Home insurance legal fees coverage if sued

When facing a lawsuit related to your home, legal fees can quickly become overwhelming. Home insurance legal fees coverage provides essential protection by helping to cover the costs of legal defense if you're sued for covered incidents. This type of coverage typically applies to liability claims, such as injuries occurring on your property or damage caused by you or family members.

While policies vary, many homeowners insurance plans include some form of legal expense protection, offering access to attorneys, court costs, and settlements up to policy limits. Understanding the extent of this coverage is crucial to safeguarding your financial well-being during legal disputes.

Understanding Home Insurance Legal Fees Coverage If You’re Sued

Home insurance can provide crucial protection if you're facing a lawsuit related to your property or personal liability. One often-overlooked but valuable component of standard homeowners insurance policies is coverage for legal fees if you are sued.

Liberty mutual vs state farm home insurance

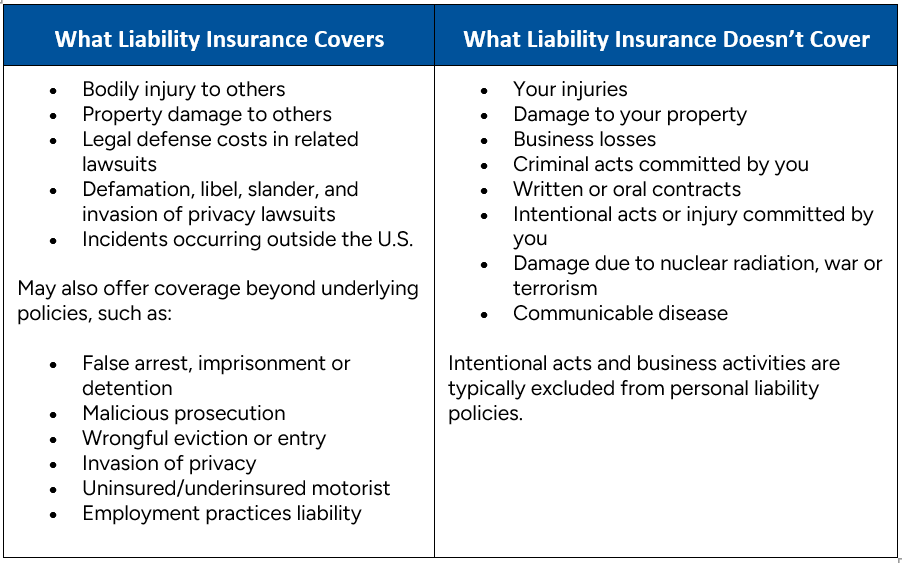

Liberty mutual vs state farm home insuranceMost homeowners policies include liability protection, typically under Coverage E, which helps pay for both damages awarded against you and the associated legal defense costs if you're held responsible for bodily injury or property damage to others. This means that if someone slips and falls on your property and decides to sue, your insurer may cover attorney fees, court costs, settlements, or judgments—up to your policy’s liability limits.

It's important to note, however, that not all lawsuits are covered; exclusions apply, especially for incidents involving intentional acts, business activities, or automobile-related claims. Understanding the scope of your policy’s legal fee coverage ensures you’re prepared should you ever face litigation.

What Legal Costs Are Covered Under Home Insurance?

Standard home insurance policies typically cover a range of legal expenses if you're sued for a covered incident. This includes fees for hiring an attorney, court filing charges, expert witness fees, and costs related to gathering evidence.

Insurers usually appoint a lawyer to defend you as part of your personal liability coverage, which activates when a third party files a claim or lawsuit due to bodily injury or property damage occurring on your premises or caused by you or members of your household. For instance, if a guest is injured by a broken stair and you're sued for negligence, your policy may pay all legal defense costs—even if the lawsuit is groundless.

Long term care insurance for in home care services middleton wi

Long term care insurance for in home care services middleton wiHowever, coverage is limited to specified perils and subject to the liability limit in your policy, commonly starting at $100,000 but often extendable to $500,000 or more through an umbrella policy.

Common Scenarios That Trigger Legal Fee Coverage

Legal fee coverage under home insurance often comes into play during real-world situations involving accidental injuries or property damage. Typical examples include a neighbor tripping over a garden hose on your lawn, a visitor getting hurt due to a loose railing, or accidental water damage from a burst pipe affecting a neighboring unit. In such cases, if the injured party pursues legal action, your home insurance’s liability provision will likely cover the cost of legal representation and settlement negotiations.

Another common scenario involves defamation claims, where you're accused of harming someone’s reputation through spoken or written statements—some policies extend coverage to civil liability for libel or slander. It’s important to act quickly by notifying your insurer as soon as legal action is threatened, since timely reporting is crucial for activating your legal defense benefits.

Exclusions and Limitations to Be Aware Of

While home insurance provides vital legal protection, it’s not all-encompassing. Policies typically exclude coverage for intentional acts, so if you are sued for purposefully harming someone or damaging property, your insurer won’t pay legal fees.

Long term care insurance for in home care services voorhees nj

Long term care insurance for in home care services voorhees njSimilarly, business-related incidents are generally not covered under a standard home policy—a client injured during work at your home office may fall outside the scope of protection unless you’ve added a business endorsement. Other exclusions include lawsuits arising from automobile accidents, regulated under auto insurance, and disputes related to contractual obligations.

