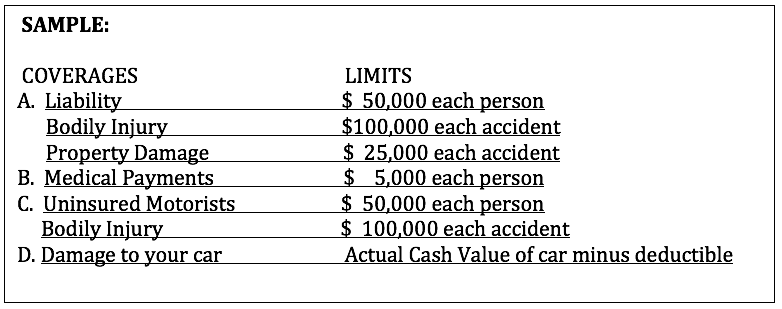

Auto Insurance Explain Split Limits

Auto insurance policies often include split limits, a format used to define the maximum coverage amounts for different types of liability. Represented as three numbers—such as 25/50/25—split limits specify the coverage caps for bodily injury per person, bodily injury per accident, and property damage, respectively.

Understanding this structure is crucial for drivers selecting appropriate protection. While split limits provide clear, segmented coverage, they can also leave policyholders exposed to out-of-pocket expenses if damages exceed the specified amounts. Choosing the right split limits involves balancing cost, risk, and legal requirements in your state.

Understanding Split Limits in Auto Insurance: What You Need to Know

Split limits are a common way auto insurance policies express liability coverage amounts. Instead of a single total amount, split limits divide your coverage into separate maximums for different types of damages: bodily injury per person, bodily injury per accident, and property damage per accident.

Do home insurance cover mold

Do home insurance cover moldThis format is typically displayed as three numbers separated by slashes, such as 25/50/25, which means $25,000 in coverage for injuries to one person, up to $50,000 total for all injuries in a single accident, and $25,000 for property damage. Understanding your split limits is crucial because they determine how much your insurance will pay if you're at fault in a collision, and anything beyond those limits may come out of your pocket.

What Do the Numbers in Split Limits Mean?

The three numbers in a split limit—such as 50/100/50—represent distinct portions of your auto liability coverage. The first number indicates the maximum amount your policy will pay for bodily injury per person in an accident, up to that limit.

The second number is the total coverage available for all bodily injuries per accident, meaning that even if multiple people are injured, the insurer will not pay more than this cap. The third number reflects the maximum coverage for property damage per accident, such as damage to another person's vehicle or property.

For example, with a 50/100/50 policy, your insurer will pay up to $50,000 for one person’s injuries, up to $100,000 total for all injured parties, and up to $50,000 for damaged property. These limits prevent you from being financially responsible for every dollar in damages, but only up to these specified amounts.

Does diy electrical wiring void home insurance

Does diy electrical wiring void home insuranceHow Split Limits Compare to Combined Single Limits

It’s important to understand the difference between split limits and combined single limits (CSL). While split limits divide your liability coverage into separate categories, a combined single limit offers one total amount of coverage for both bodily injury and property damage per accident.

For instance, a CSL policy with a $100,000 limit could pay up to $100,000 for any mix of injuries and damages, as long as the total doesn’t exceed that amount.

This makes CSL more flexible than split limits, which can restrict payouts based on the category. However, split limits are more common and often more affordable. The choice between split and combined limits depends on your risk tolerance, financial situation, and state requirements.

Examples of How Split Limits Work in Real Claims

Consider a driver with a 25/50/25 split limit policy who causes an accident resulting in injuries to two people: one with $30,000 in medical bills and another with $25,000.

Safeu home insurance review

Safeu home insurance reviewThe insurer would pay $25,000 to the first person (hitting the per-person limit) and $25,000 to the second, totaling $50,000—the maximum per-accident bodily injury coverage. The first person would still owe $5,000 out of pocket.

If property damage totaled $30,000, the policy’s $25,000 property damage limit would cover only part of it, leaving the driver liable for the remaining $5,000. This example highlights why choosing adequate limits matters. Below is a comparison table illustrating different split limit options:

| Policy Type | Bodily Injury (Per Person) | Bodily Injury (Per Accident) | Property Damage | Total Coverage Cap |

|---|---|---|---|---|

| 25/50/25 | $25,000 | $50,000 | $25,000 | Up to $75,000 |

| 50/100/50 | $50,000 | $100,000 | $50,000 | Up to $150,000 |

| 100/300/100 | $100,000 | $300,000 | $100,000 | Up to $500,000 |

Note: These totals represent the sum of bodily injury and property damage limits but do not reflect a combined single limit—payments are still restricted by each individual category.

