Home insurance climate-related risks coverage

Climate change is reshaping the landscape of home insurance as extreme weather events become more frequent and severe.

From wildfires and hurricanes to flooding and prolonged droughts, homeowners face growing risks that traditional policies may not fully cover. Insurers are responding by reassessing coverage options, adjusting premiums, and in some cases, withdrawing from high-risk areas altogether.

Understanding climate-related risks is now essential for protecting one’s property and financial well-being. This article explores how home insurance is evolving to address environmental challenges, what coverage options exist for climate-related damages, and what homeowners should consider when evaluating their policies in an era of increasing climate uncertainty.

Medical Underwriting Impact On Life Insurance Premiums

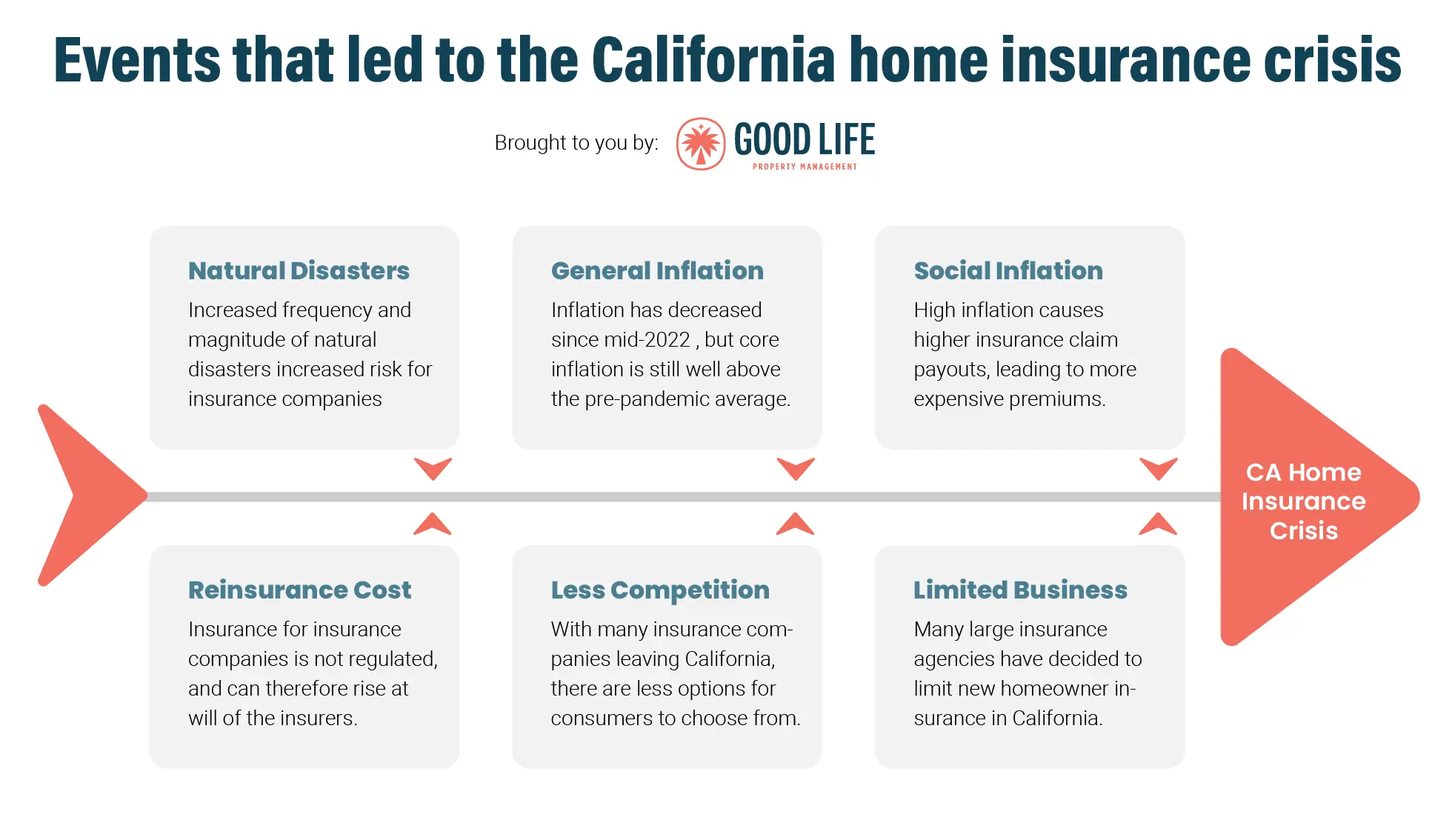

Medical Underwriting Impact On Life Insurance PremiumsAs climate change intensifies, weather events like hurricanes, wildfires, floods, and severe storms are becoming more frequent and destructive. Home insurance has evolved to address these growing climate-related risks, though coverage varies significantly depending on location, policy type, and insurer.

