Does Personal Auto Insurance Cover Turo Rental

Personal auto insurance coverage for Turo rentals is a topic of growing concern among drivers considering short-term car sharing.

While some personal policies may extend limited coverage to vehicles rented through peer-to-peer platforms like Turo, the extent of protection varies widely among insurers and specific policy terms. In many cases, personal insurance may not cover damages, liability, or theft occurring during a Turo rental, leaving drivers exposed to significant out-of-pocket costs.

Turo provides its own insurance options, but understanding how they interact with existing personal policies is crucial. Drivers must carefully review both their insurance policy and Turo’s coverage to avoid gaps and ensure adequate protection.

Best digital solutions for home insurance renewal reminders

Best digital solutions for home insurance renewal remindersDoes Personal Auto Insurance Cover Turo Rentals?

When considering using a personal auto insurance policy to cover a Turo rental, many drivers are left uncertain about what protections actually apply.

In most cases, personal auto insurance policies do not fully cover vehicle usage in peer-to-peer car-sharing platforms like Turo. While some policies may extend limited liability or uninsured motorist coverage, they often explicitly exclude coverage for any commercial or livery service, which includes renting out a vehicle through an app-based service.

Major insurers, such as State Farm, GEICO, and Allstate, typically state in their policy documents that using a personal vehicle for Turo constitutes a commercial use, thus voiding standard coverage. As a result, drivers need to understand that relying solely on personal insurance during a Turo transaction can leave them financially exposed in the event of an accident.

How Turo’s Built-in Insurance Options Work

Turo offers its own protection plans to cover both hosts (car owners) and guests (renters), which activate when a trip is confirmed.

Best home insurance north carolina

Best home insurance north carolinaThese plans—ranging from Liability Only to Premium Protection—include varying levels of liability coverage, collision protection, and roadside assistance. For example, the Premium Protection plan typically reduces or eliminates the guest’s financial responsibility for damage to the host’s vehicle, subject to the terms and any applicable deductible.

Importantly, Turo’s insurance acts as the primary coverage during active trips, meaning it pays first before any personal policy would be considered. This built-in coverage helps fill the gap left by excluded personal insurance, but guests should review coverage limits and exclusions carefully, especially for high-value vehicles or extended trips.

Why Most Personal Auto Insurance Policies Exclude Turo

Most personal auto insurance carriers specifically exclude coverage for car-sharing services like Turo because such use transforms the vehicle from personal to commercial use.

Traditional policies are designed for non-commercial, personal transportation, and renting a vehicle (even occasionally) significantly increases risk exposure—the car is driven more frequently, by unfamiliar drivers, in potentially unfamiliar areas. Insurers assess risk based on usage patterns, and peer-to-peer rentals introduce higher risk factors that are not accounted for in standard premiums.

Best home owners insurance company for codos

Best home owners insurance company for codosAs a result, insurers may deny claims arising from a Turo rental and, in some cases, could terminate a policy if they discover the vehicle was used on the platform without proper commercial insurance. This exclusion is a crucial distinction that vehicle owners on Turo must understand before listing their car.

Options for Additional Coverage When Using Turo

Drivers and vehicle owners on Turo have several options to ensure proper insurance coverage. Hosts can purchase Turo’s Protection Plans designed for higher liability limits and reduced out-of-pocket costs in case of damage. Additionally, some third-party insurers now offer non-owner car-sharing insurance or commercial endorsements that can supplement Turo’s coverage, though availability varies by state and insurer.

Guests may also consider purchasing non-owner liability policies for added protection. It’s important to note that some credit cards offer secondary rental car insurance, but these typically do not apply to peer-to-peer rentals like Turo. Therefore, both hosts and guests must carefully evaluate all available insurance layers and understand their financial responsibility before any trip begins.

| Insurance Option | Coverage Type | Applies to Hosts? | Applies to Guests? | Key Notes |

|---|---|---|---|---|

| Personal Auto Insurance | Limited or None | No | No | Typically excludes commercial use, which includes Turo rentals. |

| Turo Protection Plans | Primary coverage (Liability, Collision, Theft) | Yes | Yes | Plans range from Liability Only to Premium; coverage activates after trip confirmation. |

| Third-Party Commercial Insurance | Supplemental protection | Yes (select policies) | Yes (non-owner options) | Specialized policies for car-sharing; verify state availability and terms. |

| Credit Card Rental Coverage | Secondary coverage | No | Limited | Rarely covers peer-to-peer rentals; review card terms carefully. |

Does Personal Auto Insurance Cover Turo Rentals? A Detailed Guide

Does Your Personal Car Insurance Provide Coverage When Renting Through Turo?

