Auto Insurance Saver Reviews

Auto Insurance Saver has emerged as a popular platform for consumers seeking affordable and tailored car insurance options. By partnering with multiple insurers, it allows users to compare quotes and find policies that fit their specific needs and budgets. Reviews of Auto Insurance Saver highlight its user-friendly interface, transparency in pricing, and efficient customer service.

While many appreciate the time and money saved through its comparison tool, some users note variability in coverage options and post-purchase support. This article examines real customer feedback, industry insights, and performance metrics to provide a comprehensive evaluation of Auto Insurance Saver’s reliability, benefits, and potential drawbacks in today’s competitive insurance market.

Auto Insurance Saver Reviews: Evaluating the Pros, Cons, and Customer Experiences

Auto Insurance Saver is a digital insurance broker that aims to help drivers find affordable auto insurance by comparing quotes from multiple providers across the U.S. The platform positions itself as a cost-effective solution for consumers looking to reduce monthly premiums without sacrificing coverage.

Home insurance quote columbia

Home insurance quote columbiaReviews of Auto Insurance Saver are mixed, with some users praising its user-friendly interface and ability to deliver competitive pricing, while others express concerns about follow-up service, agent responsiveness, and transparency in pricing post-initial quote.

Many customers appreciate that the service is free to use and requires no obligation, making it a low-risk option when shopping for insurance. However, it's essential to understand how Auto Insurance Saver works, what customers are saying, and how it compares to other quote comparison platforms before trusting it with your personal information and insurance decisions.

What Is Auto Insurance Saver and How Does It Work?

Auto Insurance Saver operates as an online insurance marketplace that connects customers with a network of insurance providers and independent agents.

When users enter their personal and vehicle information on the website, Auto Insurance Saver uses this data to generate multiple quotes from different insurers, allowing consumers to compare coverage options and pricing side by side. The service does not underwrite policies directly but serves as a lead generation tool; once a quote is selected, a licensed agent from a partner company contacts the customer to finalize the policy.

Home insurance quote little rock

Home insurance quote little rockThis model allows Auto Insurance Saver to offer free quote comparisons and cater to a wide range of driver profiles, including those with less-than-perfect credit or a history of accidents. While convenient, users should be aware that the initial quote may not reflect the final rate, as agents may adjust premiums based on a more detailed risk assessment.

Customer Feedback and Common Complaints

Customer reviews of Auto Insurance Saver reveal a range of experiences, with many users reporting savings on their premiums and a quick, straightforward quoting process. Positive feedback frequently mentions the convenience of receiving multiple options in one place and the absence of pressure to buy immediately.

However, negative reviews often focus on lack of communication from assigned agents, delayed responses, or difficulty reaching representatives after submitting information. Some consumers also complain about unexpected rate increases after the initial quote or feeling misled about the final price.

Third-party review platforms like Trustpilot and the Better Business Bureau (BBB) show lower average ratings for Auto Insurance Saver, citing issues with transparency and post-quote customer support. These insights suggest that while the platform can deliver initial savings, the overall experience may vary significantly depending on the agent and insurer connected through the service.

Home insurance water damage leaking roof coverage

Home insurance water damage leaking roof coverageComparison With Other Auto Insurance Quote Services

When compared to other well-known insurance aggregators like Insurify, The Zebra, or NerdWallet, Auto Insurance Saver holds a modest position in the digital insurance landscape. These platforms offer similar services—generating multiple quotes from top insurers—but differ in user experience, data accuracy, and customer support.

One advantage of Auto Insurance Saver is its broad network of carriers, which may include regional and specialized insurers not always found on larger comparison sites. However, competitors often provide more detailed side-by-side comparisons, real-time pricing, and integrations with customer reviews of insurance companies.

