Best home insurance companies 2025

Choosing the right home insurance company in 2025 means balancing comprehensive coverage, affordability, and reliable customer service.

With evolving risks—from natural disasters to cyber threats—homeowners need policies that adapt to modern challenges. The best home insurance providers this year stand out through innovative offerings, including smart home discounts, enhanced cybersecurity protection, and seamless claims processes powered by AI.

Companies are also prioritizing transparency, bundling options, and personalized plans tailored to individual property needs. This guide evaluates top insurers based on financial strength, customer satisfaction, digital tools, and value, helping you make an informed decision to protect your most valuable asset—your home.

Allstate Life Insurance Sale

Allstate Life Insurance SaleBest Home Insurance Companies 2025: Top Providers for Coverage, Value, and Service

As homeowners seek reliable protection against unforeseen events in 2025, choosing the right home insurance provider has become more critical than ever. The best home insurance companies this year distinguish themselves through a combination of competitive pricing, comprehensive coverage options, exceptional customer service, and innovative digital tools that streamline claims and policy management.

Leading insurers like State Farm, Allstate, and USAA consistently rank at the top due to their strong financial stability, high customer satisfaction ratings from sources like J.D. Power and AM Best, and flexible policies tailored to different homeowner needs—from basic dwelling protection to full replacement cost and identity theft coverage.

Additionally, emerging providers such as Lemonade and Hippo are gaining ground with AI-driven platforms and on-demand policies that appeal to tech-savvy consumers. When evaluating the best options, factors such as local availability, bundling discounts, claims efficiency, and additional living expenses coverage play a key role in determining overall value.

Top-Rated Home Insurance Providers in 2025

In 2025, several home insurance companies stand out due to their strong reputations, broad coverage offerings, and customer-centric services. State Farm remains the largest provider in the U.S., known for its extensive agent network and personalized customer support.

Athene Term Life Insurance Reviews

Athene Term Life Insurance ReviewsAllstate excels in offering customizable policies, including roof and system protection riders, ideal for older homes. USAA continues to dominate satisfaction scores, serving military members and their families with unmatched rates and service. Amica Mutual earns top marks for customer service and dividend payouts to policyholders.

Meanwhile, digital-first insurers like Lemonade leverage artificial intelligence for instant claims processing, appealing to modern homeowners who value speed and transparency. These companies consistently perform well in third-party evaluations, making them go-to choices for reliable, long-term home protection.

Key Features to Look for in 2025’s Best Home Insurance

When selecting home insurance in 2025, homeowners should prioritize insurers that offer comprehensive coverage, flexible policy options, and advanced digital tools.

Essential features include dwelling coverage that matches full replacement cost, personal property protection with off-premises theft coverage, liability insurance (typically $300,000 or more), and additional living expenses (ALE) in case of displacement. Top providers also offer valuable add-ons like flood or earthquake endorsements, identity theft protection, and smart home discounts.

Best Ways To Sell Life Insurance Policy For Cash

Best Ways To Sell Life Insurance Policy For CashEqually important are 24/7 customer support, fast claims processing (some offer same-day payouts), and mobile apps that allow real-time policy adjustments and claim filing. Transparent pricing, strong financial strength ratings (A.M. Best “A” or higher), and availability of multi-policy discounts are other critical indicators of a quality insurer.

Comparison of Leading Home Insurance Companies in 2025

To help homeowners make informed decisions, the table below compares some of the best home insurance companies in 2025 based on key criteria, including average annual premium, customer satisfaction, financial strength, and standout features. These metrics reflect data from independent sources such as J.D. Power, AM Best, and the National Association of Insurance Commissioners (NAIC).

