Auto And Home Insurance

Auto and home insurance are essential financial safeguards that protect individuals from unexpected losses. These policies provide coverage for damages, theft, liability, and natural disasters affecting vehicles and residences. While auto insurance is legally required in most states, home insurance is typically mandated by mortgage lenders.

Together, they offer peace of mind by reducing the financial burden of accidents or unforeseen events. Many insurers offer bundled policies, leading to potential cost savings. Understanding coverage options, deductibles, and policy limits is crucial for making informed decisions. Choosing the right combination ensures comprehensive protection for both property and personal well-being.

Why Bundling Auto and Home Insurance Makes Financial Sense

Bundling auto and home insurance with the same provider is a widely adopted strategy that offers policyholders both convenience and measurable savings. When consumers combine these two essential coverages, insurers often reward them with a multi-policy discount that can reduce premiums by 10% to 25%.

Home insurance comparator

Home insurance comparatorThis cost-saving benefit arises from the reduced administrative costs for the insurance company, which they pass on to the customer. Beyond monetary advantages, bundling simplifies the management of policies—billing, renewals, and customer service all come through a single point of contact, decreasing the likelihood of missed payments or coverage gaps.

Additionally, in the event of a claim affecting both property and vehicle—such as damage caused by a natural disaster—dealing with one insurer streamlines the claims process. However, while bundling typically offers value, it's crucial to compare bundled rates with standalone policies to ensure the package truly represents the best deal available in the market.

What Is Auto and Home Insurance Bundling?

Auto and home insurance bundling refers to purchasing both vehicle and property coverage from the same insurance provider under a single account or coordinated package. This practice allows the insurer to offer a consolidated policy or apply a multi-policy discount, which reduces the overall cost for the customer.

Most major insurance companies, such as State Farm, Allstate, and Farmers, promote bundling as a loyalty incentive and a way to deepen customer relationships. Beyond discounts, bundling supports easier communication—policyholders have one deductible, one renewal date for both policies in some cases, and access to a unified support team.

Ohio home owners insurance

Ohio home owners insuranceIt’s especially beneficial for homeowners who already carry auto insurance, since the linked risks (for instance, a driver’s behavior influencing property value or safety) make combined underwriting more efficient for insurers.

Key Benefits of Combined Insurance Policies

Combined auto and home insurance policies offer several compelling advantages, starting with cost savings through bundling discounts that can significantly lower annual premiums.

In addition, policyholders enjoy improved customer service efficiency, as claims, payments, and account updates are handled through a single provider. Many insurers also offer reward programs or loyalty points for maintaining multiple policies, which can translate into future discounts or cashback.

Another major advantage is the reduction in administrative complexity—rather than managing two separate billing cycles and customer portals, everything is consolidated. Moreover, some companies offer coverage continuity protections, meaning if one policy faces cancellation due to non-payment, the other may remain active under certain circumstances, providing added financial security.

Auto-Owners Auto Insurance Review

Auto-Owners Auto Insurance ReviewFactors to Consider Before Bundling Policies

While bundling auto and home insurance often makes financial sense, consumers should evaluate several factors before committing. First, not all insurers offer the same discount rates, and in some cases, the standalone cost of one policy might be higher than what’s available through a competitor.

Therefore, maintaining the bundle could unintentionally lead to overpaying. Second, coverage quality should never be sacrificed for a discount—ensure both policies provide adequate protection limits and include necessary add-ons like personal liability coverage or uninsured motorist protection.

Finally, over-reliance on a single provider may reduce flexibility; if customer service deteriorates or rates increase unexpectedly, switching both policies simultaneously can be cumbersome. A periodic market review is recommended to ensure the bundle continues to offer optimal value.

| Feature | Auto Insurance | Home Insurance | Bundled Advantage |

|---|---|---|---|

| Premium Cost | Varies by driver, vehicle, location | Depends on home value, location, age | 10–25% discount on combined policies |

| Claims Process | Vehicle damage, liability, theft | Property damage, personal liability | Single point of contact for related incidents |

| Payment & Renewal | Monthly or semi-annual | Annual or monthly | Consolidated billing for easier management |

| Coverage Flexibility | Can add roadside assistance, rental coverage | Add-ons like flood or identity theft | Some insurers offer bundle-only upgrades |

| Customer Support | Direct for vehicle claims | Direct for property claims | Unified service line reduces confusion |

Comprehensive Guide to Auto and Home Insurance: Coverage, Benefits, and Cost Factors

What is the best auto and home insurance bundle available?

Top Insurance Providers Offering Competitive Bundles

- State Farm is consistently recognized for offering one of the most reliable auto and home insurance bundles, providing average savings of around 20% when both policies are combined. Their widespread agent network and strong financial stability make them a preferred choice for many homeowners.