Additionally, some platforms use advanced algorithms to personalize recommendations based on driving habits and financial priorities, while Auto Insurance Saver tends to rely on basic demographic and vehicle data. The table below summarizes key features across leading auto insurance comparison tools, highlighting where Auto Insurance Saver excels and where it falls short.

| Feature | Auto Insurance Saver | The Zebra | Insurify | NerdWallet |

|---|---|---|---|---|

| Free Quotes | Yes | Yes | Yes | Yes |

| Real-Time Pricing | Limited | Yes | Yes | Yes |

| Agent Follow-Up | Yes, varies by provider | Optional | Yes | No (direct insurer contact) |

| BBB Accredited | No | Yes | Yes | Yes |

| Customer Reviews Integration | No | Yes | Yes | Yes |

| Mobile App Availability | No | Yes | Yes | No |

Auto Insurance Saver Reviews: A Comprehensive and Unbiased Guide

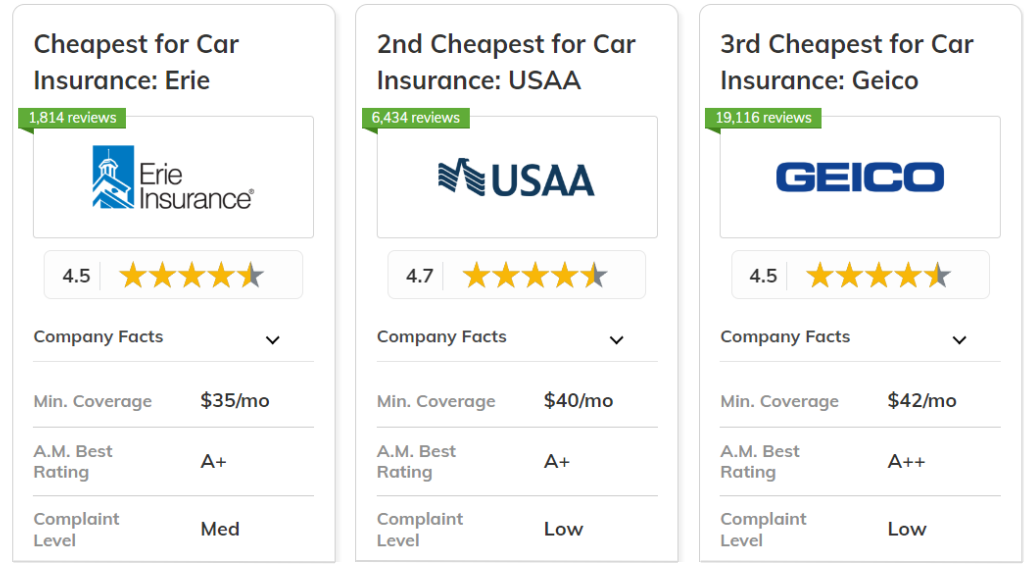

Who Offers the Most Affordable Car Insurance According to Auto Insurance Saver Reviews?

Home insurance with accidental damage

Home insurance with accidental damageTop Budget-Friendly Car Insurance Providers According to Auto Insurance Saver

- Based on comprehensive assessments by Auto Insurance Saver, several insurers consistently appear as the most affordable choices for drivers seeking low premiums without sacrificing essential coverage. These include companies like GEICO, State Farm, and Progressive, which frequently rank at the top due to their competitive base rates and broad eligibility for discounts.

- GEICO often leads the list for drivers with clean records and good credit, offering some of the lowest average annual premiums across multiple states. Their strong digital platform and military affiliation discounts contribute to their affordability appeal.

- State Farm, leveraging its vast network of local agents and longstanding reputation, provides personalized quotes that frequently result in cost savings, particularly for homeowners and multi-policy holders, making it a top contender in price-conscious evaluations.

How Auto Insurance Saver Evaluates Cost and Value in Insurance Quotes

- Auto Insurance Saver analyzes affordability by comparing average annual premiums across dozens of insurance carriers, factoring in real user data, state-specific regulations, and coverage limits such as 100/300/100 liability.

- The platform considers not just base prices but also the availability and variety of discounts—such as safe driver, bundling, low-mileage, and autopay reductions—which significantly impact the final cost of a policy.

