Ohio home owners insurance

Homeowners insurance in Ohio provides essential protection for property owners against financial losses resulting from damage, theft, or liability incidents.

With a mix of urban, suburban, and rural landscapes, Ohio residents face varying risks—from severe weather events like thunderstorms and tornadoes to property crime in densely populated areas. A standard policy typically covers dwelling damage, personal property, liability, and additional living expenses if a home becomes uninhabitable.

Ohio law does not mandate homeowners insurance, but mortgage lenders usually require it. Understanding coverage options, local risk factors, and how premiums are determined helps Ohioans make informed decisions to protect their homes and assets effectively.

Home insurance claim proof of ownership requirement

Home insurance claim proof of ownership requirementUnderstanding Ohio Homeowners Insurance: Coverage, Costs, and Legal Considerations

Ohio homeowners insurance is a crucial financial safeguard for property owners across the state, providing protection against unexpected damages to homes and personal belongings, as well as liability for accidents occurring on the property.

Given Ohio’s diverse climate—ranging from severe winter storms to tornado threats in certain regions—homeowners face unique risks that make comprehensive coverage essential. Standard policies typically include dwelling protection, personal property coverage, liability insurance, and additional living expenses if a home becomes uninhabitable due to a covered event.

While Ohio law does not mandate homeowners insurance, most mortgage lenders require proof of coverage before approving a loan, ensuring that the property securing the mortgage is protected. Understanding policy options, average costs, and state-specific risks enables Ohio residents to make informed decisions and select plans that best meet their individual needs.

What Does Standard Homeowners Insurance Cover in Ohio?

In Ohio, standard homeowners insurance policies typically follow the structure of an HO-3 policy, which offers broad protection for both the structure of the home and personal belongings. This includes coverage for damage caused by perils such as fire, lightning, windstorms, hail, vandalism, and certain types of water damage—though flooding and earthquake damage are usually excluded unless added via separate endorsements.

Home insurance claims attorney

Home insurance claims attorneyThe dwelling coverage pays for repairs or rebuilding of the home’s structure, while personal property coverage reimburses the cost of replacing stolen or damaged belongings like furniture, electronics, and clothing. Liability protection is another key component, shielding homeowners from legal expenses and medical bills if someone is injured on their property.

Additional living expenses (ALE) are also covered if the home is temporarily unlivable, helping pay for hotel stays, meals, and other costs during repairs. It's important for Ohio residents to review policy details carefully and consider adding endorsements for specific risks like sump pump failure or sewer backup, which are common in areas with aging infrastructure.

Factors That Influence Homeowners Insurance Rates in Ohio

Several factors affect homeowners insurance premiums across Ohio, making rates vary significantly by location and property characteristics. One major factor is geographical region—areas in northwest Ohio, for example, may face higher wind and tornado risks, leading to increased premiums.

The age and condition of the home also play a significant role; older homes with outdated electrical systems or plumbing may cost more to insure due to higher risk of claims. Homes equipped with modern safety features such as fire alarms, security systems, and storm shelters often qualify for discounts. Proximity to fire departments and access to reliable water sources can similarly reduce rates.

Does home insurance cover accidental damage

Does home insurance cover accidental damageCredit history is legally used in Ohio for pricing insurance, meaning that individuals with better credit often receive lower premiums. The amount of coverage selected, the deductible level, and previous insurance claims also directly impact the final cost. Shopping around and comparing quotes from multiple insurers is advised to find the most competitive rate.

Ohio homeowners must contend with a range of weather-related risks that influence the need for robust insurance protection.

The state experiences a humid continental climate, leading to heavy snowfall in winter, particularly in the “Snowbelt” region near Lake Erie, which can result in roof collapses and ice dam damage. Spring and summer months bring frequent thunderstorms and the potential for tornadoes, especially in western and central Ohio, which can cause severe structural damage and loss of property.

