Sr22 Commercial Auto Insurance

Commercial auto insurance is a critical component for businesses operating vehicles, providing essential protection against liability and financial risks.

Among the various coverage options available, SR22 commercial auto insurance serves a specific purpose for high-risk drivers who require proof of financial responsibility. Typically mandated by state authorities following traffic violations or license suspensions, an SR22 filing ensures compliance with legal driving requirements.

When combined with commercial auto coverage, it allows business owners or employees with driving infractions to maintain lawful operations. This type of insurance not only safeguards company assets but also supports regulatory compliance, minimizing disruptions in daily business activities involving vehicle use.

Auto Quotes Online Insurance

Auto Quotes Online InsuranceUnderstanding SR-22 Commercial Auto Insurance: What Business Owners Need to Know

SR-22 Commercial Auto Insurance is a specialized form of financial responsibility coverage required for commercial drivers who have been deemed high-risk by state motor vehicle departments.

Unlike standard commercial auto insurance, an SR-22 is not an insurance policy in itself but rather a certificate filed by an insurance company to prove that a driver carries the legally mandated liability coverage. This requirement typically follows serious traffic violations such as DUIs, driving without insurance, or multiple at-fault accidents.

For business owners who rely on commercial vehicles, maintaining an SR-22 filing is crucial to keeping their commercial driving privileges active and avoiding license suspension. Because commercial operations involve higher liability exposure, insurance companies often charge higher premiums for SR-22 filings in commercial contexts, and not all insurers offer coverage for this niche need.

What Is an SR-22 Filing in Commercial Auto Insurance?

An SR-22 is a document submitted by an insurance provider to a state’s Department of Motor Vehicles (DMV) certifying that a high-risk commercial driver has the minimum required liability coverage.

Auto Repair Liability Insurance

Auto Repair Liability InsuranceIt's required for individuals operating commercial vehicles—such as delivery trucks, freight haulers, or transportation services—who have violated traffic laws or driven without insurance. Unlike personal SR-22 policies, commercial SR-22 filings are linked to vehicles used for business purposes, which often results in higher coverage limits and stricter underwriting.

The filing period usually lasts between 1 to 3 years, depending on the state and the nature of the violation. Failure to maintain continuous coverage during this period can lead to the cancellation of the SR-22, automatic license suspension, and potential disruptions to business operations.

Who Needs SR-22 Commercial Auto Insurance?