- Ratings also incorporate customer satisfaction scores and claims handling efficiency to ensure that affordable insurers also deliver reliable service, filtering out companies that may offer low prices but poor support during claims.

Factors Influencing Which Insurer is Most Affordable for Different Drivers

- Affordability varies significantly based on individual circumstances including age, driving history, location, credit score, and vehicle type. For example, younger drivers may find better rates with companies like USAA (for military families) or Nationwide, which offer strong student and good-grade discounts.

- Drivers in urban areas with higher traffic density and theft rates might see better pricing from Progressive, which uses advanced telematics through its Snapshot program to reward safe driving behaviors regardless of location-based risks.

- Those with recent violations or at-fault accidents may benefit more from insurers like The General or Dairyland, which specialize in high-risk coverage and still rank favorably on Auto Insurance Saver for value under challenging circumstances.

Is EBT Car Insurance a Legitimate Option According to Auto Insurance Saver Reviews?

What Is EBT Car Insurance and How Is It Marketed?

- EBT Car Insurance is not an official insurance provider but rather a term used by some marketing campaigns that suggest individuals receiving benefits via an Electronic Benefits Transfer (EBT) card may qualify for discounted auto insurance. These promotions are often tied to third-party insurance aggregators claiming to connect low-income drivers with affordable coverage.

- Auto Insurance Saver, one such comparison platform, frequently appears in searches related to EBT Car Insurance. It positions itself as a service that helps users compare quotes from multiple insurers, with some advertisements implying eligibility for special rates based on EBT usage.

- However, no direct link exists between receiving government assistance through EBT and legally mandated reductions in car insurance premiums. Any advertised discounts are typically part of broader low-income or high-risk driver programs offered independently by certain insurers, not tied exclusively to EBT status.

What Do Auto Insurance Saver Reviews Reveal About EBT Car Insurance Claims?

- Customer reviews of Auto Insurance Saver show mixed experiences, with some users appreciating the quick quote comparisons while others report misleading advertising, especially regarding the availability of EBT-specific deals. Many reviewers were confused by the implication that EBT recipients automatically qualify for lower rates.

- Multiple third-party review platforms indicate that Auto Insurance Saver does not itself sell insurance but acts as a lead generator, redirecting users to partner agents or insurers. This intermediary role can sometimes result in inconsistent service quality and unclear communication about actual eligibility criteria.

- According to analysis from insurance watchdog groups, some campaigns associated with Auto Insurance Saver use questionable tactics, such as suggesting a government-backed insurance program for EBT users, which does not exist. These claims have drawn scrutiny for potentially deceiving vulnerable consumers.

Are There Legitimate Low-Cost Insurance Options for EBT Recipients?

- While EBT status alone does not qualify someone for discounted auto insurance, many states offer low-cost automobile insurance programs aimed at low-income drivers. Examples include California’s Low Cost Automobile Insurance Program (CLCA) and New Jersey’s Special Automobile Insurance Policy (SAIP), which have income-based eligibility requirements that may include EBT recipients.

- These state-sponsored programs provide minimum liability coverage at reduced premiums and are administered through participating private insurers. Enrollment typically requires proof of income, residency, and completion of a certified driver education course.

- For those seeking alternatives, nonprofit organizations and community outreach programs sometimes partner with insurers to offer education and subsidies. It is advisable for EBT recipients to research official state insurance department resources rather than relying on commercial lead-generation sites that use EBT as a marketing term.