Additionally, Ohio is susceptible to flash flooding due to intense rainfall and aging drainage systems, particularly in urban areas like Columbus and Cincinnati. While standard policies cover wind and hail damage, many homeowners are unaware that flood damage is not included and requires a separate policy through the National Flood Insurance Program (NFIP) or a private insurer.

Severe storms may also lead to power outages and sump pump failures, so additional endorsements for water backup can provide valuable protection. Being proactive about risk assessment and policy customization ensures better financial security when disaster strikes.

| Insurance Factor | Impact on Ohio Homeowners | Potential Cost-Saving Tips |

|---|---|---|

| Location in Ohio | Urban areas like Cleveland may have higher theft rates; rural areas face wildfire or storm exposure. Northwest Ohio sees more tornadoes. | Compare local rates by ZIP code and consider regional risk mitigation improvements. |

| Home Age and Construction | Homes built before 1980 may have outdated systems, increasing risk and premiums. | Update plumbing, electrical, and roofing to qualify for lower rates and safety discounts. |

| Credit-Based Insurance Score | Ohio insurers legally use credit history to determine pricing—better scores often mean lower premiums. | Maintain good credit and ask insurers about credit score usage policies. |

| Optional Coverage Add-Ons | Flood, sewer backup, and earthquake coverage are not standard but recommended in high-risk zones. | Add endorsements for sump pump failure or NFIP flood insurance if near rivers or low-lying areas. |

| Claims History | Multiple claims in five years can lead to higher premiums or non-renewal by insurers. | Avoid small claims; consider raising deductibles to reduce frequency-based penalties. |

Comprehensive Guide to Ohio Homeowners Insurance: Coverage, Costs, and Provider Options

What is the typical homeowners insurance cost in Ohio?

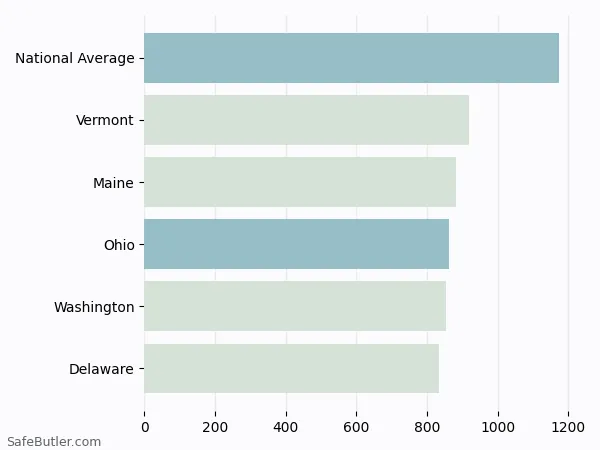

The typical cost of homeowners insurance in Ohio is approximately $1,200 to $1,500 per year, although this can vary significantly depending on numerous factors such as location, home value, coverage limits, and the insurance provider. Ohio’s relatively low cost of living contributes to more affordable insurance rates compared to the national average, which sits around $1,800 annually.

Rural areas and towns with lower crime rates and robust emergency services often have lower premiums, while urban centers like Cleveland or Cincinnati may see slightly higher costs due to population density and increased risk of property claims. Additionally, the age and condition of a home, its construction materials, and the presence of safety features such as security systems or storm shelters impact pricing.

Factors That Influence Homeowners Insurance Rates in Ohio

- Location within the state plays a critical role; homes in regions prone to severe weather, such as tornadoes or heavy snowfall in northern Ohio, may incur higher premiums due to increased risk of damage.

- The age and construction of the home affect pricing, with older homes often requiring more extensive coverage due to outdated electrical or plumbing systems, potentially raising the cost.

- Local crime rates and proximity to fire stations also influence premiums, as insurers consider fire and theft risk when determining policy costs.

- Standard policies typically include dwelling coverage, personal property protection, liability insurance, and additional living expenses, with higher coverage limits resulting in increased premiums.

