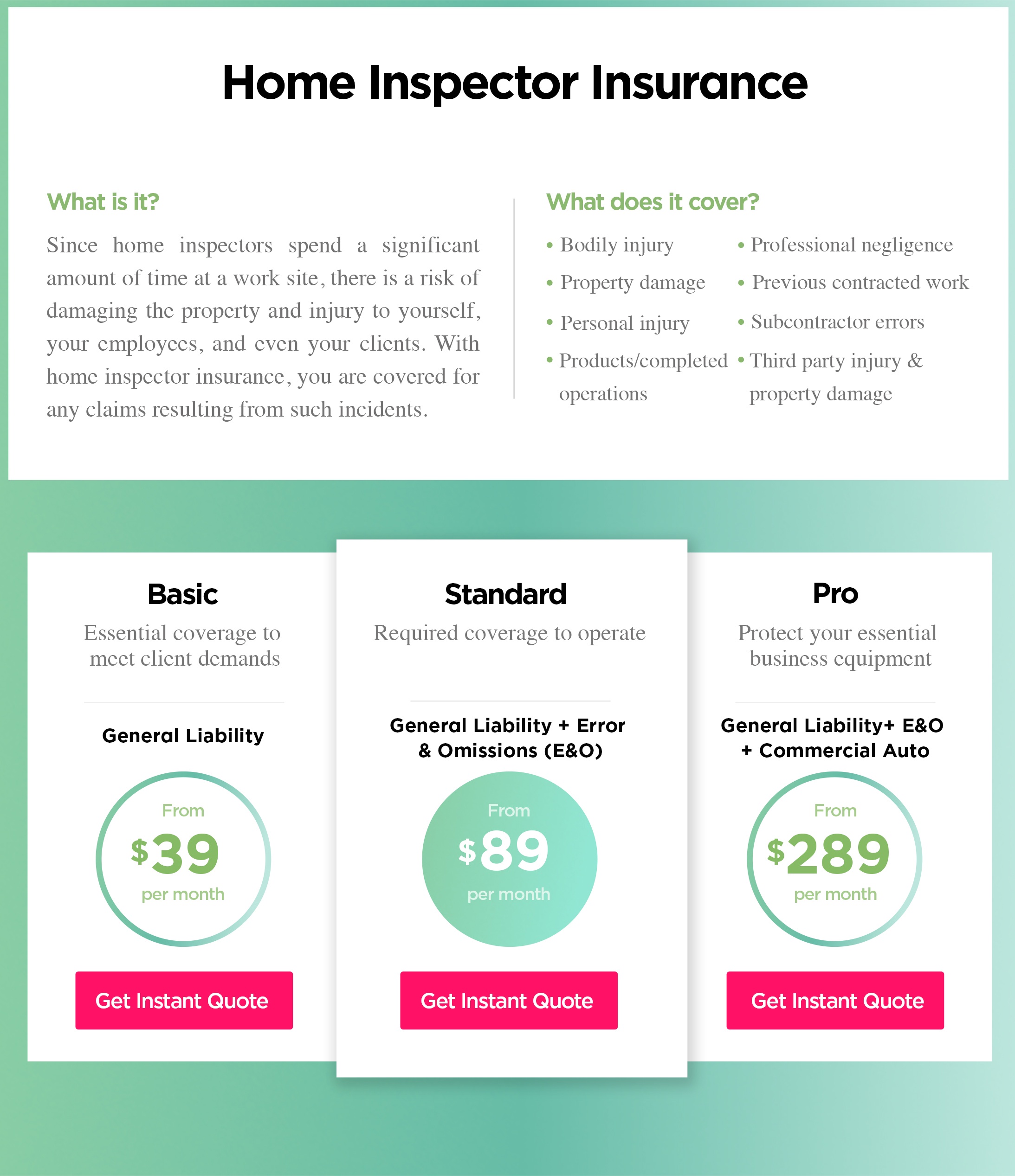

Average cost of home inspector insurance

The average cost of home inspector insurance varies based on several factors, including location, experience, coverage limits, and the size of the inspection business.

Typically, general liability insurance for home inspectors ranges from $500 to $1,500 annually, while errors and omissions (E&O) insurance can add another $750 to $2,000 per year. Combined policies often offer cost savings. High-risk regions or inspectors with prior claims may face higher premiums.

Understanding these costs is essential for home inspectors to secure adequate protection without overspending. This article explores the breakdown of insurance expenses, influencing factors, and tips for finding affordable, comprehensive coverage in the competitive inspection industry.

Can A 20 Year Term Life Insurance Policy Be Extended

Can A 20 Year Term Life Insurance Policy Be ExtendedAverage Cost of Home Inspector Insurance: What You Need to Know

The average cost of home inspector insurance typically ranges between $500 and $1,200 annually, depending on several factors such as geographic location, years of experience, coverage limits, and claims history.