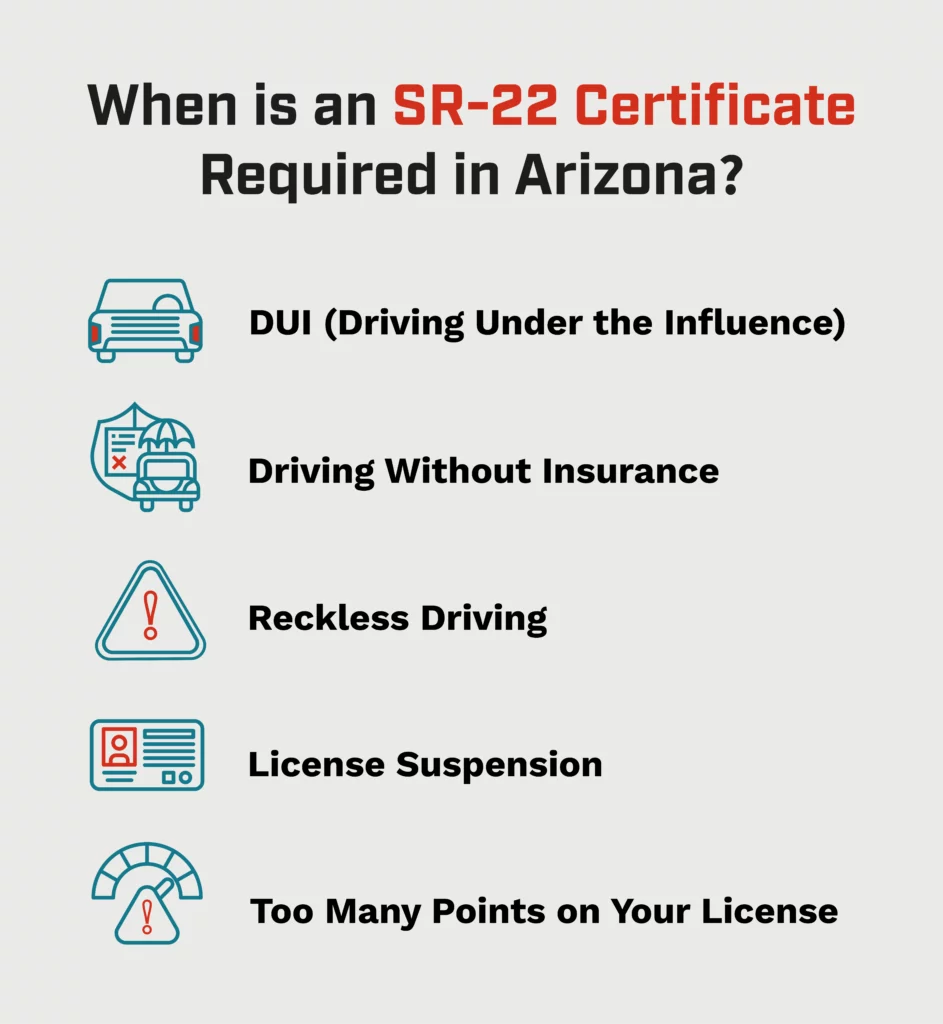

Business owners or commercial drivers who have been convicted of serious traffic offenses typically require SR-22 Commercial Auto Insurance to reinstate or maintain their driving privileges. Common situations include a DUI or DWI arrest, being caught driving without liability insurance, accumulating multiple traffic violations, or being involved in an accident without proper coverage. This requirement applies whether the driver operates a single delivery van or manages a fleet.

Commercial drivers holding a Commercial Driver’s License (CDL) are especially scrutinized, and an SR-22 filing can impact their ability to secure employment or contracts. Additionally, some states automatically require an SR-22 after a judgment involving uninsured motor vehicle accidents. It’s essential for affected drivers to contact insurers that specialize in high-risk commercial coverage, as not all providers offer SR-22 filings for commercial policies.

Auto Repair Shop Insurance Massachusetts

Auto Repair Shop Insurance MassachusettsCoverage and Cost Factors for SR-22 Commercial Auto Policies

The cost and scope of SR-22 Commercial Auto Insurance depend on several factors, including the driver’s violation history, the type of commercial vehicle, coverage limits, and the state’s regulations. While the SR-22 itself is just a filing fee—typically between $15 and $25—the associated insurance premiums are significantly higher due to the high-risk classification.

Commercial policies require broader liability coverage to account for greater potential damages due to cargo, vehicle size, and business operations. Insurers may also impose stricter terms, such as mandatory telematics or driver training programs. Additionally, continuous coverage is critical; any lapse will prompt the insurer to notify the DMV via an SR-26 form, which can restart the SR-22 requirement period. Below is a comparison of key factors influencing SR-22 commercial insurance costs.

| Factor | Impact on SR-22 Commercial Insurance |

|---|---|

| Driver’s Violation History | More severe or repeated violations lead to higher premiums and longer SR-22 filing periods. |

| Type of Commercial Vehicle | Larger vehicles (e.g., tractor-trailers) require higher liability limits, increasing overall costs. |

| State Requirements | States like Texas and Florida mandate specific minimum coverages; non-compliance risks license suspension. |

| Duration of SR-22 Filing | Typically 1–3 years; maintaining continuous coverage is essential to avoid penalties. |

| Insurance Provider | Not all insurers offer commercial SR-22 filings; specialized providers may charge more but ensure compliance. |

Comprehensive Guide to SR22 Commercial Auto Insurance: Requirements and Coverage Explained

Does Wisconsin mandate SR-22 for commercial auto insurance?

What Is an SR-22 and When Is It Required in Wisconsin?

An SR-22 is not an insurance policy but rather a certificate of financial responsibility that proves a driver carries the minimum liability coverage required by state law.

In Wisconsin, the Department of Motor Vehicles (DMV) may require an SR-22 after serious traffic violations such as driving under the influence (DUI), driving without insurance, or being involved in an at-fault accident while uninsured. This form is filed by the insurance company on behalf of the driver and is typically needed for individuals seeking to reinstate a suspended license.

The requirement applies primarily to personal auto policies and is generally tied to individual driver behavior rather than commercial operations. Wisconsin law focuses on restoring personal accountability, so SR-22 mandates are more commonly associated with personal driving infractions than commercial activities.

- SR-22 is a proof-of-insurance document filed by insurers to verify minimum liability coverage.

- In Wisconsin, it’s typically required after severe traffic offenses like DUI or driving without insurance.

- The mandate primarily targets individual drivers, not commercial fleet operations specifically.

Is SR-22 Required for Commercial Auto Insurance in Wisconsin?

Wisconsin does not specifically mandate SR-22 filings for commercial auto insurance under standard operating conditions. Commercial vehicles must carry appropriate liability insurance as required by state and federal regulations, but an SR-22 is only necessary if the owner or operator has a personal driving history that triggers the requirement.

