Best home insurance providers 2025

Choosing the right home insurance provider in 2025 means balancing coverage, cost, and customer service. With natural disasters on the rise and property values fluctuating, homeowners need reliable protection tailored to evolving risks.

The best insurers stand out through comprehensive policies, transparent pricing, and responsive claims handling. From digital-first companies simplifying the experience to established carriers expanding coverage options, the market offers diverse choices.

This guide evaluates leading home insurance providers based on financial strength, customer satisfaction, available discounts, and innovative features like smart home integration. Discover which companies deliver the most value and peace of mind for your greatest investment—your home.

Home insurance in kansas

Home insurance in kansasBest Home Insurance Providers in 2025: Top Choices for Comprehensive Coverage

As we move into 2025, the home insurance market continues to evolve, offering homeowners a wider range of options that combine affordability, digital innovation, and robust protection. The best home insurance providers this year stand out not only for their competitive premium rates but also for their customer service, claims handling efficiency, and customizable coverage options.

Companies have increasingly adopted AI-driven risk assessment, mobile-friendly platforms, and eco-friendly incentives, improving the overall policyholder experience. Whether you're a first-time homeowner or looking to switch providers, understanding which insurers lead the industry in reliability, financial strength, and customer satisfaction is essential for making an informed decision.

Leading providers are rated by independent agencies such as AM Best for their financial stability, while customer reviews highlight performance in real-world claim settlements and digital service accessibility.

Top-Rated Home Insurance Companies in 2025

In 2025, several insurers dominate the industry based on comprehensive ratings from J.D. Power, AM Best, and Consumer Reports. State Farm continues to lead with its extensive agent network and consistent customer satisfaction scores, especially in personalized service and fast claims processing.

Home inspection e&o insurance

Home inspection e&o insuranceAllstate stands out for its tech-driven tools like Smart Home Discounts and digital claim filing, appealing to tech-savvy homeowners. Farmers Insurance earns recognition for flexible policy bundling and broad geographical coverage, especially in diverse climates.

Additionally, USAA (available to military members and families) maintains top-tier rankings for low premiums and exceptional service, often outperforming competitors in member loyalty. New contenders like Lemonade use AI to streamline underwriting and claims, offering transparent pricing that appeals to younger homeowners, though with slightly more limited coverage in certain states.

Key Factors to Consider When Choosing a Provider

When evaluating the best home insurance provider in 2025, several critical factors should influence your decision. Financial strength is paramount—insurers rated “A+” or higher by AM Best are more likely to pay claims reliably, especially after large-scale disasters.

Customer service reputation, as reflected in surveys and complaint indexes from the National Association of Insurance Commissioners (NAIC), helps predict real-world support experiences. Equally important are coverage options, such as protection for high-value items, identity theft, or home-sharing activities (like Airbnb).

Home insurance age uk

Home insurance age ukLook for providers offering discounts for bundling with auto insurance, installing security systems, or maintaining long-term loyalty. Finally, ease of use through mobile apps, online portals, and responsive claims support—especially 24/7 availability—can significantly improve your experience during emergencies.

Below is a comparison of five leading home insurance providers in 2025 based on average annual premiums, key coverage features, and customer satisfaction ratings. These figures are compiled from national averages and may vary by location, home value, and policy customization.

| Insurance Provider | Avg. Annual Premium | Key Coverage Features | Customer Satisfaction (out of 5) | Discounts Offered |

|---|---|---|---|---|

| State Farm | $1,420 | Liability coverage, personal property protection, loss of use | 4.5 | Multi-policy, claims-free, home security |

| Allstate | $1,560 | Smart home integration, deductible rewards, extended rebuilding | 4.3 | Bundling, digital tools, loyalty |

| Farmers | $1,620 | Green rebuilding, personal article floaters, identity theft | 4.1 | Home & auto bundle, claims-free, protective devices |

| USAA | $1,310 | Full replacement cost, natural disaster coverage, emergency funds | 4.7 | Military loyalty, multi-policy, auto-pay |

| Lemonade | $1,290 | Renters & homeowners, AI-powered claims, eco-upgrade reimbursement | 4.0 | Bundle, security systems, paperless billing |

Top Home Insurance Providers in 2025: A Comprehensive Guide

Will home insurance rates decrease in 2025 among the top providers?

)

Factors Influencing Home Insurance Rates in 2025

- Economic inflation, particularly in construction and labor costs, continues to exert upward pressure on home insurance premiums. Even if overall inflation trends stabilize in 2025, insurers may maintain elevated rates to account for lingering material expenses and supply chain inefficiencies.

- Climate change is increasingly impacting underwriting models, with more frequent and severe natural disasters like hurricanes, wildfires, and floods. Insurers are adjusting their risk assessments, particularly in high-exposure regions such as Florida, California, and the Gulf Coast, which may prevent significant rate decreases even if national averages appear stable.

