Best insurance for historic homes 2025

Owning a historic home is a unique privilege, blending timeless charm with cultural significance. However, these distinguished properties demand specialized protection beyond standard homeowners insurance.

In 2025, the best insurance for historic homes offers tailored coverage that accounts for period-specific materials, intricate craftsmanship, and higher restoration costs. Policies now emphasize guaranteed replacement cost, ordinance or law coverage, and endorsements for original features.

As preservation regulations grow stricter, insurers are adapting with more flexible terms and expert assessments. Homeowners are increasingly seeking providers with experience in heritage properties, ensuring accurate valuation and respectful restoration. Choosing the right policy is essential to preserving history.

Rock hill second home insurance

Rock hill second home insuranceBest Insurance for Historic Homes 2025: Protecting Architectural Treasures

As we approach 2025, preserving the unique character and structural integrity of historic homes has become a top priority for homeowners and preservationists alike.

These properties, often over 50 years old and featuring original craftsmanship, antique materials, and distinct architectural styles, require specialized insurance solutions that go beyond standard home policies. The best insurance for historic homes in 2025 prioritizes agreed value coverage, restoration guarantees, and protection for period-specific materials that may no longer be commercially available.

Leading insurers now offer tailored policies in partnership with historic preservation societies, ensuring that repairs respect the home’s authenticity. With rising construction costs and climate-related risks, selecting a provider with expertise in heritage properties and flexible rebuilding terms is essential for long-term protection.

Why Standard Home Insurance Falls Short for Historic Properties

Standard homeowners insurance often fails to meet the unique needs of historic homes because it typically offers replacement cost coverage based on modern materials and methods, which can compromise the home’s authenticity during repairs.

Role of home safety measures in insurance

Role of home safety measures in insuranceIn contrast, many older homes feature hand-carved woodwork, plaster walls, original windows, and brick-laid fireplaces that are expensive or difficult to replicate. Policies designed for typical homes may not cover the cost of sourcing period-accurate materials or hiring specialized artisans trained in traditional techniques.

Moreover, standard policies may not account for extended rebuild timelines due to regulatory approvals from historic preservation boards. For these reasons, relying on conventional coverage can leave homeowners underinsured or forced to make historically inappropriate renovations.

Top Features of the Best Historic Home Insurance Policies in 2025

In 2025, the most comprehensive historic home insurance plans include agreed value coverage, eliminating disputes over appraisal after a loss since the insurer and homeowner pre-determine the home’s worth.

Additional critical features include ordinance or law coverage, which addresses higher repair costs due to modern building codes, and coverage for inherent defects, acknowledging that older homes may have original materials that predate current standards. Leading policies also offer extended rebuild provisions, allowing up to 150% of the policy limit if restoration costs unexpectedly rise.

State farm home insurance rate increase 2025

State farm home insurance rate increase 2025Insurers like Old Republic Home Insurance, Chubb Heritage, and AmFed Select stand out for including preservation consultant access, support for local historic society compliance, and reimbursement for archival documentation used in faithful restorations.

Comparing Leading Providers of Historic Home Insurance in 2025

When evaluating the best insurance providers for historic homes in 2025, several factors such as coverage scope, customer service expertise, and flexibility during claims distinguish industry leaders.

Companies like Chubb, Nationwide Heritage, and Liberty Mutual’s Classic Car & Home Insurance offer robust packages designed specifically for older and landmark properties. These insurers provide resources such as on-call restoration specialists, customized appraisal services, and inclusive coverage for detached historic structures like carriage houses or gazebos.

Regional carriers supported by state historic preservation offices are also gaining traction for their localized knowledge and faster claim resolution. Below is a comparison of key offerings from top providers in 2025.