This insurance is essential for home inspectors as it protects against claims of negligence, missed defects, or errors in inspection reports. Most professionals opt for Errors and Omissions (E&O) insurance, also known as professional liability insurance, which is the cornerstone of their coverage.

The cost can vary significantly based on the provider and the scope of the policy, with higher coverage limits and additional endorsements increasing the premium. Understanding these costs helps inspectors budget effectively and ensures they remain compliant with state requirements or client expectations.

Factors That Influence the Cost of Home Inspector Insurance

Several key variables affect the premiums for home inspector insurance. Geographic location plays a major role—inspectors in areas prone to natural disasters or with higher litigation rates often face increased costs.

Cash In On Life Insurance

Cash In On Life InsuranceThe inspector’s level of experience also impacts pricing; newer inspectors may pay more due to perceived higher risk. Coverage amount is another critical factor: a policy with a $1 million per claim limit will cost less than one with a $2 million limit.

Additionally, insurers examine an applicant’s claims history—those with prior claims are seen as higher risk and may face higher premiums or exclusions. Choosing a reputable insurance provider that specializes in inspection services can help secure competitive rates.

Types of Insurance Coverage for Home Inspectors

Home inspectors typically carry multiple types of coverage to ensure comprehensive protection. The most vital is Errors and Omissions (E&O) insurance, which covers financial losses resulting from inaccurate reports or overlooked issues during inspections.

General liability insurance is also common, protecting against bodily injury or property damage that might occur during an inspection, such as accidentally damaging a fixture. Some inspectors may add cyber liability insurance, especially if they store client data electronically, to guard against data breaches.

Guardian Life Insurance

Guardian Life InsuranceWorkers’ compensation insurance is necessary if the inspector has employees. Bundling these coverages into a Business Owner’s Policy (BOP) can sometimes reduce overall costs while providing broad protection.

The following table outlines the average annual premiums for home inspector insurance based on different coverage levels and policy types. These figures are estimates derived from national data and may vary depending on carrier and region.

| Coverage Type | Standard Coverage Limit | Average Annual Premium |

|---|---|---|

| Errors and Omissions (E&O) | $1,000,000 per claim / $2,000,000 aggregate | $600 – $900 |

| General Liability | $1,000,000 per occurrence | $300 – $600 |

| Combined E&O + General Liability | $1M/$2M E&O + $1M GL | $800 – $1,200 |

| Business Owner’s Policy (BOP) | Includes E&O, GL, property, cyber | $1,200 – $1,800 |

Average Cost of Home Inspector Insurance: A Comprehensive Guide

What is the average cost of home inspector insurance?

The average cost of home inspector insurance typically ranges from $500 to $1,200 annually for general liability coverage, while professional liability insurance (also known as errors and omissions insurance) can add another $300 to $1,500 per year.

The total annual premium often falls between $800 and $2,500, depending on several factors such as geographic location, years of experience, business size, claims history, and the scope of services provided. Some home inspectors may also opt for additional coverage like workers’ compensation or cyber liability, which can further influence the overall cost.

Independent inspectors usually pay less than larger firms, and bundling policies through a business owner’s policy (BOP) may offer cost savings. It’s important to obtain quotes from multiple insurers specializing in inspection services to find competitive rates and adequate protection.

Factors That Influence the Cost of Home Inspector Insurance

- Location plays a significant role—inspectors operating in states with higher litigation rates or greater property values often face higher premiums due to increased risk exposure.

- Years of experience and training can impact pricing, as seasoned professionals with clean claims histories are typically viewed as lower-risk by insurers and may receive discounted rates.

- The scope of inspection services offered, such as including radon, mold, or structural assessments, can also raise premium costs due to the expanded liability associated with specialized evaluations.

Types of Insurance Commonly Held by Home Inspectors

- General liability insurance protects against third-party claims of property damage or bodily injury that occur during an inspection, such as accidentally breaking an item while walking through a home.

- Professional liability insurance (errors and omissions) covers financial losses suffered by clients due to missed defects, incorrect reporting, or professional negligence, which are common risks in the inspection field.

- Some inspectors also carry commercial auto insurance if they use a vehicle for business purposes, or cyber liability insurance if they store client data electronically and face risks of data breaches.

How to Reduce the Cost of Home Inspector Insurance

- Combining multiple policies—such as general liability, property insurance, and professional liability—into a single business owner’s policy (BOP) can lead to substantial savings through bundled pricing.

- Maintaining a clean claims history over several years demonstrates reliability to insurers and often results in lower premiums or eligibility for no-claims discounts.

- Completing certified training programs or earning designations from professional organizations like ASHI (American Society of Home Inspectors) can improve credibility and potentially qualify inspectors for reduced rates.

What is the average cost of insurance for house inspectors?

