Best insurance for custom-built homes

Custom-built homes offer unparalleled personalization and quality, but they also come with unique risks that standard homeowner’s insurance may not fully cover. From specialized materials to extended construction timelines, the intricacies of custom builds demand a tailored insurance approach.

The best insurance for custom-built homes provides comprehensive protection for both the structure and the investment throughout every phase of development. Policies should account for construction delays, material shortages, and fluctuating rebuild costs.

Understanding coverage options like guaranteed replacement cost and green building repairs is essential. Choosing the right policy ensures peace of mind and financial security for one of life's most significant projects.

Rock hill second home insurance

Rock hill second home insuranceBest Insurance for Custom-Built Homes: Protecting Your Unique Investment

Custom-built homes offer unmatched personalization and craftsmanship, but they also come with unique risks and replacement challenges that standard homeowners insurance may not fully cover. The best insurance for these properties is specifically tailored to reflect the higher construction costs, specialized materials, and extended rebuild timelines often associated with custom designs.

Unlike typical homes, where replacement value can be estimated using standard benchmarks, custom-built homes require appraisals based on unique architecture, labor-intensive techniques, and non-standard finishes. As a result, the ideal policy should include guaranteed replacement cost coverage, which ensures the home can be rebuilt exactly as designed, even if costs exceed the policy limit.

Additional features like ordinance or law coverage and extended build-out periods are also critical, providing financial protection against zoning changes or construction delays. Choosing an insurer with experience in high-value and custom properties ensures a smoother claims process and more accurate risk evaluation.

Key Features of Ideal Custom Home Insurance Policies

The best insurance policies for custom-built homes go beyond basic protection by offering comprehensive coverage designed for high-value, one-of-a-kind residences. Essential features include guaranteed or extended replacement cost coverage, which pays for a complete rebuild even if costs surpass the policy amount due to fluctuations in labor or material pricing.

Role of home safety measures in insurance

Role of home safety measures in insuranceInflation guard is another vital component, automatically adjusting coverage limits to keep pace with construction cost increases. Coverage for high-end materials—such as granite countertops, imported tiles, or custom cabinetry—ensures that luxurious finishes are adequately protected.

Additional living expenses should also be robust, allowing homeowners to maintain their standard of living during extended reconstruction periods. Finally, water backup, earthquake, and flood endorsements should be considered based on geographic location, ensuring all potential risks are addressed.

Top Insurance Providers for Custom-Built Homes

Several insurers specialize in covering high-value and custom-built homes, offering policies that reflect the complexity and expense of these properties. Companies like Chubb, American Family Premier, and Nationwide Exclusive are recognized leaders in the luxury home insurance market, providing customizable coverage with higher limits and specialized support.

Chubb, for instance, offers valuable upgrades such as increased coverage for fine art, jewelry, and electronic systems commonly found in custom homes. American Family's Premier package includes concierge claims service and green rebuild options, appealing to eco-conscious homeowners.

State farm home insurance rate increase 2025

State farm home insurance rate increase 2025Meanwhile, Nationwide’s Exclusive Home program focuses on personalized risk assessments and extended replacement cost up to 150% of the dwelling limit. These insurers also employ underwriters familiar with architectural nuances, ensuring accurate valuations and minimizing disputes during claims.

Factors That Influence Custom Home Insurance Costs

Insurance premiums for custom-built homes are influenced by a combination of structural, locational, and personal factors that reflect the increased risk and value of these properties. The construction quality and materials used—such as steel framing, stone exteriors, or custom millwork—can both increase rebuilding costs and, in some cases, reduce risk, thereby affecting premiums.

Location plays a major role; homes in areas prone to wildfires, hurricanes, or floods face higher rates and may require additional endorsements. The home’s square footage, architectural complexity, and inclusion of amenities like pools, guest houses, or home automation systems also impact pricing.

Additionally, the homeowner's claims history, credit score, and chosen deductible level contribute to the final cost. Understanding these variables helps homeowners select the most cost-effective policy without sacrificing essential coverage.

| Insurance Feature | Why It Matters | Recommended Option |

|---|---|---|

| Guaranteed Replacement Cost | Covers full rebuild costs regardless of policy limits, essential for unique designs. | Chubb, Nationwide Exclusive |

| Extended Period of Construction | Provides coverage for delays in rebuilding due to permits or labor shortages. | American Family Premier |

| Ordinance or Law Coverage | Pays for upgrades required by new building codes after a loss. | Chubb, Nationwide |

| Inflation Guard | Adjusts coverage annually to match rising construction costs. | American Family, Nationwide |

| High-Value Personal Property Coverage | Protects premium interiors, art, and luxury appliances. | Chubb, American Family |

Best Insurance Options for Custom-Built Homes: A Comprehensive Guide

What insurance coverage is essential during the construction of a custom-built home?

