Auto Insurance Coverage Terms

Understanding auto insurance coverage terms is essential for every driver navigating the complexities of vehicle protection.

Policies consist of various components, each serving a distinct purpose in safeguarding against financial loss. From liability coverage, which addresses damages to others, to comprehensive and collision coverage that protects your own vehicle, knowing what each term means ensures informed decision-making.

Additional options like personal injury protection and uninsured motorist coverage further expand protection. Familiarity with deductibles, premiums, and coverage limits helps drivers choose appropriate plans. Misinterpreting these terms can lead to inadequate coverage or unexpected expenses after an accident.

Auto Insurance Quotes Lakeland Fl

Auto Insurance Quotes Lakeland FlUnderstanding Auto Insurance Coverage Terms

Auto insurance is a critical safeguard for drivers, providing financial protection against physical damage, bodily injury, and liability resulting from traffic incidents. However, making informed decisions about coverage requires a clear understanding of key terms and components included in most auto insurance policies.

From liability limits to deductibles and policy exclusions, these terms define the scope of protection and determine what you are responsible for paying in the event of a claim. Familiarizing yourself with these elements ensures you select appropriate coverage levels, avoid unexpected out-of-pocket expenses, and maximize the benefits of your policy when you need it most.

Types of Auto Insurance Coverage

There are several essential types of coverage included in most standard auto insurance policies, each designed to protect against different risks. Liability coverage is the most fundamental and typically required by law; it pays for damages or injuries you cause to others in an accident, split into two components: bodily injury liability and property damage liability.

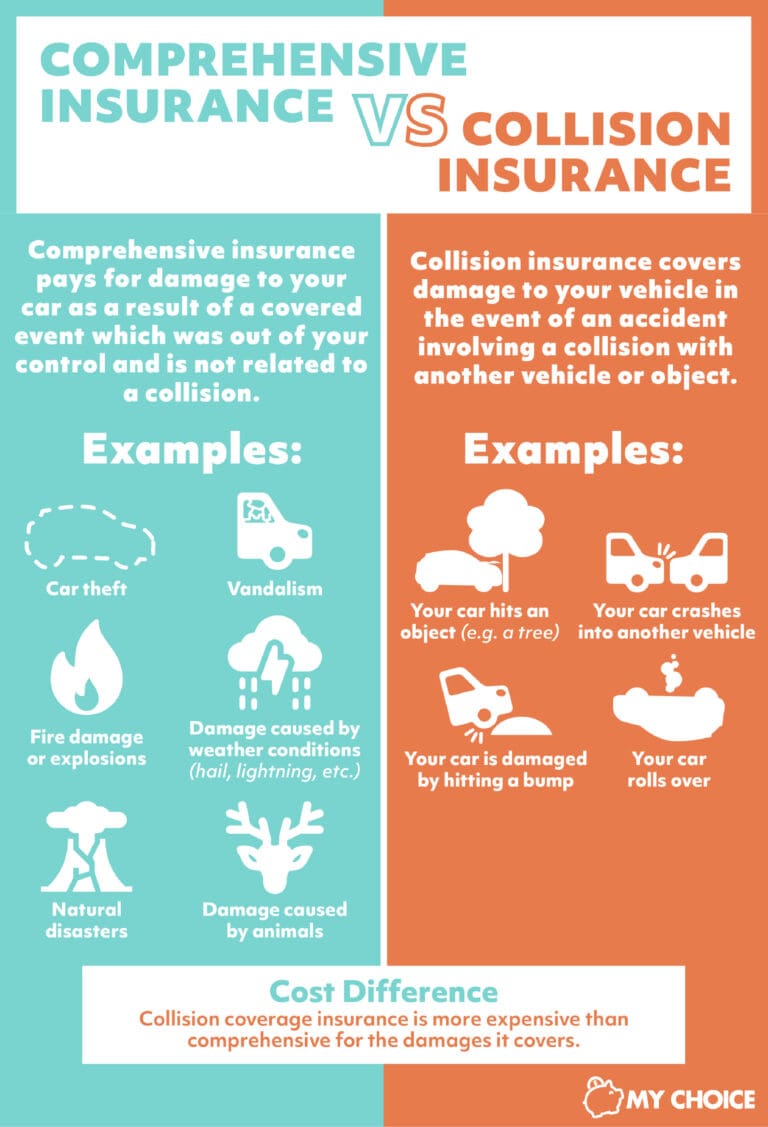

Collision coverage helps pay for repairs to your vehicle after a crash, regardless of fault, while comprehensive coverage covers non-collision-related damage such as theft, vandalism, or natural disasters. Additional options like personal injury protection (PIP) or medical payments coverage (MedPay) assist with medical bills for you and your passengers, and uninsured/underinsured motorist coverage protects you if the at-fault driver has inadequate or no insurance.

