Health Insurance Coverage For Glp 1

Access to GLP-1 receptor agonists, a class of medications widely used in managing type 2 diabetes and, more recently, obesity, increasingly depends on health insurance coverage.

These drugs, including semaglutide and liraglutide, have demonstrated significant benefits in improving glycemic control and promoting weight loss. However, their high costs place them out of reach for many without insurance support.

Coverage policies vary widely among public and private insurers, often involving strict eligibility requirements, prior authorizations, and step therapy protocols. As demand for GLP-1 treatments grows, patients, providers, and policymakers face challenges in navigating affordability and access, making equitable insurance coverage a critical issue in modern healthcare.

Cheap Auto Insurance Jacksonville Fl

Cheap Auto Insurance Jacksonville FlUnderstanding Health Insurance Coverage for GLP-1 Medications

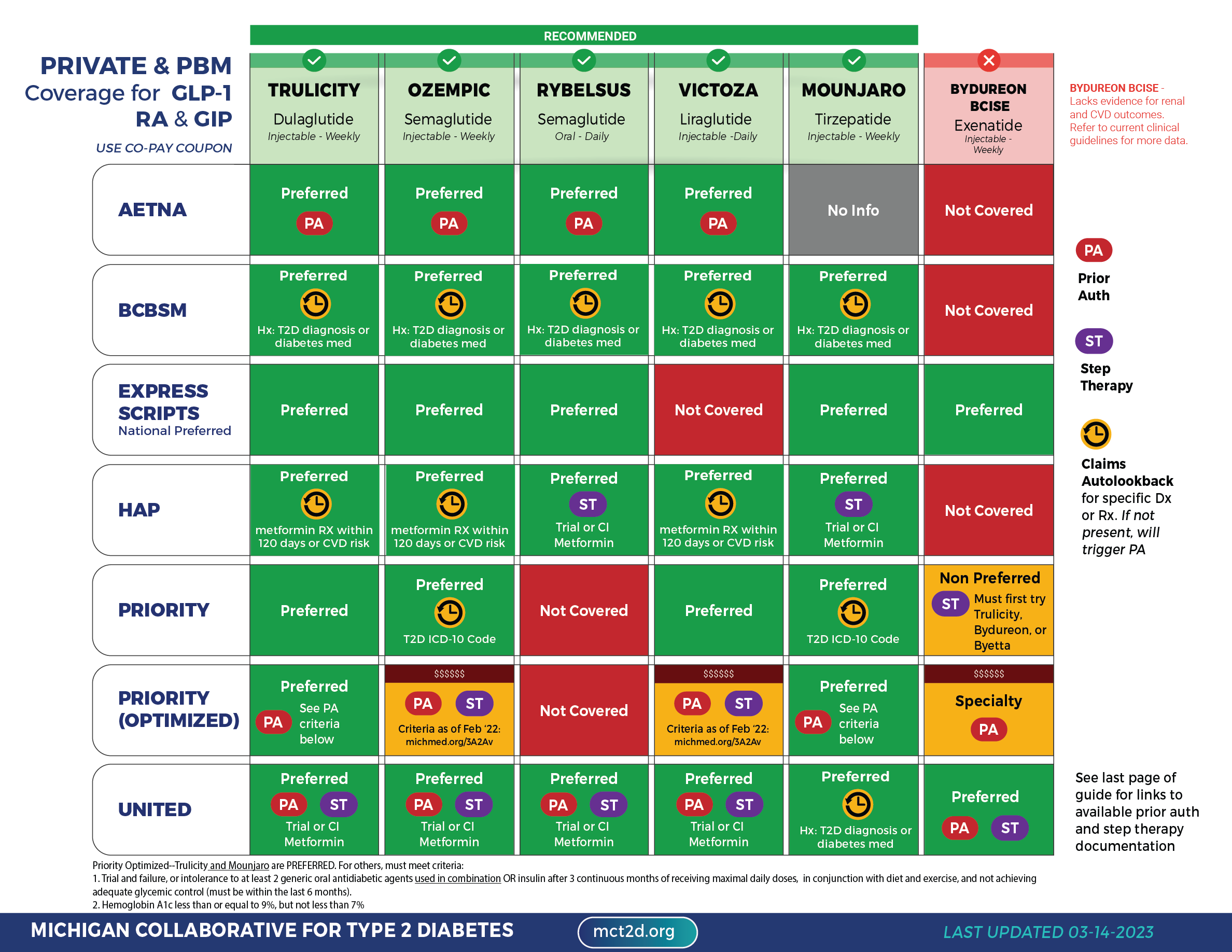

GLP-1 receptor agonists, such as semaglutide (Ozempic, Wegovy), liraglutide (Victoza, Saxenda), and dulaglutide (Trulicity), are increasingly prescribed for the management of type 2 diabetes and, in some cases, for chronic weight management. As their popularity grows—driven by proven efficacy in lowering blood sugar and promoting weight loss—patients are becoming more concerned about health insurance coverage and out-of-pocket costs.

