Odessa tx home insurance

Home insurance in Odessa, Texas, is a crucial investment for homeowners seeking to protect their property and financial well-being. Due to the region's unique climate and geographic conditions, including extreme temperatures, high winds, and occasional hailstorms, having reliable coverage is essential.

Policies in Odessa typically offer protection against fire, theft, vandalism, and weather-related damage, with options to add coverage for floods or tornadoes. Insurance rates vary based on home age, location, and coverage limits. Understanding local risks and selecting the right policy ensures residents stay protected year-round.

Understanding Home Insurance in Odessa, TX: Coverage, Costs, and Key Considerations

Home insurance in Odessa, Texas, is an essential safeguard for homeowners in this West Texas city, where extreme weather, rising property values, and regional risks can impact both home safety and financial stability. Given Odessa's location in a part of the state prone to severe hailstorms, high winds, and occasional wildfires, having a comprehensive home insurance policy is crucial for protecting your property and assets.

New boston home insurance

New boston home insuranceInsurers in the area typically offer several types of coverage, including dwelling protection, personal property, liability, and loss of use, with premiums influenced by factors such as the home’s age, construction type, security features, and proximity to fire stations.

Additionally, because Texas does not require home insurance by law, many lenders still mandate coverage for mortgage holders. Reviewing quotes from multiple insurers and understanding policy exclusions—especially regarding flood and windstorm damage, which often require separate policies—is key to making an informed decision that balances affordability and protection.

Common Risks and Perils Covered in Odessa Home Insurance Policies

Homeowners in Odessa face a range of natural and man-made risks that standard home insurance policies are designed to mitigate.

The region experiences intense summer thunderstorms that bring damaging hail, strong winds, and lightning strikes—all of which are typically covered under dwelling and personal property sections of most policies. Fire damage, another significant concern, is generally included, as are incidents like vandalism and theft.

Norton home insurance

Norton home insuranceHowever, it’s important to carefully review each policy for exclusions. For example, flooding—which can occur during heavy rains in low-lying areas—is not covered under standard Texas home insurance and requires a separate flood insurance policy through the National Flood Insurance Program (NFIP) or a private insurer.

Similarly, some insurers may require a separate endorsement or policy for windstorm coverage if you live in a designated catastrophe area, although Odessa is not typically included in the coastal wind pool zones. Understanding what is and isn’t covered helps homeowners avoid gaps in protection.

Factors That Influence Home Insurance Rates in Odessa, TX

Several variables can impact the cost of home insurance in Odessa, making premiums vary significantly from one household to another. One of the most influential factors is the age and condition of the home—older homes with outdated electrical, plumbing, or roofing systems may face higher premiums due to increased risk.

The construction materials also play a role; homes built with hurricane-resistant or impact-resistant materials often receive lower rates. Insurers also consider claims history, both individual and neighborhood-wide, as areas with frequent insurance claims are seen as higher risk. Additionally, safety features such as security systems, smoke detectors, and storm shutters can lead to discounts.

Policy expert reviews home insurance

Policy expert reviews home insuranceThe amount of coverage chosen—including dwelling coverage limits, deductible amounts, and liability coverage—also affects the monthly or annual cost. Shopping around and bundling home and auto insurance with the same provider are common strategies used by Odessa residents to reduce premiums.