Builders Risk Insurance

- Builders risk insurance is one of the most critical coverages during the construction of a custom-built home, as it protects the structure itself from physical damage caused by perils such as fire, wind, theft, and vandalism while under construction.

- This policy typically covers materials, equipment, and the partially completed structure on-site, helping to mitigate financial loss if an unforeseen event interrupts or damages the building process.

- It is usually taken out by the homeowner or the general contractor and remains active from groundbreaking until the homeowner occupies the home, ensuring continuous protection throughout every phase of construction.

General Liability Insurance

- General liability insurance safeguards the homeowner and contractor against third-party claims of bodily injury or property damage that may occur on the construction site.

- For example, if a delivery person slips and falls on the property or if a worker accidentally damages a neighbor's landscaping, this coverage can pay for medical expenses, legal fees, or repair costs.

- It is essential for managing potential lawsuits and maintaining financial stability during construction, especially given the inherently hazardous nature of active building zones.

Workers Compensation Insurance

- Workers compensation insurance is mandatory in most regions when hiring contractors or laborers and provides medical benefits and wage replacement to employees injured on the job.

- During custom home construction, multiple workers are often present, increasing the likelihood of workplace accidents such as falls, equipment injuries, or exposure incidents.

- Having this coverage not only protects the workforce but also shields the homeowner from direct liability, ensuring that injured workers receive proper care without leading to costly personal injury claims against the property owner.