Standard homeowners’ policies typically cover certain weather-related damages—such as wind or hail—but often exclude losses from floods or earthquakes, which require separate endorsements or standalone policies. Insurers are increasingly leveraging data analytics and climate modeling to assess regional risk, adjust premiums, and modify underwriting criteria.

In high-risk zones, policyholders may face challenges such as increased premiums, reduced coverage options, or difficulty securing insurance at all. As a result, both insurers and homeowners are adapting through risk mitigation strategies, improved building standards, and government-supported insurance programs.

Types of Climate Risks Covered by Standard Home Insurance

Standard home insurance policies generally provide coverage for several climate-related perils, including windstorms, hail, lightning strikes, and damage from sudden events like falling trees during storms. These policies typically protect the dwelling, other structures, personal property, and liability.

Metropolitan Life Auto Insurance

Metropolitan Life Auto InsuranceHowever, critical exclusions often apply—most notably for flood damage caused by overflowing rivers or storm surges, which is not covered under traditional policies and requires a separate flood insurance policy, usually available through the National Flood Insurance Program (NFIP) or private insurers.

Similarly, damage from seismic events like earthquakes is also excluded and needs additional coverage. It’s essential for homeowners in climate-vulnerable regions to carefully review their policy declarations to understand which perils are included and identify gaps in protection.

| Climate-Related Peril | Typically Covered? | Additional Coverage Needed? |

|---|---|---|

| Windstorm / Hurricane | Yes (varies by region) | Possible windstorm deductible or separate policy in high-risk areas |

| Flood | No | Yes – Flood insurance through NFIP or private market |

| Wildfire | Yes | Rarely; but insurers may restrict policies in high-risk zones |

| Earthquake | No | Yes – Earthquake insurance endorsement |

| Hail and Lightning | Yes | No |

The rising frequency and severity of climate-driven disasters have a direct impact on both the availability and affordability of home insurance.

In regions increasingly prone to wildfires—such as California—or coastal hurricane zones like Florida, insurers are responding by raising premiums, increasing deductibles, or withdrawing from markets altogether. Some homeowners face non-renewals or must turn to state-run “insurance of last resort” programs, such as FAIR (Fair Access to Insurance Requirements) plans, which offer limited coverage at higher costs.

Mortgage Loan Life Insurance

Mortgage Loan Life InsuranceInsurers use predictive climate models to evaluate long-term risk, which influences their willingness to underwrite policies in vulnerable areas. These market shifts are pressuring governments to develop new regulatory frameworks and public-private partnerships to ensure continued access to essential insurance protection.

Mitigation Strategies to Improve Climate Risk Coverage

Homeowners can take proactive steps to reduce exposure to climate-related risks and potentially improve insurance terms.

Implementing mitigation measures such as installing storm shutters, fire-resistant roofing, elevating homes in flood-prone areas, or creating defensible space around properties in wildfire zones can make a significant difference. Many insurers offer premium discounts for such upgrades, recognizing their effectiveness in reducing claims.

Additionally, updating older homes to meet modern building codes enhances resilience. Community-level efforts, including improved land-use planning and infrastructure investment, also play a crucial role. Ultimately, a combination of individual action and systemic change is needed to sustain affordable and comprehensive home insurance in an era of escalating climate risk.

Most Reputable Buyers For Life Insurance Policies

Most Reputable Buyers For Life Insurance Policies

Protection Against Wind and Hail Damage

Standard home insurance policies typically include coverage for structural and personal property damage caused by windstorms and hail, which are common climate-related risks. As extreme weather events become more frequent due to climate change, homes in hurricane-prone regions or areas with severe thunderstorms benefit from this protection.

Insurers generally cover repairs to roofs, siding, windows, and other exterior components damaged by high winds. Personal belongings inside the home, such as furniture and electronics, may also be reimbursed if damaged by these perils.