| Insurance Company | Avg. Annual Premium | Customer Satisfaction (J.D. Power) | Financial Strength (AM Best) | Standout Features |

|---|---|---|---|---|

| State Farm | $1,450 | 845/1,000 | A++ | Nationwide agent support, multi-policy discounts, reliable claims service |

| Allstate | $1,620 | 829/1,000 | A+ | Customizable add-ons, digital tools, smart home discounts |

| USAA | $1,320 | 870/1,000 | A++ | Lowest average rates, military-exclusive benefits, excellent service |

| Amica Mutual | $1,700 | 865/1,000 | A+ | Dividend payments, high customer loyalty, top-rated support |

| Lemonade | $1,250 | 810/1,000 | A- | AI-powered claims, instant policy issuance, eco-friendly discounts |

Best Home Insurance Companies in 2025: Comprehensive Guide and Comparisons

Which home insurance company is considered the most reliable in 2025?

Top-Rated Home Insurance Companies in 2025 Based on Financial Strength

In 2025, several home insurance providers stand out for their exceptional financial stability, a key factor in determining reliability. Companies such as State Farm, Allstate, and USAA continue to earn top marks from major credit rating agencies like AM Best, Moody’s, and Standard & Poor’s.

Strong financial health ensures that an insurer can meet its obligations, even in the aftermath of widespread disasters or economic downturns. Customers benefit from policies backed by companies with a proven track record of solvency and consistent performance. Below are three insurers recognized for superior financial strength:

- State Farm – Maintains an AM Best rating of A++, reflecting outstanding ability to meet ongoing insurance obligations and a robust balance sheet.

- USAA – Also rated A++ by AM Best, USAA is known for its niche focus on military families and its long-term financial resilience.

- Chubb – Despite a higher price point, Chubb offers an A++ rating and is renowned for underwriting discipline and capital adequacy.

Customer Satisfaction and Service Reliability in 2025

Reliability in home insurance is not solely about paying claims but also about how smoothly the process unfolds. In 2025, customer satisfaction surveys from J.D. Power and the National Association of Insurance Commissioners (NAIC) reveal insurers that excel in response time, digital accessibility, and claim handling.

High reliability often correlates with low complaint ratios and high retention rates. Homeowners increasingly value responsive customer service, intuitive mobile apps, and transparent communication during stressful events. The following companies have consistently led in customer experience metrics:

- Amica Mutual – Ranked highest in J.D. Power’s 2025 U.S. Home Insurance Study for overall customer satisfaction, praised for its friendly agents and fast claims processing.

- USAA – Offers 24/7 support, military-hour flexibility, and personalized digital tools, resulting in a loyal customer base and superior service reviews.

- Liberty Mutual – Improved its customer service framework significantly since 2023, introducing AI-driven chat support and faster claim verification.

Claim Handling and Policy Flexibility in 2025

One of the most significant indicators of a reliable home insurance provider is its efficiency and fairness in claim settlements. In 2025, top insurers differentiate themselves through rapid deployment of adjusters, minimal claim denials, and flexible coverage options tailored to modern homeowner needs.

Policyholders benefit from customizable add-ons such as inflation protection, green home rebuilding, or high-value personal property endorsements. Clear communication during the claims process and fair assessment practices enhance trust and long-term reliability. The following insurers lead in claim reliability and policy adaptability:

- State Farm – Processes a high percentage of claims within 72 hours and offers flexible rebuilding cost coverage that adjusts automatically with market changes.

- Allstate – Provides NextGen claim tools, including photo-based estimates and real-time tracking, reducing settlement time and increasing transparency.

- Chubb – Known for concierge-level claims service, often assigning dedicated representatives for high-net-worth clients and offering guaranteed replacement cost coverage.

Will home insurance rates decrease in 2025, and which companies offer the best coverage?

)

Will Home Insurance Rates Decrease in 2025?

- As of current industry forecasts, it is unlikely that home insurance rates will broadly decrease in 2025. Instead, experts anticipate continued rate increases or stabilization at high levels due to rising construction costs, increased severity of weather-related claims, and inflationary pressures. Insurers are adjusting premiums to reflect the growing financial risks associated with climate change, especially in regions prone to wildfires, hurricanes, and flooding.