Home insurance climate-related risks coverage

Home insurance climate-related risks coverage| Insurance Provider | Agreed Value Coverage | Ordinance & Law Coverage | Restoration Consultant Access | Max Extended Rebuild Percentage |

|---|---|---|---|---|

| Chubb Heritage | Yes – Full coverage up to $10M | Up to $500,000 included | Yes – 24/7 specialist hotline | 150% |

| Nationwide Heritage | Yes – Customized valuation process | Up to $250,000 | Yes – Assigned restoration advisor | 125% |

| Liberty Mutual Classic | Yes – With historical appraisal | Up to $200,000 | Limited – Referral network only | 120% |

| Old Republic Home Insurance | Yes – For designated landmark homes | Up to $1M (customizable) | Yes – In-house preservation team | 175% |

Best Insurance for Historic Homes in 2025: A Comprehensive Guide

What are the top property insurance options for historic homes in 2025?

Specialized Historic Home Insurance Providers

When insuring a historic home, standard property insurance policies often fall short because they don’t account for the unique construction methods, rare materials, and restoration requirements inherent in older properties.

Specialized insurers have emerged to address these specific needs, offering coverage tailored to the architectural and cultural value of historic homes. These companies typically employ adjusters and underwriters with expertise in period construction and preservation standards, ensuring accurate valuation and appropriate claim settlement.

- Eclipse Historical Insurance is a leading provider known for its comprehensive replacement cost coverage, which includes historically accurate materials like lime plaster, old-growth timber, and hand-cut stone, even if they are more expensive than modern equivalents.

- Old Republic Specialty Insurance offers customizable policies for homes listed on the National Register of Historic Places, with endorsements for ordinance or law coverage, which is critical when local preservation regulations affect repair or rebuild options.

- Chubb’s Historic Home Insurance program provides extended replacement cost coverage (often up to 150% of the dwelling’s appraised value) and includes protection for original architectural features such as wainscoting, staircase balustrades, and period hardware.

Key Coverage Features for Historic Properties

Insurance for historic homes must go beyond basic protection against fire or theft. Due to the age and craftsmanship involved, policies must address challenges such as sourcing authentic materials, compliance with preservation laws, and the labor-intensive nature of restoration work. The best policies in 2025 reflect an understanding that restoring a 19th-century Victorian or a Colonial-era farmhouse requires expertise and time, often exceeding the scope of conventional home insurance.

Home insurance companies columbus

Home insurance companies columbus- Guaranteed or extended replacement cost coverage ensures that even if reconstruction costs exceed the policy limit due to the scarcity of materials or artisan labor, the insurer will cover the full cost, preventing financial burden on the homeowner.

- Ordinance or law coverage is essential because many historic homes are subject to preservation regulations that may require specific restoration techniques or materials, increasing repair costs significantly after damage.

- Detached structures and site-specific features like period fencing, carriage houses, or historic landscaping are often included in comprehensive historic home policies, recognizing the full scope of a property’s historical value.

Differences Between Standard and Historic Home Policies

Understanding the distinction between a standard homeowners policy and one designed for a historic property is crucial for adequate protection.

Standard policies generally use replacement cost valuation based on modern construction methods and materials, which can severely undervalue a historic home's true restoration cost. In contrast, historic home insurance policies utilize appraisals from preservation experts and account for the specialized skills required for authentic restoration.

- Valuation methodology differs significantly; historic policies rely on agreed-upon value or functional replacement cost, where repairs use historically appropriate techniques rather than modern substitutes, even if more costly.

- Standard policies often exclude coverage for deterioration due to age—a common issue in older homes—whereas historic-specific policies may provide coverage for concealed damage discovered during authorized restoration work.

- Claims processing in historic home insurance usually involves preservation consultants to verify that repairs align with historical accuracy, ensuring compliance with heritage standards and avoiding coverage disputes during restoration.

