Best home insurance price

Choosing the best home insurance doesn’t have to mean paying the highest price. With so many providers offering varying levels of coverage, finding an affordable policy that still protects your property and belongings is more achievable than ever. Factors like location, home value, and coverage needs all influence pricing, but savvy homeowners can compare quotes, take advantage of discounts, and adjust deductibles to lower premiums.

Understanding what affects cost empowers you to make informed decisions. This guide explores how to identify the best home insurance price without sacrificing essential protection, ensuring peace of mind and long-term savings.

How to Find the Best Home Insurance Price Without Sacrificing Coverage

Securing the best home insurance price requires more than just choosing the cheapest policy—homeowners must balance affordability with comprehensive protection.

Home insurance quote indiana

Home insurance quote indianaThe ideal policy offers sufficient dwelling coverage, liability protection, and personal property reimbursement at a competitive rate. Insurance premiums vary widely based on location, home value, claims history, and coverage options, so it's essential to compare multiple quotes from reputable insurers.

Utilizing online comparison tools, bundling policies, raising deductibles (when feasible), and qualifying for discounts (such as for installing security systems or maintaining a claims-free record) can significantly reduce costs. Additionally, reviewing and updating coverage annually ensures that homeowners aren’t overpaying for outdated or excessive protection.

Factors That Influence Home Insurance Rates

Several key elements determine the home insurance premium you’ll pay, making it critical to understand how insurers calculate risk.

Your home’s location plays a major role—properties in areas prone to natural disasters like hurricanes, wildfires, or floods typically face higher premiums due to increased risk. The age and condition of the home, construction materials, and roof type also affect pricing, with newer, durable structures often qualifying for lower rates.

Home insurance quote oklahoma city

Home insurance quote oklahoma cityInsurers also evaluate your credit score, claims history, and even local crime rates. Safety features such as smoke detectors, burglar alarms, and fire sprinklers can reduce risk and lead to insurance discounts. Recognizing how these variables influence pricing empowers homeowners to take proactive steps in lowering their premiums.

Strategies to Lower Your Home Insurance Cost

Homeowners have several effective methods for reducing their home insurance expenses without compromising essential protection. One of the most impactful steps is bundling home and auto insurance with the same provider, which often leads to substantial multi-policy discounts of 15% to 25%.

Increasing your deductible can also lower premiums, as it shifts more financial responsibility to you in the event of a claim—though this approach is best for those with emergency savings. Maintaining a strong credit score is crucial, as most insurers use credit-based insurance scores to set rates.

Additionally, completing a home safety inspection or upgrading vulnerable systems (like plumbing or electrical) can qualify you for discounts. Finally, always ask insurers about available reductions, such as those for retired individuals or members of certain professional organizations.

Home insurance quotes gulfport ms

Home insurance quotes gulfport msTop Providers Offering Competitive Home Insurance Prices