- Regulatory oversight in certain states may limit dramatic rate increases, but this does not necessarily translate into rate reductions. In competitive markets, providers might slow the pace of hikes, but proactive decreases are rare unless there is a measurable drop in claims frequency or severity.

Outlook for Major Insurance Providers in 2025

- Larger insurers such as State Farm, Allstate, and Nationwide are likely to maintain a cautious approach in 2025, emphasizing financial resilience over aggressive pricing. While they may offer selective discounts or introduce usage-based policies, widespread rate reductions are improbable given their exposure to climate-related claims.

- Some regional providers, particularly those exiting high-risk areas due to financial strain, are recalibrating their portfolios. Companies like Citizens Property Insurance in Florida have been transitioning policies back to private insurers, creating market volatility that discourages general rate decreases.

- Federally backed programs such as the NFIP (National Flood Insurance Program) may undergo rate adjustments based on updated flood mapping, but these changes are designed to reflect true risk rather than reduce costs. This shift supports broader industry trends toward risk-based pricing instead of across-the-board decreases.

Potential Scenarios Where Rates May Stabilize or Decline

- Areas experiencing reduced claim volumes—potentially due to improved building codes, better disaster preparedness, or favorable weather patterns—could see slower rate increases. In rare cases, minor downward adjustments may occur if insurers experience better-than-expected loss ratios in specific ZIP codes.

- Increased competition in less exposed regions, such as the Midwest or Northeast, might prompt select insurers to offer promotional rates or loyalty discounts. However, these are typically targeted and temporary, not indicative of industry-wide decreases.

- Advancements in risk modeling, including AI-driven analytics and real-time weather monitoring, could allow insurers to price policies more accurately. While this might prevent unnecessary hikes, it is unlikely to result in broad reductions unless accompanied by a systemic decline in property damage events.

Which home insurance provider offers the best coverage in 2025?

Home insurance claim proof of ownership requirement

Home insurance claim proof of ownership requirementTop Home Insurance Providers with Comprehensive Coverage in 2025

- State Farm continues to stand out in 2025 for offering some of the most comprehensive home insurance coverage options, particularly due to its broad range of customizable policies. With strong financial backing and a nationwide network of agents, State Farm provides extended dwelling protection, personal property coverage, liability safeguards, and additional living expenses with relatively few exclusions. Their Claim Satisfaction Index remains high, indicating reliable service during critical times.

- Allstate is recognized for its innovative policy add-ons such as smart home discounts, increased roof coverage, and identity theft protection bundled within home policies. In 2025, Allstate enhances its value through digital claim filing and real-time damage assessment using AI tools, improving customer experience. Their dedication to modernizing service delivery without compromising coverage breadth strengthens their position among top-tier providers.

- Amica Mutual consistently ranks at the top in customer satisfaction surveys and claims handling efficiency. Offering guaranteed renewable policies and dividend payouts to policyholders, Amica combines robust standard coverage with a no-claims surcharge policy, making it attractive for long-term homeowners. Their inclusion of premium concierge services and superior customer support adds significant value beyond typical policy terms.

Factors That Define the Best Home Insurance Coverage in 2025

- Comprehensive coverage in 2025 extends beyond standard perils to include protection against emerging risks such as cyber liability (for smart home devices), mold due to climate-related humidity, and temporary housing inflation caused by construction material shortages. The best providers now offer optional riders addressing these concerns, providing more holistic protection tailored to evolving homeowner needs.

- Claims processing efficiency is a major differentiator, with leading companies leveraging AI-driven damage assessment, drone inspections, and same-day claim approvals. Providers that minimize delays and offer transparent online tracking systems gain significant trust and satisfaction ratings. The ability to file and manage claims seamlessly through mobile apps is now considered standard for top-tier insurers.

- Customization and flexibility in policy building allow homeowners to scale coverage based on location-specific risks, such as wildfire zones, coastal flooding, or urban theft rates. The best providers in 2025 offer modular coverage options, enabling policyholders to add earthquake insurance, sewer backup, or equipment breakdown protection without complex underwriting processes.

Regional Considerations and Provider Strength in 2025

- Insurance needs vary significantly by region, influencing which provider offers the best coverage. For example, USAA excels in military communities and states with high veteran populations, offering exclusive benefits and lower rates for service members, despite its membership restrictions. In hurricane-prone areas like Florida, providers such as Citizens Property Insurance (while a last-resort option) and Nationwide offer specialized windstorm and flood add-ons that are essential for adequate protection.