Is rental home insurance worth it

Is rental home insurance worth itUnderstanding Personal Car Insurance and Turo Rentals

- Standard personal car insurance policies are primarily designed to cover vehicles owned by the policyholder for personal use, such as commuting, running errands, or leisure travel. These policies typically do not extend coverage to scenarios involving commercial activity, which includes renting out your vehicle through peer-to-peer platforms like Turo.

- When you list your car on Turo, you are engaging in a form of short-term rental operation, which many insurers consider a business use of the vehicle. Most personal auto policies explicitly exclude coverage for commercial activities, meaning that in the event of an accident during a rental period, your insurer might deny the claim.

- It's crucial to review your policy documents or contact your insurance provider directly to confirm whether your personal coverage applies when the vehicle is rented. Failing to disclose vehicle rental activity could result in policy cancellation or legal complications if a claim is filed.

Turo’s Built-In Insurance Options

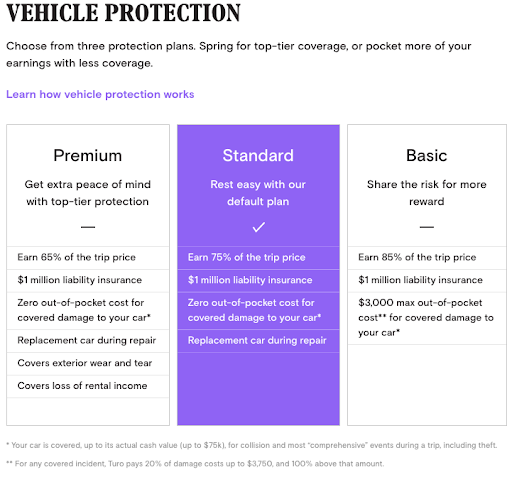

- Turo provides its own protection plans to cover both car owners and renters, offering different levels of coverage depending on the selected plan: Minimum, Standard, and Premium. These plans activate during the rental period and are designed to bridge the gap left by personal insurance exclusions.

- The Minimum plan provides liability coverage only, typically meeting state requirements, but offers no protection for damage to the host’s vehicle. The Standard and Premium plans include increasing levels of protection for damage to the vehicle, with the Premium plan waiving the deductible and providing more comprehensive benefits.

- Turo’s protection plans are coordinated with the renter’s responsibility and often include liability coverage, collision protection, and theft coverage. These plans operate independently of personal insurance, though coordination may occur if claims exceed Turo’s coverage limits or involve unique circumstances.

How Your Personal Insurance May Still Play a Role

- In certain situations, your personal auto insurance might still contribute, especially if a claim exceeds Turo’s coverage limits or involves specific types of claims not fully addressed by Turo’s protection plans. Some policies may provide secondary coverage after primary benefits from Turo are exhausted.

- Additionally, if you carry umbrella liability insurance, this policy may extend coverage beyond the limits of both your personal auto insurance and Turo’s protection plan, provided the incident is not explicitly excluded. However, this depends on the terms of the umbrella policy and the nature of the rental activity.

- It is not uncommon for personal insurers to require that any rental income or vehicle-sharing activity be disclosed. Some insurers offer endorsements or separate policies for peer-to-peer vehicle sharing, ensuring legal and financial protection while using platforms like Turo.

Frequently Asked Questions

Does my personal auto insurance cover me when renting through Turo?

In most cases, standard personal auto insurance does not cover vehicles rented through Turo. Turo operates as a peer-to-peer car-sharing platform, and traditional insurers typically exclude coverage for vehicles used in commercial rentals. While your policy might cover liability in some situations, comprehensive or collision coverage usually won’t apply. Always verify with your insurer before using Turo to avoid unexpected out-of-pocket costs.

Will my credit card provide insurance for Turo rentals?

Some credit cards offer rental car insurance that may extend to Turo, but coverage varies widely. Many cards exclude peer-to-peer rentals like Turo from their benefits. Even if coverage applies, it might only provide secondary insurance and not cover all vehicle types or damages. Check your card’s terms and conditions carefully and contact the issuer directly to confirm whether Turo rentals are included before relying on credit card coverage.

What insurance options does Turo provide for renters?

Turo offers multiple protection plans: Minimum, Standard, and Premium. The Minimum plan meets legal requirements but includes a high deductible. Standard reduces the deductible and adds some coverage. Premium offers the most protection, including a $0 deductible for damages and additional benefits like roadside assistance. These plans cover liability, collision, and theft, helping protect both renters and vehicle owners during the rental period.

Can I use my existing insurance to cover a car I list on Turo?

Most personal auto insurance policies do not cover vehicles used for commercial purposes like Turo rentals. If you list your car on Turo, your personal policy may cancel or deny claims during a rental. Turo provides its own insurance and protection plans that activate when the car is rented. It's essential to inform your insurer or consider switching to a rideshare or commercial policy to maintain proper coverage.

Leave a Reply