Cheap home insurance in michigan

Finding affordable home insurance in Michigan doesn’t have to be a challenge. With rising property values and varying weather risks across the state, securing low-cost coverage requires smart shopping and understanding local market trends.

Numerous providers offer competitive rates, especially in cities with lower crime rates and reliable infrastructure. Homeowners can reduce premiums by bundling policies, improving home security, and maintaining a strong credit score.

Additionally, Michigan’s unique no-fault insurance system impacts overall costs. This guide explores practical strategies to help Michigan residents find cheap home insurance without sacrificing essential coverage or peace of mind.

Evaluate The Insurance Company Metlife On Term Life Insurance

Evaluate The Insurance Company Metlife On Term Life InsuranceFinding Affordable Home Insurance in Michigan: Top Tips and Options

Securing cheap home insurance in Michigan doesn’t mean compromising protection. Many homeowners can significantly reduce their premiums by shopping around, improving home safety, and bundling policies.

Insurance rates in Michigan vary widely based on location, home age, credit score, and claim history. By understanding the factors that influence pricing and leveraging available discounts, residents can find affordable coverage that still provides comprehensive protection against damage, theft, and liability. C

omparing quotes from multiple insurers is essential, as premiums for the same level of coverage can differ by hundreds of dollars between providers. Additionally, maintaining a good credit score and installing security systems like smoke detectors and monitored alarms may qualify you for further reductions.

Factors That Influence Home Insurance Rates in Michigan

Several key factors affect how much you pay for home insurance in Michigan. Location plays a major role—homes in areas prone to severe weather or high crime rates typically face higher premiums.

Evaluate The Life Insurance Company Selectquote On Simple Life Insurance

Evaluate The Life Insurance Company Selectquote On Simple Life InsuranceThe age and construction type of your home also impact cost, with older homes often requiring more coverage due to outdated electrical or plumbing systems. Insurers also look at your credit-based insurance score, claims history, and whether you’ve had lapses in coverage.

Adding safety and security features—such as storm shutters, fire alarms, and smart security systems—can lead to discounts. Moreover, increasing your deductible can lower your monthly premium, though it means paying more out-of-pocket in the event of a claim.