- Regional variations will play a significant role in determining rate movements. Areas with frequent natural disasters may see steeper premium hikes, while markets with improved risk management and lower claim frequencies could experience slower increases or temporary pauses in rate growth.

- Regulatory scrutiny in certain states may also impact future pricing. Some state insurance departments are reviewing rate hike requests more closely, potentially limiting how much insurers can raise prices. However, these interventions are unlikely to result in overall rate decreases but may prevent further escalation in specific areas.

Top Home Insurance Companies for Comprehensive Coverage

- State Farm remains a leading provider due to its extensive agent network, customizable policies, and strong financial stability. It offers robust dwelling and liability coverage, along with popular add-ons like identity restoration and equipment breakdown protection. Its claims satisfaction ratings are consistently high, making it a reliable choice for homeowners seeking dependable service.

- Allstate stands out for its wide range of policy enhancements, including premium rewards for safe homes and claim-free histories. It provides optional coverages such as extended replacement cost and protection for valuable items, appealing to homeowners with high-value properties or costly possessions.

- Amica Mutual consistently ranks at the top for customer satisfaction and financial strength. As a mutual insurer, it returns profits to policyholders through dividends. Amica offers full replacement cost coverage, no-depreciation claims payments, and personal property protection with broad perils coverage, making it ideal for those prioritizing peace of mind and long-term value.

Factors Influencing Home Insurance Affordability and Value

- Insurers evaluate property-specific factors such as location, age of the home, claims history, and local crime rates when setting premiums. Homes equipped with security systems, fire alarms, and storm-resistant features may qualify for discounts, improving affordability. Proactively mitigating risks can lead to lower rates even in high-cost markets.

- The competitive landscape also affects pricing. Companies like USAA (available to military members and their families) and Nationwide offer competitive bundles and loyalty programs that can reduce overall costs. Shopping around and comparing quotes annually allows homeowners to identify better value options despite rising base rates.

- Increased adoption of usage-based pricing models and data analytics is enabling more personalized policies. Some insurers now offer programs where premiums are adjusted based on real-time risk assessments or home maintenance habits. These innovations may enhance affordability for low-risk policyholders, even if average market rates remain elevated in 2025.

What is the 80% home insurance rule and how does it impact coverage with top insurers in 2025?