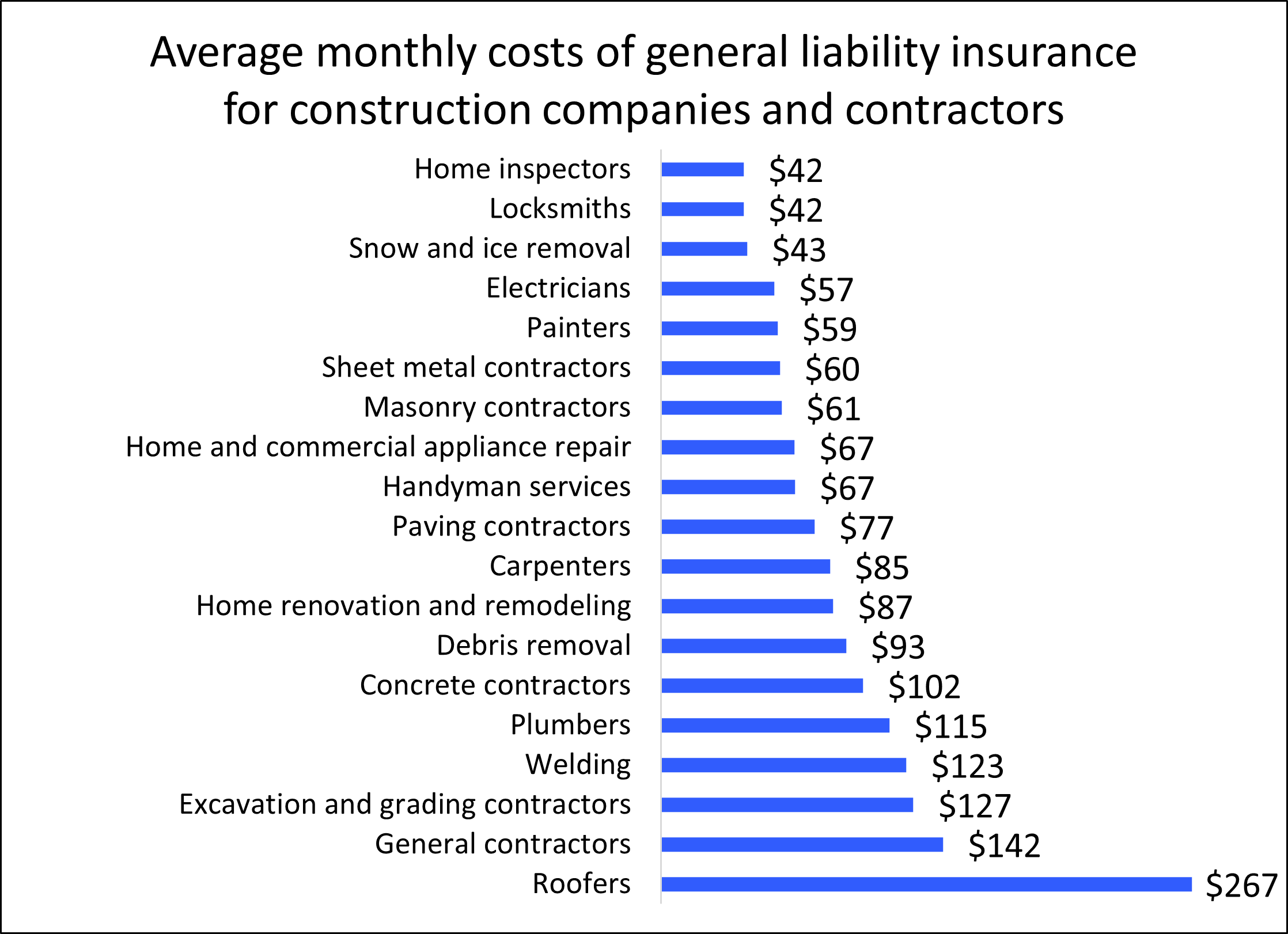

What is the average cost of $1,000,000 general liability insurance for custom-built homes?

The average cost of $1,000,000 general liability insurance for custom-built homes typically ranges between $1,000 and $3,500 annually, depending on various factors such as location, builder experience, project complexity, and coverage limits.

Contractors and custom home builders usually purchase general liability insurance to protect against third-party claims involving bodily injury, property damage, and advertising injury arising during construction.

Premiums can vary significantly based on risk exposure—for instance, a builder working on high-end projects in earthquake-prone areas may face higher rates. Additionally, insurers often evaluate a builder's claims history, number of employees, and safety protocols when determining policy costs.

Factors That Influence the Cost of General Liability Insurance for Custom Home Builders

- Geographic location plays a major role; regions with higher construction costs, harsher weather, or stricter regulations—like California or Florida—generally have higher premiums due to increased risk exposure.

- The builder’s experience and claims history directly impact pricing; contractors with a long track record and no recent claims are seen as lower risk and often receive more favorable rates.

- Project scope and home value are critical; building a 10,000-square-foot luxury home involves more materials, labor, and potential liability than a standard custom build, which increases the insurer’s perceived risk and therefore the cost.

Common Coverage Components Included in a $1M General Liability Policy

- Bodily injury coverage protects builders if a third party, such as a visitor or subcontractor, is injured on the job site due to the contractor’s operations, covering medical expenses and legal fees if a lawsuit arises.

- Property damage coverage applies when a builder accidentally damages a client’s property or that of a neighboring structure during construction, such as drilling into a gas line or causing water damage.

- Personal and advertising injury coverage includes liabilities like defamation, copyright infringement in design plans, or wrongful use of another company’s name in promotional materials related to the build.

- Implementing comprehensive safety programs and providing regular training for employees demonstrates risk mitigation to insurers, which can lead to lower premiums over time.

- Maintaining a clean claims history by resolving minor issues before they escalate helps keep policy rates stable or even qualify for no-claim discounts.

- Working with an experienced insurance broker who specializes in construction can help tailor a policy to the specific needs of custom home building, potentially bundling coverage or identifying overlooked discounts.

What is the top-rated insurance provider for custom-built manufactured homes?

Top-Rated Insurance Providers for Custom-Built Manufactured Homes

When evaluating the top-rated insurance provider for custom-built manufactured homes, American Family Insurance frequently stands out due to its specialized coverage options, strong financial ratings, and positive customer reviews.

Unlike standard homeowners insurance, policies for custom-built manufactured homes must account for unique construction methods, foundation types, and transport considerations. American Family offers tailored manufactured home policies that include protection for the structure, personal property, liability, and additional living expenses.

Their agents are trained to assess non-traditional builds, and they work with homes placed on permanent foundations as well as those on rented land. Other reputable providers include Nationwide and Farmers Insurance, both of which offer customizable plans and strong claims support, though availability may vary by state.

- American Family Insurance provides customizable policies specifically designed for manufactured homes, including custom builds with non-standard features.

- Nationwide offers robust coverage options with add-ons for upgrades, detached structures, and alternative energy sources commonly found in custom units.

- Farmers Insurance is known for flexibility in underwriting, making it a strong option for homeowners who have made extensive modifications or used unique materials in their builds.

Key Coverage Features to Look for in a Policy

When selecting an insurance provider for a custom-built manufactured home, it’s essential to look beyond brand recognition and evaluate the specifics of coverage.

Standard policies may not account for high-end finishes, custom installations, or energy-efficient upgrades, which can significantly affect rebuild costs. The best providers offer extended replacement cost coverage, which pays more than the policy limit if construction prices rise unexpectedly.

