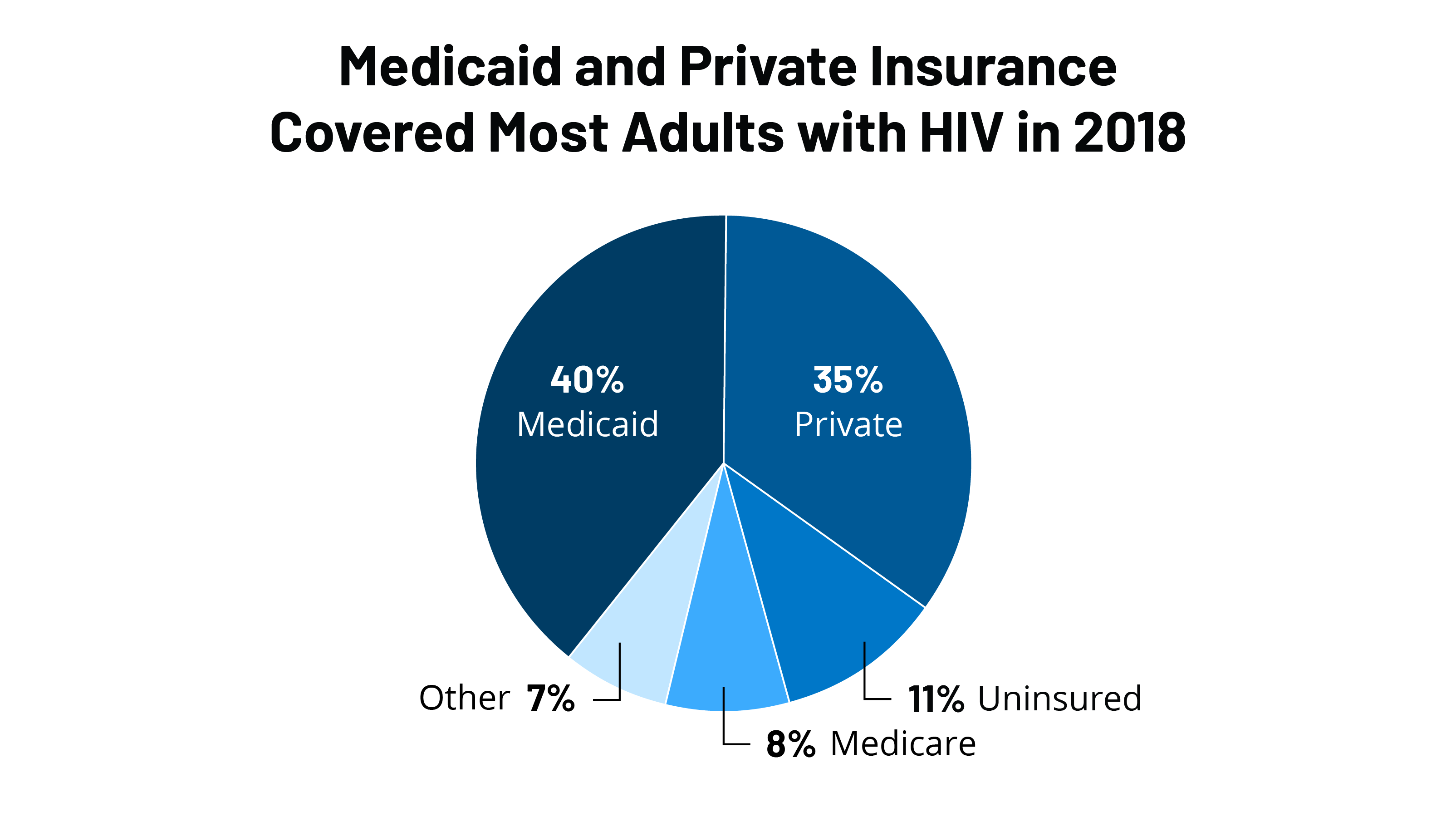

Public and Private Insurance Options for HIV Care

A variety of public and private health insurance options are available to cover HIV-related care, each with distinct benefits and limitations. Medicaid provides comprehensive coverage for low-income individuals and is a major source of care for people with HIV, especially in states that expanded eligibility under the ACA.