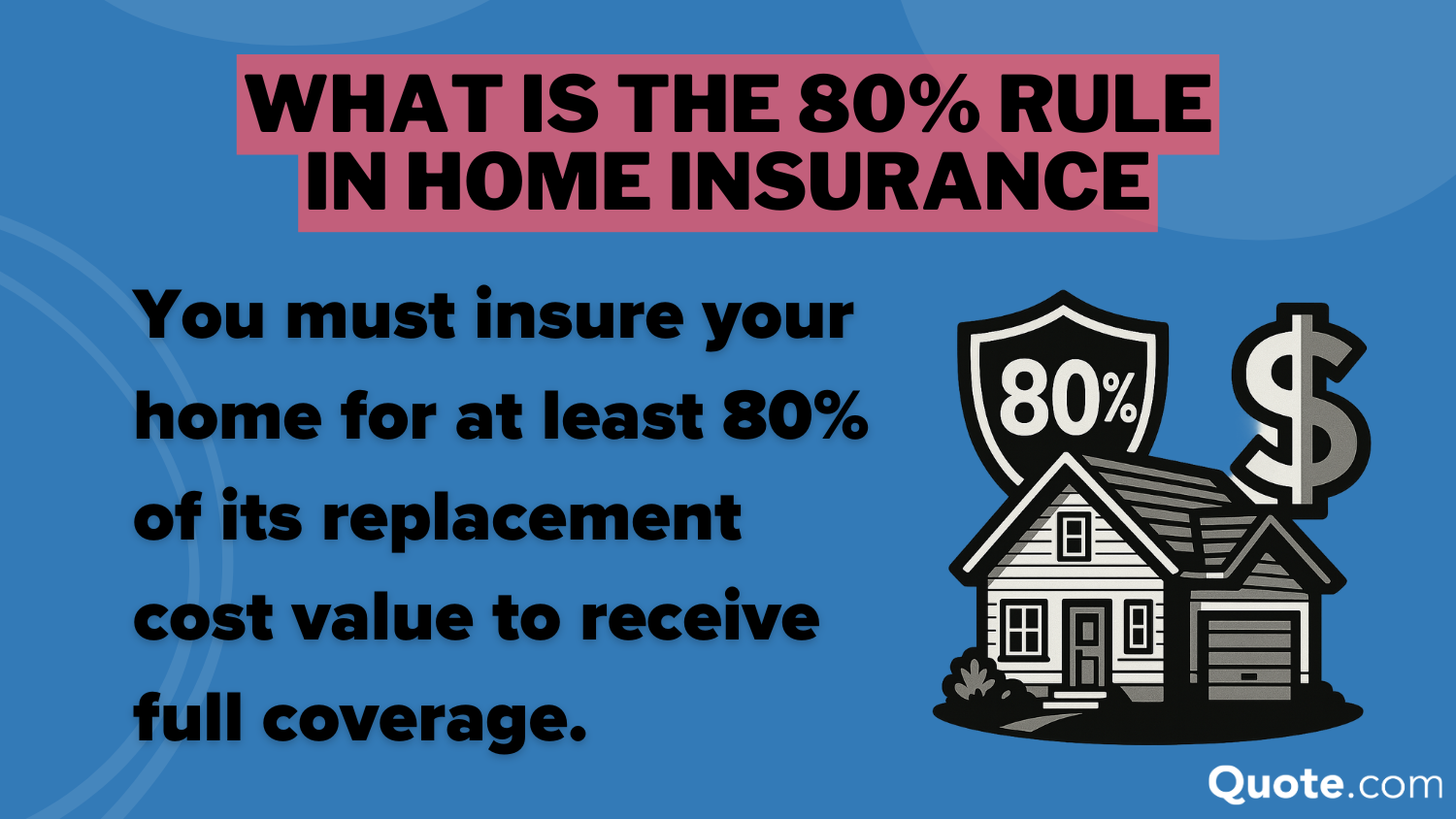

What is the 80% rule in home insurance for historic properties in 2025?

Definition and Application of the 80% Rule in Home Insurance

- The 80% rule in home insurance stipulates that homeowners must carry coverage equal to at least 80% of their home’s replacement cost to qualify for full reimbursement in the event of a partial loss. If the insured amount falls below this threshold, the insurance company may apply a coinsurance penalty, meaning the homeowner would receive only a proportionate share of the claim payout based on how much coverage they carry relative to the required amount.