- Optional add-ons like water backup coverage, sump pump failure protection, or earthquake insurance can be valuable in certain areas of Ohio but will raise the overall cost of the policy.

- Choosing a higher deductible can lower the annual premium but means the homeowner will pay more out of pocket if a claim is filed, making this a key financial consideration.

Ways to Save on Homeowners Insurance in Ohio

- Shopping around and comparing quotes from multiple insurers can lead to significant savings, as pricing models and discounts vary between companies.

- Many insurers offer discounts for bundling home and auto insurance, having a security system, being claims-free, or paying the full annual premium upfront.

- Making home improvements such as upgrading the roof, installing storm shutters, or reinforcing foundations can reduce risk and lead to lower premiums over time.

What is the top-rated home insurance provider in Ohio?

The top-rated home insurance provider in Ohio is generally considered to be Erie Insurance based on customer satisfaction, affordability, and overall coverage options.

According to data from sources like J.D. Power and the National Association of Insurance Commissioners (NAIC), Erie consistently ranks high in customer satisfaction across the Midwest, including Ohio. The company is known for offering personalized policies, competitive rates, and strong local agent support.

Additionally, Erie tends to have fewer customer complaints compared to industry averages, which contributes to its high ratings. While other major insurers like State Farm, Allstate, and Nationwide also operate widely in Ohio and maintain solid reputations, Erie Insurance stands out for its regional focus and superior service in the state.

Factors That Contribute to Erie Insurance’s High Ratings in Ohio

- Erie Insurance benefits from a strong regional presence, allowing it to tailor policies specifically to Ohio’s climate, housing markets, and risk factors such as severe weather and property crime rates.

- The company consistently scores above average in J.D. Power’s U.S. Home Insurance Study, particularly in claims satisfaction and customer service, indicating reliable support when policyholders need it most.

- Erie offers a range of customizable coverage options, including identity theft protection and equipment breakdown coverage, which enhances the overall value for homeowners.

Comparison with Other Major Home Insurance Providers in Ohio

- State Farm is one of the largest insurers in Ohio and offers broad availability and competitive pricing, but customer satisfaction ratings often fall slightly below Erie’s, especially in claim handling.

- Allstate provides extensive coverage add-ons and digital tools for policy management, but tends to be more expensive on average and receives more complaints related to rate increases and claim disputes.

- Nationwide is known for strong financial stability and a variety of policy options, yet it does not consistently match Erie’s regional customer service ratings or pricing advantages in Ohio.

How Ohio Homeowners Can Choose the Best Insurance Provider

- Start by comparing quotes from multiple providers, including Erie Insurance, State Farm, and local mutual companies, to evaluate both cost and coverage depth for your specific location and home value.

- Review each company’s track record for customer service and claims handling, using resources like the Ohio Department of Insurance and third-party rating agencies such as AM Best and J.D. Power.

- Consider bundling home and auto insurance, as many providers, including Erie and State Farm, offer multi-policy discounts that can significantly reduce annual premiums.

Is homeowners insurance mandatory in Ohio?

Homeowners insurance is not legally required by the state of Ohio. However, while Ohio law does not mandate that homeowners carry insurance, most mortgage lenders do require borrowers to maintain a homeowner's insurance policy as a condition of the loan.

This protects the lender's financial interest in the property in case of damage from fire, storms, theft, or other covered perils. Even for homeowners who own their property outright, having insurance is strongly recommended to cover repair or rebuilding costs, protect personal belongings, and provide liability coverage if someone is injured on the property.

Why Mortgage Lenders Require Homeowners Insurance in Ohio

- Mortgage lenders require homeowners insurance because the home serves as collateral for the loan. If the property is damaged or destroyed and the homeowner cannot afford to repair it, the value of the collateral decreases, increasing the lender’s risk.

- Lenders typically mandate a minimum level of coverage that corresponds to the loan amount and the replacement cost of the home. This ensures that sufficient funds are available to rebuild or repair the structure after a covered loss.

