Common Complaints In Auto Insurance Reviews

Many auto insurance customers express recurring concerns in online reviews, highlighting issues that span claims processing, customer service, and pricing transparency. Delays in claim settlements, poor communication, and unexpected premium increases are among the most frequent complaints. Policyholders often report frustration when representatives are unresponsive or lack clarity during critical moments. Additionally, confusion over coverage details and dissatisfaction with adjuster assessments contribute to negative feedback. While some insurers excel in digital tools and convenience, others fall short in delivering consistent support. These complaints underscore the importance of choosing a provider not only for affordability but also for reliability and customer care throughout the policy lifecycle.

Common Complaints in Auto Insurance Reviews: What Policyholders Are Saying

Auto insurance is a necessity for most drivers, yet it remains a frequent source of frustration due to recurring issues reported in customer reviews. Many policyholders express dissatisfaction not at the moment of purchase but when they interact with their insurer during critical moments—such as filing a claim, receiving a surprising rate increase, or attempting to reach customer service. These complaints often revolve around perceived delays, lack of transparency, and inconsistent communication, which together contribute to negative user experiences. Common themes include claim denials or undervaluation, poor responsiveness during emergencies, and misleading marketing that doesn’t align with actual policy terms. Understanding these widespread grievances can help consumers make more informed decisions and set realistic expectations when choosing an auto insurance provider.

Delayed or Denied Claims Processing

One of the most frequently cited issues in auto insurance reviews is the delayed processing of claims or outright denials, which can cause significant stress for policyholders involved in accidents. Customers often report waiting several days—or even weeks—for an adjuster to inspect damages, delaying essential repairs and disrupting daily transportation. Even more frustrating are claim denials based on technicalities, such as alleged missed payments or disputes over fault determination, which some consumers feel are unfairly applied. In some cases, insurers may undervalue repair costs, pressuring customers to accept lower settlements than needed to restore their vehicles. These experiences erode trust and highlight the importance of fully understanding policy exclusions and claims procedures before an incident occurs.

Best apps for organizing home insurance documents for families

Best apps for organizing home insurance documents for families| Complaint Type | Common Reasons Cited | Customer Impact |

|---|---|---|

| Delayed Claims | Understaffed claims departments, backlog during peak seasons, inefficient communication | Extended vehicle downtime, increased out-of-pocket expenses |

| Denied Claims | Policy exclusions, disputed fault, late reporting | Full financial responsibility for repairs or medical bills |

| Low Settlement Offers | Depreciation deductions, use of aftermarket parts, minimal total loss evaluations | Insufficient funds to cover actual repair or replacement costs |

Lack of Customer Service Responsiveness

Another widespread complaint highlighted in auto insurance reviews is the lack of timely and effective customer service. Many policyholders struggle to reach a live agent via phone, experience long hold times, or receive generic automated responses when seeking assistance. This lack of accessibility becomes especially problematic during emergencies or after accidents when immediate guidance is crucial. Some customers report being transferred multiple times without resolution, while others note inconsistent information provided by different representatives. The growing reliance on digital platforms has also led to frustrations when online portals are difficult to navigate or fail to support key functions like uploading documents or tracking claim status. As a result, responsive and knowledgeable support is often seen as a distinguishing factor between satisfactory and poor insurance experiences.

A significant number of reviews cite unexpected premium increases and the presence of hidden fees as major sources of dissatisfaction with auto insurance providers. Customers frequently report receiving renewal notices with substantial rate hikes—sometimes doubling their monthly payments—without a clear explanation or prior warning. These increases are often attributed to factors such as algorithm-based risk assessments, changes in credit score, or adjustments in coverage tiers that were not adequately communicated. Additionally, some insurers introduce administrative fees, policy issuance charges, or cancellation penalties that were not disclosed during the initial sign-up process. Such practices lead to feelings of being misled and undermine trust, prompting many consumers to seek more transparent alternatives.

Common Complaints in Auto Insurance Reviews: A Detailed Guide

Top Auto Insurance Providers with the Lowest Complaint Index

According to data from the National Association of Insurance Commissioners (NAIC), USAA consistently ranks as one of the auto insurance providers with the fewest customer complaints relative to the size of its customer base. The NAIC calculates a Complaint Index that compares the number of complaints received about a company to the average number expected for companies of similar size. A score below 1.0 indicates fewer complaints than average. USAA frequently reports an index well below 1.0, often around 0.25 to 0.35, which demonstrates exceptional customer satisfaction and efficient claims handling. Other insurers with low complaint indexes include Amica Mutual and Erie Insurance, both of which emphasize customer service and localized operations. These companies typically maintain strong financial ratings and invest heavily in customer support systems.

Best digital solutions for home insurance renewal reminders

Best digital solutions for home insurance renewal reminders- USAA serves military members, veterans, and their families and has long been recognized for high customer satisfaction due to personalized service and streamlined digital tools.

- Amica Mutual operates on a mutual ownership model, meaning it is owned by policyholders, which aligns its priorities with customer satisfaction rather than shareholder profits.