Medicare serves those over 65 or with long-term disabilities, including advanced HIV, and includes prescription drug coverage through Part D. Private insurance plans, whether employer-sponsored or purchased through marketplaces, must cover essential health benefits, including prescription drugs and preventive services, though cost-sharing can still pose barriers.

Cheapest Auto Insurance In Connecticut

Cheapest Auto Insurance In ConnecticutFor those outside these systems, the Ryan White HIV/AIDS Program acts as a safety net, funding medical visits, medications, mental health services, and transportation support. Choosing the right insurance requires understanding formularies, provider networks, and out-of-pocket costs to ensure continuous, effective HIV management.

| Insurance Type | Covers Antiretrovirals? | Eligibility Requirements | Key Benefits |

|---|---|---|---|

| Medicaid | Yes, comprehensive | Low income, varies by state | No premiums, low co-pays, full HIV care coverage |

| Medicare | Yes (Part D for drugs) | Age 65+ or disabled | Wide provider access, includes hospital and drug coverage |

| Private Insurance | Yes, under ACA rules | Employment or marketplace enrollment | Flexible plans, but varying deductibles and networks |

| Ryan White Program | Yes (for uninsured/underinsured) | HIV-positive, income-limited, uninsured | Free medications, medical visits, support services |

Comprehensive Guide to Health Insurance and HIV: Coverage, Costs, and Care Options

Does health insurance provide coverage for individuals diagnosed with HIV?

Coverage for HIV Treatment Under Health Insurance Plans

- Most private health insurance plans in the United States, including those purchased through the Health Insurance Marketplace, provide coverage for individuals diagnosed with HIV. These plans are required by the Affordable Care Act (ACA) to cover essential health benefits, including prescription drugs, outpatient care, hospitalization, and preventive services, all of which are critical for HIV management.

- Medicaid and Medicare also offer comprehensive coverage for people living with HIV, especially for low-income individuals and those who have developed AIDS-related complications. Medicaid coverage varies by state, but all states generally include antiretroviral therapy (ART) medications and regular laboratory monitoring.

- Insurance providers cannot deny coverage or charge higher premiums based on an HIV diagnosis, as this is considered a pre-existing condition protected under the ACA. This ensures that individuals receive continuous and equitable access to necessary medical care without discrimination.

Out-of-Pocket Costs and Financial Assistance Programs

- While health insurance covers many HIV-related services, individuals may still face out-of-pocket expenses such as copayments, deductibles, and coinsurance. These costs can vary significantly depending on the specific insurance plan and the medications prescribed.

- Fortunately, several financial assistance programs help reduce these costs. The Ryan White HIV/AIDS Program, for instance, provides services such as medication assistance, medical care, and support services for those who are underinsured or uninsured.

- Pharmaceutical companies often offer patient assistance programs (PAPs) that provide free or low-cost antiretroviral drugs to eligible individuals. Additionally, some nonprofit organizations and community health centers also offer grants or sliding-scale fee structures based on income.

Access to Preventive and Support Services

- Health insurance plans typically include coverage for preventive services related to HIV, such as screening tests, counseling, and pre-exposure prophylaxis (PrEP) for individuals at high risk of acquiring HIV. These services are often provided at no additional cost under ACA guidelines.

- Many insurance policies also support access to mental health services, substance use treatment, and case management, all of which play a vital role in the holistic care of individuals living with HIV. These supportive services help improve treatment adherence and overall quality of life.