While many private insurers, Medicare Advantage plans, and Medicaid programs do offer some level of coverage for these medications, the extent and conditions vary widely. Coverage often depends on factors such as the specific indication (diabetes vs. obesity), prior authorization requirements, step therapy protocols, and the patient’s formulary tier. Understanding these nuances is essential for patients seeking affordable access to these life-changing treatments.

How Insurance Plans Classify GLP-1 Medications

Insurance companies categorize GLP-1 medications within their drug formularies, typically placing them in higher cost tiers, such as Tier 3 or specialty tiers, which results in higher co-pays or coinsurance for patients.

The classification often hinges on whether the drug is approved for diabetes treatment or weight loss, as coverage for obesity-related prescriptions is frequently more restricted. For instance, Wegovy and Saxenda—approved specifically for chronic weight management—are less consistently covered than Ozempic or Trulicity, which are primarily indicated for type 2 diabetes.

Cheap Auto Insurance Lakeland Fl

Cheap Auto Insurance Lakeland FlSome insurers may only cover GLP-1 drugs after patients fail to respond to lower-cost alternatives like metformin or lifestyle interventions, a process known as step therapy. Knowing where a specific GLP-1 medication falls within a patient’s insurance plan is crucial for anticipating costs and navigating coverage rules.

One of the most common hurdles in accessing GLP-1 medications is the prior authorization (PA) requirement imposed by health insurers.

This process demands that healthcare providers submit detailed medical documentation proving the medical necessity of the drug—for example, demonstrating a patient’s HbA1c level above a certain threshold or a BMI that meets obesity criteria. Insurers may also require proof that the patient has attempted and failed other treatments before approving GLP-1 therapy.

These administrative barriers, while intended to manage costs, often delay treatment and create frustration for patients and physicians. Additionally, some plans impose quantity limits or restrict coverage to certain dosages, further complicating access. Patients should proactively consult their insurer or pharmacy benefit manager (PBM) to understand PA requirements and reduce potential delays.

Cheapest Auto Insurance In Connecticut

Cheapest Auto Insurance In ConnecticutCost Variability Across Different Insurance Types

The out-of-pocket cost for GLP-1 medications can vary dramatically depending on the type of insurance a patient holds.

For example, Medicare Part D plans may cover GLP-1 drugs for diabetes but frequently exclude weight loss formulations, leaving patients responsible for full costs—sometimes over $1,000 per month. In contrast, some employer-sponsored health plans provide partial coverage with co-pays ranging from $50 to $200 per month, though higher tiers can lead to coinsurance of 25–50%.

Commercial insurers like UnitedHealthcare, Aetna, or Cigna typically have restrictive policies around obesity-related prescriptions but may be more lenient for diabetes indications. Medicaid coverage varies significantly by state, with some states offering robust access while others have strict limitations. Below is a comparative overview of typical coverage scenarios:

| Insurance Type | Coverage for GLP-1 (Diabetes) | Coverage for GLP-1 (Weight Loss) | Average Monthly Out-of-Pocket Cost |

|---|---|---|---|

| Medicare Part D | Generally Covered | Rarely Covered | $0–$1,300 |

| Employer-Sponsored Plan | Covered (with PA) | Sometimes Covered | $50–$500 |

| Medicaid (State Varies) | Variable | Limited or No Coverage | $0–$200 |

| Commercial Insurance (e.g., UnitedHealthcare) | Covered (with Step Therapy) | Strict Criteria | $100–$800 |

Understanding GLP-1 Health Insurance Coverage: A Comprehensive Guide

Which health insurance plans cover GLP-1 medications for weight loss?

Commercial Auto Insurance Asheville Nc

Commercial Auto Insurance Asheville NcPrivate Health Insurance Plans and GLP-1 Coverage

Several private health insurance providers in the United States offer coverage for GLP-1 receptor agonists when prescribed for weight loss, though approval often depends on specific medical criteria. Many insurers require documentation of obesity-related comorbidities, such as type 2 diabetes, hypertension, or sleep apnea, before authorizing these medications.

Additionally, prior authorization is commonly mandated, meaning healthcare providers must submit clinical justifications to the insurer. While some plans may cover drugs like semaglutide (Wegovy) or liraglutide (Saxenda) under their pharmacy benefits, others may categorize them as investigational or cosmetic and deny coverage altogether.