They also include protection for specialty items like custom cabinetry, solar panels, and upgraded plumbing or electrical systems. Additionally, liability coverage and medical payments to others should be sufficient to protect against lawsuits, and optional endorsements for flood or wind damage are critical depending on location.

- Extended replacement cost coverage ensures your home can be rebuilt to original specifications even if costs exceed the policy limit.

- Customization endorsements allow for inclusion of high-value upgrades such as hardwood floors, granite countertops, or smart home systems.

- Foundation and anchoring protection is crucial, especially for homes classified as personal property (not real estate), as proper installation affects risk assessment and premium rates.

Factors That Influence Insurance Rates for Custom Manufactured Homes

Insurance premiums for custom-built manufactured homes are influenced by several key factors, including the home’s age, construction quality, location, and how it’s titled (personal property vs. real estate). Homes on permanent foundations with HUD certification typically receive lower rates, while those in high-risk areas for tornadoes, wildfires, or floods cost more to insure.

The level of customization also plays a role—homes with premium materials or unique designs may require higher coverage limits, which increases the premium. Insurers also consider the homeowner’s claims history, credit score (in applicable states), and whether safety features like smoke detectors, security systems, or fire sprinklers are installed.

- Geographic location affects risk exposure; homes in coastal or storm-prone regions often require additional windstorm or flood policies.

- Title classification impacts premiums—manufactured homes deeded as real estate typically receive better rates due to perceived stability and permanence.

- Available discounts such as bundling with auto insurance, having a claims-free history, or installing protective devices can significantly reduce overall costs.