For example, if a commercial driver has a suspended license due to a personal DUI conviction, their insurer may be required to file an SR-22, regardless of whether they drive a commercial vehicle. However, the SR-22 itself is tied to the individual, not the type of vehicle insured. Therefore, the necessity of an SR-22 in the context of commercial insurance stems from the driver’s record, not from commercial insurance regulations.

- Commercial auto insurance in Wisconsin does not automatically require an SR-22 filing.

- The need for an SR-22 arises from individual driving violations, not commercial licensing.

- If a commercial driver has a disqualifying personal offense, an SR-22 may still be filed under their policy.

How Does Wisconsin Handle Insurance Compliance for Commercial Fleets?

For commercial fleets, Wisconsin adheres to both state insurance minimums and federal Department of Transportation (DOT) requirements, especially for vehicles over a certain weight or those used in interstate commerce.

Carriers must maintain valid liability insurance, and proof of coverage is often filed using forms like the MCS-90 endorsement, not the SR-22. The MCS-90 assures compliance with minimum financial responsibility for motor carriers and is submitted to the DOT and state authorities.

Wisconsin monitors compliance through audits, roadside inspections, and required filings for commercial operators. The state's focus for commercial entities is on continuous liability coverage and adherence to FMCSA (Federal Motor Carrier Safety Administration) standards, rather than individual driver penalties reflected by SR-22 requirements.

- Commercial fleets must comply with both Wisconsin state laws and federal DOT insurance mandates.

- Proof of commercial insurance typically involves forms like the MCS-90, not SR-22.

- Compliance is enforced through FMCSA regulations, audits, and operational inspections.

What is the role of an SR-22 in commercial auto insurance in Missouri?

What Is an SR-22 in the Context of Missouri Insurance Law?

- An SR-22 is not an insurance policy itself but a certificate of financial responsibility issued by an insurance company and filed with the Missouri Department of Revenue (DOR). It serves as proof that a driver carries the minimum liability coverage required by state law.

- In Missouri, the SR-22 is typically mandated for high-risk drivers who have been involved in serious traffic violations, such as driving under the influence (DUI), driving without insurance, or accumulating multiple at-fault accidents.

- For commercial auto insurance, the SR-22 applies when a business vehicle operator has a driving history that triggers the need for financial responsibility verification. The filing ensures that the commercial driver or fleet maintains active insurance coverage as required by law.

When Is an SR-22 Required for Commercial Auto Insurance in Missouri?

- An SR-22 becomes necessary for commercial drivers in Missouri after a license suspension due to offenses like operating a vehicle without liability insurance, especially if the vehicle is used for business purposes.

- Fleet operators or owner-operators who have been convicted of serious moving violations, such as excessive speeding or reckless driving while using a commercial vehicle, may also be required to file an SR-22.

- The Missouri DOR will notify the driver when an SR-22 is required. Once notified, the commercial policyholder must contact their insurance provider to have the form issued and electronically submitted to the state.

How Does an SR-22 Affect Commercial Auto Insurance Policies?

- The inclusion of an SR-22 filing often results in higher insurance premiums for commercial policies, as it signals to insurers that the driver presents a higher-than-average risk.

- Insurance companies that offer commercial coverage may require continuous payment and active policy status for the duration of the SR-22 requirement, usually three years in Missouri. Any lapse in coverage could lead to license suspension again.

- Upon cancellation of the policy, the insurance company is obligated to notify the Missouri DOR by filing an SR-26 form, which can trigger reinstatement penalties and extended SR-22 filing periods for the commercial vehicle operator.

Does Michigan mandate an SR-22 for commercial auto insurance?

What is an SR-22 and How Does It Apply to Auto Insurance?

- An SR-22 is a certificate of financial responsibility filed by an insurance company on behalf of a driver to prove they meet their state's minimum auto insurance requirements. It is not an insurance policy itself but rather a document that shows proof of insurance coverage.

- States typically require an SR-22 after serious traffic violations such as DUIs, driving without insurance, or multiple at-fault accidents. The form is submitted directly to the state's Department of Motor Vehicles (DMV) by the insurer.

- While SR-22 requirements are common for personal auto insurance, they generally pertain to individual driving history rather than commercial operations, which are subject to different regulatory standards and coverage requirements.

Does Michigan Require SR-22 for Commercial Vehicle Operators?

- No, Michigan does not mandate an SR-22 filing specifically for commercial auto insurance. The SR-22 in Michigan is typically required for individual drivers who have had license suspensions due to offenses like driving under the influence or being caught without insurance.

- Commercial vehicle operators in Michigan are subject to separate insurance regulations, including higher liability limits and compliance with Michigan's commercial vehicle registration rules. These requirements are independent of SR-22 filings.