- UnitedHealthcare may cover certain GLP-1s for weight loss if BMI thresholds are met and other health conditions are present, with prior authorization required.

- Anthem Blue Cross Blue Shield varies by state, but generally covers GLP-1 medications when clinical guidelines are followed and medical necessity is proven.

- Aetna often requires a BMI of 30 or higher (or 27 with comorbidities) and evidence of failed lifestyle interventions before approving coverage.

Medicare, Medicaid, and Government Programs

Medicare Part D plans do not currently cover GLP-1 medications for the sole purpose of weight loss, as the program excludes drugs used exclusively for managing obesity. However, if a GLP-1 agonist like semaglutide is prescribed for type 2 diabetes (e.g., Ozempic), it may be covered under certain Part D plans.

Medicare Advantage plans may have slightly different formulary rules, but most still follow the exclusion for weight-loss-specific use. Medicaid coverage varies significantly by state, with a few states such as Oregon and Massachusetts offering limited coverage for obesity treatment under specific programs, but widespread access remains limited.

- Traditional Medicare (Parts A and B) does not cover GLP-1 drugs for weight loss, considering them non-essential.

- Medicare Part D may cover GLP-1 medications if they are approved for diabetes management rather than weight reduction.

- State Medicaid programs like those in Vermont and California may provide case-by-case approval, often requiring strict documentation of medical necessity.

Employer-Sponsored Insurance and Formulary Restrictions

Employer-sponsored health plans typically follow national pharmacy benefit manager (PBM) guidelines, which influence whether GLP-1 medications are included in their formulary for weight loss. Coverage can vary widely depending on the employer and the plan design, with high-tier copays or step therapy requirements common.

Many plans enforce step therapy, requiring patients to try and fail cheaper weight-loss medications or lifestyle programs before approving GLP-1s. Some self-insured employers are beginning to include these medications as part of wellness initiatives, especially if long-term health cost savings are projected.

- Large employers like Amazon and Alphabet have started covering GLP-1 drugs through partnerships with telehealth weight-loss programs.

- PBMs such as CVS Caremark and Express Scripts often place GLP-1s on higher formulary tiers, resulting in out-of-pocket costs exceeding $1,000 per month without subsidies.

- Some employers are revising wellness policies to include obesity as a treatable condition, expanding access to GLP-1 therapy under medical rather than pharmacy benefits.

What Is the Best Health Insurance Coverage for GLP-1 Medications?

Understanding Insurance Coverage for GLP-1 Medications

- GLP-1 receptor agonists, such as semaglutide (Ozempic, Wegovy), liraglutide (Victoza, Saxenda), and dulaglutide (Trulicity), are widely prescribed for type 2 diabetes and, increasingly, for weight management. However, their high cost often necessitates insurance coverage to make treatment accessible.

- Most major health insurance providers, including Aetna, UnitedHealthcare, and Cigna, do offer coverage for GLP-1 medications, but typically only under certain conditions such as a confirmed diagnosis of type 2 diabetes or obesity with a BMI over 30 (or 27 with comorbidities).

- Coverage often depends on medical necessity, prior authorization, and step therapy requirements, meaning patients may need to try and fail on alternative treatments like metformin before gaining access to GLP-1 drugs.

Types of Insurance Plans That Offer the Best GLP-1 Coverage

- Employer-sponsored health plans, particularly those categorized as PPOs (Preferred Provider Organizations), often provide more comprehensive coverage for GLP-1 medications compared to HMOs. These plans usually have broader formularies and fewer restrictions.

- Medicare Part D prescription drug plans and Medicare Advantage plans vary significantly; some cover GLP-1 drugs for diabetes but exclude them for obesity-related weight loss. Patients should review plan-specific formularies annually during open enrollment.

- Private marketplace plans under the Affordable Care Act (ACA) may include GLP-1 coverage, but it frequently comes with high out-of-pocket costs, tiered pricing (e.g., Tier 3 or specialty drugs), and strict utilization management protocols.

Strategies to Maximize GLP-1 Medication Insurance Benefits

- Patients should work with their healthcare providers to ensure all necessary documentation—such as diagnosis codes, treatment history, and BMI records—is submitted to support medical necessity and improve the chances of prior authorization approval.

- Using manufacturer assistance programs, like those from Novo Nordisk or Eli Lilly, can reduce out-of-pocket costs even when insurance requires high copays or denies coverage initially.

- Reviewing the plan’s appeals process is crucial. If a claim is denied, patients can challenge the decision with clinical evidence, potentially securing coverage after an initial rejection.

What Does Health Insurance Cover for GLP-1 Medications?

Understanding Medical Coverage for GLP-1 Agonists

Health insurance plans may cover GLP-1 receptor agonists, but the extent of coverage depends heavily on the specific insurance provider, policy type, and medical necessity.