Home And Auto Insurance In Anaheim

Home And Auto Insurance In Anaheim| Coverage Type | What It Covers | Is It Required? |

|---|---|---|

| Liability (Bodily Injury & Property Damage) | Damage or injuries you cause to others | Yes, in most states |

| Collision | Repairs to your car after an accident | No (but often required by lenders) |

| Comprehensive | Theft, fire, vandalism, weather damage | No |

| Uninsured/Underinsured Motorist | Costs if hit by a driver with no or insufficient insurance | Required in some states |

| Personal Injury Protection (PIP) | Medical expenses, lost wages for you and passengers | Required in no-fault states |

Understanding terms like deductibles, coverage limits, and premiums is essential to grasping how your policy functions.

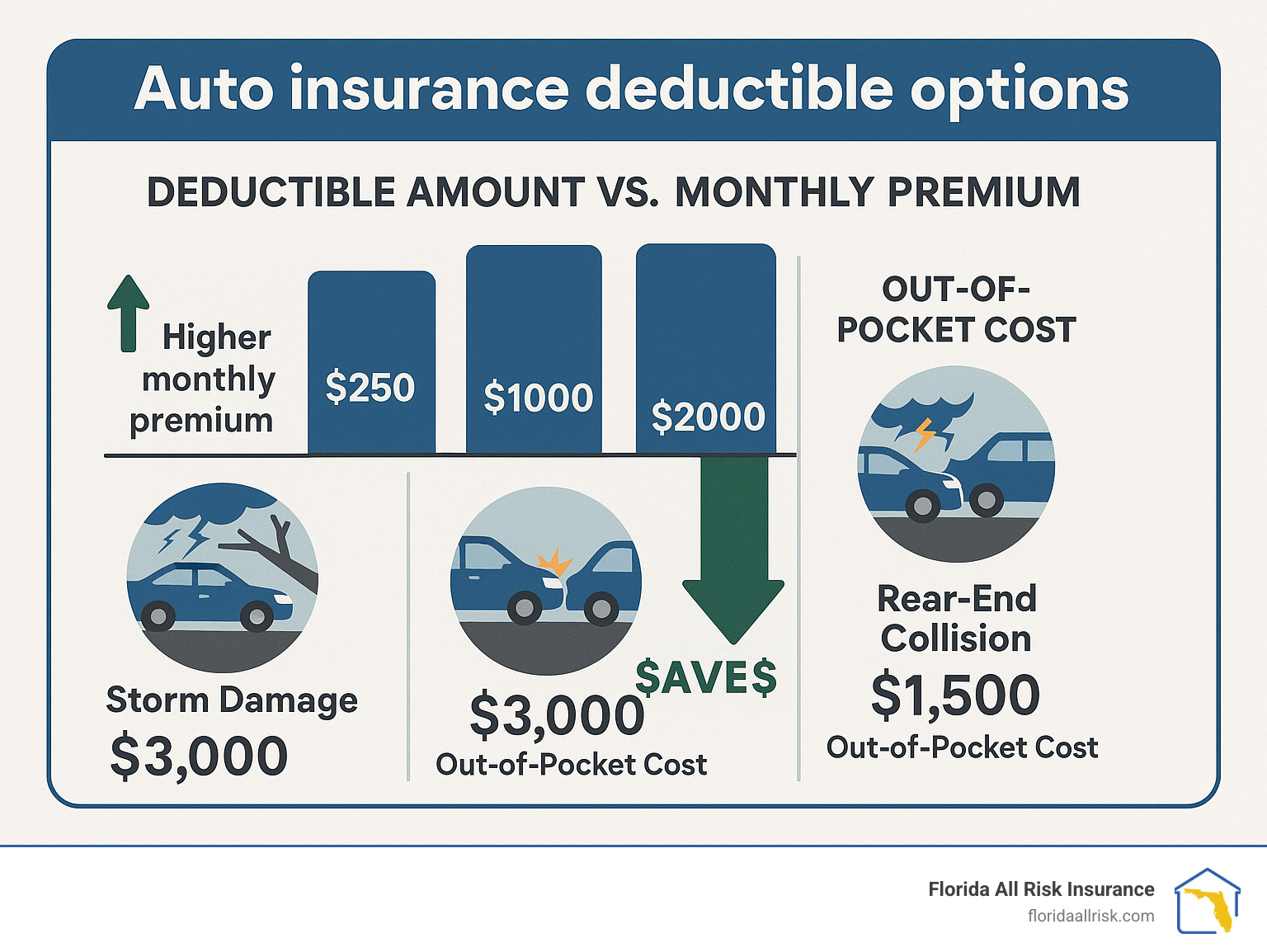

A deductible is the amount you must pay out of pocket before your insurance kicks in—higher deductibles usually result in lower premiums but higher out-of-pocket costs when filing a claim. Coverage limits define the maximum amount your insurer will pay for a covered loss, often expressed in split formats (e.g., 100/300/100 for bodily injury and property damage liability).