- For historic properties in 2025, applying the 80% rule becomes more complex due to unique architectural materials, craftsmanship, and restoration costs. Unlike standard homes, the replacement value of historic homes often includes custom masonry, antique woodwork, or period-specific fixtures, all of which can significantly increase repair costs compared to modern construction practices.

- Insurance providers may require detailed appraisals or replacement cost evaluations specific to historic buildings to determine if the policy meets the 80% standard. In some cases, specialized insurance policies, such as those offered through heritage preservation programs or endorsed by historical societies, account for these nuances and help ensure compliance with the rule while covering restoration authenticity.

Risks of Not Meeting the 80% Coverage Threshold for Historic Homes

- One major risk of falling short of the 80% rule is underinsurance, where the policyholder may be responsible for a substantial portion of repair costs after damage. For instance, if a historic home with a $1 million replacement value carries only $600,000 in coverage (60%), the insurer might cover only 75% of a $100,000 claim, leaving the homeowner with a $25,000 out-of-pocket expense.

- Historic properties often face extended repair timelines due to limited availability of skilled artisans and bespoke materials. Without sufficient coverage, owners may delay or compromise on restoration quality, potentially violating preservation standards or losing eligibility for tax incentives and grants tied to historic status.

- Additionally, increased frequency of extreme weather events in 2025 amplifies exposure for older structures not originally built to modern resilience standards. A failure to meet the 80% rule could result in disproportionately high financial strain after events like severe storms or flooding, especially if special endorsements for flood or earthquake damage are not included alongside standard coverage.

Strategies to Comply with the 80% Rule for Historic Property Insurance

- Homeowners should obtain a professional appraisal that reflects the true replacement cost of their historic property, including estimates for maintaining historical accuracy in materials and workmanship. This appraisal should be updated periodically—ideally every three to five years or after major renovations—to reflect inflation and labor market changes in specialty trades.

- Purchasing an agreed value policy, where the insurer and homeowner pre-determine the coverage amount and waive the 80% rule, can be an effective alternative for qualifying historic homes. This option eliminates the risk of coinsurance penalties but often comes with higher premiums and stricter underwriting requirements.

- Engaging with insurers who specialize in historic or heritage properties is also critical. These companies typically offer tailored policies that include coverage for reconstruction using original methods and materials, temporary relocation during repairs, and even architectural consulting services to ensure compliance with local preservation ordinances, all contributing to a more accurate and sufficient insurance valuation.

What is the best home insurance for seniors owning historic homes in 2025?

Specialized Insurance Providers for Historic Homes

- Insurance carriers such as Erie Insurance and Amica Mutual are increasingly recognized in 2025 for offering customized coverage options suitable for historic homes, particularly through endorsements that cover period-specific materials and craftsmanship.

- Companies like Lexington Insurance, a subsidiary of American International Group (AIG), specialize in high-value and unique properties, providing flexible policies that account for the restoration costs and architectural significance of older homes.

- Seniors benefit from providers that partner with preservation societies, such as the National Trust for Historic Preservation, which may offer group discounts and access to contractors experienced in heritage restoration.

Coverage Features Tailored to Senior Homeowners

-

- Look for policies that include guaranteed replacement cost coverage, ensuring that in the event of damage, rebuilding with historically accurate materials is fully covered, even if costs exceed the policy limit.

- Many insurers in 2025 now offer age-friendly features such as waiving inflation guard clauses for seniors on fixed incomes, simplifying premium stability over time.

<3>Additional living expense (ALE) coverage is especially important, as restoration of a historic property may take longer than standard rebuilds, requiring extended temporary housing support.

- Insurers evaluate the home’s condition, location, and any previous restorations; seniors who have invested in preventive maintenance or installed discreet modern safety systems (e.g., hidden fire suppression) may receive premium reductions.

- Many companies offer senior-specific discounts, particularly for those aged 55 and over, which can be combined with loyalty programs or bundling home and auto policies.