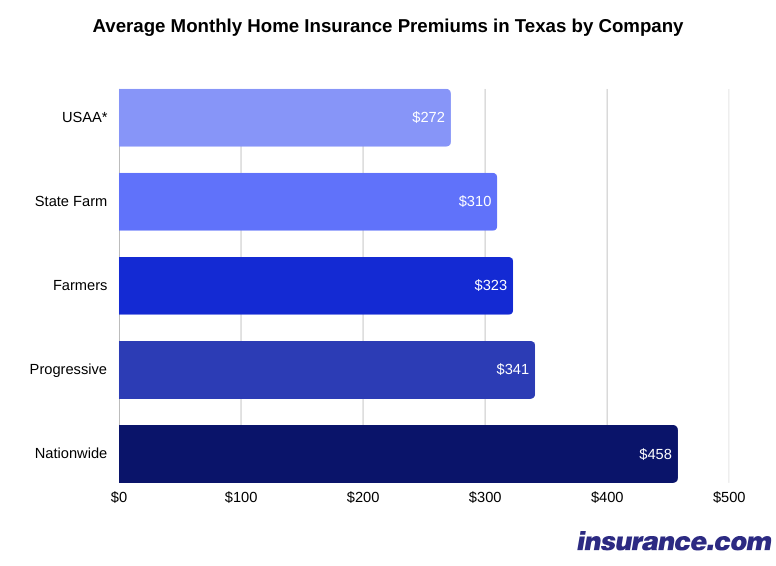

Top Home Insurance Providers Serving Odessa, Texas

Several reputable insurance companies offer home coverage to residents of Odessa, each with different strengths in pricing, customer service, and claims handling.

National carriers such as State Farm, Allstate, Farmers Insurance, and Nationwide maintain a strong presence in the area and often provide customizable policies with multiple discount options. Regional insurers, including Texas Farm Bureau Insurance and AmFam Insurance, are also popular choices among local homeowners for their localized expertise and responsive claims processes.

When comparing providers, it’s important to evaluate not just cost but also the financial stability, customer satisfaction ratings, and ease of filing claims. Many companies now offer online tools to get instant quotes, and independent agents can help compare multiple options side by side.

| Insurance Provider | Estimated Annual Premium (Odessa, TX) | Key Features | Discounts Available |

|---|---|---|---|

| State Farm | $1,450 | Extensive local agent network, fast claims processing | Multi-policy, home monitoring, claims-free |

| Allstate | $1,620 | Customizable coverage, digital tools for claims | Bundling, safety features, loyalty |

| Farmers Insurance | $1,580 | Strong Texas presence, personalized service | Home and auto bundle, new home, claim-free |

| Texas Farm Bureau | $1,500 | Local focus, solid customer satisfaction | Membership-based, multi-policy, safety devices |

| Nationwide | $1,700 | Comprehensive coverage options | Smart home, bundling, paperless billing |

Odessa TX Home Insurance: A Comprehensive Guide to Coverage and Providers

What is the most affordable home insurance in Odessa, TX?

Top Budget-Friendly Home Insurance Providers in Odessa, TX

Several insurance companies offer competitively priced home insurance policies in Odessa, TX, making it easier for homeowners to find affordable coverage.

National insurers like State Farm, Nationwide, and Allstate consistently rank among the most affordable options in the region due to their broad coverage plans and discount opportunities. State Farm, in particular, is known for offering some of the lowest average premiums in Texas, supported by a strong local agent network in Odessa.

Additionally, Texas-based companies such as USAA (available to military members and their families) and Farm Bureau Financial Services often provide cost-effective plans tailored to regional risks like windstorms and hail, common in West Texas. Shopping around and obtaining quotes from multiple carriers is essential to securing the best rate.

- State Farm offers personalized plans with multi-policy and home safety discounts that can significantly reduce annual premiums.

- Nationwide provides a Smart Home Discount for installing approved security and monitoring systems, lowering rates for tech-equipped homes.

- USAA consistently ranks as one of the most affordable and highest-rated insurers for eligible customers, combining low prices with excellent customer service.

Factors That Influence Home Insurance Costs in Odessa

The cost of home insurance in Odessa is shaped by a combination of environmental, structural, and personal factors. The city's location in a region prone to extreme weather—including hailstorms, high winds, and occasional wildfires—can increase premiums.

Insurers also evaluate the age and condition of a home, the construction materials used, and the proximity to fire stations and hydrants. Credit score and claims history play a substantial role as well; homeowners with higher credit ratings typically qualify for lower rates.

Moreover, choosing a higher deductible can reduce monthly premiums, though it means paying more out-of-pocket in the event of a claim. Understanding these variables helps homeowners better anticipate pricing and take steps to reduce their risk profile.

- Properties located near emergency services benefit from lower premiums due to reduced fire risk.

- Homes with reinforced roofs, storm shutters, or updated electrical systems may qualify for protective device discounts.

- Drivers with clean claims histories over the past 3–5 years are often rewarded with loyalty or claims-free discounts.