- Continuity of care is facilitated through insurance coverage that allows patients to see specialists like infectious disease doctors and access regular CD4 and viral load testing. Ensuring uninterrupted access to these services is essential for maintaining viral suppression and preventing disease progression.

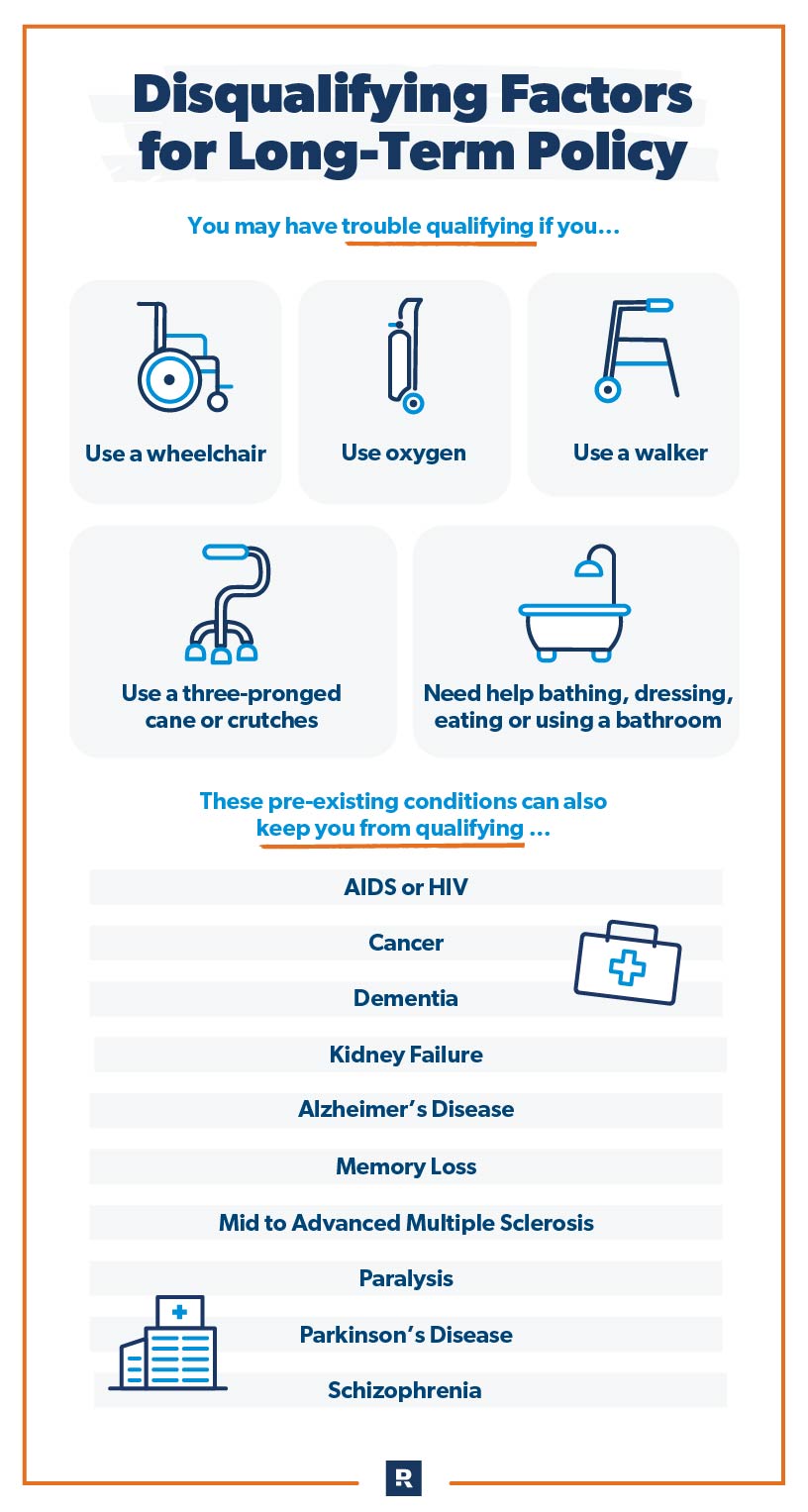

Can you get long-term care insurance if you have HIV?

