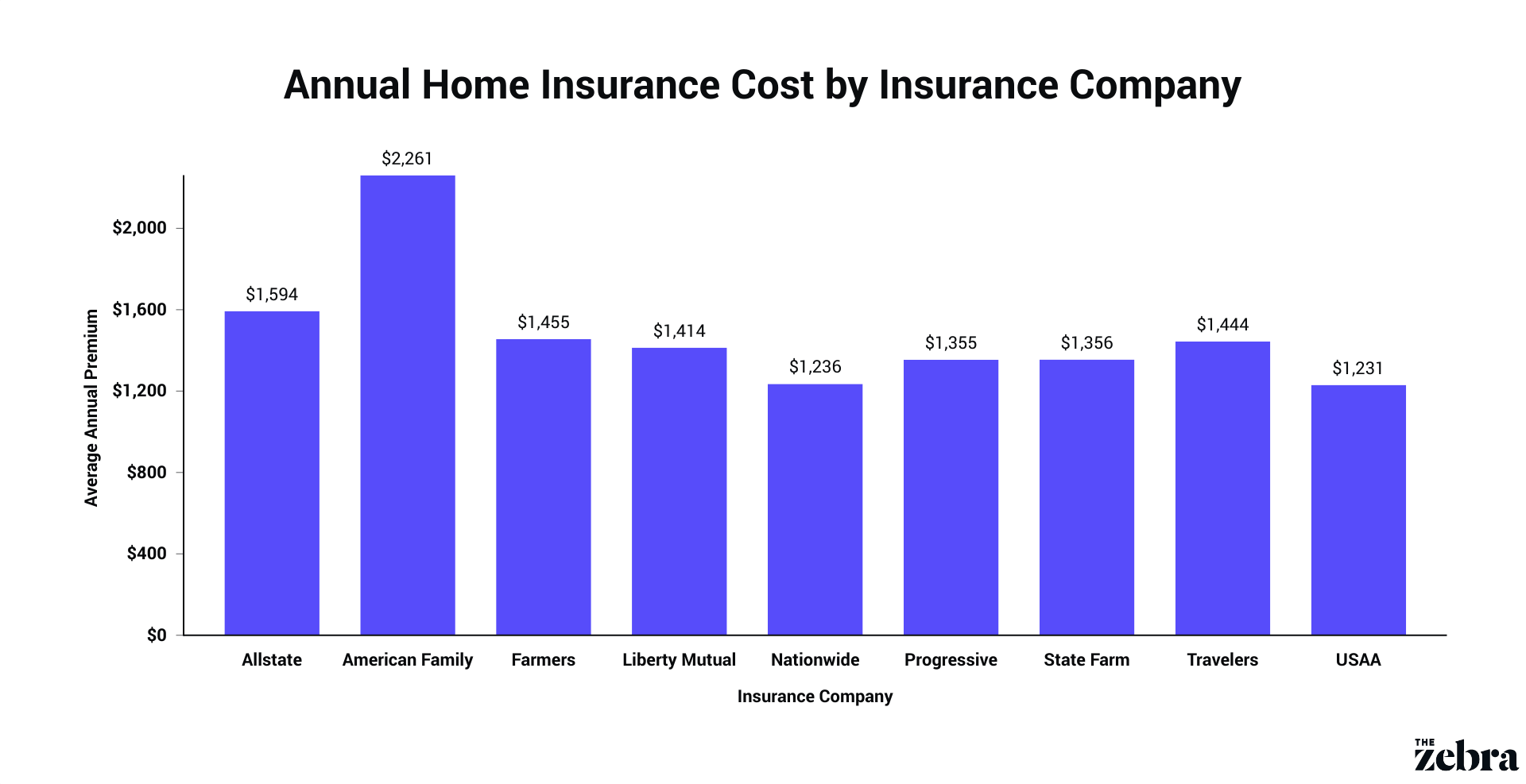

Average cost of home owners insurance

The average cost of homeowners insurance in the United States varies significantly depending on location, property value, and coverage needs.

As of 2023, the national average ranges from $1,200 to $1,800 annually, though premiums can be much higher in high-risk areas prone to natural disasters. Factors such as home size, construction type, credit score, and deductible levels all influence final rates.

Insurance is often required by lenders and provides essential protection against damage, liability, and loss. Understanding regional differences and available discounts can help homeowners secure adequate coverage at a competitive price.

Home insurance north charleston sc

Home insurance north charleston scAverage Cost of Homeowners Insurance: What You Need to Know

The average cost of homeowners insurance in the United States is approximately $1,800 per year, though this figure can vary significantly based on location, home value, coverage limits, and other risk factors.