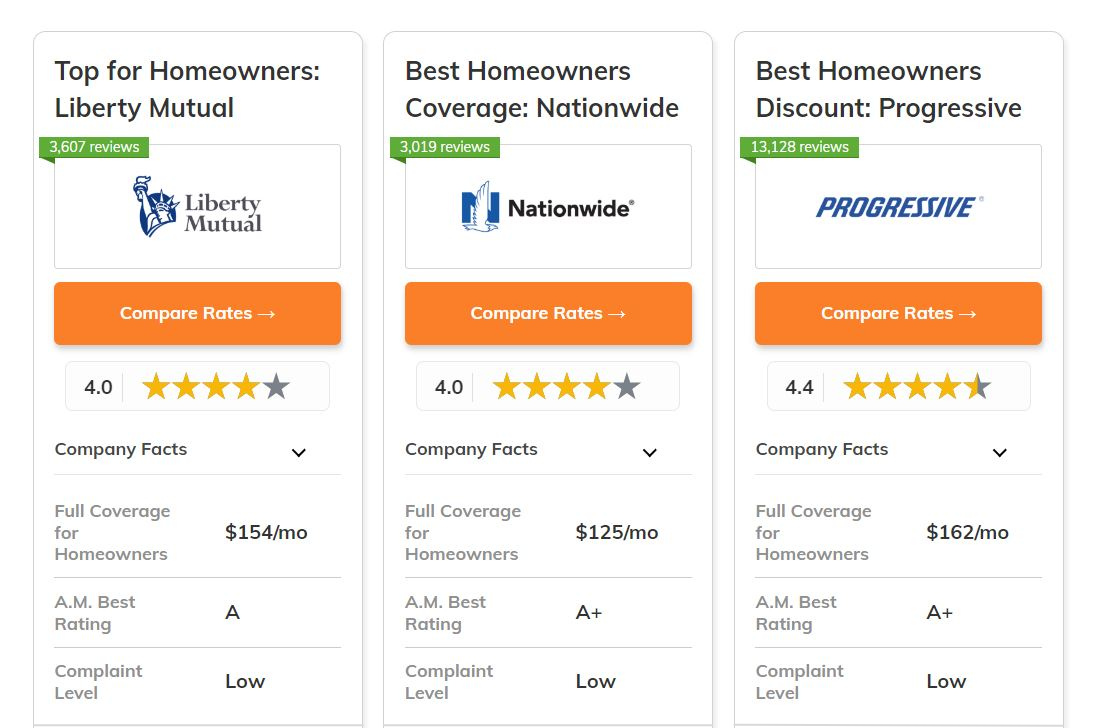

When searching for the best home insurance price, comparing offerings from top-rated insurers ensures you get both quality and value. Companies like State Farm, Allstate, Liberty Mutual, Nationwide, and Amica consistently rank high for affordability, customer service, and comprehensive coverage options.

Each insurer uses different pricing models and discount structures, so a low rate with one provider might not reflect availability across the board. For example, Amica is known for superior service and loyalty rewards, while State Farm frequently offers among the lowest average premiums, especially for bundled policies.

Online insurers like Plynt and Hippo also disrupt the market with data-driven pricing and modern home monitoring integrations. Reviewing independent ratings from sources like J.D. Power and AM Best can help identify insurers that balance cost with reliability.

| Insurance Provider | Average Annual Premium | Notable Discounts | Customer Satisfaction Rating (J.D. Power) |

|---|---|---|---|

| State Farm | $1,200 | Multi-policy, Claims-free, Loyalty | 854/1,000 |

| Amica | $1,450 | Dividend payouts, Safety devices, Bundling | 875/1,000 |

| Allstate | $1,600 | Protective devices, New home, Paperless billing | 820/1,000 |

| Liberty Mutual | $1,700 | Home monitoring discounts, Advance quote | 815/1,000 |

| Nationwide | $1,500 | Weatherproofing, Paperless, Bundling | 842/1,000 |

Best Home Insurance Rates: A Comprehensive Guide to Finding Affordable Coverage

What is the most competitive home insurance rate available?

How to check if a home insurance company is reliable

How to check if a home insurance company is reliableThe most competitive home insurance rate available varies significantly depending on a range of factors including your location, the value and age of your home, your credit score, coverage needs, and individual insurer pricing models.

There is no single lowest rate applicable to all homeowners, as insurers assess risk differently and offer customized quotes. To find the most competitive rate, it’s essential to shop around, compare multiple quotes, and consider both national and regional providers.

Bundling policies, increasing deductibles, and qualifying for discounts can also significantly reduce premiums. Because rates change frequently and are influenced by dynamic market conditions, the most competitive option today might not be the best choice six months from now.

Factors That Influence Home Insurance Rates

- Location plays a crucial role in determining home insurance costs. Homes in areas prone to natural disasters such as hurricanes, wildfires, or floods generally face higher premiums due to increased risk of claims.

- The age and condition of the home also affect pricing. Older homes may have outdated electrical or plumbing systems, leading insurers to charge more, whereas newer constructions with updated safety features can qualify for lower rates.

- Your personal claims history, credit score, and insurance score are used by most companies to assess the likelihood of future claims. Homeowners with strong credit and no claims history typically receive the most favorable pricing.

How to Compare Quotes Effectively

- Obtain at least three to five quotes from different insurers, including well-known national companies and reputable regional providers who may offer better rates in specific areas.

- Ensure that each quote includes the same coverage limits, deductibles, and additional protections such as personal property and liability coverage to make comparisons accurate and meaningful.

- Use independent comparison websites or work with a licensed insurance agent who can access multiple carriers and help identify discounts you might qualify for, such as multi-policy, home security, or claims-free discounts.

- Bundle your home and auto insurance policies with the same provider, which often results in a substantial discount—sometimes up to 25% off both policies.

- Consider increasing your deductible, the amount you pay out of pocket before insurance kicks in, to lower your monthly or annual premium, provided you have enough savings to cover the higher out-of-pocket cost if a claim arises.

- Invest in home improvements that reduce risk, such as installing a monitored security system, reinforcing your roof, or upgrading plumbing and electrical systems, which can lead to permanent premium reductions.