- Erie Insurance combines regional focus with strong agent relationships, contributing to lower complaint volumes and high retention rates.

How the NAIC Complaint Index Measures Customer Satisfaction

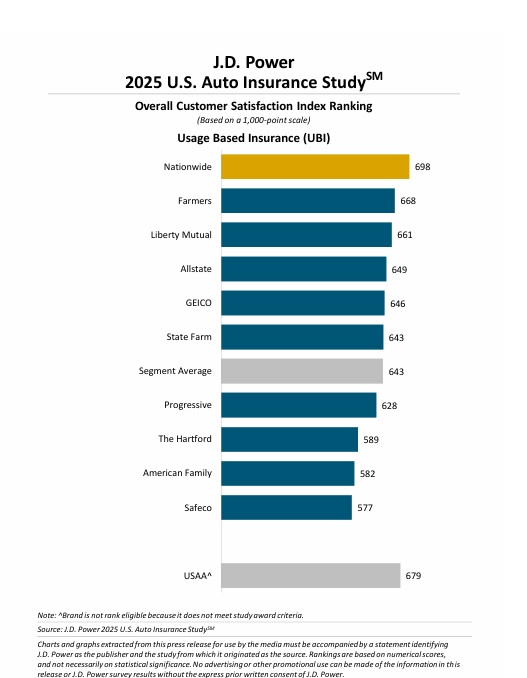

The NAIC Complaint Index is one of the most reliable metrics for assessing customer satisfaction across insurance providers. This index aggregates formal complaints submitted by consumers to state insurance departments and normalizes the data based on the insurer’s market share. For example, a company with a high number of policies would naturally receive more complaints, so the index adjusts for scale. A rating of 1.0 represents the industry average; anything below that suggests the company receives fewer complaints than expected. Insurers like USAA and Amica regularly achieve scores significantly below 1.0, indicating superior performance in resolving claims, handling billing issues, and offering responsive customer service. Independent studies and consumer surveys, such as those from J.D. Power, often corroborate these findings.

- The NAIC gathers data from all 50 states and compiles annual reports that are publicly accessible, allowing consumers to compare insurers objectively.

- Complaint categories include claims denial disputes, premium billing errors, communication lapses, and policy coverage misunderstandings.

- Insurers with transparent policies, fast claims processing, and accessible support teams typically score better on the index.

Factors Contributing to Low Complaint Rates in Auto Insurance

Several operational and strategic elements contribute to why certain auto insurers receive fewer customer complaints. First, companies with strong digital platforms allow customers to file claims, manage policies, and communicate with agents seamlessly, reducing frustration. Second, proactive customer service—such as automated claim updates and personalized outreach—helps prevent issues from escalating into formal complaints. Third, transparency in pricing, clear policy language, and fair claims settlements build long-term trust. Additionally, insurers that train agents extensively and maintain consistent underwriting standards minimize errors and misunderstandings that often lead to dissatisfaction. These factors collectively explain why USAA, Amica, and Erie stand out in industry rankings.

- Investment in user-friendly mobile apps and online portals reduces delays and enhances the overall customer experience.

- Use of data analytics enables faster claim assessments and reduces the likelihood of disputes over payout amounts.

- Focus on policyholder education—through newsletters, FAQs, and proactive alerts—helps customers understand coverage limits and claims procedures.

Frequently Asked Questions

Why do customers complain about slow claims processing in auto insurance?

Customers often complain about slow claims processing due to understaffed claims departments, required documentation delays, and internal review procedures. Insurers may also take extra time to investigate accidents thoroughly, especially when liability is unclear. While some delays are unavoidable, inefficient communication and outdated systems can worsen the problem, leading to customer frustration and negative reviews about responsiveness and service speed.

What causes dissatisfaction with customer service in auto insurance reviews?

Dissatisfaction with customer service often stems from long hold times, unresponsive agents, and difficulty reaching a live representative. Customers also report inconsistent information from support staff and lack of follow-up on inquiries. Poor training, high agent turnover, and inadequate support channels contribute to these issues. When policyholders feel ignored or misinformed during critical moments like accidents or billing disputes, negative reviews about customer service become more likely.

Best home insurance north carolina

Best home insurance north carolinaPolicyholders frequently complain about unexpected premium hikes, even without filing claims. These increases may result from broader market trends, rising repair costs, or company-wide rate adjustments. Insurers may also reassess risk based on location, driving behavior, or credit score changes. Lack of transparency about the reasons behind rate increases often fuels frustration, leading customers to feel misled or unfairly treated, especially if they've maintained safe driving records.

How do claim denials become a common complaint in auto insurance reviews?

Claim denials are a frequent source of complaints, especially when customers believe their claim was valid. Insurers may deny claims due to policy exclusions, lapses in coverage, or insufficient evidence. Some customers feel the terms were unclear or misunderstood when purchasing the policy. A denial without clear explanation or appeal options can lead to distrust. Feeling wronged after paying premiums for years amplifies frustration and results in negative reviews.

Best home owners insurance company for codos

Best home owners insurance company for codos

Leave a Reply