Understanding Split Limits in Auto Insurance: A Comprehensive Guide

What are 100/200/50 split limits in auto insurance and how do they work?

:max_bytes(150000):strip_icc()/TermDefinitions_split-limits-final-ca398d08d85446c0a089ca207a5d9c82.jpg)

Understanding 100/200/50 Split Limits in Auto Insurance

- The 100/200/50 split limit is a common format used to describe the liability coverage amounts in an auto insurance policy. These numbers represent the maximum dollar amounts your insurance will pay per person, per accident, and for property damage in the event you are at fault in a collision.

- The first number, 100, stands for $100,000 in bodily injury liability coverage per person. This means your insurance will cover up to $100,000 in medical expenses, lost wages, or other damages for each injured person in an accident you cause, up to that individual limit.

- The second number, 200, indicates a total of $200,000 in bodily injury liability coverage per accident. Even if multiple people are injured, the total amount your insurer will pay for all injuries in a single accident cannot exceed $200,000.

- The third number, 50, refers to $50,000 in property damage liability coverage per accident. This covers the cost of damage your vehicle causes to another person's property, such as their car, fence, or building.

How 100/200/50 Coverage Applies After an Accident

- When you are responsible for an accident, your insurance company uses the split limits to determine how much they will pay out to the other parties involved. For example, if three people are injured and each has $80,000 in medical bills, your policy would cover all of it since each claim is under the $100,000 per person limit and the total of $240,000 exceeds the $200,000 per accident cap.

- In such a case, the insurer would pay up to $200,000 for all bodily injuries combined, even though the total damages are higher. You could be personally liable for the remaining $40,000 if the injured parties pursue legal action and a court orders payment beyond your coverage.

- For property damage, if you cause $45,000 in damage to another vehicle and structure, your insurer would cover the full amount since it is below the $50,000 limit. However, if the damage totals $60,000, you would be responsible for the $10,000 difference unless you have additional coverage like an umbrella policy.

- It is important to note that these limits only apply to the other people involved; they do not cover your own medical bills or vehicle repairs, which would require separate coverages such as personal injury protection or collision insurance.

Why Choosing 100/200/50 Coverage Matters

- Selecting 100/200/50 split limits provides a balanced level of protection that exceeds many state minimum requirements, helping to reduce the risk of out-of-pocket expenses after a serious accident.

- Medical costs and vehicle repairs have risen over time, making higher limits more important. A single serious injury can quickly surpass $100,000 in expenses, and multiple injuries can exceed $200,000, leaving underinsured drivers exposed to lawsuits.

- Having $50,000 in property damage coverage may be sufficient for most standard vehicles, but it could fall short in cases involving expensive cars, commercial vehicles, or substantial property damage, such as crashing into a home or business building.

- Insurance professionals often recommend at least 100/200/50 coverage, especially in areas with high traffic density or costly healthcare. It offers a reasonable compromise between affordability and protection against financial loss due to liability claims.

What Do $250,000/$500,000 Split Limits Mean in Auto Insurance Coverage?

Understanding Split Limits in Auto Insurance

- Split limits in auto insurance refer to the way coverage amounts are divided across different types of liability protection. In a $250,000/$500,000 split limit policy, the numbers represent maximum payout amounts for specific categories of bodily injury claims. The first figure ($250,000) indicates the most the insurer will pay per person injured in an accident you cause, while the second figure ($500,000) represents the total amount available for all injuries in a single accident, regardless of how many people are hurt.

- This structure ensures that the insurance company’s financial responsibility is capped both on an individual and aggregate basis. It is important to recognize that these limits do not apply to property damage, which typically has a separate limit outlined in the policy, such as $100,000 or $250,000.

- Understanding the separation of these limits is essential because exceeding them means you could be held personally responsible for any additional costs. For example, if one person suffers severe injuries requiring $300,000 in medical expenses, your policy would only cover $250,000, leaving you liable for the remaining $50,000.

Breakdown of $250,000/$500,000 Coverage

- The $250,000 portion of the split limit refers to the bodily injury liability coverage per person. This means if one individual is injured in an accident you're at fault for, your insurance will cover up to $250,000 in medical bills, lost wages, pain, and suffering for that individual. This per-person cap is designed to prevent excessive payouts for a single claimant, helping to manage risk for the insurer.

- The $500,000 component is the per-accident total for all bodily injury claims combined. So, if multiple people are injured, the total paid out for all medical and related expenses cannot exceed $500,000. For instance, if three people are injured and each requires $200,000 in damages, the total cost would be $600,000, but your policy would only cover $500,000, leaving $100,000 as your personal liability.