What is the most affordable home insurance with the best price-to-coverage ratio?

How to choose homeowners insurance for older home

How to choose homeowners insurance for older homeThe most affordable home insurance with the best price-to-coverage ratio varies depending on location, home value, and individual risk factors, but several insurers consistently receive high marks for offering competitive rates without compromising essential coverage. Companies like Amica Mutual, State Farm, and USAA often rank at the top for their balance of low premiums and comprehensive protection.

Amica, in particular, is frequently recognized for its strong customer service and broad policy inclusions, even though it may have slightly higher base rates than some competitors. However, for budget-conscious homeowners, insurers such as Nationwide and Allstate offer customizable plans that allow policyholders to adjust coverage limits and deductibles to fit their financial needs.

Bundling home and auto insurance can also lead to significant discounts, improving the overall value. The key is comparing personalized quotes and evaluating not just the monthly cost but also what perils are covered, limits on personal property and liability, and available add-ons.

Factors That Influence Home Insurance Affordability

- Geographic location plays a major role; homes in areas prone to natural disasters like hurricanes or wildfires typically face higher premiums due to increased risk.

- The age and condition of the home affect pricing—older homes with outdated electrical or plumbing systems may cost more to insure than newer, updated constructions.

- Insurance providers also consider credit score, claims history, and installed safety features such as security systems or storm shutters, all of which can lower premiums significantly.

Top Insurers Offering Competitive Price-to-Coverage Ratios

- Amica Mutual is well-regarded for offering robust standard coverage, including protection for personal belongings, liability, and additional living expenses, paired with excellent customer satisfaction ratings.

- State Farm provides widespread availability and flexible policy options, with strong discounts for multi-policy bundles, home safety upgrades, and long-term customers.

- USAA, available exclusively to military members and their families, consistently ranks high for low premiums and superior service, often offering some of the most favorable terms in the industry.

How to Maximize Value and Reduce Home Insurance Costs

- Shop around annually and request quotes from multiple insurers to ensure you are getting the best available rate for your specific needs and location.

- Increasing your deductible can lower your monthly premium, but it's important to ensure you have enough savings to cover the higher out-of-pocket cost if a claim arises.

- Take advantage of available discounts, such as those for installing smart home devices, maintaining a claims-free record, or insuring multiple properties with the same provider.

What is the most affordable home insurance provider based on price comparison?

Top Affordable Home Insurance Providers Based on Price Comparisons

According to recent price comparisons across major insurance review platforms and consumer studies, several home insurance providers consistently rank as the most affordable options.

State Farm, USAA, and Amica Mutual frequently appear at the top of affordability lists. State Farm benefits from a vast network of agents and competitive base premiums, making it a go-to for many budget-conscious homeowners. USAA, while only available to military members and their families, often offers some of the lowest rates in the market along with high customer satisfaction.

Amica Mutual, though slightly higher in price than the other two, delivers low average premiums combined with excellent service and consistent financial strength. Price is influenced by location, home value, coverage limits, and individual risk profiles, so affordability can vary.

- State Farm offers widely accessible low premiums and multiple discount opportunities, such as bundling with auto insurance and installing home security systems.

- USAA provides exceptional pricing for eligible military-affiliated customers, supported by strong financial ratings and digital service tools.

- Amica Mutual maintains a balance between affordability and service quality, frequently earning top marks in claims satisfaction and policyholder support.

Factors That Influence Home Insurance Affordability

The overall cost of home insurance depends on several variables that differ by provider and policyholder. Location plays a critical role—homes in areas prone to natural disasters such as hurricanes, wildfires, or floods will generally face higher premiums.

The age and condition of the property, construction materials, and local crime rates also affect pricing. Additionally, insurers evaluate a homeowner’s claims history, credit score (in most states), and the amount of coverage desired.

Providers like Nationwide and Erie Insurance offer regionally competitive rates by tailoring policies to local risk factors, contributing to their affordability in specific areas. It’s important for consumers to compare not only base rates but also how these factors are weighted by each insurer.

- Geographic location impacts risk exposure and local regulations, directly influencing base premium calculations across all providers.

- Home characteristics such as roof age, square footage, and safety features like smoke detectors or sprinkler systems can lead to lower rates.

- Personal factors, including credit-based insurance scores and prior claims history, are used by insurers to assess risk and set individual pricing.

How to Compare Home Insurance Prices Effectively

To accurately identify the most affordable home insurance provider, consumers should gather multiple quotes using consistent coverage levels and deductibles.