The average cost of insurance for house inspectors typically ranges from $500 to $2,000 per year for professional liability insurance, also known as errors and omissions (E&O) insurance. This range can vary significantly depending on several factors such as geographic location, years of experience, the scope of services offered, and the level of coverage desired.

For instance, inspectors in regions with higher litigation rates or more expensive real estate markets may face higher premiums. Additionally, most house inspectors also carry general liability insurance, which can add another $300 to $800 annually.

Many choose to bundle these policies through a Business Owner’s Policy (BOP), which may reduce overall costs. It’s also common for inspectors to obtain additional coverage such as workers’ compensation (if they have employees) or commercial auto insurance if they use vehicles for inspections.

Factors That Influence Insurance Costs for House Inspectors

- Geographic location plays a major role in determining insurance premiums. Inspectors operating in states with high lawsuit frequencies, such as California or Florida, often pay more due to increased risk exposure.

- The scope and complexity of inspection services impact costs. Those offering specialized assessments like structural, electrical, or mold inspections may require broader coverage, leading to higher premiums.

- An inspector’s claims history and years of experience also affect pricing. New inspectors with no track record may face higher initial rates, while those with clean records over many years can qualify for discounts or lower premiums.

Types of Insurance Commonly Held by House Inspectors

- Professional liability insurance (E&O) is essential, covering financial losses caused by missed defects, incorrect reports, or alleged negligence during an inspection. This is usually the most substantial component of an inspector’s insurance portfolio.

- General liability insurance protects against third-party bodily injury or property damage claims, such as a client tripping over equipment at a property. This complements E&O by addressing physical rather than professional risks.

- Commercial auto insurance applies if the inspector uses a vehicle for business purposes. Personal auto policies typically exclude coverage for business-related use, making this separate policy necessary for adequate protection.

Ways to Reduce Insurance Expenses for Home Inspectors

- Combining multiple policies into a Business Owner’s Policy (BOP) can lead to savings, as insurers often offer bundled rates for general liability, property, and sometimes E&O coverage.

- Maintaining a claim-free history demonstrates reliability to insurers, which can result in loyalty discounts or lower renewal premiums over time.

- Completing certified training programs or earning professional designations, such as Certified Professional Inspector (CPI), may qualify inspectors for reduced rates by showcasing a higher standard of practice and reduced risk.

What is the average cost of liability insurance for home inspectors?

The average cost of liability insurance for home inspectors typically ranges between $500 and $1,200 annually, depending on several key factors.

This type of insurance, often referred to as errors and omissions (E&O) insurance, protects home inspectors from claims related to missed defects, incorrect assessments, or professional negligence during property evaluations.

The exact premium varies based on geographic location, the inspector’s experience, claims history, coverage limits, and the size of the inspection business. Many home inspectors also choose to bundle general liability insurance with their E&O policy, which can affect the total cost but offers more comprehensive protection.

Factors That Influence the Cost of Liability Insurance for Home Inspectors

- Geographic location plays a significant role in determining premiums, as states with higher litigation rates or more stringent building regulations often result in increased insurance costs. For example, inspectors operating in densely populated areas or regions prone to natural disasters may face higher risk exposure.

- The level of experience and professional certifications held by the inspector can also impact pricing. Inspectors with longer experience, proper licensing, and affiliations with recognized organizations like ASHI (American Society of Home Inspectors) may qualify for lower rates due to their perceived reliability and reduced risk.

- Coverage limits and deductible amounts are key components that determine the final cost. Higher coverage limits, such as $1 million per claim and $2 million in aggregate, often lead to higher annual premiums, while selecting a higher deductible can reduce the overall cost but increases out-of-pocket expenses if a claim arises.

Types of Liability Coverage Essential for Home Inspectors

- Errors and omissions (E&O) insurance is the most critical coverage for home inspectors, addressing claims of professional negligence, oversights in inspection reports, or failure to identify major property issues. This coverage is specifically designed to protect against financial losses stemming from inaccurate or incomplete inspections.

- General liability insurance covers third-party bodily injuries or property damage that might occur during an inspection, such as accidentally damaging a client’s fixture or slipping and breaking an item. While not directly related to the inspection report, it protects against physical risks associated with the job.

- Some inspectors also opt for cyber liability insurance, especially if they store client data or digital reports online. This coverage safeguards against data breaches or loss of sensitive customer information, which has become increasingly important in digital documentation practices.

- Maintaining a clean claims history is one of the most effective ways to keep premiums low. Insurers view inspectors with few or no prior claims as lower risk, which often translates into more favorable rates during policy renewals.

- Completing continuing education courses and obtaining advanced certifications can demonstrate professional competence and commitment to quality, leading insurers to offer discounts or reduced premiums.

- Comparing quotes from multiple insurance providers and working with a specialist in professional liability for inspectors can help identify cost-saving opportunities. Bundling E&O with general liability or other business coverages may also result in package discounts.