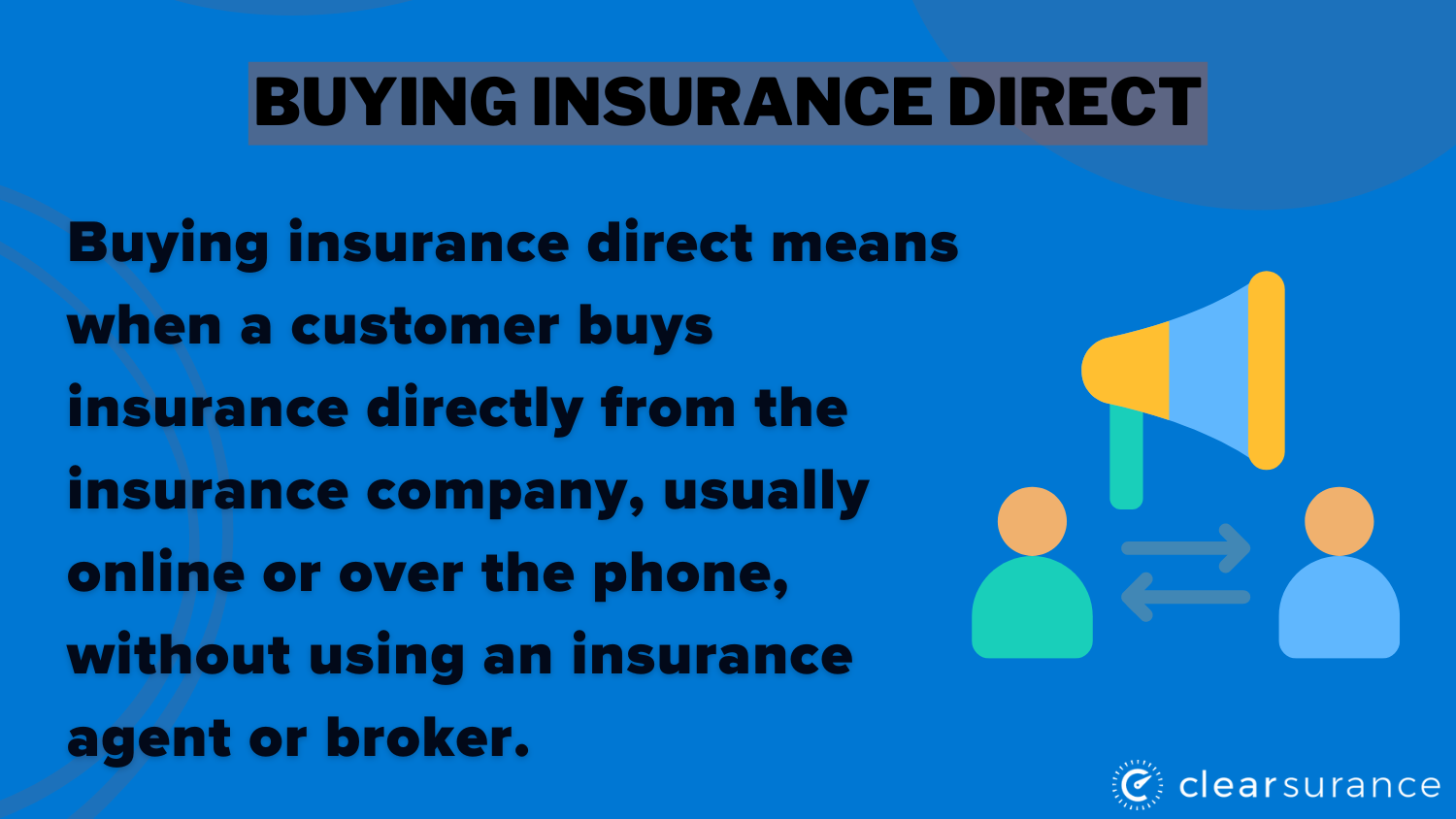

Is buying auto insurance directly from the insurer more cost-effective than using third-party platforms?

Price Comparison and Transparency

When evaluating whether buying auto insurance directly from the insurer is more cost-effective, one must consider how pricing transparency differs between direct and third-party channels.

Insurance companies often market their direct policies as cheaper because they eliminate intermediary commissions. However, third-party platforms aggregate quotes from multiple insurers, allowing consumers to compare prices side by side. This broad visibility can lead to discovering lower rates that might not be immediately available on a single insurer’s website.