Relying on online comparison tools from reputable sources like NerdWallet, Bankrate, or The Zebra allows side-by-side evaluation of premiums, available discounts, and customer satisfaction ratings. It is essential to ensure each quote includes the same dwelling coverage amount, liability limits, and additional protections like personal property and loss of use.

Direct outreach to insurers or working with an independent agent can uncover promotions or regional discounts not always visible online. Regularly reviewing and comparing policies annually helps homeowners avoid overpaying as market conditions and personal circumstances change.

- Obtain at least three detailed quotes with identical coverage specifications to ensure accurate price comparisons across different insurers.

- Review available discounts such as multi-policy bundling, claims-free incentives, and safety device installations that can significantly reduce overall costs.

- Use independent comparison platforms or licensed agents to access broader market data and personalized recommendations based on individual homeowner profiles.

What is the most affordable home insurance provider in Louisiana?

The most affordable home insurance provider in Louisiana can vary depending on the region, property type, and individual risk factors, but based on average premiums and customer feedback, State Farm is frequently recognized as one of the most cost-effective options.

According to data from the National Association of Insurance Commissioners (NAIC) and third-party comparison platforms like NerdWallet and Bankrate, State Farm consistently ranks among the lowest in average annual premiums for homeowners insurance in Louisiana.

This affordability is supported by its broad coverage options, strong financial stability, and widespread network of local agents who help customize policies to fit homeowner needs. However, other providers such as Allstate, USAA (for eligible military members), and Progressive also offer competitive rates, especially for those bundling home and auto insurance.

Factors That Influence Home Insurance Costs in Louisiana

- Geographic location plays a major role; homes in coastal areas like New Orleans or Lake Charles face higher risks from hurricanes and flooding, which increases premiums across all insurers.

- Credit-based insurance scores are commonly used by Louisiana insurers to determine pricing, with better scores typically qualifying for lower rates.

- The age and construction type of a home also affect cost—older homes or those built with materials more vulnerable to storm damage usually come with higher premiums.

Top Low-Cost Home Insurance Providers in Louisiana

- State Farm offers some of the lowest average annual rates in the state, with strong customer service and numerous discounts, including multi-policy, claims-free, and home security incentives.

- Allstate provides competitive pricing, particularly for customers who bundle policies, and offers optional coverage enhancements like roof protection and deductible rewards.

- USAA, while exclusive to military members and their families, consistently delivers some of the most affordable and comprehensive coverage options, with excellent customer satisfaction ratings.

How to Find the Most Affordable Policy for Your Home

- Obtain multiple quotes from different insurers to compare not only price but also coverage limits, deductibles, and exclusions—tools like Insurify, Policygenius, and The Zebra make this easier.

- Ask about available discounts, such as those for installing storm shutters, having a monitored security system, or being a long-term customer.

- Consider raising your deductible to lower your premium, but ensure you have emergency savings to cover the higher out-of-pocket cost if you file a claim.

Frequently Asked Questions

What factors influence the best home insurance price?

The best home insurance price depends on several factors including your home’s location, age, and size, as well as your coverage needs and deductible amount. Credit history, claims history, and protective features like alarms or fire detectors also impact rates. Insurers evaluate the risk of damage from natural disasters and crime in your area. Comparing multiple quotes and adjusting coverage options can help secure a lower, more competitive price.

How can I find the cheapest home insurance without sacrificing coverage?

To find affordable home insurance without compromising protection, compare quotes from multiple reputable insurers online. Look for bundling discounts with auto insurance, increase your deductible if affordable, and ask about available discounts for security systems, loyalty, or claims-free history. Review policy details carefully to ensure adequate coverage limits and understand exclusions. Regularly reassess your policy and shop around every few years to maintain the best value.

Does my credit score affect my home insurance price?

Yes, in most states, insurers use your credit-based insurance score to help determine your premium. A higher score often leads to lower rates, as it suggests lower financial risk. However, the impact varies by state and provider. Improving your credit score through on-time payments and reduced debt can lead to better home insurance pricing. Some insurers may offer coverage without considering credit, especially in regulated states.

Is it worth switching home insurance providers for a lower price?

Switching providers can save money if you find a significantly lower rate with comparable or better coverage. Always compare policy details, not just price, to ensure similar protection levels. Be aware of potential cancellation fees and timing to avoid lapses in coverage. Many insurers allow mid-term switching with a pro-rated refund. Regularly reviewing and comparing options every renewal period helps maintain the best home insurance price.

Leave a Reply