- If a commercial driver personally needs an SR-22 due to a traffic violation involving any vehicle (including a personal one), the SR-22 is tied to the individual, not the commercial policy, and would still be processed as a personal requirement.

What Insurance Requirements Apply to Commercial Vehicles in Michigan?

- Commercial vehicles in Michigan must carry liability insurance that meets or exceeds the state's minimum coverage limits: $250,000 for bodily injury or death per accident involving two or more people, and $10,000 for property damage.

- Depending on the type of cargo and vehicle weight, federal and state regulations may impose additional insurance requirements, such as those enforced by the Federal Motor Carrier Safety Administration (FMCSA) for interstate operations.

- Businesses operating commercial fleets must ensure proper endorsement on their policies, maintain accurate records, and may need to file a BMC-91X or other federal forms for interstate hauling, but none of these include an SR-22 filing requirement.

Can you obtain SR22 commercial auto insurance after a DUI conviction?

Yes, you can obtain SR22 commercial auto insurance after a DUI conviction, but the process comes with specific limitations and requirements.

An SR22 is not an insurance policy itself but rather a certificate of financial responsibility filed by your insurance provider with the state to prove that you carry the minimum liability coverage required by law. After a DUI conviction, many states mandate the filing of an SR22 to reinstate or maintain a driver’s license, including for those operating commercial vehicles.

While commercial drivers face stricter regulations due to the nature of their work, some insurance companies do offer SR22-compliant commercial auto insurance to high-risk drivers. However, these policies often come with higher premiums, more restrictive terms, and limited provider options.

Eligibility for SR22 Commercial Auto Insurance Post-DUI

- Eligibility largely depends on state regulations and the specifics of the DUI conviction, including whether it was a first offense or if there were aggravating factors such as injury or high blood alcohol content.

- Commercial drivers must typically meet additional federal and state licensing requirements through the Department of Transportation (DOT), which may include passing a new physical exam, undergoing substance abuse evaluation, and completing driver improvement courses.

- Insurance providers assess the applicant’s driving record, employment history, and prior insurance claims before approving coverage, and some insurers specialize in high-risk commercial policies that include SR22 filing.

How to Obtain SR22 Commercial Auto Insurance

- Start by contacting licensed insurance providers that offer high-risk or non-standard insurance policies and explicitly confirm they handle SR22 filings for commercial vehicle operators.

- Provide necessary documentation such as your commercial driver’s license (CDL), details of the DUI conviction, court orders, and past insurance history to get an accurate quote.

- Once you purchase a qualifying policy, the insurer will file Form SR22 directly with your state’s Department of Motor Vehicles (DMV) on your behalf, which is essential for reinstating driving privileges.

Cost and Coverage Considerations for Commercial SR22 Policies

- Premiums for commercial SR22 insurance are significantly higher than standard rates due to the increased risk associated with a DUI, with costs varying based on location, vehicle type, and driving history.

- Coverage typically includes only the state-mandated minimum liability limits, but additional protections like collision, comprehensive, or cargo insurance may be offered at extra cost.

- Maintaining continuous coverage is crucial—any lapse can result in the SR22 being canceled, leading to license suspension and potential delays in resuming legal commercial operations.

Frequently Asked Questions

What is SR22 Commercial Auto Insurance?

SR22 Commercial Auto Insurance is a certificate of financial responsibility required for commercial drivers who have been convicted of serious traffic violations, such as DUIs. It proves that the driver carries the state-mandated minimum liability coverage. While not an actual insurance policy, the SR22 form is filed by the insurance company with the DMV to verify coverage for high-risk commercial drivers operating business vehicles.

Who needs SR22 Commercial Auto Insurance?

Commercial drivers who have been found guilty of major traffic offenses, such as driving under the influence, reckless driving, or operating a vehicle without insurance, typically need SR22 Commercial Auto Insurance. It’s often required by state DMVs to reinstate a suspended license. This applies to those using vehicles for business purposes, ensuring they maintain proper liability coverage as mandated by law to continue legally operating commercial vehicles.

How long do you need to maintain SR22 filing?

Most states require drivers to maintain an active SR22 filing for 3 years, though this period can range from 2 to 5 years depending on the offense and state regulations. It’s crucial to keep continuous auto insurance coverage during this time. If the policy lapses, the insurance company is required to notify the DMV by filing an SR-26 form, which could result in license suspension once again.

Does SR22 Commercial Auto Insurance cover vehicle damage?

No, SR22 Commercial Auto Insurance does not cover physical damage to vehicles. The SR22 is solely a documentation of liability insurance that meets state requirements. It covers damages or injuries the driver causes to others in an accident, not repairs to their own commercial vehicle. For protection against collision or comprehensive damage, additional coverages like collision and comprehensive insurance must be purchased separately.

Leave a Reply