Top Insurance Providers Offering Low-Cost Home Coverage in Michigan

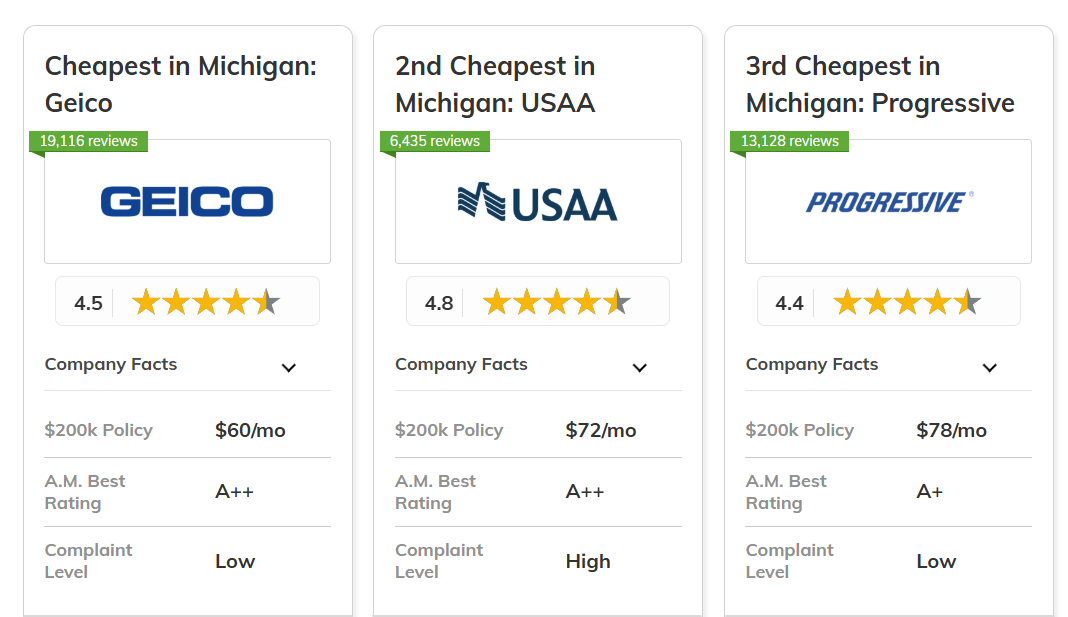

Many national and regional insurers offer competitive rates for cheap home insurance in Michigan. Companies like State Farm, Farm Bureau Insurance, Allstate, and Nationwide frequently rank high for affordability and customer satisfaction in the state.

Farm Bureau, in particular, is known for offering strong discounts to Michigan residents, including multi-policy and home claim-free incentives. Smaller regional carriers may also provide cost-effective options tailored to local risk factors.

Evaluate The Progressive Insurance Company Hiscox On Ap Life

Evaluate The Progressive Insurance Company Hiscox On Ap LifeOnline comparison tools make it easier to evaluate coverage limits, deductibles, and additional benefits like replacement cost coverage. Always verify an insurer’s financial strength and customer service reputation before committing to a policy.

Homeowners in Michigan can access multiple discounts to reduce their home insurance costs. One of the most common is the multi-policy discount, offered when you bundle home and auto insurance with the same provider.

Installing safety features such as deadbolts, smoke detectors, and security systems can also slash premiums. Many insurers reward customers for being claims-free, maintaining a good credit score, or being a long-term policyholder.

Seniors and new homeowners may qualify for specialized discounts. Additionally, paying your annual premium upfront instead of in monthly installments can result in savings. Always ask your provider about all available discounts to ensure you're getting the best possible rate.

I'm 26 Can I Get Lower Rate Term Life Insurance

I'm 26 Can I Get Lower Rate Term Life Insurance| Insurance Company | Estimated Annual Premium (MI Average) | Key Discounts Offered |

|---|---|---|

| Farm Bureau Insurance | $950 | Multi-policy, claims-free, home safety, loyal customer |

| State Farm | $1,020 | Bundling, paperless billing, auto-pay, home security |

| Allstate | $1,100 | Protective device discount, new home, loyalty, bundling |

| Nationwide | $1,080 | Multi-home, claims-free, paperless, automatic payments |

| Liberty Mutual | $1,250 | Home and auto bundle, new customer, safety features |

How to Find Affordable Home Insurance in Michigan: A Comprehensive Guide

What is the average cost of affordable home insurance in Michigan?

The average cost of affordable home insurance in Michigan varies depending on several factors, including location, home value, coverage levels, and the insurance provider. As of the latest data, the average annual premium for homeowners insurance in Michigan ranges from $1,500 to $2,200.

This places Michigan above the national average, which is often attributed to specific state regulations, weather risks, and property crime rates in certain areas. Affordable policies can often be found by comparing quotes from multiple insurers, taking advantage of discounts, and adjusting deductibles or coverage limits based on individual needs.

Factors That Influence Home Insurance Costs in Michigan

- Location plays a significant role in determining insurance premiums. Homes in areas prone to severe weather, such as thunderstorms or snowstorms, might incur higher rates due to increased risk of damage.

- The age and construction of the home also affect pricing. Older homes with outdated electrical or plumbing systems may be more expensive to insure compared to newer, code-compliant structures built with modern materials.

- Crime rates in the neighborhood influence premiums as well. Homes in areas with higher burglary or vandalism rates typically face higher insurance costs due to greater risk exposure.

How to Find Affordable Home Insurance Options

- Shopping around and comparing quotes from at least three to five different insurers can reveal substantial differences in pricing and coverage options, helping homeowners identify the most cost-effective plan.

- Taking advantage of available discounts—such as bundling home and auto insurance, installing security systems, or holding a claims-free record—can reduce annual premiums by 10% to 25%.