What is the average cost of home inspection in California, and how does it relate to home inspector insurance rates?

The average cost of a home inspection in California typically ranges from $300 to $500, depending on various factors such as property size, location, age of the home, and the scope of the inspection.

Larger homes or properties with additional structures (like detached garages or pools) may incur higher fees, sometimes reaching $600 or more. Inspectors in high-cost areas like San Francisco or Los Angeles may charge more due to regional market demands.

This fee covers a comprehensive evaluation of the property’s major systems, including the foundation, roof, electrical, plumbing, and HVAC. While home inspection costs are largely driven by market competition and service scope, they are indirectly influenced by operational expenses that home inspectors face, including professional liability insurance.

Factors That Influence Home Inspection Pricing in California

- Property size and complexity: Larger homes with multiple stories or auxiliary structures require more time and expertise to evaluate, leading to higher inspection fees. A 1,500-square-foot home may cost closer to $350, while a 3,000-square-foot residence might exceed $500.

- Geographic location: Urban centers such as San Diego, Sacramento, and the Bay Area often command higher inspection rates due to elevated cost of living and higher demand for real estate services. Rural areas may see slightly reduced pricing.

- Age and condition of the home: Older homes, particularly those built before 1970, may require more detailed assessments due to outdated electrical systems, plumbing materials (like galvanized steel or lead), or potential issues with the foundation, increasing the inspector’s time commitment and risk exposure.

Role of Home Inspector Insurance in Operational Costs

- Home inspectors are required to carry Errors and Omissions (E&O) insurance, also known as professional liability insurance, which protects them if a client sues over a missed defect during the inspection. Premiums for E&O insurance vary based on the inspector’s experience, claim history, and coverage limits, with annual costs ranging from $800 to $2,500 or more.

- This insurance expense is a significant component of an inspector’s overhead. To offset these costs, inspectors may adjust their service fees. Inspectors operating in high-risk regions or offering expanded services (e.g., termite, sewer, or mold inspections) often carry higher premiums, which can be reflected in their pricing structure.

- Insurance providers assess risk based on factors such as inspection volume, reporting accuracy, and adherence to industry standards (e.g., compliance with the California Real Estate Inspection Association guidelines). A clean claims history can result in lower premiums over time, allowing some inspectors to remain competitively priced.

Connection Between Inspection Quality and Insurance Risk Management

- Higher-quality inspections that follow standardized checklists and include detailed reporting reduce the likelihood of oversights, thereby minimizing liability exposure. As a result, insurance underwriters may view thorough inspectors as lower risk, potentially offering more favorable rates.

- Inspectors who invest in additional certifications—such as those from the American Society of Home Inspectors (ASHI) or the International Association of Certified Home Inspectors (InterNACHI)—demonstrate a commitment to professionalism, which can enhance their credibility and lead to reduced insurance premiums.

- Because insurance rates correlate with risk, inspectors in California may prioritize comprehensive training, up-to-date equipment (like thermal imaging cameras and moisture meters), and clear client disclosures to limit legal exposure. These practices, while increasing service reliability, are partially funded through inspection fees, linking service pricing directly to risk-mitigation strategies.

Frequently Asked Questions

What is the average cost of home inspector insurance?

The average cost of home inspector insurance typically ranges from $500 to $1,200 annually. This price varies based on location, experience, coverage limits, and claims history. A standard policy includes general liability and errors and omissions (E&O) coverage, both essential for protecting against common risks. New inspectors may pay more initially until they establish a clean claims record. Shopping around and bundling policies can help reduce overall costs.

What factors influence the price of home inspector insurance?

Several factors affect home inspector insurance costs, including geographic location, years of experience, types of inspections performed, and coverage limits. Inspectors in high-risk areas may face higher premiums. Additional influences include claims history, business size, and whether they provide environmental testing. Choosing higher deductibles or bundling coverage can lower premiums. Insurers also consider client volume and inspection volume when calculating risk and pricing policies accordingly.

Does home inspector insurance cover legal fees?

Yes, most home inspector insurance policies, particularly errors and omissions (E&O) coverage, include protection for legal fees. If a client sues over alleged negligence or missed defects, the policy typically covers attorney costs, court fees, and potential settlements up to the policy limit. General liability insurance may also cover legal expenses related to bodily injury or property damage claims. This protection is crucial for avoiding out-of-pocket legal expenses during disputes.

Can I get home inspector insurance as an independent contractor?

Yes, independent home inspectors can obtain insurance tailored to their needs. Most providers offer policies specifically for self-employed inspectors, including both general liability and professional liability (E&O) coverage. These policies protect against claims of negligence, oversights, or injuries during inspections. Proof of licensure and inspection volume may be required. Independent contractors often benefit from customizable plans that scale with their business growth and risk exposure.

Leave a Reply