- Wind damage coverage includes repairs to roofs, fences, and exterior structures caused by strong winds from hurricanes, tornadoes, or severe storms.

- Hail protection covers dents, cracks, or punctures in roofing materials, gutters, and siding resulting from intense hail storms.

- Most policies provide both dwelling and personal property protection for wind and hail events, though specific limits and deductibles may apply depending on the geographic location.

Water Damage from Weather Events (Excluding Flooding)

Home insurance often covers water damage that results indirectly from climate-related weather, such as rain entering through a wind-damaged roof or broken window.

National Union Life And Limb Insurance Company

National Union Life And Limb Insurance CompanyHowever, it's important to note that standard policies typically exclude damage from surface water or rising floodwaters. Coverage applies when the water intrusion is a direct result of a covered peril like windstorm damage. For instance, if a tree falls on the roof during a storm and allows rainwater inside, the resulting damage would likely be covered.

- Coverage applies to water damage caused by sudden and accidental incidents linked to covered perils, such as wind-driven rain entering through a compromised roof.

- Damage from burst pipes due to freezing temperatures, often related to extreme winter weather, is commonly included under standard policies.

- Exclusions include prolonged seepage, groundwater intrusion, or damage from overflowing rivers and storm surges—these generally require a separate flood insurance policy.

In regions increasingly affected by prolonged droughts and higher temperatures, the risk of wildfires is growing. Many home insurance policies include coverage for fire damage caused by wildfires, protecting the structure of the home, other detached structures, and personal belongings.

Some insurers in high-risk areas may require specific wildfire endorsements or impose higher deductibles. As climate conditions shift, certain carriers may also reevaluate risk profiles and adjust coverage terms accordingly.

- Fire damage from wildfires is usually covered under the dwelling and personal property sections, helping pay for rebuilding and replacement costs.

- Additional living expenses (ALE) may be included if the home becomes uninhabitable, covering temporary housing and related costs during repairs.

- Insurers in fire-prone zones may request property mitigation measures (e.g., fire-resistant roofing or defensible space) to maintain or qualify for coverage.

Flood Insurance Through the National Flood Insurance Program (NFIP) and Private Carriers

- As of 2022, standard homeowners insurance policies typically exclude flood damage, making separate flood insurance essential in climate-vulnerable areas. The National Flood Insurance Program (NFIP), administered by FEMA, offers policies that cover structural damage and personal property losses due to flooding caused by extreme weather events such as hurricanes and heavy rainfall.

- In addition to the NFIP, a growing number of private insurers began offering more competitive and flexible flood coverage options. These private policies often provide higher coverage limits, broader definitions of flood events, and faster claim processing, which is particularly beneficial in regions experiencing increased flood frequency due to climate change.

- Homeowners in high-risk flood zones—especially those in coastal or low-lying areas—are increasingly required by mortgage lenders to carry flood insurance. With climate projections indicating rising sea levels and more intense precipitation patterns, both public and private flood insurance options have become critical components of comprehensive home protection strategies.

- As wildfires became more frequent and severe in regions like California, Oregon, and Colorado, insurers introduced coverage enhancements to address fire-related risks. These include extended dwelling coverage to account for increased rebuilding costs due to fire-resistant materials and more comprehensive personal property protection for losses caused by smoke, embers, and evacuation-related damage.

- Some insurers began offering discounts or premium reductions for homes with fire mitigation features such as ember-resistant vents, ignition-resistant roofing, and defensible space around the property. These incentives encourage homeowners to invest in preventative measures that reduce vulnerability to wildfire threats exacerbated by prolonged drought and hotter temperatures.

- In high-risk areas, specialized insurance policies or state-supported FAIR (Fair Access to Insurance Requirements) plans became more common. These plans serve as insurers of last resort for properties that struggle to obtain coverage in the private market due to elevated wildfire risks linked to climate change.

Coverage for Extreme Weather Events: Windstorm and Hail Endorsements

- With the increased intensity of hurricanes and severe thunderstorms, standard home insurance policies often require additional endorsements to cover windstorm and hail damage—particularly in coastal regions and the Midwest. These endorsements provide essential protection against roof damage, broken windows, and structural compromise caused by extreme winds.

- In states like Florida, Texas, and Louisiana, insurers may exclude wind damage from standard policies, necessitating standalone windstorm insurance through state-run pools such as the Texas Windstorm Insurance Association (TWIA). These programs help bridge the gap in coverage where private insurers are unwilling to assume the risk due to climate-related storm intensification.

