Average home insurance cost calculator

Understanding the average home insurance cost can help homeowners make informed financial decisions. With so many variables affecting premiums—such as location, home value, coverage limits, and credit history—calculating an accurate estimate can be challenging.

An average home insurance cost calculator simplifies this process by analyzing key factors and providing personalized projections. These tools allow users to compare quotes, adjust coverage options, and identify potential savings.

Whether you're a first-time homeowner or looking to switch providers, using a calculator offers transparency and control over your insurance expenses, making it an essential step in protecting your property and budget effectively.

Can A 20 Year Term Life Insurance Policy Be Extended

Can A 20 Year Term Life Insurance Policy Be ExtendedAn average home insurance cost calculator is a powerful online tool that helps homeowners estimate how much they may pay for their homeowners insurance based on a range of property-specific and location-based factors.

These calculators typically require users to input key details such as the home’s value, square footage, construction type, geographic location, and coverage preferences. By analyzing this data, the calculator uses actuarial models and regional claims history to produce a realistic estimate of annual or monthly premiums.

Insurance providers and third-party comparison websites offer these tools to help consumers understand cost variables before committing to a policy. Using such a calculator allows individuals to compare quotes from multiple insurers, identify potential cost-saving opportunities, and make an informed decision that aligns with their financial needs and protection requirements.

Key Inputs Required in a Home Insurance Cost Calculator

To generate an accurate estimate, an average home insurance cost calculator requires several crucial inputs from the user.

Cash In On Life Insurance

Cash In On Life InsuranceThese include the home’s replacement cost, which is different from market value and reflects how much it would cost to rebuild the home from scratch; the deductible amount chosen (e.g., $500, $1,000); and the desired coverage limits for dwelling, personal property, liability, and additional living expenses. Location factors such as the ZIP code, proximity to fire stations, and exposure to natural disasters like hurricanes or wildfires are also considered.

Personal factors like credit score (in most states), claims history, and whether the home has safety features—such as security systems or storm shutters—also influence the calculated cost. Providing precise information ensures the estimate is as close as possible to actual quotes.

How Accurate Are Online Home Insurance Calculators?

The accuracy of an average home insurance cost calculator depends on the quality and specificity of the data entered and the sophistication of the algorithm used by the platform.

While these tools provide a useful starting point, they may not account for every underwriting nuance a carrier applies during a full application process. For instance, some insurers might offer discounts for bundling home and auto policies or for being claims-free, which basic calculators might not factor in completely. Additionally, regulatory differences between states can affect pricing models.

Guardian Life Insurance

Guardian Life InsuranceTherefore, while calculators can give a close approximation, especially when sourced from reputable insurers or financial websites, final premiums may vary. Users should treat these estimates as informed benchmarks rather than definitive pricing.

Top Features to Look for in a Reliable Insurance Cost Calculator

When selecting an average home insurance cost calculator, it’s essential to choose one with transparent inputs, clear explanations of terms, and the ability to customize coverage levels.

A reliable calculator should allow side-by-side comparison of multiple providers, show breakdowns of costs (like base premium, discounts, and surcharges), and support adjustments based on risk factors such as local crime rates or flood zones. Some advanced tools integrate real-time data from insurance carriers for more precise estimates and include interactive elements such as sliders or dropdown menus for ease of use.

Additionally, calculators that provide personalized tips to lower premiums—such as raising deductibles or installing smart home devices—add significant value. Ensuring the tool is hosted by a licensed insurer or a well-known financial platform increases credibility.

| Input Factor | Impact on Premium | Example Values |

|---|---|---|

| Home Replacement Cost | High – Larger homes cost more to insure | $250,000 – $750,000+ |

| Location (ZIP Code) | High – Affects exposure to natural disasters | Coastal vs. inland areas |

| Credit Score | Medium – Better scores often lead to lower rates | Excellent (750+) to Poor (below 600) |

| Deductible Amount | Medium – Higher deductibles reduce premiums | $500, $1,000, $2,500 |

| Home Safety Features | Low to Medium – Can qualify for discounts | Smart alarms, fire sprinklers, deadbolts |

How to Calculate the Average Home Insurance Cost: A Comprehensive Guide

What is the average home insurance cost for a $500,000 house?