- In the western United States, especially in fire-prone regions like California, companies like Chubb and Farmers provide enhanced wildfire coverage, including debris removal, evacuation expense reimbursement, and extended replacement cost benefits. These specialized offerings make them more suitable than national averages in high-risk zones, where standard policies often fall short.

- Northeastern and Midwestern homeowners benefit from providers like Erie Insurance and Liberty Mutual, who offer strong coverage for winter-related incidents such as ice dam damage, burst pipes, and snow collapse. These insurers often bundle home and auto policies with additional discounts, improving affordability while maintaining high coverage limits and low complaint ratios reported to state insurance departments.

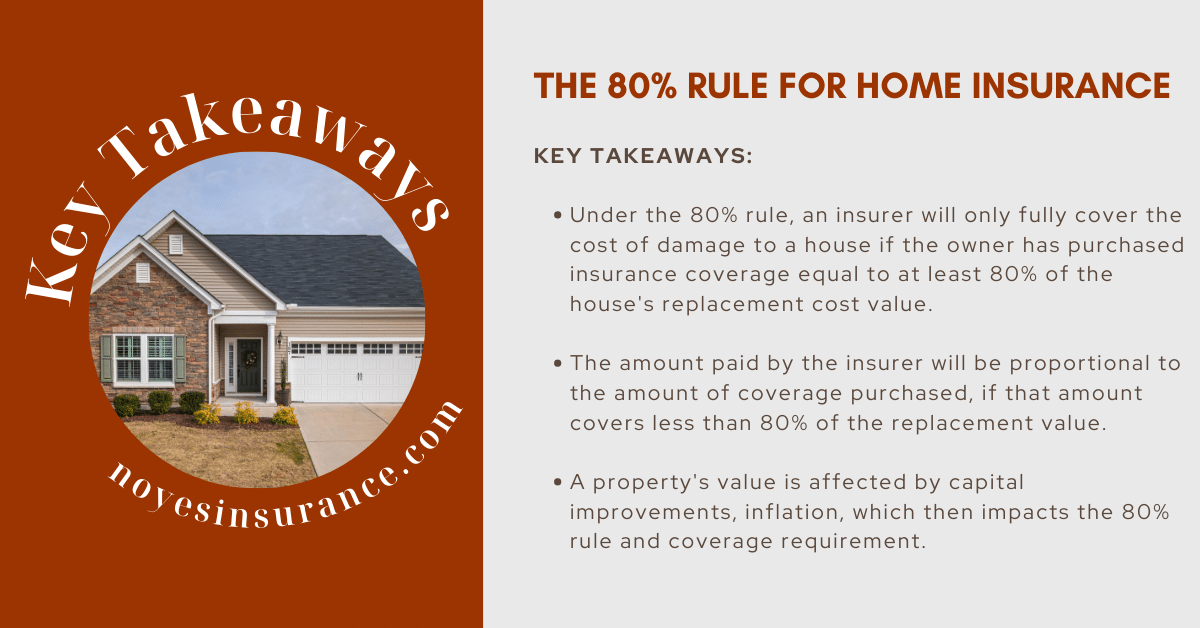

What Does the 80% Rule Mean for Home Insurance Coverage in 2025?

Understanding the 80% Rule in Home Insurance

- The 80% rule in home insurance is a principle used by insurers to determine the minimum amount of coverage a homeowner should carry to receive full reimbursement for a partial loss. If a homeowner insures their property for less than 80% of its replacement cost, the insurer may reduce the claim payout proportionally.

- This rule primarily applies to structural damage, such as that caused by fire, wind, or other covered perils. Its purpose is to encourage homeowners to maintain coverage levels that reflect the true cost to rebuild their homes, reducing the risk of underinsurance across the policy base.

- For example, if a home’s replacement value is $300,000, the homeowner should carry at least $240,000 in dwelling coverage (80% of $300,000) to qualify for full payment on most claims. Falling below this threshold triggers a co-insurance penalty, meaning the policyholder shares more of the loss.

How the 80% Rule Affects Claim Payouts in 2025

- In 2025, the 80% rule continues to influence how much homeowners receive during a claim, especially in regions where construction costs have risen due to labor shortages or material inflation. If a homeowner is underinsured, the insurer calculates the payout based on the ratio of actual coverage to required coverage.

- For instance, if a home needs $300,000 to rebuild but is only insured for $200,000 (67% of replacement cost), and a $50,000 repair is needed, the insurer pays only a portion. The formula typically reduces the claim: ($200,000 / $240,000) x $50,000 = $41,667, leaving the homeowner to cover the remaining $8,333.

- This calculation emphasizes why maintaining adequate coverage is crucial. As rebuilding expenses climb nationwide, failure to adjust policy limits annually can leave homeowners exposed to significant out-of-pocket costs even with an active policy.