Premiums are the regular payments—monthly or biannually—you make to keep your policy active. Choosing higher limits increases protection but also raises premiums, so finding a balance depends on your financial situation and risk tolerance.

Policy Exclusions and Endorsements

Every auto insurance policy includes exclusions, which are specific situations or conditions not covered under the standard policy. Common exclusions include intentional damage, using your vehicle for illegal activities, or driving without a valid license.

How To Submit Medical Bills To Auto Insurance

How To Submit Medical Bills To Auto InsuranceAdditionally, damage from normal wear and tear or mechanical breakdowns are typically not covered. To expand protection, policyholders can add endorsements (also known as riders), which modify the original policy to include additional coverage.

Examples include rental reimbursement, roadside assistance, or gap insurance, which covers the difference between your car’s value and what you owe if it's totaled. Reviewing exclusions and evaluating optional endorsements helps ensure your coverage aligns with your needs.

Comprehensive Guide to Auto Insurance Coverage Terms

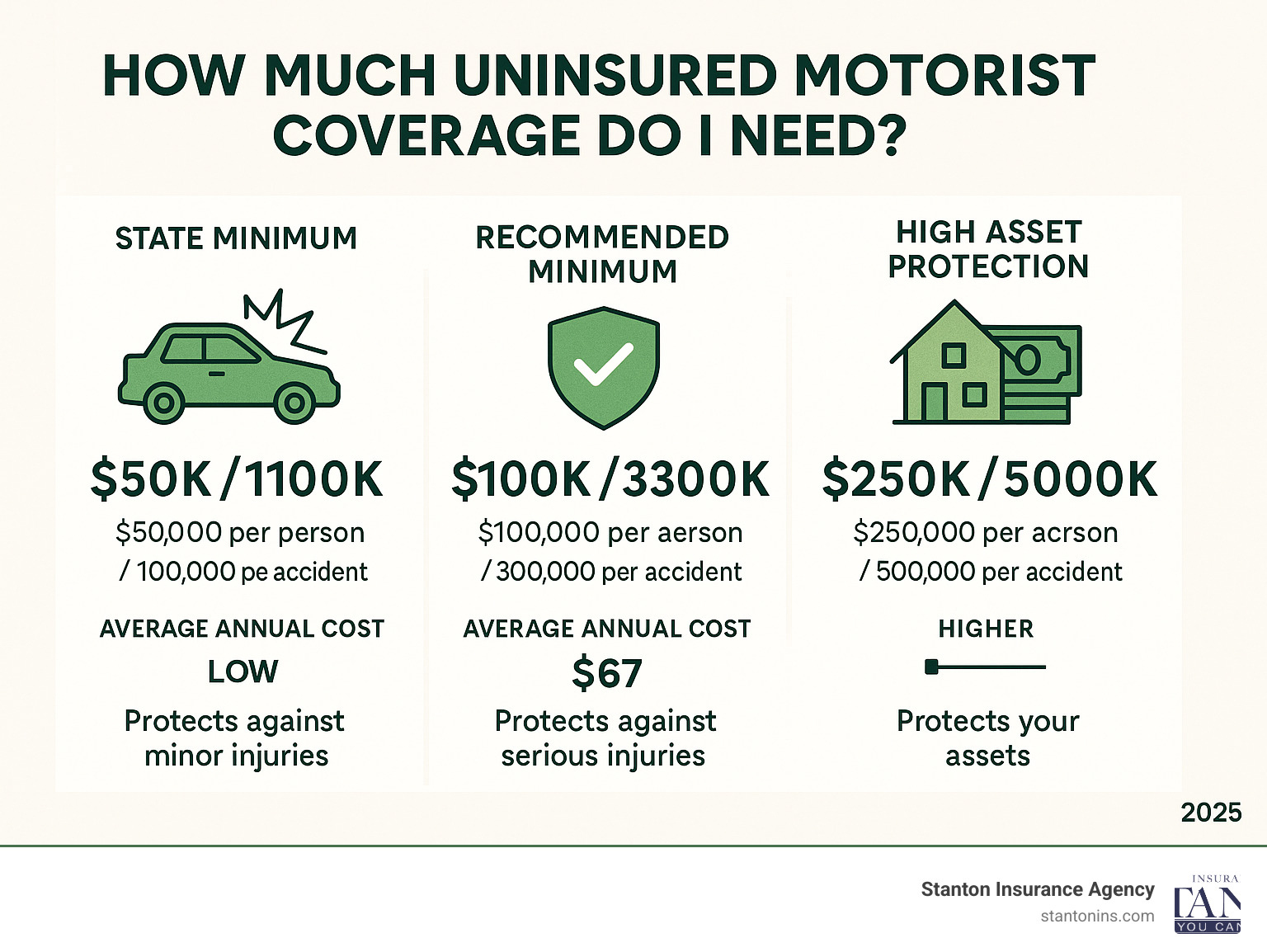

What does $100k/$300k/$100k mean in auto insurance coverage?

The notation $100k/$300k/$100k in auto insurance refers to the liability coverage limits offered by an insurance policy. These three values represent the maximum amounts an insurer will pay for specific types of damages in the event of an at-fault accident.

Illinois Commercial Auto Insurance

Illinois Commercial Auto InsuranceThe first number refers to bodily injury liability per person, the second relates to bodily injury liability per accident, and the third corresponds to property damage liability per accident. This structure ensures that coverage is distributed according to specific legal and financial responsibilities after a crash, protecting both the insured and third parties involved.

What Does Each Number Represent in $100k/$300k/$100k?

- The $100k stands for the maximum amount the insurance company will pay per person for bodily injury claims if you're at fault in an accident. For example, if three people in the other vehicle suffer injuries, the insurer will cover up to $100,000 for each individual’s medical expenses, lost wages, and pain and suffering.

- The $300k is the total maximum payout for all bodily injury claims combined in a single accident. Even if multiple people are injured, the insurer will not pay more than $300,000 in total, regardless of the number of victims. This means that if four people each had $100k in damages, the total would exceed the limit, and the insurer would cover only up to $300k collectively.