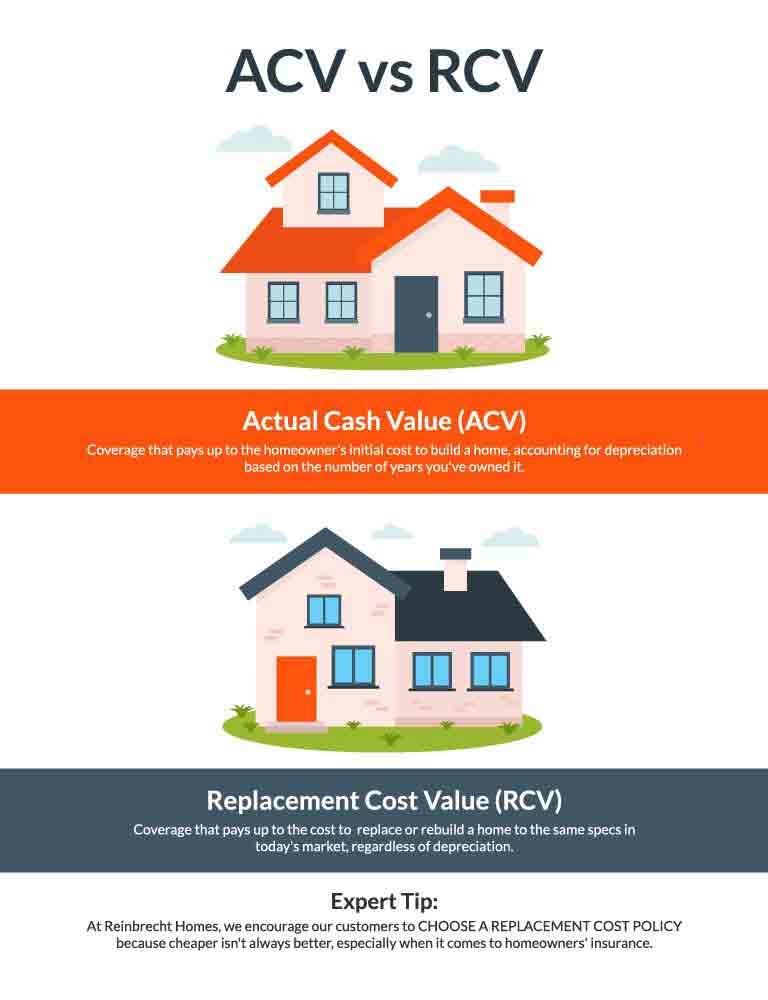

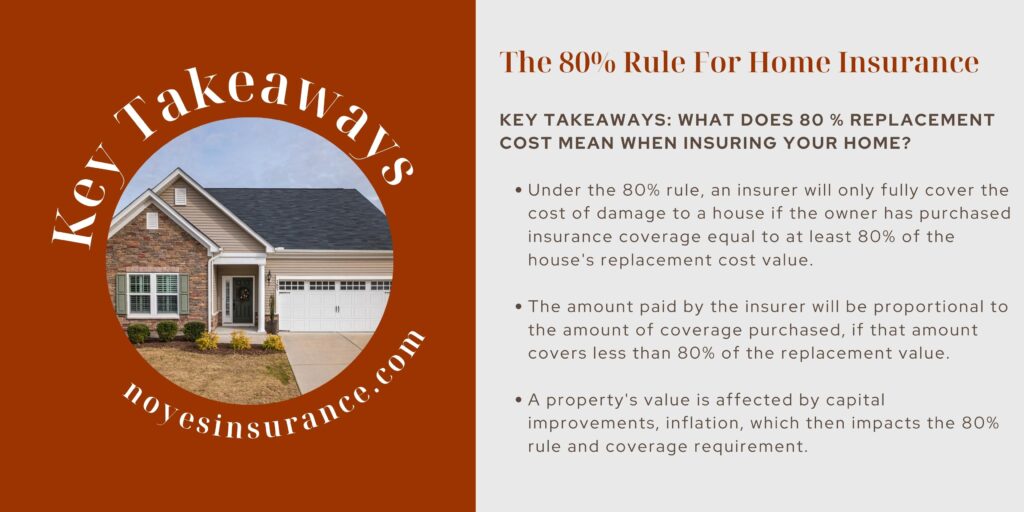

What does the 80% rule mean for insuring a custom-built home?

Understanding the 80% Rule in Home Insurance

- The 80% rule is a standard guideline used by insurance companies to determine the minimum amount of coverage a homeowner should carry to ensure full reimbursement for repair or replacement costs in the event of damage.

- This rule stipulates that to qualify for full replacement cost coverage, a homeowner must insure their property for at least 80% of its total rebuild cost, not the market value or purchase price.

- For a custom-built home, which often includes unique materials, high-end finishes, and specialized labor, accurately estimating the rebuild cost is critical. If the insured amount falls below 80% of this cost, the homeowner may be subject to coinsurance penalties and receive only a portion of the claim amount.

How the 80% Rule Affects Custom-Built Homes

- Custom-built homes typically have higher construction costs due to design complexity, premium materials, and location-specific factors, making compliance with the 80% rule more challenging and essential.

- If the home is insured for less than 80% of its replacement value, the insurance payout will be reduced proportionally. For example, if only 60% coverage is in place, the insurer might pay only 75% of the claim, leaving the homeowner responsible for the balance.

- Due to the personalized nature of custom homes, standard valuation tools may not capture true rebuild costs. Homeowners should obtain a professional appraisal or detailed reconstruction estimate to ensure they meet the 80% threshold and avoid underinsurance.

Steps to Ensure Compliance with the 80% Rule

- Begin by obtaining a current and accurate replacement cost evaluation from a qualified builder, contractor, or home appraisal service familiar with custom construction.

- Review your insurance policy annually, especially after renovations or upgrades, to confirm that the coverage limit still meets or exceeds 80% of the updated rebuild cost.

- Communicate regularly with your insurance provider to clarify how they calculate replacement cost and ensure your policy includes coverage for specialized elements such as custom cabinetry, imported fixtures, or architectural designs.

Frequently Asked Questions

What makes custom-built home insurance different from standard home insurance?

Custom-built home insurance is tailored to cover the unique materials, design, and construction process of a custom home. Unlike standard policies, it accounts for higher rebuild costs, specialty finishes, and potential delays during construction. It often includes guaranteed replacement cost coverage and protects against construction-specific risks like materials in transit or contractor errors, ensuring full financial protection throughout and after the build.

Does custom-built home insurance cover construction-phase risks?

Yes, many custom-built home insurance policies include coverage during the construction phase. This protects against risks such as theft of materials, vandalism, weather damage, or accidents on-site. Builder's risk insurance is often part of the package, covering the structure while under construction. It ensures financial protection from the foundation stage until the home is completed and occupied, bridging the gap between construction and traditional homeowners insurance.

How do insurers determine the cost of custom-built home insurance?

Insurers evaluate factors like construction materials, square footage, design complexity, location, and total rebuild cost. Unique features such as high-end finishes or smart home systems may increase value and risk. Location-based hazards like floods or wildfires also impact premiums. Accurate appraisals and detailed building plans help determine proper coverage limits, ensuring the policy aligns with the home’s actual cost to rebuild and maintain.

Can I get guaranteed replacement cost with custom-built home insurance?

Yes, most high-quality custom-built home insurance policies offer guaranteed replacement cost coverage. This means the insurer will pay whatever it costs to rebuild your home as designed, even if expenses exceed your policy limit. It’s essential for custom homes due to unpredictable material or labor cost increases. This protection ensures your investment is fully covered, regardless of future construction market fluctuations or unexpected rebuilding challenges.

Leave a Reply