- This breakdown helps policyholders assess whether their coverage is sufficient based on potential risk scenarios. High-cost medical treatments, long-term disability, or lawsuits can quickly surpass these limits, so drivers in areas with higher litigation rates or medical costs may consider higher coverage tiers.

Why Choosing $250,000/$500,000 Limits Matters

- Selecting a $250,000/$500,000 split limit strikes a balance between affordability and protection for many drivers. It offers a significant increase in coverage compared to state minimum requirements, which are often as low as $25,000 per person, helping reduce the risk of out-of-pocket expenses after a serious accident.

- This level of coverage is often recommended by insurance professionals, especially for drivers with assets to protect. If a lawsuit exceeds your policy limits, plaintiffs can pursue your personal savings, real estate, or future income. Higher limits act as a financial safeguard in such situations.

- Additionally, opting for $250,000/$500,000 limits may be required by lenders if you have a leased or financed vehicle and can enhance your overall protection without a dramatic increase in premium costs, particularly when bundled with other insurance policies or discounts.

What does a 50/100/25 split limit mean in auto insurance?

Understanding the Structure of 50/100/25 Split Limits

- A 50/100/25 split limit in auto insurance refers to the specific dollar amounts of coverage available under bodily injury and property damage liability portions of a policy. The three numbers represent thousands of dollars and break down into maximum coverage per person, per accident, and for property damage.

- The first number, 50, stands for $50,000 in coverage for bodily injury liability per person injured in an at-fault accident. This means if one person sustains injuries, the insurance will pay up to $50,000 to cover their medical expenses, lost wages, and other related costs.

- The second number, 100, refers to $100,000 as the total maximum coverage for bodily injury per accident, regardless of the number of injured parties. If multiple people are hurt, the total payout for all injuries combined cannot exceed $100,000, with individual payouts capped at $50,000 each.

What the 25 in 50/100/25 Represents

- The last number, 25, corresponds to $25,000 in property damage liability coverage. This portion of the split limit pays for damage your vehicle causes to someone else’s property, such as another car, fence, or building, when you are at fault.

- If you cause an accident that damages multiple vehicles or other structures, your insurer will cover the repairs or replacements up to the $25,000 limit. You are personally responsible for any costs exceeding this amount.

- Property damage liability is essential because repair or replacement costs for vehicles can quickly surpass $25,000, especially if newer models are involved. Drivers in areas with high vehicle values may consider higher limits for better protection.

Why 50/100/25 Is a Common Coverage Choice

- The 50/100/25 split limit is widely adopted because it offers balanced protection that meets or exceeds the minimum requirements in many U.S. states. It provides a moderate level of coverage for both bodily injury and property damage.

- Many drivers find this tier sufficient for average risk exposure, especially if they drive moderately and own an older vehicle. Insurance companies often present this as a standard package option when shopping for policies.

- Despite its popularity, some financial advisors and insurance experts suggest higher limits, particularly for individuals with significant assets. Medical bills and vehicle repair costs continue to rise, making higher limits a prudent choice for long-term financial protection.

Frequently Asked Questions

What does split limits mean in auto insurance?

Split limits in auto insurance refer to a policy that divides coverage into separate amounts for bodily injury per person, bodily injury per accident, and property damage. For example, 25/50/20 means $25,000 per person for injuries, up to $50,000 total per accident, and $20,000 for property damage. This format gives clear, distinct coverage levels for different types of losses.

How do split limits affect my coverage after an accident?

Split limits determine the maximum your insurer will pay for each type of damage after an accident. If you're at fault, the bodily injury per person limit covers one injured party, up to the per-accident cap for all injuries, and property damage has a separate limit. If costs exceed these amounts, you may have to pay the difference out of pocket.

What is an example of how split limits work in a real claim?

If you cause an accident with split limits of 50/100/25, your insurer pays up to $50,000 in medical expenses per injured person, with a $100,000 total cap for all injuries from that accident, and up to $25,000 for vehicle or property repairs. If three people suffer $40,000 each in injuries, the total $120,000 exceeds the $100,000 limit, leaving $20,000 uncovered.

Are split limits better than a single combined limit?

Split limits offer more detailed coverage control and are often more affordable than a single combined limit policy. However, combined limits provide greater flexibility, as the full amount can be used for any claim type. Split limits may leave you underinsured if medical costs exceed per-person or per-accident caps, so choosing depends on your risk tolerance, budget, and state requirements.

Leave a Reply