Auto Insurance Reform Michigan

Michigan’s auto insurance system has undergone significant reform in recent years, reshaping how drivers access and pay for coverage. Long known for having some of the highest premiums in the nation, the state implemented sweeping changes aimed at increasing affordability and flexibility.

The 2019 reform legislation introduced new options for personalized coverage, including the ability to choose lower personal injury protection (PIP) limits. These changes were designed to reduce financial strain on consumers while maintaining essential protections. As the market adjusts, stakeholders continue to assess the long-term impact on premiums, coverage choices, and overall system stability.

Understanding Auto Insurance Reform in Michigan

Michigan has undergone significant changes in its auto insurance landscape with the passage of comprehensive auto insurance reform in 2019. Prior to this, Michigan had some of the highest auto insurance premiums in the nation due to its unique no-fault system, which guaranteed lifetime personal injury protection (PIP) benefits regardless of fault.

Home insurance quote columbia

Home insurance quote columbiaThe reform, officially known as Public Act 21 of 2019, aimed to increase affordability and consumer choice by restructuring how medical coverage is handled in auto insurance policies. Key elements of the reform included allowing drivers to choose their level of PIP coverage—from unlimited to lower limits or even opt-out if covered by Medicare or other health plans—along with the creation of a state-run reinsurance program to stabilize rates.

This shift has made premiums more flexible but has also raised concerns about reduced benefits for seriously injured individuals. As the reform continues to be implemented, both consumers and insurers are adjusting to a more dynamic and varied insurance marketplace in Michigan.

Key Components of Michigan’s Auto Insurance Reform

The centerpiece of Michigan’s auto insurance reform is the change in Personal Injury Protection (PIP) options. Before 2019, all drivers were automatically enrolled in unlimited PIP coverage, contributing to sky-high premiums.

The reform introduced tiered PIP coverage levels, allowing drivers to select from $250,000, $500,000, or unlimited coverage, or opt out entirely if they have qualified state health insurance or Medicare. Additionally, the reform created the Moving Forward Fund, a state reinsurance program that reimburses insurers for a portion of high-cost no-fault claims, helping to reduce overall premium costs.

Home insurance quote little rock

Home insurance quote little rockThe law also strengthened anti-fraud measures, established a personalized credit scoring rule limiting its use in rate determination, and mandated a review of rate increases. These components were designed to give consumers greater control over their insurance costs while maintaining essential protections.

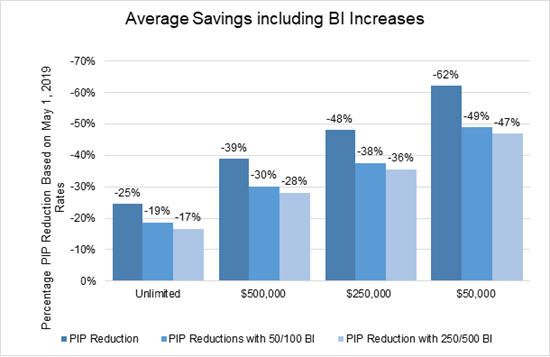

Since the implementation of the reform, Michigan drivers have experienced a noticeable decline in average auto insurance premiums, although the extent varies by region and individual circumstances. According to data from the Michigan Department of Insurance and Financial Services (DIFS), average premiums dropped by more than 10% in the first year post-reform.

The introduction of choice in PIP coverage has enabled drivers to tailor their policies based on personal health coverage and financial needs. However, critics argue that reducing or opting out of PIP coverage may leave vulnerable populations underinsured in the event of a catastrophic injury.

Elderly drivers on Medicare and low-income individuals without supplemental health care could face financial strain if they suffer serious accidents without adequate injury protection. While cost savings are significant, the long-term societal impact of reduced coverage levels remains a subject of ongoing debate among policymakers and consumer advocates.