- The final $100k refers to property damage liability, which covers damage your vehicle causes to someone else’s property—most commonly their car, but also structures like fences or buildings. This limit applies per accident, so if the damage exceeds $100,000, you would be personally responsible for the remaining costs.

How Does $100k/$300k/$100k Protection Benefit You Financially?

- This coverage level protects your personal assets by limiting your out-of-pocket financial exposure after being found at fault. Without sufficient insurance, you could be sued for amounts exceeding your policy limits, potentially leading to wage garnishment or loss of savings.

- It meets or exceeds the minimum liability requirements in many states, offering broader protection than basic policies. Higher limits like these are often recommended by insurance professionals, especially in areas with high traffic density or expensive medical and repair costs.

- In the event of a serious accident involving multiple injured parties or costly vehicle repairs, this tier of coverage reduces the likelihood of exhausting your policy. For instance, a single hospital stay can exceed $50,000, and vehicle repairs or replacements can quickly add up, making $100k/$300k/$100k a prudent level of protection.

When Might $100k/$300k/$100k Not Be Enough Coverage?

- If an accident results in catastrophic injuries or multiple fatalities, medical and legal expenses could surpass the $300,000 cap on bodily injury coverage. In such cases, victims may sue for additional compensation, putting your personal assets at risk.

- High-value property damage, such as crashing into a luxury vehicle, commercial equipment, or a residential structure, may exceed the $100,000 property damage limit. Repair or replacement costs for certain vehicles alone can surpass this amount, leaving you liable for the difference.

- Certain states or jurisdictions have higher average claim amounts due to elevated medical costs or legal precedents favoring higher damages. In these areas, drivers may want to consider even higher limits, such as $250k/$500k/$250k or adding an umbrella policy for additional protection.

Do I need comprehensive and collision coverage for my auto insurance?

When Is Comprehensive and Collision Coverage Necessary?

- Comprehensive and collision coverage is typically required if you have an auto loan or lease. Lenders and leasing companies want to protect their financial interest in the vehicle, so they mandate both coverages until the car is fully paid off.

- If you drive a newer or more expensive vehicle, maintaining both coverages is often recommended. Repair or replacement costs for such vehicles can be high, and out-of-pocket expenses after an accident or loss could be significant without adequate insurance.

- Drivers in areas with high rates of theft, vandalism, or severe weather may benefit from comprehensive coverage specifically. It helps cover damages from events like hailstorms, fire, animal collisions, or break-ins, which are not related to driving incidents.