Strategies to Stay Compliant with the 80% Rule in 2025

- Homeowners should regularly review their policy declarations page and request a replacement cost evaluation from their insurer or an independent appraiser, especially after home improvements or in high-inflation markets. This ensures coverage keeps pace with current construction trends.

- Opting for extended or guaranteed replacement cost coverage can help bypass the 80% rule entirely. These policy upgrades promise to cover the full rebuilding cost even if it exceeds the policy limit, often up to a specified percentage above the dwelling coverage amount.

- Consulting with an insurance agent at renewal time to adjust coverage limits based on local cost-per-square-foot data and material price indices is a proactive step. In 2025, with volatile supply chains and evolving building codes, staying ahead of coverage gaps is more important than ever.

What are the most affordable home insurance providers in Louisiana for 2025?

Top Affordable Home Insurance Providers in Louisiana for 2025

- Lafayette Insurance Company continues to be one of the most cost-effective options for homeowners in Louisiana in 2025, offering regionally tailored policies that account for local climate risks and construction costs. Known for competitive base rates and loyalty discounts, it’s a preferred choice among long-term residents, especially in rural parishes.

- State Farm maintains a strong presence across Louisiana with consistently low average premiums, particularly for customers who bundle home and auto insurance. Its extensive network of local agents allows for personalized service and faster claims processing, contributing to high customer satisfaction despite rising industry prices.

- USAA stands out for affordability, but is limited to active-duty military members, veterans, and their eligible family members. In 2025, USAA remains one of the lowest-cost providers in the state, offering high coverage limits and excellent customer service, essential in a region prone to hurricanes and flooding.

Factors Influencing Home Insurance Costs in Louisiana

- Geographic location plays a major role, with homes near the Gulf Coast facing significantly higher premiums due to hurricane exposure. Insurers factor in storm frequency, flood zones, and proximity to the shoreline when calculating risk, often requiring windstorm and flood endorsements that increase overall cost.

- Construction type and home age impact pricing, as older homes with outdated electrical or plumbing systems are considered higher risk. Homes built to modern hurricane-resistant standards, such as those with reinforced roofs and impact-resistant windows, often receive discounts.

- Credit score and claims history are critical underwriting factors in Louisiana. Insurers typically offer better rates to policyholders with higher credit scores and no recent claims, reflecting their lower perceived risk. Maintaining a clean history can lead to multi-year discounts and lower base premiums.

How to Save Money on Home Insurance in Louisiana

- Comparing quotes from at least three insurers annually helps homeowners secure the best rates, as pricing models and discounts can vary widely. Independent online comparison tools and local insurance agents can provide multiple options tailored to individual needs and property characteristics.

- Installing safety and mitigation features, such as storm shutters, reinforced garage doors, or monitored security systems, can lead to significant premium reductions. Some insurers offer discounts of up to 15% for homes in fortified zones that meet specific hurricane-resistant construction standards.

- Choosing a higher deductible lowers monthly premiums, though it requires setting aside funds in case of a claim. This strategy works best for financially stable homeowners who want to minimize ongoing costs while maintaining adequate coverage for severe events.

Frequently Asked Questions

What are the top home insurance providers in 2025?

In 2025, the best home insurance providers include State Farm, Allstate, USAA, and Amica. These companies consistently rank high for customer satisfaction, comprehensive coverage options, and competitive pricing. State Farm leads in affordability and agent support, while USAA excels for military families. Amica stands out for superior service and financial strength. Allstate offers innovative policy features like smart home discounts, making it a strong overall choice.

How do I choose the best home insurance provider?

To choose the best home insurance provider, compare coverage options, premiums, customer service ratings, and available discounts. Look for insurers with strong financial ratings from agencies like AM Best. Consider customer reviews and claims satisfaction scores. Ensure the provider offers protection for your home’s value, possessions, and liability needs. Also, verify if they provide add-ons like flood or earthquake coverage if required in your area.

Home insurance claims attorney

Home insurance claims attorneyWhich home insurance company offers the cheapest rates in 2025?

In 2025, State Farm typically offers the cheapest home insurance rates for most homeowners, thanks to extensive agent networks and personalized quotes. Farmers Insurance and Allstate also provide competitive pricing, especially for those bundling home and auto policies. Rates vary by location, home value, and coverage needs, so it’s essential to compare personalized quotes from multiple providers to find the most affordable option for your specific situation.

Does USAA offer home insurance in 2025 and who is eligible?

Yes, USAA offers home insurance in 2025 and is highly rated for coverage, service, and value. It’s available exclusively to active, retired, and honorably discharged military members and their eligible family members. USAA provides excellent customer support, competitive rates, and specialized options for military lifestyles, such as coverage during deployments. Civilians are not eligible but can explore other top providers like State Farm or Allstate.

Leave a Reply