The average home insurance cost for a $500,000 house typically ranges between $2,500 and $4,500 annually in the United States.

However, this amount can vary significantly based on location, home features, claims history, coverage levels, and insurance provider. Homes in areas prone to natural disasters like hurricanes, wildfires, or tornadoes often incur higher premiums.

Additionally, insurers calculate coverage based on the cost to rebuild the home rather than its market value, so construction costs in your region play a major role. Personal factors such as credit score, policy deductibles, and available discounts also influence the final price.

Factors That Influence Insurance Costs for a $500,000 Home

- Location plays a critical role—properties in high-risk zones for floods, earthquakes, or severe storms usually have higher premiums due to increased likelihood of claims. Urban areas may also experience higher rates due to increased crime or fire density.

- Construction type and age of the home impact pricing; newer homes with modern safety systems (like fire alarms and security cameras) may qualify for lower rates, while older homes might require costly upgrades that increase insurance costs.

- Personal risk factors such as the homeowner’s credit history, claims history, and even insurance score affect the premium. Insurers often view applicants with poor credit or frequent past claims as higher risks, leading to increased costs.

Types of Coverage Needed for a $500,000 Property

- Dwelling coverage is essential—it pays to rebuild or repair the home’s structure after a covered loss, and for a $500,000 house, this coverage typically needs to match the full reconstruction value, which may exceed the market price.

- Personal property coverage protects belongings inside the home, such as furniture and electronics. Coverage is usually set at 50% to 75% of the dwelling amount unless specified otherwise, so for a $500,000 home, this could range from $250,000 to $375,000.

- Additional living expenses (ALE) coverage helps pay for temporary housing and living costs if the home becomes uninhabitable due to a covered event. This is especially valuable for high-value homes where everyday expenses are higher.

How to Reduce Insurance Costs on High-Value Homes

- Bundling home and auto insurance with the same provider can offer substantial discounts, sometimes reducing premiums by 10% to 25%, and many insurers offer loyalty programs for long-term customers.

- Installing safety and security upgrades such as monitored alarm systems, reinforced roofing, or storm shutters may qualify the homeowner for discounts, especially in disaster-prone regions.

- Raising the deductible can lower the monthly premium significantly, though it means the homeowner would pay more out-of-pocket in the event of a claim, so this strategy requires careful financial planning.

What is the average home insurance cost for a $100,000 house?

The average home insurance cost for a $100,000 house typically ranges between $300 and $800 per year, depending on several key factors. While the home's value is one component, insurance premiums are not directly proportional to the dwelling's market value.

Instead, insurers calculate coverage based on the cost to rebuild the home, which includes materials, labor, and local construction regulations. A house valued at $100,000 may have a much higher rebuild cost, especially in areas with elevated construction expenses.

Additionally, location plays a critical role—homes in regions prone to natural disasters such as hurricanes, wildfires, or severe storms often face higher premiums. Other determining factors include the home’s age, construction materials, proximity to fire services, and the policyholder’s claims history and credit score.

Factors That Influence Home Insurance Costs for a $100,000 House

- Location is one of the most significant factors; homes in areas with high crime rates or increased risk of natural disasters like floods or earthquakes generally incur higher premiums due to the elevated risk of claims.

- The age and condition of the home also impact the rate; older homes may have outdated electrical systems or plumbing, which increase the risk of fire or water damage, leading to higher insurance costs.

- Insurance companies also consider local fire protection services; homes located near fire stations or hydrants typically receive lower rates because of the reduced risk of extensive fire damage.

How Rebuild Cost Differs from Market Value in Insurance Calculations

- Insurance providers base dwelling coverage on the cost to rebuild the home from the ground up, not its market value, which means a $100,000 house could cost significantly more to reconstruct depending on regional labor and material prices.

- For example, two identical homes in different states might have the same market value but vastly different rebuild costs due to varying construction regulations, labor expenses, and material availability.

- This rebuild cost influences the dwelling coverage portion of the policy, which is usually the largest component of a home insurance premium, explaining why insuring a lower-valued home can still result in moderate to high annual costs.

- Increasing your deductible can reduce your annual premium, as you agree to pay more out of pocket in the event of a claim, which lowers the insurer’s financial risk.