- Direct insurers may offer lower advertised rates due to reduced overhead, but these rates are often limited to specific customer profiles or require long-term commitment.

- Third-party platforms can reveal competitive discounts from lesser-known or regional insurers that consumers might otherwise overlook.

- Some direct insurers apply price optimization strategies, charging higher initial rates to customers who don’t shop around, while third-party sites encourage comparison shopping, indirectly promoting better deals.

Availability of Discounts and Bundling Options

The variety and accessibility of discounts play a significant role in determining overall cost-effectiveness. Insurers frequently offer exclusive discounts to customers who purchase policies directly, such as online purchase incentives, loyalty rewards, or multi-policy bundling.

However, third-party platforms may not have access to all these exclusive promotions, potentially causing customers to miss savings opportunities. Still, some independent agents working on third-party websites can unlock additional carrier-specific discounts based on a buyer’s unique profile.

- Direct channels often provide early signing bonuses, paperless billing reductions, and auto-pay discounts that are not always visible or applicable through brokers.

- Customers who bundle home and auto insurance typically receive larger discounts when purchasing both directly from the same insurer.

- Third-party platforms might not fully disclose all eligibility criteria for discounts, leading to inaccurate quote comparisons if key qualifiers like occupation or alumni associations are omitted.

Customer Service and Policy Customization

While cost is a primary concern, the level of service and flexibility offered can indirectly affect value and long-term expenses. Purchasing directly from an insurer allows for continuous customer support through dedicated representatives familiar with the company’s systems and policies.

This can streamline the claims process and help identify cost-saving adjustments over time. In contrast, third-party platforms vary widely in support quality—some offer expert guidance, while others are purely transactional, offering limited post-purchase assistance.

- Direct insurers are more likely to proactively notify policyholders of available rate reductions based on improved driving records or changes in credit score.

- Third-party agents may represent multiple companies, giving them insight into nuanced policy features across insurers, which helps tailor coverage more effectively to individual needs.

- Customers using direct channels may face limited flexibility in payment scheduling or endorsements compared to third-party brokers who can negotiate terms on their behalf with underwriters.

Frequently Asked Questions

What is Auto Insurance Saver and how does it work?

Auto Insurance Saver is an online platform that helps users compare auto insurance quotes from multiple providers. By entering basic information like driving history and vehicle details, users receive personalized quotes.

The service aims to save time and money by offering competitive rates. It partners with reputable insurers and uses secure technology to protect user data. There is no obligation to purchase, making it an easy way to find affordable coverage tailored to individual needs.

Are Auto Insurance Saver reviews trustworthy?

Auto Insurance Saver reviews can offer helpful insights, but should be evaluated critically. Many positive reviews highlight savings and ease of use, while negative ones may point to mismatched expectations or customer service issues.

Independent third-party sites often provide balanced perspectives. Users should consider multiple sources and check review authenticity. Overall, while reviews can guide decisions, personal research and direct comparison of quotes are more reliable when choosing an insurance plan through the platform.

Does using Auto Insurance Saver affect my credit score?

No, using Auto Insurance Saver does not affect your credit score. The platform performs a soft credit inquiry when generating quotes, which insurers may use to assess rates.

Soft inquiries do not impact credit. Only hard inquiries, like those during loan applications, affect scores. Auto Insurance Saver is safe to use for shopping around, and you can compare multiple offers without credit consequences. Always confirm with individual insurers if they use credit-based insurance scores in their pricing.

Can I buy insurance directly through Auto Insurance Saver?

Auto Insurance Saver does not sell insurance directly. Instead, it connects users with licensed insurance providers who offer quotes. After reviewing options, users contact the chosen insurer to finalize and purchase a policy.

The platform simplifies comparison but isn’t an insurance carrier itself. This model allows for transparency and choice. Once you select a plan, the insurer handles all enrollment details, ensuring proper coverage starts according to their terms and timelines.

Leave a Reply