Home insurance water damage leaking roof coverage

Home insurance water damage leaking roof coverageChallenges and Ongoing Adjustments

Despite the progress made through reform, Michigan’s auto insurance system continues to face challenges. Insurers have raised concerns about the financial sustainability of the reinsurance program, especially amid rising medical costs and provider billing disputes.

Additionally, the complexity of navigating new coverage options has caused confusion among consumers, with some unintentionally selecting inadequate coverage. Independent agents and government outreach campaigns have worked to improve understanding, but gaps remain.

Moreover, legal battles over provider reimbursement rates, particularly concerning medical providers asserting rights to unlimited billing, have created uncertainty in the claims process. The state continues to monitor these issues closely, with periodic legislative reviews scheduled to assess whether further adjustments to the law are needed to balance affordability, protection, and market stability.

| Reform Feature | Pre-Reform (Before 2019) | Post-Reform (After 2019) |

|---|---|---|

| PIP Coverage | Unlimited medical benefits mandatory | Choice of $250K, $500K, unlimited, or opt-out |

| Average Premium | Highest in the U.S. (~$2,800/year) | Reduced by 10-20% on average |

| Reinsurance Program | None | State-run Moving Forward Fund in place |

| Credit Scoring | Major factor in pricing | Rate increases limited by credit-based factors |

| Consumer Protection | Limited choice and transparency | Enhanced disclosure and fraud prevention measures |

Understanding Michigan Auto Insurance Reform: A Comprehensive Guide

Is Michigan maintaining its no-fault status in 2025 after auto insurance reforms?

Yes, Michigan is maintaining its no-fault status in 2025 after the auto insurance reforms. The changes implemented in recent years, particularly those stemming from the landmark reform legislation passed in 2019, have reshaped how personal injury protection (PIP) benefits are structured within the existing no-fault framework—but they have not eliminated no-fault insurance altogether.

As of 2025, Michigan remains a no-fault auto insurance state, meaning that drivers involved in accidents generally must seek compensation for medical expenses and certain other losses from their own insurance companies, regardless of who caused the crash.

The reforms introduced more flexibility for consumers by allowing them to choose different levels of PIP coverage or opt out entirely under specific circumstances, but the core principle of no-fault insurance continues to apply across the state.

What Changes Did the 2019 Auto Insurance Reforms Bring to Michigan’s No-Fault System?

- One of the most significant changes introduced in 2019 was the ability for drivers to choose their level of Personal Injury Protection (PIP) coverage, ranging from unlimited medical coverage to as low as $25,000 or even opting out if covered by a qualified health plan or Medicare. This marked a major departure from the previous requirement of unlimited PIP coverage for all drivers.

- Insurers were mandated to offer a choice of PIP coverage tiers at policy renewal or purchase, increasing consumer awareness and empowering individuals to make cost-conscious decisions based on their medical insurance and financial situations.

- The reforms also included provisions to control costs by improving coordination between auto and health insurers, limiting attorney fee structures, and establishing a fee schedule for reimbursement of PIP medical services, which helped reduce overall premium costs over time.

How Does Michigan’s No-Fault System Function in 2025 After the Reforms?

- In 2025, Michigan’s no-fault system still ensures that injured parties receive prompt payment for medical bills, rehabilitation costs, lost wages, and other covered economic losses through their own auto insurance policy, without having to prove fault in an accident.

- The core structure of no-fault remains intact, but with tiered PIP options now being the standard, individuals must actively select their desired level of coverage, making insurance purchasing more personalized but also placing greater responsibility on consumers to understand their choices.

- Additionally, the reformed system maintains the right to sue in cases of serious injury under specified thresholds, such as permanent serious disfigurement or disabling injury, preserving a balance between no-fault benefits and tort liability.

What Impact Have the Reforms Had on Premiums and Consumer Choice?

- Since the reforms took effect, average auto insurance premiums in Michigan have decreased significantly compared to the years before 2019, offering financial relief to many drivers who previously faced some of the highest rates in the nation.