- Installing safety and security features such as smoke detectors, burglar alarms, deadbolt locks, or storm shutters may qualify you for discounts from most insurance providers.

- Shopping around and comparing quotes from multiple insurers ensures you find the most competitive rate, as pricing models and risk assessments vary significantly between companies, even for similarly valued homes.

What is the average monthly cost of homeowners insurance based on a home insurance calculator?

The average monthly cost of homeowners insurance in the United States typically ranges from $100 to $150, based on data derived from various home insurance calculators and industry reports.

This translates to an annual cost of approximately $1,200 to $1,800. However, the exact amount can vary significantly depending on several factors such as the home’s location, size, age, construction type, chosen coverage limits, deductible amount, and the homeowner’s claims history.

Online home insurance calculators use these variables to estimate personalized quotes, helping users understand potential costs before obtaining formal policies from insurers. It's important to note that regions with higher risks of natural disasters—like hurricanes, wildfires, or tornadoes—often face substantially higher premiums.

Factors That Influence Homeowners Insurance Monthly Rates

- Location plays a major role in determining insurance costs. Homes in areas prone to natural disasters such as floods, earthquakes, or wildfires generally incur higher premiums because of the increased risk of claims. Urban versus rural settings also impact pricing due to differences in crime rates and emergency service response times.

- The age and condition of the home are critical. Older homes may require more maintenance and have outdated electrical or plumbing systems, increasing the likelihood of incidents like fires or water damage. Insurers may charge more for older properties unless they’ve been fully renovated with modern safety features.

- Coverage level and deductible choices directly affect monthly payments. A policy with higher coverage limits to protect valuable belongings or provide extended liability protection will naturally cost more. Conversely, selecting a higher deductible can lower the premium but increases out-of-pocket expenses during a claim.

- Home insurance calculators collect key information from users, including the home’s square footage, construction materials, proximity to fire stations and hydrants, and the roof type and age. These details help assess the structural risk and rebuilding cost, which are fundamental to determining the premium.

- The calculators also consider the desired coverage types—such as dwelling protection, personal property, liability, and additional living expenses—and adjust the estimate accordingly. Users can modify these options to see how changes in coverage affect the total cost.

- Historical data from insurers and regional risk assessments are built into these tools to provide realistic estimates. While these calculators don’t replace official quotes, they offer a reliable starting point for comparing average costs across different providers and locations.