How to Save on Home Insurance in Odessa, TX

Homeowners in Odessa can take several proactive steps to reduce their insurance costs without sacrificing coverage. One of the most effective strategies is bundling home and auto insurance with the same provider, which commonly yields a multi-policy discount of 10% to 20%. Improving home security by installing deadbolts, monitored alarm systems, or smart home devices can trigger additional savings.

Maintaining a good credit score is another way to qualify for lower rates, as insurers view high creditworthiness as a sign of lower risk. Finally, routinely comparing quotes from at least three insurers ensures that you're not overpaying and allows you to leverage competitive offers when negotiating with providers.

- Combining insurance policies with one carrier often leads to substantial annual savings through loyalty programs.

- Investing in impact-resistant roofing materials can qualify you for a windstorm mitigation discount, especially important in West Texas.

- Updating outdated plumbing, electrical, and HVAC systems reduces risk for insurers, potentially resulting in lower premiums.

What is the average home insurance cost in Odessa, TX?

What Is the Average Home Insurance Cost in Odessa, TX?

The average annual cost of homeowners insurance in Odessa, Texas, is approximately $2,200 to $2,600 for a standard policy covering a home valued at around $250,000.

This range is slightly above the national average, which sits closer to $1,800 per year. The higher cost in Odessa can be attributed to regional risk factors such as severe weather patterns, including hailstorms and high winds, which are common in West Texas.

Insurance providers take into account the increased likelihood of property damage when calculating premiums. Additionally, fluctuations in local construction costs and the age of homes in certain neighborhoods further influence pricing. It’s important to note that individual rates can vary significantly based on coverage limits, deductibles, and the specific insurer.

- Home insurance in Odessa averages between $2,200 and $2,600 annually, exceeding the U.S. national average.

- Regional weather risks like hail and strong winds contribute to higher premiums in the area.

- Local construction costs and home age are key factors insurers use to determine individual rates.

What Factors Influence Home Insurance Rates in Odessa?

Several distinct factors impact how much homeowners in Odessa pay for insurance coverage. First, the property’s location within the city can affect risk exposure—homes in areas with higher crime rates or limited fire protection may face steeper premiums.

Second, the construction type and age of a home play a significant role; older homes with outdated electrical or plumbing systems often cost more to insure. Third, coverage options such as dwelling protection, personal property, liability, and additional covered perils like windstorm or sewer backup also influence total cost.

Insurers may offer discounts for safety features such as monitored alarm systems, storm shutters, or newer roofs, which can help reduce premiums. Finally, a homeowner’s claims history and credit score are commonly used by underwriters to assess risk.

- Neighborhood crime rates and proximity to fire stations are location-based factors affecting premiums.

- Older homes or those with outdated systems typically incur higher insurance costs.

- Available discounts for safety upgrades and strong credit history can lower overall rates.

How Does Odessa Compare to Other Texas Cities in Home Insurance Costs?

When compared to other cities in Texas, Odessa’s home insurance rates are moderate but higher than some metropolitan areas. For example, homeowners in Austin pay an average of $2,000 per year, while those in Houston face rates close to $2,400 annually.

In contrast, cities like Midland, which share similar weather and regional risks, report average premiums in the same range as Odessa. However, coastal cities such as Galveston often exceed $3,000 per year due to hurricane exposure and mandatory windstorm coverage.

The inland location of Odessa reduces exposure to hurricanes but increases vulnerability to hail and tornadoes, which are priced into policies. Regional availability of insurers and local regulatory environments also contribute to differences across Texas cities.

- Odessa's rates are higher than Austin’s but comparable to Houston and nearby Midland.

- Coastal Texas cities generally have higher premiums due to hurricane-related risks.

- Common severe weather in West Texas, like hailstorms, leads to elevated premiums relative to less volatile regions.

What is the average home insurance cost for a $500,000 house in Odessa, TX?

The average home insurance cost for a $500,000 house in Odessa, TX typically ranges from $2,500 to $4,000 annually. This estimate depends on various factors including the home’s construction type, age, claims history, chosen deductible, and the level of coverage selected. Insurance providers in West Texas also consider regional risks such as hail storms, high winds, and limited water supply when calculating premiums.