These medications, originally developed for type 2 diabetes management—such as semaglutide (Ozempic), liraglutide (Victoza), and dulaglutide (Trulicity)—are increasingly prescribed for weight management, which influences insurance decisions.

Most insurers require a formal diagnosis of type 2 diabetes or, in some cases, obesity with related comorbidities before approving coverage. Prior authorization is commonly required, meaning doctors must submit clinical documentation justifying the prescription. Even when approved, patients might still face high co-pays or coinsurance depending on their plan's formulary and tier placement of the medication.

- Insurance plans typically cover GLP-1 medications when prescribed for FDA-approved uses, such as managing type 2 diabetes.

- Some Medicare Advantage plans and private insurers are beginning to cover GLP-1 drugs for weight loss if specific health criteria are met.

- Patients may need to try and fail on other treatments like lifestyle modifications or oral medications before insurance authorizes GLP-1 therapy.

Factors Influencing Insurance Approval

Several factors determine whether a health insurance provider will approve coverage for GLP-1 medications. Primary considerations include the patient's diagnosis, body mass index (BMI), and presence of comorbid conditions such as hypertension, sleep apnea, or cardiovascular disease.

Insurers often require a BMI above a certain threshold—commonly 30 or higher, or 27 with at least one weight-related condition—for weight management prescriptions.

In addition, documentation from a healthcare provider detailing failed attempts at weight loss through diet, exercise, or alternative medications can be necessary. The prescribing physician must also adhere to the insurer's prior authorization process, which may involve submitting lab results, medical history, and a treatment plan.

- Insurers frequently use medical guidelines, such as those from the American Diabetes Association or Endocrine Society, to evaluate eligibility.

- Patients with higher BMIs and documented comorbidities are more likely to receive approval for GLP-1 coverage.

- Policies may vary between commercial insurance, Medicaid, and Medicare, with some programs offering limited or no coverage for off-label weight loss use.

Out-of-Pocket Costs and Financial Assistance Programs

Even when health insurance provides partial coverage for GLP-1 medications, patients often face significant out-of-pocket expenses due to high drug costs and variable co-insurance rates. Monthly prices for these injectable medications can range from several hundred to over a thousand dollars, and insurance may place them on a high-tier formulary, resulting in greater patient responsibility. Deductibles must typically be met before coverage begins, further increasing upfront costs.

To mitigate these financial barriers, pharmaceutical companies often offer patient assistance programs or savings cards that reduce or eliminate co-pays for eligible individuals. Some nonprofit organizations and pharmacy discount programs may also provide support for uninsured or underinsured patients needing long-term treatment.

- Many manufacturers provide co-pay assistance programs that can lower monthly costs to as little as $25 for commercially insured patients.

- Patients without insurance or those on Medicare may qualify for free medication through manufacturer-sponsored patient support programs.

- Pharmacy benefit managers sometimes negotiate lower prices, and using specific in-network pharmacies can result in cost savings.

Frequently Asked Questions

Does health insurance typically cover GLP-1 medications for weight loss?

Most health insurance plans cover GLP-1 medications when prescribed for FDA-approved conditions like type 2 diabetes. Coverage for weight loss varies significantly by provider and plan. Some insurers may cover these drugs for weight management if specific criteria are met, such as a diagnosis of obesity and failed attempts at other weight-loss methods. Always check with your insurance provider to understand your benefits and potential out-of-pocket costs.

Which GLP-1 drugs are most commonly covered by insurance?

Insurance plans most commonly cover GLP-1 medications like liraglutide (Victoza, Saxenda) and dulaglutide (Trulicity) when used to treat type 2 diabetes. Coverage for other drugs such as semaglutide (Ozempic, Wegovy) depends on medical necessity and plan policies. Wegovy is more likely to be covered for weight management, while Ozempic may require diabetes-related justification. Prior authorization is often required, and formulary lists vary by insurer.

How can I find out if my insurance covers GLP-1 medication?

To determine if your insurance covers GLP-1 medication, contact your provider directly or review your plan’s drug formulary online. You can also ask your pharmacist or healthcare provider to check coverage using your insurance details. Many insurers require prior authorization, so your doctor may need to submit medical records justifying the prescription. Be prepared for potential step therapy requirements before approval.

What should I do if my insurance denies coverage for a GLP-1 drug?

If your insurance denies coverage, you can appeal the decision by submitting a formal appeal with supporting documentation from your healthcare provider. Your doctor can write a letter explaining medical necessity. You may also explore patient assistance programs offered by drug manufacturers or switch to a covered alternative. Some pharmacies offer cash discount programs that may reduce out-of-pocket costs even without insurance coverage.

Leave a Reply