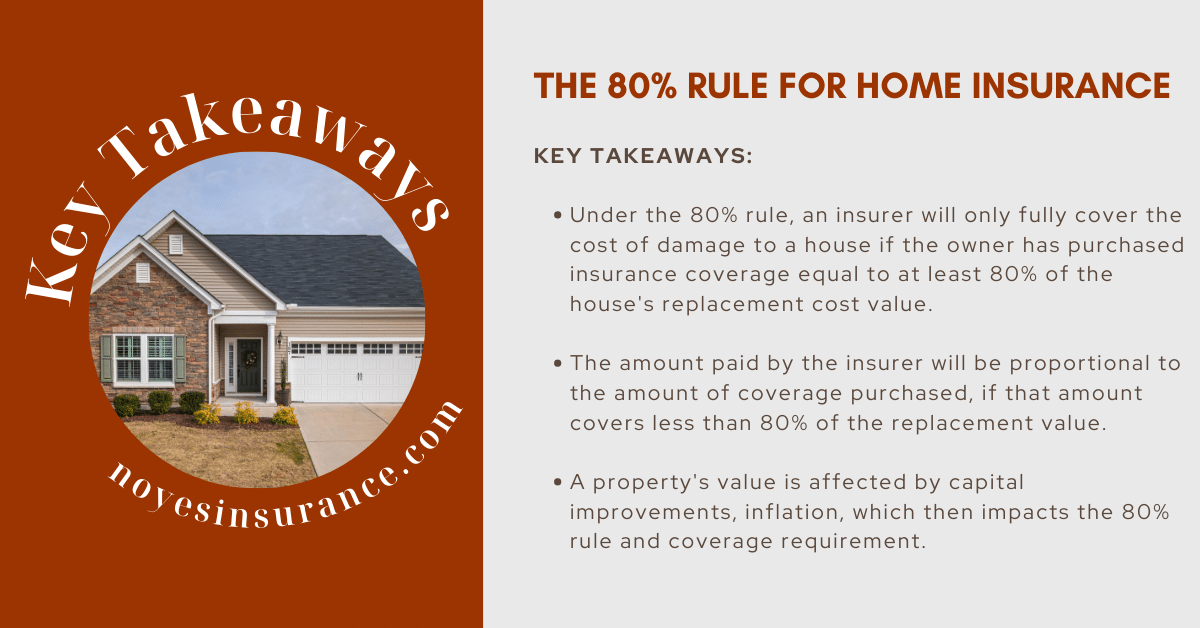

Understanding the 80% Home Insurance Rule

- The 80% home insurance rule is a guideline used by most major insurers to determine the minimum amount of dwelling coverage a homeowner must carry to receive full reimbursement for a partial loss. According to this rule, homeowners must be insured for at least 80% of their home’s replacement cost value to qualify for complete payment of a claim that doesn’t involve a total loss.

- If a homeowner’s policy covers less than 80% of the home’s replacement cost, the insurer applies a coinsurance penalty. This means the payout for a claim is reduced in proportion to how much the coverage falls short of the 80% threshold. For example, if a home has a replacement value of $500,000 but is only insured for $350,000 (70%), the homeowner would receive only a portion of a repair claim, even if the damage is below the deductible threshold.

- This rule is intended to encourage homeowners to maintain coverage that adequately reflects current rebuilding costs, factoring in inflation, materials, labor, and local construction regulations. As property rebuilding expenses have risen steadily in recent years, especially through 2024–2025 due to supply chain recovery fluctuations and labor shortages, maintaining alignment with the 80% rule has become increasingly important to avoid underinsurance.

How the 80% Rule Affects Claims with Top Insurers in 2025

- Major insurers such as State Farm, Allstate, and Nationwide continue to enforce the 80% rule in 2025, especially in states prone to natural disasters like hurricanes, wildfires, and severe storms. These companies use proprietary rebuilding cost calculators to estimate replacement values and apply the coinsurance clause when claims are filed underinsured homes.

- In practice, if a homeowner with a $400,000 replacement cost only has $300,000 in dwelling coverage (75%), and files a $50,000 claim for roof damage, the insurer may pay only about $46,875 after applying the coinsurance formula. This reduction occurs because the homeowner didn’t meet the 80% threshold, resulting in a partial denial based on proportional underinsurance.

- Some insurers now offer inflation guard endorsements or extended replacement cost coverage to help policyholders automatically adjust coverage limits annually, keeping them within the 80% safe zone. However, these features do not eliminate the need for homeowners to periodically reassess their dwelling coverage, especially after home renovations or in rapidly appreciating real estate markets.

Strategies to Comply with the 80% Rule in 2025

- Homeowners should obtain a professional replacement cost assessment, preferably every 3 to 5 years, to ensure their dwelling coverage keeps pace with inflation and construction cost trends. Many insurers partner with third-party valuation tools like Xactware or CoreLogic to provide up-to-date estimates.

- Purchasing agreed value policies, offered by some top-tier insurers, can bypass the 80% rule by locking in a pre-determined replacement cost. These policies typically require documentation such as appraisals and are more common in high-value home markets.

- Regular policy reviews with a licensed agent are essential, particularly after any home improvement or regional market shifts. In 2025, several insurers are introducing AI-driven policy dashboards that alert homeowners when their coverage drops below recommended thresholds, helping maintain compliance with the 80% rule proactively.

What are the most affordable home insurance providers in Louisiana for 2025?