- Adjusting coverage limits and increasing deductibles may lower monthly or annual payments, though homeowners should ensure they maintain sufficient protection for potential losses.

State-Specific Considerations for Michigan Homeowners

- Michigan has unique insurance regulations, including no-fault auto insurance laws that can indirectly impact home insurance, especially for bundled policies offered by the same provider.

- Some insurers may factor in the risk of water backup or sump pump overflow, which are common in areas with high water tables; adding or removing this endorsement affects the overall premium.

- Urban areas like Detroit often have higher premiums due to increased risks related to property crime and fire, while rural or suburban areas might offer more affordable rates depending on local infrastructure and emergency response availability.

What is the cheapest home insurance provider in Michigan?

Why Life Insurance Policy Show Guaranteed Assumptions And Non Guaranteed

Why Life Insurance Policy Show Guaranteed Assumptions And Non GuaranteedThe cheapest home insurance provider in Michigan can vary depending on individual circumstances such as location, home value, credit score, and claims history.

However, based on recent industry data and comparisons from sources like NerdWallet, Bankrate, and Insurify, Farmers Insurance often ranks among the most affordable options for standard homeowners insurance in Michigan. Other competitively priced providers include State Farm and Allstate, especially for customers who qualify for multiple policy discounts or loyalty programs.

It's essential to note that while Farmers may offer lower base premiums, individual rates can differ significantly. Therefore, obtaining personalized quotes from multiple carriers is the most effective way to identify the lowest rate for your specific needs.

Factors That Influence Home Insurance Rates in Michigan

- Location within Michigan plays a critical role in determining premiums. Homes in areas prone to severe weather, such as thunderstorms or flooding in regions near the Great Lakes, typically face higher rates due to increased risk of damage.

- Credit history is another major factor insurers consider. In Michigan, companies like Farmers and State Farm use credit-based insurance scores to help assess risk, meaning applicants with higher scores often qualify for lower premiums.

- The age and condition of a home also influence pricing. Older homes with outdated electrical or plumbing systems may cost more to insure, whereas newer constructions or updated properties with safety features like security systems or storm shelters might qualify for discounts.

Top Low-Cost Providers Compared in Michigan

- Farmers Insurance frequently appears as one of the lowest-cost providers in statewide comparisons, particularly for homeowners without recent claims. Their pricing is competitive for both basic and comprehensive coverage, and they offer bundling options with auto insurance that can further reduce costs.

- State Farm, while not always the cheapest, often provides stable and affordable rates, especially for long-term customers. Their local agents allow for personalized service, and they have a strong presence across Michigan, contributing to high customer satisfaction and reliable claims handling.

- Allstate is another contender for affordability, particularly for customers who take advantage of protective device discounts or enroll in usage-based programs like Drivewise when bundling with auto policies. Though rates can be higher for high-risk profiles, average premiums remain competitive.

Ways to Reduce Your Home Insurance Costs in Michigan

- Bundling home and auto insurance policies with the same provider, commonly offered by companies like Allstate and State Farm, can yield savings of up to 25%. This is one of the most accessible and widely available discounts across insurers in the state.

- Improving home security can lead to premium reductions. Installing deadbolt locks, smoke detectors, burglar alarms, or monitored security systems may qualify you for discounts from insurers such as Farmers and Nationwide.

- Maintaining a good credit score and a claims-free history over several years will make you eligible for loyalty discounts and lower risk classifications. Some insurers review these factors annually and may automatically adjust premiums downward for consistent, responsible customers.

What is the most affordable home insurance provider in Michigan?

Top Affordable Home Insurance Providers in Michigan

When evaluating the most affordable home insurance providers in Michigan, several companies consistently rank high in terms of competitive pricing and reliable coverage.

Based on recent rate comparisons and customer data, companies like Frankenmuth Insurance, Farm Bureau Insurance, and Auto-Owners Insurance are frequently cited as offering some of the lowest premiums in the state.