- Some insurers also offer upgraded materials and labor cost coverage to ensure homes can be rebuilt to modern, storm-resistant standards after catastrophic wind events. This is especially important as climate change contributes to more frequent and powerful storms, increasing repair and reconstruction expenses beyond traditional policy limits.

Coverage for Wildfire Damage

- Home insurance policies in California typically include coverage for damage caused by wildfires, which are a significant and growing risk due to climate change. This coverage generally includes the repair or rebuilding of the home’s structure, replacement of personal belongings, and additional living expenses if the home becomes uninhabitable.

- Insurers have become increasingly cautious in high-risk fire zones, often requiring homeowners to implement fire-resistant construction materials or defensible space around the property to qualify for coverage. Some insurers may also offer discounts for homes with enhanced fire protection features.

- Due to the rising frequency of wildfires, some insurance companies have stopped offering policies in certain areas or have significantly increased premiums. As a result, the California FAIR Plan serves as a last-resort option for homeowners who cannot secure coverage in the private market.

Flood Protection and Insurance Limitations

- Standard home insurance policies in California do not cover flooding, which is a growing concern due to extreme weather events, rising sea levels, and increased storm intensity linked to climate change. Homeowners in flood-prone areas must purchase separate flood insurance, typically through the National Flood Insurance Program (NFIP) or private insurers.

- Because flood risk is not uniformly addressed in standard policies, many California residents remain underinsured when it comes to water damage from heavy rains, storm surges, or overflowing rivers. Insurance providers often assess flood risk using Federal Emergency Management Agency (FEMA) flood maps, which are periodically updated to reflect changing climate conditions.

- Some insurance companies are beginning to integrate climate modeling into their underwriting processes, which can affect the availability and pricing of flood-related coverage. As climate patterns shift, the definition of a “flood-prone” area may expand, potentially increasing the number of homeowners required to carry flood insurance.

Adaptations to Earthquake and Extreme Heat Risks

- While standard home insurance in California covers many perils, earthquake damage is generally excluded and requires a separate policy or endorsement, often provided by the California Earthquake Authority. The heightened seismic activity and climate-induced changes in groundwater levels can influence subsurface stresses, potentially increasing earthquake risks.

- Extreme heat, though not directly covered as a physical damage peril, can indirectly affect home insurance through increased strain on building materials, higher risks of fire, and greater cooling system usage. Insurers may consider a home’s resilience to heat—such as insulation quality and roofing materials—when determining premiums.

- Insurers are increasingly incorporating climate data into risk assessments, leading to more precise but sometimes restrictive policies. Homes located in areas projected to face prolonged heatwaves or drought conditions may face higher premiums or stricter coverage terms, reflecting the long-term impact of climate change on property risk profiles.

Frequently Asked Questions

Standard home insurance policies often cover certain climate-related risks like windstorms, hail, and lightning damage. However, they usually exclude floods and earthquakes, which require separate policies. Coverage may vary based on location and insurer. It's important to review your policy details and consider additional coverage if you live in areas prone to wildfires, hurricanes, or rising flood risks due to climate change.

Does home insurance cover damage from flooding caused by climate change?

Most standard home insurance policies do not cover flooding, regardless of whether it's caused by climate change. Flood damage typically requires a separate flood insurance policy, often available through government programs like the National Flood Insurance Program (NFIP) in the U.S. Homeowners in flood-prone or high-risk climate areas should assess their exposure and consider purchasing flood insurance to protect against rising sea levels and extreme weather events.

Are wildfires caused by climate change covered by home insurance?

Yes, most home insurance policies cover damage caused by wildfires, including those intensified by climate change. This coverage generally includes structural damage, loss of personal belongings, and additional living expenses if the home becomes uninhabitable. However, premiums may increase in high-risk areas, and some insurers may require additional fire-resistant upgrades or even refuse coverage in extreme cases, depending on regional risk assessments.

Climate change can lead to more frequent and severe weather events, increasing risk for insurers. As a result, homeowners in vulnerable areas may see higher premiums or difficulty obtaining coverage. Insurers use climate data to adjust pricing and risk models. You can potentially reduce costs by improving home resilience—such as installing storm shutters or fire-resistant materials—and shopping around for insurers with favorable climate risk assessments.

Leave a Reply