When Might You Consider Dropping Comprehensive and Collision Coverage?

- You may consider dropping these coverages if your vehicle has significantly depreciated in value and the annual premium costs exceed a certain percentage—often recommended as 10%—of the car's current market value.

- Drivers who have saved enough to pay for repairs or replacement out of pocket may choose to forgo these coverages. This can be a cost-saving strategy, especially for older vehicles with low resale value.

- If you live in a low-risk area with minimal traffic, crime, and natural hazards, the likelihood of filing a claim could be low. In such cases, maintaining expensive coverage might not be cost-effective over time.

How to Decide Based on Your Personal Situation?

- Assess your financial situation by evaluating how much you could afford to lose if your car were totaled or severely damaged. If replacing the vehicle would cause financial strain, keeping both coverages is generally wise.

- Compare the total annual cost of comprehensive and collision coverage against the actual cash value of your car. Use online valuation tools to determine current market value and weigh that against premiums.

- Consider your driving habits and environment. Frequent driving, high annual mileage, or parking in urban areas with higher risks of accidents or theft increases the need for both types of coverage.

Which deductible is more cost-effective for auto insurance: $500 or $1000?

The cost-effectiveness of a $500 versus a $1000 deductible for auto insurance depends on several financial and behavioral factors, including your driving history, risk tolerance, and ability to absorb out-of-pocket costs after an accident. Generally, a higher deductible like $1000 results in lower monthly premiums because you're assuming more financial responsibility in the event of a claim.

Insurance And Auto Law Attorney Raleigh Nc

Insurance And Auto Law Attorney Raleigh NcHowever, this also means you'll pay more upfront when filing a claim. Conversely, a $500 deductible leads to higher premiums but less out-of-pocket expense when repairs are needed. The more cost-effective option ultimately hinges on how frequently you anticipate making claims and your current financial stability.

- Choosing a $1000 deductible typically reduces your annual auto insurance premium by 10% to 20% compared to a $500 deductible, depending on the insurer and your location.

- This savings accumulates over time, especially if you go several years without filing a claim, making the higher deductible financially beneficial in the long run for cautious drivers.

- However, it's essential to calculate whether the annual savings outweigh the risk of paying an extra $500 out of pocket if you need to file a claim, particularly if emergency funds are limited.

Assessing Claim Frequency and Driving Behavior

- Drivers with a clean record and low risk of accidents may find a $1000 deductible more cost-effective since they are less likely to file frequent claims.

- On the other hand, those who commute in high-traffic areas or have a history of minor collisions might benefit more from a $500 deductible to minimize out-of-pocket costs when incidents occur.

- Consistent, safe driving habits increase the likelihood that the premium savings from a higher deductible will outweigh occasional repair expenses paid in full.

Financial Readiness and Emergency Fund Considerations

- Opting for a $1000 deductible requires having at least $1000 readily available to cover repair costs without disrupting your budget.

- If paying $500 or $1000 suddenly would cause financial strain, the higher premium associated with a $500 deductible may be a safer and more practical choice.

- Financial experts often recommend aligning your deductible with your emergency fund; if you can't comfortably cover $1000, the lower deductible reduces financial risk during unexpected events.

Frequently Asked Questions

What does liability coverage include in auto insurance?

Liability coverage pays for injuries and property damage you cause to others in an accident. It does not cover your own injuries or vehicle damage. This coverage typically includes two parts: bodily injury liability and property damage liability. Most states require minimum liability limits. Choosing higher limits can provide better financial protection and is often recommended for added security.

What is comprehensive coverage in auto insurance?

Comprehensive coverage helps pay for damage to your car from non-collision events like theft, fire, vandalism, falling objects, or animal strikes. It does not cover collision damage or personal injury. Comprehensive coverage usually comes with a deductible. It’s optional but recommended if your car is valuable or financed. This coverage helps protect your vehicle from a wide range of unexpected incidents.

How does collision coverage work?

Collision coverage pays for repairs to your vehicle after an accident involving another car or object, regardless of fault. It applies even if you're at fault. This coverage includes damage from events like rollovers or hitting a guardrail. It typically has a deductible. While optional, it’s beneficial for newer or more expensive vehicles. It helps reduce out-of-pocket repair costs after an accident.

What is uninsured/underinsured motorist coverage?

This coverage protects you if you're in an accident with a driver who has no insurance or insufficient coverage. It helps pay for your medical expenses, lost wages, and sometimes property damage. It's crucial in areas with many uninsured drivers. Many states require this coverage. It ensures you’re not left paying high costs due to another driver’s lack of adequate insurance.

Leave a Reply