Additionally, activities involving certain dog breeds or trampolines might be restricted or require additional liability coverage. Understanding these policy limitations helps prevent unexpected out-of-pocket legal expenses.

| Coverage Type | Typical Limit | Includes Legal Fees? | Common Exclusions |

|---|---|---|---|

| Personal Liability (Coverage E) | $100,000–$500,000+ | Yes, for covered incidents | Intentional harm, business activities, auto-related claims |

| Medical Payments to Others (Coverage F) | $1,000–$10,000 | No | Only covers medical bills, not legal defense |

| Umbrella Liability Policy | $1 million–$5 million+ | Yes, beyond primary policy limits | Requires underlying home/auto coverage, may exclude high-risk behaviors |

Understanding Home Insurance Legal Fees Coverage When Facing a Lawsuit

What does legal liability coverage in home insurance include if you're sued?

Legal liability coverage in home insurance protects you financially if someone files a lawsuit against you for bodily injury or property damage that occurred on your property or was caused by you, a family member, or even your pet.

If you're sued, this coverage typically pays for legal defense costs, settlements, or court-ordered judgments up to the policy's liability limit. It does not cover intentional acts or damage caused by certain excluded risks like automobiles or business activities. This protection applies both on and off your property in many cases, offering broad coverage for unforeseen accidents involving third parties.

What Legal Costs Are Covered Under Liability Insurance?

- Legal liability coverage pays for attorney fees when you are defending against a lawsuit, even if the claim is groundless, ensuring you can obtain proper legal representation.

- It includes court costs such as filing fees, expert witness fees, and other litigation-related expenses incurred during the legal process.

- The policy may cover the cost of appeals if the case is taken to a higher court, helping manage extended legal procedures.

What Types of Incidents Are Typically Covered?

- Slip-and-fall accidents on your property, such as a guest tripping on a wet floor or uneven walkway, are commonly covered under liability insurance.

- Dog bites or injuries caused by your pet are included, provided the breed is not excluded by the policy, offering protection against animal-related claims.

- Accidental property damage, like your child breaking a neighbor's expensive electronic device during a playdate, may be reimbursed if a claim is filed.

What Are the Limits and Exclusions of Liability Coverage?

- Policies include a per-occurrence limit, which is the maximum amount the insurer will pay for a single incident, often ranging from $100,000 to $500,000 or more.

- Intentional harm, criminal acts, or damage resulting from operating a business from home are generally not covered and require separate insurance.

- Damage caused by motor vehicles, including motorcycles or off-road vehicles, is excluded and typically falls under auto insurance policies.

Does home insurance cover legal fees if you're sued?

What Home Insurance Typically Covers Regarding Legal Fees

- Standard home insurance policies usually include liability coverage, which can extend to legal expenses if you're sued for bodily injury or property damage that occurs on your property or results from your actions.

- For example, if a visitor slips and falls on your icy sidewalk and decides to sue, your policy may pay for your legal defense, including attorney fees, court costs, and any settlement or judgment up to the policy’s liability limit.

- It's important to note that this coverage applies to incidents that are accidental and unintentional; it does not cover injuries or damages resulting from deliberate acts or illegal behavior.

Limitations and Exclusions in Legal Fee Coverage

- While home insurance can cover legal fees, there are specific exclusions—such as disputes over property boundaries, slander, or intentional harm—that generally fall outside the scope of standard liability protection.

- Coverage limits also apply; if legal costs exceed your policy’s liability limit (typically ranging from $100,000 to $500,000), you may be responsible for the remaining expenses unless you have additional insurance like an umbrella policy.

- Additionally, legal matters related to business activities, even if run from home, are usually not covered and may require separate commercial liability insurance.

How to Ensure Adequate Coverage for Legal Situations

- Review your policy’s liability section carefully to understand the extent of legal fee coverage, including what types of incidents are included and the maximum amount the insurer will pay.

- Consider increasing your liability limits or purchasing an umbrella insurance policy, which provides extra liability protection and can cover legal fees beyond what your home policy allows.

- Consult with your insurance agent to clarify any ambiguous terms, especially if you have a higher risk profile due to factors like owning a swimming pool, having frequent guests, or living in an area with high litigation rates.

Frequently Asked Questions

What legal fees does home insurance typically cover if I'm sued?

Home insurance often covers legal defense costs if you're sued for bodily injury or property damage occurring on your property. This includes attorney fees, court costs, and settlements up to your policy’s liability limit. Personal liability coverage generally applies, but intentional acts or business-related issues are excluded. Always review your policy for specifics, as coverage varies by provider and plan. Confirm limits and exclusions with your insurer.

Does homeowners insurance cover me if someone sues me for defamation?

Standard homeowners insurance may cover lawsuits involving defamation, such as slander or libel, under personal liability coverage. However, coverage depends on the policy and circumstances. Intentional or business-related claims are often excluded. Some insurers offer personal injury protection that includes defamation. Review your policy carefully or consult your provider to understand whether and to what extent legal fees for such lawsuits are covered.

Will my home insurance pay for legal fees if I'm sued by a contractor?

Home insurance typically won’t cover legal fees in disputes with contractors related to work quality, payment, or contracts. Liability coverage applies mainly to injuries or property damage claims by third parties. Disputes with professionals usually fall outside this scope. You may need a separate legal policy or rely on mediation/arbitration. Always check your policy details and consider legal advice if facing a contractor lawsuit.

How high are the legal fee coverage limits in standard home insurance policies?

Standard home insurance policies typically offer personal liability coverage limits ranging from $100,000 to $500,000, which includes legal defense fees. Higher limits are available through endorsements or umbrella policies. Legal costs are paid in addition to the settlement, up to the liability limit. If expenses exceed the limit, you're responsible for the remainder. Review your policy and consult your insurer to ensure adequate coverage.

Leave a Reply