Additionally, since Odessa is located in a region with higher-than-average exposure to severe weather and some seismic activity related to oilfield operations, insurers may apply specific endorsements or higher windstorm deductibles. It is common for homeowners to carry dwelling coverage equal to the rebuild cost, not the market value, which helps determine the premium more accurately.

Factors That Influence Home Insurance Rates in Odessa, TX

- Location and Regional Risks: Homes in Odessa face higher exposure to extreme weather, including hail and wind, which directly impacts premiums. Insurers evaluate historical claims data for the area, and parts of West Texas have frequent severe storm activity, leading to higher risk classification.

- Construction and Home Age: Newer homes built with impact-resistant materials may qualify for lower premiums. In contrast, older homes might require costly updates to electrical, plumbing, or roofing systems, increasing the insurer’s perceived risk.

- Insurance Market and Provider Selection: Different carriers use varying models to assess risk. Some insurers are more experienced in underwriting policies in high-risk Texas regions, offering more competitive rates than national providers unfamiliar with local conditions.

Coverage Options for a $500,000 Home in Odessa

- Dwelling Coverage: For a home valued at $500,000, insurers typically recommend purchasing coverage based on the cost to rebuild, which may be lower than market value, especially in volatile real estate areas. Rebuild estimates in Odessa average between $125 and $150 per square foot, influencing total dwelling coverage needed.

- Additional Living Expenses and Liability Protection: Most policies include coverage for temporary housing if the home becomes uninhabitable. For a high-value property, owners often increase liability limits from the standard $100,000 to $300,000 or more to better protect assets.

- Endorsements and Riders: Given local risks, policyholders may add endorsements for sewer backup, equipment breakdown, or higher coverage for valuable items. Some may opt for a personal umbrella policy, which complements the home insurance and provides excess liability coverage.

How to Reduce Home Insurance Costs on a $500,000 House

- Improve Home Safety and Security: Installing monitored security systems, fire alarms, deadbolts, and impact-resistant windows can lead to multi-policy and safety discounts, potentially reducing premiums by 5% to 15%.

- Combine Policies and Increase Deductibles: Bundling home and auto insurance with the same provider often leads to a multi-policy discount. Additionally, selecting a higher deductible—such as $2,500 instead of $1,000—can significantly reduce the annual premium, though it increases out-of-pocket costs after a claim.

- Shop Around and Review Annually: Insurance rates vary widely among providers. Homeowners should obtain quotes from at least three insurers familiar with the Odessa market. Reassessing coverage each year ensures the policy remains competitive and reflects any home improvements or risk reductions.

Frequently Asked Questions

What factors affect home insurance rates in Odessa, TX?

Home insurance rates in Odessa, TX are influenced by several factors, including the home’s age, construction type, location, and claim history. Proximity to fire stations, local crime rates, and coverage limits also play a significant role. Additionally, high winds and hail common in the region may increase premiums due to storm-related risks. Insurers evaluate these factors to determine risk and set appropriate pricing for homeowners.

Does Odessa home insurance cover damage from hail and windstorms?

Yes, most standard home insurance policies in Odessa cover damage from hail and windstorms, which are common in the area. This includes repairs to roofs, siding, and windows damaged during severe weather. However, deductibles may apply, and some insurers offer separate wind/hail deductibles. It’s important to review your policy details to understand coverage limits and ensure adequate protection against frequent regional weather threats.

How can I lower my home insurance costs in Odessa, TX?

You can lower your home insurance costs in Odessa by installing storm-resistant roofing, upgrading windows, and adding security systems. Bundling insurance policies, maintaining a good credit score, and increasing your deductible can also reduce premiums. Regularly comparing quotes from multiple insurers helps ensure competitive pricing. Ask your provider about available discounts, such as loyalty or claims-free reductions, to maximize savings on your home coverage.

Is flood insurance included in standard Odessa home insurance policies?

No, standard home insurance policies in Odessa do not cover flood damage. Since parts of West Texas can experience flash flooding, especially during heavy rains, separate flood insurance is recommended. Coverage can be obtained through the National Flood Insurance Program (NFIP) or private insurers. It protects your home and belongings from water damage caused by overflowing rivers, drainage issues, or storms, providing essential protection beyond standard policies.

Leave a Reply