Eligibility for Long-Term Care Insurance with HIV

- Individuals living with HIV can, in some cases, qualify for long-term care insurance, although eligibility depends on several factors including the stage of the disease, overall health, and insurance provider guidelines. In the past, an HIV diagnosis often led to automatic denial, but medical advances have changed this landscape significantly.

- Today, thanks to effective antiretroviral therapy (ART), many people with HIV maintain low viral loads and high CD4 counts, which insurers may view as indicators of stable health. As a result, some underwriters may consider applicants with well-managed HIV on a case-by-case basis.

- It is important to work with experienced insurance agents who understand how different companies evaluate HIV status and who can guide applicants toward insurers more likely to offer coverage under such circumstances.

Factors Insurers Evaluate for HIV-Positive Applicants

- Insurance companies typically review medical records, including viral load, CD4 count, and adherence to treatment, when assessing risk for long-term care coverage. Stability over time—such as consistent lab results and no recent hospitalizations—is often crucial to approval.

- Age at the time of application also plays a significant role; younger applicants with controlled HIV may stand a better chance of qualifying than those with advanced age or additional comorbidities like cardiovascular disease or diabetes.

- Insurers may also consider the cause of HIV transmission, frequency of medical visits, and whether the applicant has disclosed other health issues, all of which can influence underwriting decisions and potential premium rates.

Alternative Options if Traditional Coverage Is Denied

- If traditional long-term care insurance is unavailable due to HIV status, some individuals explore hybrid life insurance policies that include long-term care benefits. These policies combine life insurance with a rider that allows access to funds if long-term care is needed.

- Another option is short-term care insurance, which offers limited coverage for a defined period and may have less stringent health requirements, making it more accessible for people with chronic conditions like HIV.

- Additionally, setting up a dedicated savings or investment plan designed to cover future care expenses can serve as a practical alternative, especially when paired with legal tools like trusts to protect assets and ensure funds are used appropriately.

Frequently Asked Questions

Can I get health insurance if I have HIV?

Yes, you can get health insurance if you have HIV. Under the Affordable Care Act in the U.S., insurers cannot deny coverage or charge higher premiums based on pre-existing conditions like HIV. All health plans must provide essential health benefits, including prescription drugs and preventive services. You can obtain coverage through private insurers, Medicaid, or the Health Insurance Marketplace, ensuring access to necessary care without discrimination.

Commercial Auto Insurance Asheville Nc

Commercial Auto Insurance Asheville NcDoes health insurance cover HIV treatment and medications?

Yes, most health insurance plans cover HIV treatment and antiretroviral medications. Coverage includes doctor visits, lab tests, and prescribed drugs under the plan’s formulary. The Affordable Care Act mandates that insurance plans cover essential health benefits, which encompass chronic disease management. However, specific medications may vary by plan, so it’s important to check your formulary or contact your insurer to confirm coverage details for HIV-related care.

Are there special health insurance programs for people with HIV?

Yes, there are programs that help people with HIV access health insurance and care. The Ryan White HIV/AIDS Program provides services like medical care, medications, and insurance premium assistance for low-income individuals. It does not replace health insurance but helps fill gaps in coverage. Many states also offer Medicaid expansion, which can cover low-income individuals living with HIV, ensuring continuous access to treatment and support services.

No, your HIV status is protected by privacy laws like HIPAA in the U.S. Health insurance companies cannot share your medical information, including HIV status, without your consent. This information is kept confidential and is only used for treatment, billing, or insurance purposes. Unauthorized disclosure is illegal. You control who receives your health data, ensuring your privacy and protecting you from discrimination based on your medical condition.

Leave a Reply