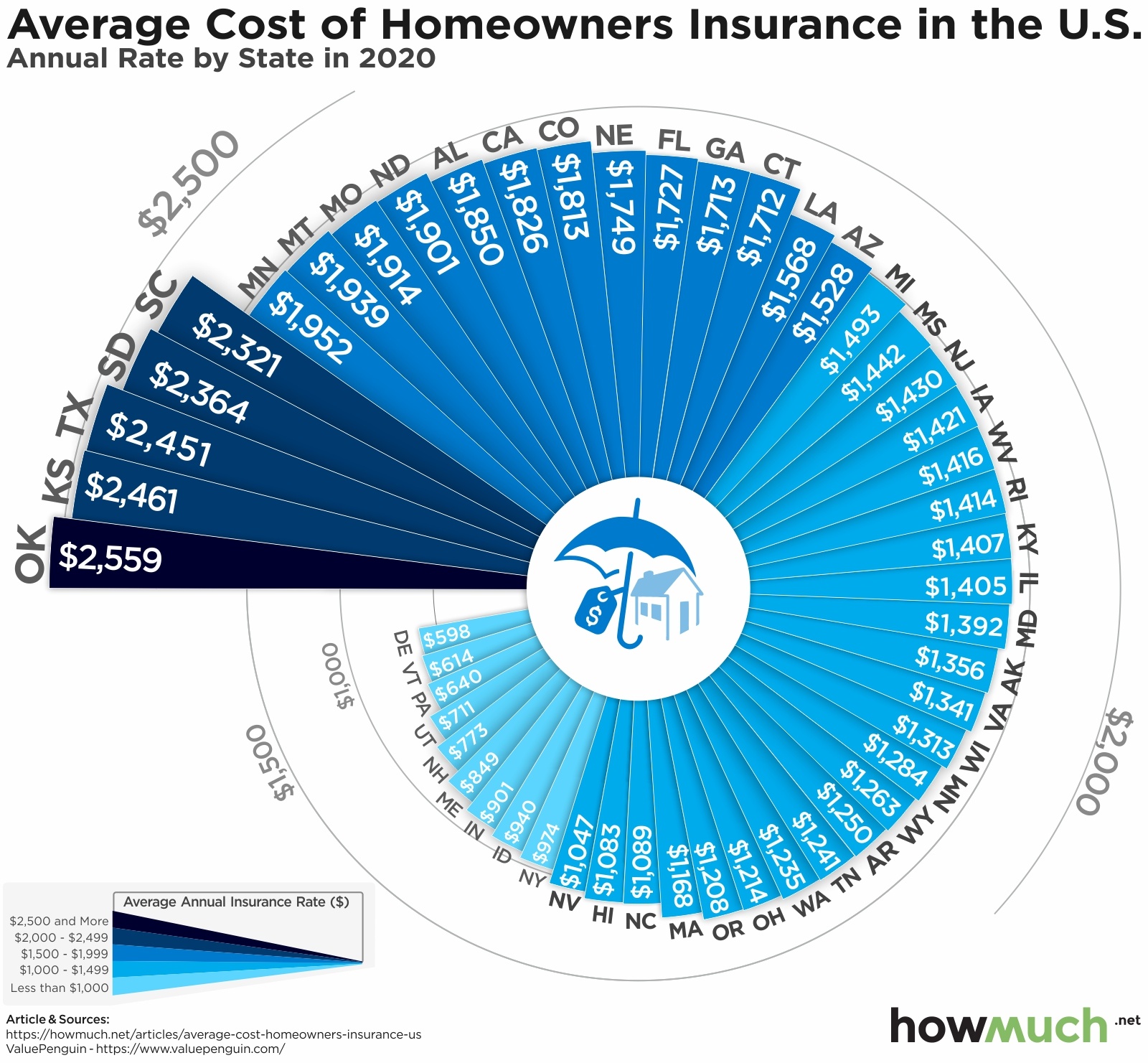

Regional Variations in Homeowners Insurance Costs

- States like Texas, Florida, and Louisiana often report some of the highest homeowners insurance premiums due to frequent hurricanes, flooding, and high reinsurance costs. In contrast, states such as Hawaii, Vermont, and Utah generally have lower average premiums because of fewer natural disaster risks and stable housing markets.

- Within states, even neighboring cities can have vastly different insurance costs. For example, a coastal property in Florida may pay double or triple the amount for the same coverage as a home located inland, reflecting the disparity in storm exposure.

- Local regulations and building codes also contribute to cost differences. Areas with strict construction standards may reduce risk and lead to lower premiums, while regions with less oversight could see higher rates due to increased chances of property damage.

Frequently Asked Questions

What is an average home insurance cost calculator?

An average home insurance cost calculator is an online tool that estimates how much homeowners insurance might cost based on factors like location, home value, coverage needs, and personal information. It helps users compare potential premiums from different insurers and make informed decisions. These calculators use real-time data to provide accurate, personalized estimates, simplifying the process of budgeting for home protection.

How accurate is an average home insurance cost calculator?

An average home insurance cost calculator provides a close estimate based on the information you input, such as home size, location, and desired coverage. While it's not a final quote, it's highly accurate for preliminary planning. Results may vary slightly between insurers due to differing underwriting rules. For the most precise pricing, follow up with official quotes from providers after using the calculator.

What factors affect the results in a home insurance cost calculator?

Key factors include your home's location, age, size, construction type, and local crime or disaster risks. Personal factors like credit score, claims history, and coverage limits also impact results. Additional endorsements or higher deductibles can lower or raise the estimated premium. Ensuring accurate input improves the calculator’s ability to deliver a reliable cost estimate tailored to your specific situation and insurance needs.

Can I use the calculator for different types of homes?

Yes, most home insurance cost calculators support various property types, including single-family homes, condos, townhouses, and rental properties. You'll typically select your home type during the process to ensure accurate estimates. Each property type has unique risk factors and coverage needs, so the calculator adjusts accordingly. Always verify details with insurers to confirm coverage options match your home’s specific requirements.

Leave a Reply