Insurance premiums are calculated to cover potential damages from perils such as fire, windstorms, theft, and liability claims. Regions prone to natural disasters—like hurricanes in Florida or wildfires in California—typically face higher premiums due to increased risk exposure.

Additionally, the age and condition of the home, credit score, and claims history can all influence the final price. Understanding the components that affect these costs enables homeowners to shop wisely, compare quotes, and potentially reduce their premiums through discounts or home improvements.

Factors That Influence Homeowners Insurance Rates

Several key variables directly impact the cost of homeowners insurance. Location is one of the most significant: homes in areas with high crime rates or susceptibility to natural disasters usually have higher premiums.

Home insurance quote indiana

Home insurance quote indianaThe dwelling’s characteristics—such as square footage, construction materials, roof type, and age—also play a role. Insurers also evaluate the level of coverage selected, including dwelling coverage, personal property protection, liability limits, and additional endorsements like flood or earthquake insurance.

A homeowner’s credit-based insurance score and claims history can further alter pricing, with a strong credit profile and minimal past claims often leading to lower costs. By understanding these factors, consumers can take proactive steps to manage and potentially reduce their insurance expenses.

Regional Differences in Home Insurance Costs

Homeowners insurance costs vary widely across the U.S. due to regional risks and housing markets. For instance, Texas and Florida rank among the most expensive states because of their exposure to hurricanes, hail, and tornadoes, leading to average annual premiums exceeding $2,500.

In contrast, states like Maine and Utah often report some of the lowest average premiums—around $1,000 to $1,300 per year—thanks to lower risks of severe weather and stable housing markets.

Home insurance quote oklahoma city

Home insurance quote oklahoma cityUrban versus rural settings also matter; densely populated areas may see higher costs due to increased theft and vandalism rates. Buyers and current homeowners should research local trends and consult insurers familiar with regional risk profiles to ensure accurate and competitive pricing.

Typical Coverage Components and Associated Costs

A standard homeowners insurance policy includes multiple coverage types, each affecting the overall premium cost. Dwelling coverage, which protects the physical structure of the home, usually represents the largest portion of the premium.

Other structures coverage applies to detached buildings like garages or sheds, typically set at 10% of dwelling coverage. Personal property coverage safeguards belongings inside the home, often at 50% of dwelling limits, while loss of use coverage pays for temporary housing if the home becomes uninhabitable.

Personal liability and medical payments to others protect against legal and medical costs arising from injuries on the property, commonly offering $100,000 to $500,000 in coverage. Below is a table summarizing average coverage limits and their impact on annual premiums.

Home insurance quotes gulfport ms

Home insurance quotes gulfport ms| Coverage Type | Typical Limit | Estimated Cost Impact |

|---|---|---|

| Dwelling Coverage | $300,000 | Most significant cost driver—70-80% of premium |

| Other Structures | 10% of dwelling | Small additional cost—around 5-10% of premium |

| Personal Property | 50% of dwelling | Moderate impact—10-15% of premium |

| Loss of Use | 20% of dwelling | Minor cost—usually 5% or less |

| Personal Liability | $300,000 | Low cost per $100k—higher limits available at small increase |

Average Cost of Homeowners Insurance: A Comprehensive Guide

What is the average homeowners insurance cost for a $500,000 home?

The average homeowners insurance cost for a $500,000 home in the United States typically ranges from $2,500 to $4,500 per year. However, this amount can vary significantly based on location, construction type, claims history, and the level of coverage selected. Homes in areas prone to natural disasters such as hurricanes, wildfires, or earthquakes may see premiums on the higher end of the spectrum.

Additionally, insurance providers consider replacement cost—not the market value—when calculating premiums, meaning the expense to rebuild the home using current materials and labor costs. For a $500,000 home, especially one with high-end finishes or located in a high-risk zone, insurance costs could exceed $5,000 annually.

Factors Influencing Homeowners Insurance Costs for a $500,000 Home

- Location plays a critical role in determining insurance premiums. Homes in regions with high crime rates or frequent severe weather—like Florida (hurricanes) or California (wildfires)—face higher rates due to increased risk exposure. Insurers assess local hazards and adjust premiums accordingly.

- The age and condition of the home significantly impact cost. Older homes may have outdated electrical systems or plumbing, increasing the likelihood of claims. In contrast, newer homes built with modern safety features like fire sprinklers or reinforced roofs may qualify for discounts.

- Replacement cost estimation is not the same as market value. For a $500,000 home, the cost to rebuild might be higher or lower depending on local construction costs, materials used, and square footage. Insurers calculate premiums based on this projected rebuilding expense.