- Consumers now have greater autonomy in shaping their coverage, with a substantial number of policyholders selecting lower PIP limits or opting out due to existing health coverage, reflecting a shift toward customized, cost-effective insurance solutions.

- However, concerns remain about the long-term adequacy of lower coverage levels in catastrophic injury cases, prompting ongoing discussions among policymakers, insurers, and consumer advocates about ensuring sufficient protection within the reformed no-fault model.

Will auto insurance rates in Michigan decrease following recent insurance reforms?

- Michigan's auto insurance landscape underwent significant changes with the no-fault reform legislation passed in 2019, which allowed drivers to choose their level of personal injury protection (PIP) coverage. Prior to this reform, Michigan required unlimited medical coverage for accident-related injuries, a major driver of high premiums. By enabling policyholders to opt for lower coverage tiers—including options with $250,000, $500,000, or no PIP coverage—premiums have seen downward pressure.

- The ability to customize coverage has empowered consumers to align their policies with individual risk tolerance and financial situations, contributing to reduced average costs. Insurers, in turn, have recalibrated their pricing models based on these new risk parameters, resulting in lower base rates, especially for drivers who elect minimal or no PIP benefits.

- Actuarial data from the Michigan Department of Insurance and Financial Services (DIFS) has shown a measurable decline in average premiums since the reform's implementation. However, the extent of savings varies significantly based on region, driving history, and chosen coverage, indicating that while rates have decreased overall, the benefit distribution is not uniform across all driver demographics.

Role of Increased Market Competition

- Another consequence of the reform has been increased competition among insurance providers. With more flexibility in coverage options and regulatory oversight aimed at curbing excessive pricing, new insurers have entered the Michigan market, and existing carriers have introduced more competitive rate structures.

- Greater competition has led to more transparent pricing and promotional incentives, such as multi-policy discounts, safe-driver programs, and digital policy management tools, all of which contribute to affordability. This dynamic has further encouraged rate reductions as companies strive to capture or retain market share in a newly liberalized environment.

- Consumer choice has expanded significantly, and annual rate comparisons have become more impactful. Data from insurance comparison platforms show that Michigan drivers who actively shop around can achieve savings of 20% or more by switching carriers, indicating that market forces are now playing a stronger role in moderating costs.

Influence of Ongoing Regulatory Oversight and Adjustments

- The Michigan Catastrophic Claims Association (MCCA), which handles extremely high-cost injury claims, has also undergone changes affecting premiums. The per-vehicle assessment charged by the MCCA has fluctuated, but recent trends show reduced surcharges due to investment gains and lower-than-expected claim volumes, contributing to lower overall insurance costs.

- Regulatory caps on attorney fee structures related to no-fault claims have helped reduce systemic cost drivers such as fraud and inflated settlements. These legal reforms have led to lower claim payouts, which insurers have passed on to consumers in the form of reduced rates.

- Ongoing monitoring by DIFS ensures compliance with rate-filing standards and fairness in pricing practices. While future fluctuations may occur based on economic conditions or claim trends, the regulatory framework established by the reforms continues to support a more stable and responsive auto insurance market in Michigan.

Is Michigan still a no-fault auto insurance state after recent reforms?

Yes, Michigan remains a no-fault auto insurance state after the recent reforms implemented in 2020, although the system has undergone significant changes that have fundamentally altered how personal injury protection (PIP) benefits are structured.

The core principle of no-fault insurance—which guarantees medical and related benefits to accident victims regardless of who caused the crash—still applies.

However, the mandatory unlimited lifetime medical coverage was replaced with a tiered system, allowing drivers to choose their level of PIP coverage. This reform aimed to reduce spiraling insurance premiums while maintaining essential protections for injured drivers and passengers.

What Changes Did Michigan’s Auto Insurance Reforms Introduce?