Top Affordable Home Insurance Providers in Louisiana for 2025

- State Farm continues to lead the market in Louisiana for 2025 with highly competitive rates and widespread availability. Known for strong customer service and personalized policies, State Farm offers savings through bundling, loyalty programs, and discounts for home security systems and claim-free histories.

- USAA is consistently one of the most affordable options, though it is exclusive to military members, veterans, and their immediate families. USAA’s combination of low premiums, excellent customer satisfaction ratings, and comprehensive coverage makes it a top choice for eligible homeowners across the state.

- Liberty Mutual provides scalable coverage options and frequent discounts, particularly for customers who install smart home devices or maintain long-term policies. Their flexible payment plans and localized underwriting practices make them a practical and affordable alternative in high-risk areas of Louisiana.

Factors Influencing Home Insurance Affordability in Louisiana

- Geographic location significantly affects premiums, especially in coastal parishes vulnerable to hurricanes and flooding. Insurers like Nationwide and Allstate adjust rates based on proximity to the Gulf Coast, storm history, and local building codes.

- Credit score remains a critical factor in determining rates across most major insurers. Companies such as Farmers and Travelers commonly offer lower premiums to policyholders with strong credit histories, sometimes reducing annual costs by 20% or more.

- Home construction type and age play a major role; newer homes built with storm-resistant materials often qualify for discounts. Insurers including Allstate and Progressive reward hurricane shutters, reinforced roofs, and elevated foundations—common upgrades in flood-prone zones.

How to Save on Home Insurance in Louisiana

- Comparing quotes from multiple insurers annually can uncover significant savings. Websites like Insurify, The Zebra, and NerdWallet allow side-by-side comparisons, often revealing lower rates from less prominent carriers such as NFIP-participating insurers or regional companies like Southern Specialty.

- Bundling home and auto insurance typically results in discounts ranging from 10% to 25%. Providers like State Farm and Allstate emphasize bundle incentives, and some also offer additional reductions for paperless billing and automatic payments.

- Improving home resilience through retrofitting can reduce premiums over time. Installing impact-resistant windows, securing HVAC units, and upgrading electrical systems not only increase safety but also qualify for discounts from most major insurers operating in Louisiana.

Frequently Asked Questions

What are the top home insurance companies in 2025?

In 2025, top home insurance companies include State Farm, Allstate, USAA (for military families), and Nationwide. These providers are recognized for their comprehensive coverage options, strong financial ratings, excellent customer service, and user-friendly digital platforms. USAA consistently ranks highest in customer satisfaction, while State Farm leads in affordability and accessibility. Always compare quotes and read reviews to find the best fit for your specific needs and location.

How do I choose the best home insurance provider in 2025?

To choose the best home insurance provider in 2025, evaluate companies based on coverage options, customer service ratings, pricing, financial strength, and available discounts. Compare multiple quotes, read customer reviews, and check complaint indices from organizations like J.D. Power or AM Best. Consider insurers with easy claims processes, 24/7 support, and digital tools. Your home’s location, age, and value also impact the best choice, so tailor your selection accordingly.

Which home insurance company offers the cheapest rates in 2025?

In 2025, companies like State Farm, Farmers, and Amica typically offer some of the most competitive rates. State Farm often ranks as the cheapest for many homeowners due to widespread availability and personalized discounts. However, the lowest rate depends on your location, home value, credit history, and coverage needs. It’s essential to compare quotes from at least three providers to ensure you’re getting the best possible deal for your specific situation.

Do home insurance companies in 2025 offer smart home discounts?

Yes, most leading home insurance companies in 2025 offer discounts for smart home devices. Installing security systems, smart thermostats, water leak detectors, or fire alarms can reduce premiums with providers like Allstate, Nationwide, and State Farm. These devices lower risk, which insurers reward with savings—often 5% to 20%. Be sure to confirm eligibility and required brands with your insurer, as discount terms vary by company and policy type.

Leave a Reply