- Failure to maintain homeowners insurance can result in the lender purchasing a force-placed insurance policy on behalf of the borrower, which is often more expensive and provides less comprehensive coverage than a standard policy.

Benefits of Having Homeowners Insurance Without a Mortgage

- Even if you own your home outright, homeowners insurance offers valuable protection for your personal assets. It covers the cost of repairing or rebuilding your home after a covered event, such as a fire or windstorm, which could otherwise result in significant out-of-pocket expenses.

- Homeowners insurance includes personal property coverage, which helps replace or repair belongings like furniture, electronics, and clothing that are lost or damaged due to covered perils.

- Liability protection is another key benefit. If a guest is injured on your property and decides to sue, the policy can cover medical expenses, legal fees, and court-awarded damages, helping to safeguard your savings and financial stability.

Coverage Options and Endorsements Available in Ohio

- Standard homeowners insurance policies in Ohio typically include dwelling coverage, other structures coverage, personal property protection, liability coverage, and additional living expenses if your home becomes uninhabitable after a covered loss.

- Residents in certain areas may consider adding endorsements for specific risks, such as sewer backup, water damage from sump pump overflow, or coverage for valuable items like jewelry or artwork that exceed standard policy limits.

- Given Ohio’s susceptibility to severe weather, including thunderstorms and tornadoes, policyholders may also explore enhanced windstorm coverage or higher deductibles for storm-related claims to manage premiums while maintaining adequate protection.

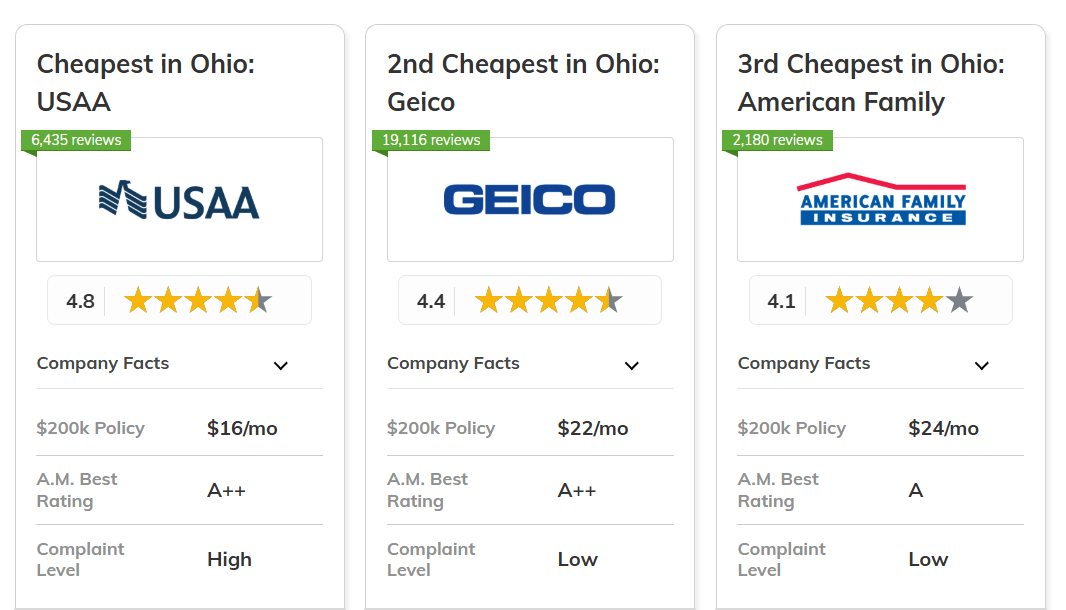

What are the cheapest homeowner insurance rates in Ohio?

Factors That Influence Homeowners Insurance Rates in Ohio

- Location within Ohio significantly affects premiums, as homes in areas prone to severe weather, such as tornadoes or heavy snowfall, typically face higher rates. Urban areas like Cleveland or Cincinnati may have elevated risks of theft or fire, leading insurers to charge more compared to rural regions with lower crime and fewer weather-related claims.