- The 2019 reforms, effective July 2020, ended the previous requirement for all drivers to carry unlimited personal injury protection (PIP) medical coverage. Instead, policyholders can now select from several PIP coverage options, ranging from unlimited medical coverage to lower limits such as $50,000, $250,000, or opting out entirely if they or a household member have qualifying group health insurance.

- Another major change involves the assignment of future claims for Michigan’s Catastrophic Claims Association (MCCA) fee. Drivers who had auto insurance policies in place before June 11, 2019, retain lifetime access to the MCCA backstop, but new drivers and those who let their coverage lapse may face reduced MCCA support as they pay into the system only for a limited time based on their days of coverage.

- The reforms also introduced greater rate regulation, requiring insurance companies to justify rate increases more transparently. This was designed to increase competition and reduce premiums, which were historically among the highest in the nation.

How Has the No-Fault Core Principle Been Preserved?

- Maintaining the essence of no-fault insurance, Michigan law still mandates that auto insurers must provide medical benefits, wage loss, survivor benefits, and attendant care to injured parties without considering fault at the time of the collision. This continues to differentiate Michigan from at-fault (tort-based) states where victims must prove negligence to recover damages.

- Drivers are still required to carry PIP coverage as part of their auto policy unless they affirmatively opt out under specific conditions, such as having acceptable health coverage that applies to auto-related injuries. This ensures that most people injured in auto accidents continue to receive timely medical care without lengthy legal disputes.

- The no-fault system also still allows injured individuals to sue for non-economic damages—such as pain and suffering—only if they suffer a “serious impairment of body function,” a threshold that remains in place to limit litigation and ensure the system focuses on significant injuries.

- Following the reforms, average auto insurance premiums in Michigan decreased significantly for many drivers, especially those who opted for lower levels of PIP coverage. This made coverage more affordable and allowed consumers greater control over their insurance choices based on personal health coverage and financial circumstances.

- However, some consumers, particularly those who chose to keep unlimited coverage or have complex medical needs, have seen more modest savings or even continued high costs. The expected broader market competition has been slow to materialize uniformly across all regions and insurance providers.

- There are also concerns about the long-term sustainability of the MCCA under the new tiered access model. With new drivers contributing based on days of coverage rather than permanent access, some experts worry about future funding gaps if catastrophic injury claims rise while contributions decline.

Frequently Asked Questions

What did the Michigan auto insurance reform change in 2019?

The 2019 Michigan auto insurance reform changed how personal injury protection (PIP) coverage is structured.

Previously, all drivers had unlimited medical benefits, but the reform introduced tiered options. Now, drivers can choose different levels of PIP coverage, including opting out entirely with written confirmation. The reform also aimed to reduce insurance premiums and improve system transparency by offering more affordable choices and enhancing oversight.

Can I opt out of unlimited medical coverage under the new Michigan law?

Yes, under the Michigan auto insurance reform, you can opt out of unlimited personal injury protection (PIP) medical coverage. To do so, you must sign a no-fault election form provided by your insurer confirming your decision.

This option helps reduce premium costs, but you’ll need alternative medical coverage, like a health plan that covers auto accident injuries. Always ensure your chosen health insurance covers such injuries before opting out.

The auto insurance reform in Michigan aimed to reduce high insurance premiums by introducing more coverage choices. Since policyholders can now select lower or no PIP coverage, many drivers have seen premium decreases.

However, actual savings vary based on driving history, location, and coverage selection. While prices have dropped overall, they are influenced by multiple factors, including insurer policies and individual risk profiles, resulting in mixed outcomes across the state.

What are the new PIP coverage options available in Michigan?

Michigan now offers several PIP coverage options: unlimited medical benefits, $500,000, $250,000, $50,000, or opting out with qualified health coverage.

Drivers injured in accidents can receive benefits based on their chosen tier. The options allow for more personalized and potentially lower-cost policies. Each level affects how much the insurance will pay for medical treatment after an accident, giving drivers more control over their coverage and costs.

Leave a Reply