- The proximity to fire stations, updated electrical and plumbing systems, and the use of fire-resistant roofing materials can significantly reduce risk profiles, leading to more favorable insurance quotes for older homeowners.

Are historic homes more costly to insure in 2025?

Factors That Increase Insurance Costs for Historic Homes

- One of the primary reasons historic homes tend to be more costly to insure is the specialized nature of their construction. Many of these properties were built using materials and techniques that are no longer standard, making repairs more complex and often requiring skilled artisans or custom materials.

- Another contributing factor is the increased replacement cost. Due to unique architectural elements such as hand-carved wood, original plasterwork, or antique fixtures, rebuilding or restoring a historic home after damage can be significantly more expensive than typical modern homes.

- Additionally, many historic homes lack modern safety features such as updated electrical systems, fire suppression systems, or reinforced plumbing. These outdated systems increase the risk of fire, water damage, or other hazards, prompting insurers to adjust premiums upward to account for higher potential claims.

- The geographic location of a historic home plays a crucial role in determining insurance costs. Homes situated in areas prone to natural disasters—such as hurricanes, floods, or wildfires—will naturally face higher premiums, especially if restoration after such events must comply with strict preservation standards.

- Local and national historic preservation regulations often impose restrictions on renovations or repairs, requiring property owners to use specific materials or methods that maintain historical authenticity. These requirements can extend repair timelines and increase costs, which insurers take into account when calculating coverage.

- Some historic districts are governed by commissions that must approve even minor changes to a property. This bureaucratic layer can delay repairs after a loss, and insurers may view this as an increased exposure, leading to higher premiums to offset the added risk and complexity.

Specialized Insurance Policies and Market Trends in 2025

- In 2025, more insurers are offering specialized coverage for historic properties, known as agreed value or guaranteed replacement cost policies. These policies aim to cover the full cost of restoration using authentic materials and craftsmanship, which typically results in higher premiums compared to standard homeowners’ insurance.

- The rising cost of construction materials and labor shortages continue to influence insurance pricing. For historic homes, which already demand premium labor and rare materials, these market conditions amplify the cost of both repairs and insurance coverage.

- As climate change increases the frequency and severity of extreme weather events, insurers are reevaluating risk models across all property types. Historic homes, often less resilient to such events due to age and structure, are facing upward pressure on rates as insurers adjust to evolving environmental risks.

Frequently Asked Questions

What makes insurance for historic homes different from standard home insurance?

Historic homes require specialized insurance due to their unique architecture, age, and restoration materials. Standard policies often undervalue these factors, while historic home insurance covers replacement costs with period-appropriate materials and skilled labor. It also includes broader protection for structural features and often provides coverage even if the home is vacant, which is essential for properties awaiting restoration or in transitional ownership.

Which insurers are considered the best for historic homes in 2025?

In 2025, top insurers for historic homes include Amica, PURE Insurance, Erie Insurance, and Chubb. These companies offer policies tailored to older, high-value homes, with features like guaranteed replacement cost, no depreciation deduction for original features, and expert restoration guidance. They also provide high coverage limits and personalized service, which are crucial for preserving the authenticity and value of historic properties.

Does historic home insurance cover restoration and preservation costs?

Yes, the best historic home insurance policies cover restoration and preservation using traditional materials and craftsmanship. These policies typically include guaranteed or extended replacement cost coverage to account for higher restoration expenses. Some insurers partner with preservation experts and offer access to networks of certified contractors. This ensures repairs maintain historical accuracy, even if costs exceed standard construction prices due to specialized labor and materials.

Are there special requirements to qualify for historic home insurance?

Yes, insurers usually require a home appraisal, detailed documentation of historical features, and proof of proper maintenance. Some policies may need the home to be listed on a historic register or meet specific age criteria. Insurers also evaluate security, location, and renovation history. Maintaining the home’s original integrity while ensuring modern safety standards can improve eligibility and help secure favorable premium rates on a specialized historic home policy.

Leave a Reply