- Dwelling coverage is the core component and protects the physical structure of the home. For a $500,000 home, this coverage typically mirrors the estimated rebuild cost. Coverage extensions, such as protection for high-value items like custom cabinetry or smart home systems, can increase the premium.

- Personal property coverage safeguards belongings inside the home, such as furniture, electronics, and clothing. This is usually set at 50% to 75% of the dwelling coverage. A home with more valuable contents will require higher limits, raising the overall premium.

- Liability protection and additional living expenses (ALE) also influence cost. Liability coverage, usually starting at $100,000 but often recommended at $300,000 or more for a higher-value home, protects against lawsuits. ALE covers living costs if the home becomes uninhabitable, and higher limits mean higher premiums.

Ways to Reduce Homeowners Insurance Costs on a $500,000 Home

- Installing safety and security features such as monitored alarm systems, smoke detectors, or reinforced roofing can significantly reduce premiums. Many insurers offer discounts of 5% to 20% for homes equipped with these features, especially in areas at risk for theft or fire.

- Shopping around and comparing quotes from multiple insurers is crucial. Providers use different models and risk assessments, so premiums for the same property can vary by hundreds or even thousands of dollars annually. Bundling home and auto insurance with the same company often leads to additional savings.

- Reviewing policy limits and deductibles regularly can help optimize costs. Raising the deductible—say from $1,000 to $2,500—can lower the annual premium, though it means paying more out-of-pocket in the event of a claim. Ensuring coverage aligns with actual rebuild costs, not over-insuring, avoids unnecessary expenses.

What is the 80/20 rule in home insurance and how does it impact average homeowners insurance costs?

The 80/20 rule in home insurance, also known as the 80% rule or coinsurance clause, is a principle that requires homeowners to insure their property for at least 80% of its replacement cost to receive full compensation for a partial loss.

If the homeowner insures the property for less than this threshold, the insurance company may reduce the payout proportionally, meaning the homeowner could end up paying a significant portion of repair or rebuilding costs out of pocket.

This rule is designed to encourage policyholders to maintain adequate coverage and prevent underinsurance, especially in cases where rebuilding costs after a disaster exceed initial expectations. For the average homeowner, understanding this rule is critical to avoid unexpected financial gaps when filing a claim.

How the 80/20 Rule Works in Practice

- Insurance companies apply the 80/20 rule by comparing the actual amount of coverage purchased to the required minimum—80% of the home’s replacement value. For example, if a home’s replacement cost is $300,000, the homeowner should carry at least $240,000 in dwelling coverage to meet the 80% threshold.

- If the homeowner only has $200,000 in coverage, they are underinsured. In the event of a covered loss, say $50,000 in roof damage, the insurer may not pay the full amount. Instead, the payout is reduced based on the percentage of coverage the homeowner has relative to the 80% benchmark.

- The formula used by insurers involves dividing the actual coverage by the required coverage (e.g., $200,000 / $240,000 = 83.3%) and then multiplying that percentage by the claim amount. This means the homeowner might only receive about $41,650 of the $50,000 claim, leaving them responsible for the remainder plus any deductible.

Impact of the 80/20 Rule on Homeowners Insurance Costs

- The 80/20 rule encourages homeowners to purchase higher coverage limits, which can increase their premiums. However, this increase is often modest compared to the potential out-of-pocket expenses from a partial claim denial or reduction.

- Homeowners who underestimate their home’s replacement cost—often confusing it with market value—may unintentionally violate the 80% rule. Market value includes land, location, and real estate trends, whereas replacement cost is based on construction materials, labor, and design. This misunderstanding can lead to underinsurance and higher financial risk.

- In regions prone to natural disasters, construction costs can fluctuate significantly, increasing the replacement value of homes. If a homeowner does not update their policy accordingly, they may fall below the 80% threshold, increasing their share of loss expenses despite having insurance.

Strategies to Comply with the 80/20 Rule and Avoid Claim Penalties

- Homeowners should regularly review their policy declarations page and consult with their insurer or agent to confirm their dwelling coverage reflects current replacement costs. Some insurance providers offer replacement cost estimators or require professional appraisals for older or unique homes.

- Adding an extended or guaranteed replacement cost endorsement can help bypass the 80/20 rule. These upgrades ensure the insurer pays to rebuild the home even if costs exceed the policy limit, offering greater financial protection.

- Keeping documentation of upgrades, renovations, and major home improvements allows homeowners to accurately adjust coverage as needed. Failing to account for improvements like a new kitchen or additional square footage may leave the home underinsured relative to its updated replacement value.