- Progressive stands out with its customizable bundling options and price comparison tool, Snapshot, which can further reduce premiums. They often provide competitive rates for customers with mixed driving histories and offer additional discounts for safety features in homes.

- GEICO is known for its low base rates and straightforward bundling process, with customers typically saving between 10% and 15%. Their online platform allows for easy management of both auto and home policies, and they offer additional perks like identity theft protection.

Factors That Influence Bundle Savings and Coverage Quality

- The location of your home plays a significant role in determining the cost of your bundle. Areas prone to natural disasters or with high crime rates may affect your home insurance premium more than your auto rate, thereby altering overall savings.

- Your credit-based insurance score is used by most insurers to calculate premiums. A higher score generally leads to lower rates on both auto and home policies, substantially increasing the total value of your bundle discount.

- Claims history and driving record are evaluated across both policies. A clean record on both fronts can unlock deeper discounts and better terms, while past claims or accidents may limit available savings and affect eligibility for certain programs.

How to Maximize Benefits from Your Insurance Bundle

- Review and compare multiple insurers annually, even after bundling, as rates and offers change. Shifting providers every few years can yield greater savings than staying loyal to one company without reassessment.

- Consolidate additional policies such as umbrella, identity theft, or life insurance with the same provider to unlock further multi-policy discounts and streamline management.

- Invest in home safety upgrades like security systems, storm shutters, or fire alarms, which can reduce home insurance costs and indirectly increase the value of your bundle by lowering the overall premium base.

Is bundling home and auto insurance truly more cost-effective?

How Does Bundling Home and Auto Insurance Work?

- When consumers choose to bundle home and auto insurance, they purchase both policies from the same insurance provider, often referred to as a multi-policy discount. This arrangement simplifies billing and customer service since policyholders deal with a single company for two major coverage needs.

- Insurance companies incentivize bundling by offering a discount on the total premium cost, usually ranging from 5% to 25%, depending on the provider and location. This discount is applied automatically when both policies are active under the same insurer.

- The process typically involves quoting each policy separately first and then combining them under one account. Customers may also benefit from streamlined claims handling and consolidated policy management through a single online portal or customer support line.

What Factors Influence the Actual Savings from Bundling?

- The extent of savings from bundling depends heavily on the individual's risk profile, including credit score, claims history, driving record, and the value of insured property. A person with a history of claims may receive a smaller discount or see less overall benefit despite bundling.

- Geographic location plays a significant role; insurance rates vary by state and region due to differing regulations, weather risks, and crime rates. Bundling in areas with high home insurance premiums may yield more noticeable savings compared to lower-risk areas.

- Not all insurance providers offer the same discount rates or have competitive base prices. Some companies advertise large bundle discounts but compensate with higher standalone premiums, which can diminish the net financial advantage. Shopping around and comparing bundled quotes from multiple insurers is essential to identify true cost effectiveness.

Are There Situations Where Bundling Is Not the Best Option?

- If one insurer offers a significantly cheaper auto policy but a much more expensive homeowners policy compared to competitors, bundling with them may result in higher total costs. In such cases, maintaining separate policies with different specialized providers could yield better overall pricing.

- Some niche insurers or regional carriers may provide superior coverage terms or lower rates for a single type of policy. Opting for a bundled deal might mean sacrificing quality coverage or key endorsements available only through standalone providers.

- Customers who frequently switch providers or have complex insurance needs—such as renters, frequent movers, or those with unique property risks—may find that the flexibility of separate policies outweighs the modest savings from bundling. Limited loyalty benefits and early cancellation fees can also reduce the long-term value of remaining with a bundled provider.