Frankenmuth, a Michigan-based insurer, is particularly notable for its regional focus and deep understanding of local property risks, which allows it to offer tailored and cost-effective policies. These insurers tend to provide significant discounts for bundling home and auto insurance, maintaining claim-free records, and installing home safety features.

- Frankenmuth Insurance is often ranked among the cheapest due to its strong regional presence and customer loyalty programs.

- Farm Bureau Insurance offers low rates especially for residents in rural areas and those with long-term policies.

- Auto-Owners Insurance provides competitive pricing combined with high customer satisfaction ratings and multiple discount opportunities.

Factors That Influence Home Insurance Rates in Michigan

The cost of home insurance in Michigan is determined by a combination of personal, property-specific, and regional factors. Insurers assess the age and construction type of the home, its location, claims history, and proximity to fire stations and hydrants. Additionally, credit-based insurance scores play a significant role in pricing across the state, with better scores typically leading to lower premiums.

Weather-related risks such as severe storms and freezing temperatures also impact rates, especially in regions prone to water damage from frozen pipes. Policyholders can often reduce their costs by increasing their deductible, improving home security, or joining affinity groups that qualify for discounts.

- The location of the home within Michigan—urban, suburban, or rural—impacts both risk exposure and insurance pricing.

- Home characteristics such as roof age, square footage, and building materials affect underwriting decisions and premiums.

- Insurance providers use credit history as a predictive factor for claims likelihood, influencing rate eligibility.

How to Find the Cheapest Home Insurance Policy in Michigan

To secure the most affordable home insurance policy in Michigan, it's essential to shop around and compare quotes from multiple insurers.

Online comparison tools and independent insurance agents can help gather accurate and comprehensive pricing data tailored to your specific home and needs. It's also important to review available discounts such as multi-policy bundling, automatic payment, or new home credits.

Maintaining a strong credit score and a claim-free history can further reduce rates over time. Regularly re-evaluating your policy ensures you're not paying for excess coverage and allows you to take advantage of better market offers.

- Obtain at least three personalized quotes from top insurers to establish a reliable price baseline.

- Ask about all available discounts, including those for security systems, retirement status, or home renovations.

- Work with an independent agent who can access multiple carriers and find niche or regional providers with lower rates.

Frequently Asked Questions

What factors affect the cost of cheap home insurance in Michigan?

The cost of affordable home insurance in Michigan depends on several factors, including your home’s location, age, and construction type. Credit score, claims history, and coverage limits also play a role. Areas prone to severe weather or higher crime rates may see increased premiums. Installing safety features like smoke detectors or security systems can lower costs. Shopping around and comparing quotes helps find the most competitively priced, reliable coverage for your specific situation.

How can I find the cheapest home insurance provider in Michigan?

To find the cheapest home insurance in Michigan, compare quotes from multiple reputable insurers online. Check customer reviews, financial strength ratings, and available discounts. Consider bundling home and auto insurance for extra savings. Ask about discounts for safety upgrades, claims-free history, or paying in full. Using an independent insurance agent can help identify cost-effective options. Always verify that low-cost policies still offer adequate coverage and strong customer support for claims.

Does Michigan law require homeowners to have home insurance?

Michigan state law does not legally require homeowners to carry home insurance. However, if you have a mortgage, your lender will likely require insurance as a condition of the loan. Even without a mortgage, insurance protects your investment from unexpected damages like fire, theft, or storms. Skipping coverage could lead to significant out-of-pocket costs. It's wise to have a policy, regardless of legal requirements, to ensure financial security and peace of mind.

What coverage is included in cheap home insurance policies in Michigan?

Affordable home insurance in Michigan typically includes dwelling coverage, personal property protection, liability insurance, and additional living expenses. While lower-cost policies meet basic needs, they may have lower coverage limits or higher deductibles. Always review what perils are covered—like fire, wind, or vandalism—and consider adding endorsements for earthquakes or water backup. Ensure the policy provides sufficient protection for your home’s value and risk factors.

Leave a Reply