What is the average cost of homeowners insurance in the United States?

The average cost of homeowners insurance in the United States is approximately $1,784 per year, or about $149 per month, according to data from the National Association of Insurance Commissioners (NAIC) and other insurance industry reports.

However, this figure can vary significantly based on location, the size and age of the home, coverage limits, deductible amounts, and the homeowner’s claims history. States prone to natural disasters such as hurricanes, wildfires, or tornadoes typically have higher premiums due to increased risk.

Urban areas may also have different rates compared to rural ones, and homes with upgraded security systems or recent renovations might qualify for lower rates. It's important to note that this average reflects a standard policy covering dwelling, personal property, liability, and additional living expenses.

- Location plays a crucial role in determining insurance costs. Homes in areas with high crime rates or those vulnerable to natural disasters like floods, earthquakes, or hurricanes usually face higher premiums. Insurers assess regional risk levels when setting rates, which means two identical homes in different states could have vastly different insurance costs.

- The age and condition of the home are also significant. Older homes may have outdated electrical wiring, plumbing, or roofing, which increases the likelihood of claims and can drive up premiums. Conversely, newer homes built with modern safety features and updated materials often cost less to insure.

- Coverage amount and deductible choices directly affect the price of a policy. Opting for higher coverage limits increases premiums, while selecting a higher deductible can lower the monthly cost. Insurers also consider the construction type, square footage, and rebuild cost when calculating the premium.

State-by-State Variations in Home Insurance Costs

- Texas has one of the highest average annual premiums, often exceeding $2,500, due to exposure to hurricanes, hailstorms, and high wind damage. Coastal properties are particularly expensive to insure, and many homeowners require windstorm insurance through state-backed plans.

- California also faces elevated rates, averaging over $1,500 per year, primarily because of wildfire risks. Insurers in fire-prone regions may impose stricter underwriting rules or offer limited coverage, which can increase costs for consumers.

- In contrast, states like Maine, Iowa, and Vermont tend to have lower average premiums—often under $1,200 annually—due to relatively stable weather patterns, fewer natural disasters, and lower rates of burglary and vandalism. These regions are considered lower risk by insurance providers.

How to Reduce Your Homeowners Insurance Costs

- Shopping around and comparing quotes from multiple insurers can lead to substantial savings. Each company uses different models and risk assessments, so premiums for the same coverage can vary widely. Using online comparison tools or working with an independent agent may help identify more affordable options.

- Taking advantage of available discounts can reduce your premium. Many insurers offer reductions for bundling home and auto insurance, installing security systems, having a claims-free record, or maintaining a good credit score. Some also provide loyalty discounts for long-term customers.

- Raising your deductible is another way to lower your monthly or annual payment. While this means you’ll pay more out-of-pocket in the event of a claim, it reduces the insurer’s risk and, in turn, your premium. However, homeowners should ensure they have enough savings to cover the higher deductible if needed.

Frequently Asked Questions

What is the average cost of homeowners insurance in the United States?

The average cost of homeowners insurance in the U.S. is about $1,700 per year, though this can vary significantly by state. Factors such as location, home value, coverage limits, and local crime or disaster risks influence the price. States prone to extreme weather, like Florida or Texas, often have higher premiums. It’s important to compare quotes from multiple insurers to find a policy that fits your budget and coverage needs.

Why does the cost of homeowners insurance vary by state?

Homeowners insurance costs vary by state due to differences in climate, natural disaster frequency, construction costs, and local regulations. Areas with higher risks of hurricanes, wildfires, or tornadoes typically have higher premiums. Additionally, states with costly building materials or strict labor laws can increase repair expenses. Insurers assess these regional risks when calculating rates, making coverage more expensive in certain locations than others across the country.

How can I reduce the cost of my homeowners insurance?

You can reduce homeowners insurance costs by increasing your deductible, bundling policies with the same insurer, and installing safety features like security systems or smoke detectors. Maintaining a good credit score also helps, as many insurers use credit-based insurance scores. Additionally, shopping around annually and asking about available discounts can lead to significant savings without compromising essential coverage for your home and belongings.

Does the age and condition of my home affect insurance costs?

Yes, the age and condition of your home can significantly impact insurance costs. Older homes may have outdated electrical, plumbing, or roofing systems, increasing the risk of claims and leading to higher premiums. Homes with modern upgrades or built with durable materials often qualify for lower rates. Insurers may also charge more for homes in poor condition due to the higher likelihood of repairs or replacements after damage occurs.

Leave a Reply