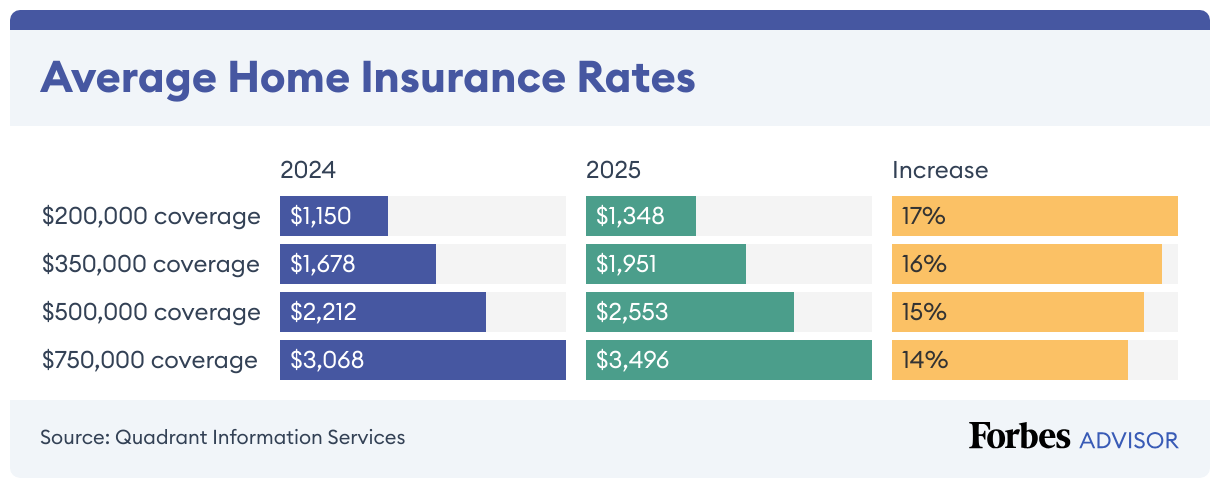

What is the average home insurance cost for a $200,000 house when bundled with auto insurance?

The average home insurance cost for a $200,000 house when bundled with auto insurance typically ranges between $1,000 and $1,400 annually, depending on location, insurer, and individual risk factors. Bundling home and auto insurance often leads to savings of 10% to 25% compared to purchasing policies separately.

For a home valued at $200,000, the coverage generally includes dwelling protection, personal property, liability, and additional living expenses. When combined with auto insurance, insurers provide multi-policy discounts that reduce the overall premium. However, exact costs vary significantly by state, credit score, claims history, and home characteristics such as construction type and proximity to emergency services.

Factors That Influence Bundled Home and Auto Insurance Rates

- Geographic location plays a major role, as regions prone to natural disasters like hurricanes, wildfires, or severe storms face higher home insurance premiums, which affects the bundled rate.

- Credit history is commonly used by insurers to determine risk; policyholders with higher credit scores typically receive lower bundled insurance rates.

- The age and condition of the home, including updated electrical, plumbing, and roofing systems, can reduce risk in the eyes of insurers and lead to lower premiums when bundled with auto coverage.

How Bundling Reduces the Cost of Home Insurance

- Insurance providers incentivize customers to purchase multiple policies through multi-policy discounts, which commonly reduce the total cost of home and auto insurance by 10% to 25%.

- Bundling simplifies billing and account management, leading to reduced administrative costs for insurers, some of which are passed on to the consumer.

- Customers with a longer history of bundling policies may qualify for loyalty discounts or additional perks, further lowering the home insurance cost for a $200,000 house.

Comparison of Bundled vs. Separate Home and Auto Insurance

- Bundled policies often offer greater overall savings, with many insurers advertising lower combined premiums than if the same policies were purchased individually from the same company.

- While bundling provides convenience and discounts, it may not always be the cheapest option; some consumers find better rates by shopping and purchasing home and auto insurance from different specialized providers.

- Separate policies offer more flexibility, allowing homeowners to switch auto insurers without affecting home coverage, or to tailor each policy with different deductibles and limits based on individual needs.

Frequently Asked Questions

What does auto insurance typically cover?

Auto insurance generally covers liability for bodily injury and property damage, collision and comprehensive damage to your vehicle, and medical payments or personal injury protection. It may also include uninsured/underinsured motorist coverage. Policies vary by provider and state, so it’s important to review your plan. Coverage helps protect you financially in accidents, theft, or natural disasters, ensuring compliance with legal requirements and peace of mind while driving.

What is home insurance and what perils does it cover?

Home insurance protects your house and belongings against risks like fire, theft, vandalism, and certain natural disasters. It typically includes dwelling coverage, personal property protection, liability for injuries on your property, and additional living expenses if displacement occurs. However, floods and earthquakes often require separate policies. Home insurance provides financial security and peace of mind, helping homeowners recover quickly after unexpected damage or loss.

Can I bundle auto and home insurance together?

Yes, most insurers offer bundled policies that combine auto and home insurance, often resulting in significant discounts. Bundling simplifies billing and claims management while increasing overall coverage coordination. It also strengthens customer loyalty with providers. Many homeowners benefit from lower premiums and better service. Be sure to compare bundled rates with standalone policies to confirm cost-effectiveness and ensure all your coverage needs are adequately met under the combined plan.

How do claims work for auto and home insurance?

For both auto and home insurance, filing a claim starts with reporting the incident to your insurer, providing details and documentation like photos or police reports. An adjuster assesses the damage and determines coverage and payout. Repairs are made after approval, and you pay your deductible. Claims can affect premiums, so insurers evaluate frequency and fault. Prompt, accurate reporting ensures faster processing and fair resolution.

Leave a Reply