- The age and condition of a home also play a crucial role in determining insurance costs. Older homes with outdated electrical systems or plumbing may require higher premiums due to increased risk of fire or water damage. In contrast, newer constructions or properties with updated safety features like smoke detectors and security systems often qualify for lower rates.

- Insurance companies evaluate a homeowner’s claims history and credit score when calculating premiums. A history of frequent claims can signal higher risk, resulting in increased costs. Similarly, policyholders with strong credit profiles are typically viewed as more reliable, which can lead to better pricing options.

Top Insurance Providers with Low Rates in Ohio

- State Farm is frequently recognized for offering some of the most competitive homeowners insurance rates in Ohio. The company benefits from a large customer base and extensive agent network, allowing it to provide affordable premiums, especially for homeowners with clean claims records and strong credit.

- Allstate offers customizable policies and frequent discounts, such as bundling home and auto insurance or installing home security systems, which help reduce overall costs. While rates vary by location, Allstate remains a strong contender for low-cost coverage in many Ohio counties.

- USAA (available to military members and their families) consistently ranks among the cheapest and highest-rated insurers in the state. Its combination of low premiums, excellent customer service, and loyalty benefits makes it a top choice for eligible Ohio residents seeking affordable yet reliable coverage.

How to Find and Secure the Cheapest Homeowners Insurance in Ohio

- Compare quotes from multiple insurers to identify the most affordable options tailored to your specific home and needs. Online comparison tools allow you to review rates from companies like Nationwide, Erie Insurance, and Farmers, helping you spot discrepancies and uncover lower-priced policies.

- Take advantage of available discounts offered by insurers, such as those for having a claims-free history, retiring homeowners, or homes equipped with storm shelters or fire-resistant materials. These can substantially reduce annual premiums when combined.

- Consider adjusting your deductible or coverage limits based on your risk tolerance and property value. While lowering coverage is not recommended for essential protections, raising your deductible can significantly cut your premium, especially if you have savings to cover out-of-pocket costs in case of a claim.

Frequently Asked Questions

What does Ohio homeowners insurance typically cover?

Ohio homeowners insurance generally covers dwelling damage, personal property, liability protection, and additional living expenses. It protects against perils like fire, windstorms, and theft. Coverage extends to structures attached to the home, such as garages. Personal liability helps pay for injuries or property damage you cause others. However, floods and earthquakes usually require separate policies. Always review your policy to understand specific inclusions, limits, and exclusions based on your provider and home location in Ohio.

How much homeowners insurance do I need in Ohio?

The amount of homeowners insurance you need in Ohio depends on your home’s replacement cost, personal belongings’ value, and desired liability coverage. Most experts recommend enough dwelling coverage to rebuild your home, typically based on square footage and construction costs. Consider at least $300,000 in liability coverage, though $500,000 or more is safer. Evaluate your personal property and additional living expenses to ensure adequate protection tailored to your needs.

Why are home insurance rates different across Ohio?

Home insurance rates in Ohio vary due to location, home age, construction type, crime rates, and proximity to fire services. Areas more prone to severe weather or with higher crime may have increased premiums. Older homes may cost more to insure due to outdated systems. Insurance companies also consider your credit history and claims history. Shopping around and comparing quotes can help find the best rate based on your specific circumstances and chosen coverage levels.

Does Ohio homeowners insurance cover water damage?

Ohio homeowners insurance typically covers sudden and accidental water damage, such as burst pipes or appliance leaks. However, it does not cover damage from long-term issues like gradual leaks or poor maintenance. Flooding from external sources, such as heavy rain or overflowing rivers, requires a separate flood insurance policy. Always check your policy details and consider additional coverage options if you live in an area susceptible to water-related risks to ensure comprehensive protection.

Leave a Reply