Do You Need Special Car Insurance To Drive For Uber

Driving for Uber offers flexibility and income potential, but it also raises important questions about insurance coverage.

Personal car insurance policies typically don’t cover accidents that occur while driving for a rideshare service. This leaves many drivers exposed to significant financial risk. Uber provides its own insurance, but there are gaps in coverage depending on the driver’s activity—whether waiting for a ride request, en route to pick up a passenger, or during a trip.

Understanding these limitations is crucial. Specialized rideshare insurance or endorsements may be necessary to ensure comprehensive protection. Without proper coverage, drivers could face out-of-pocket expenses, claim denials, or even policy cancellation.

Do You Need Special Insurance For Airbnb

Do You Need Special Insurance For AirbnbDo You Need Special Car Insurance To Drive For Uber?

Yes, you do need special car insurance to drive for Uber, as your personal auto insurance policy typically does not cover you when you're using your vehicle for ridesharing activities.

Most personal car insurance providers consider driving for Uber a commercial use of your vehicle, which voids coverage during active trips—especially once you’ve accepted a ride request. To ensure proper protection, Uber provides a commercial insurance policy that covers drivers during certain periods of the rideshare process, but it's not a substitute for having rideshare-specific coverage.

Many drivers opt for a rideshare endorsement or a dedicated rideshare insurance policy that bridges the gap between personal insurance and Uber’s coverage, particularly during periods when you’re logged into the app but haven’t yet accepted a ride (Period 1), where personal policies often don’t apply and Uber’s insurance may offer limited protection.

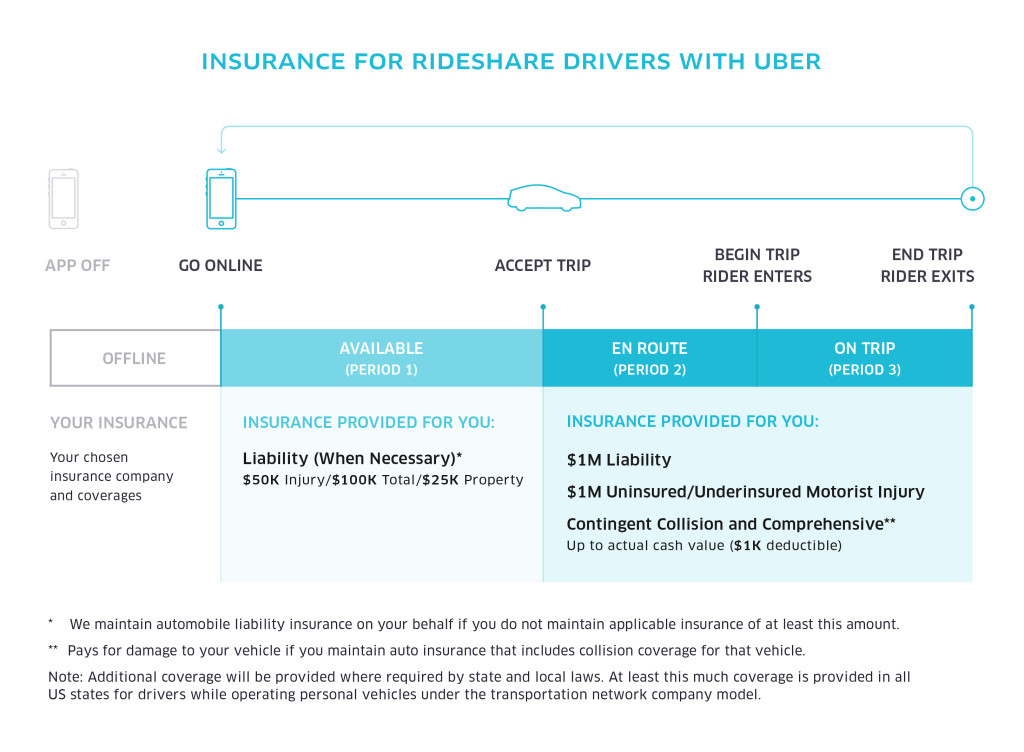

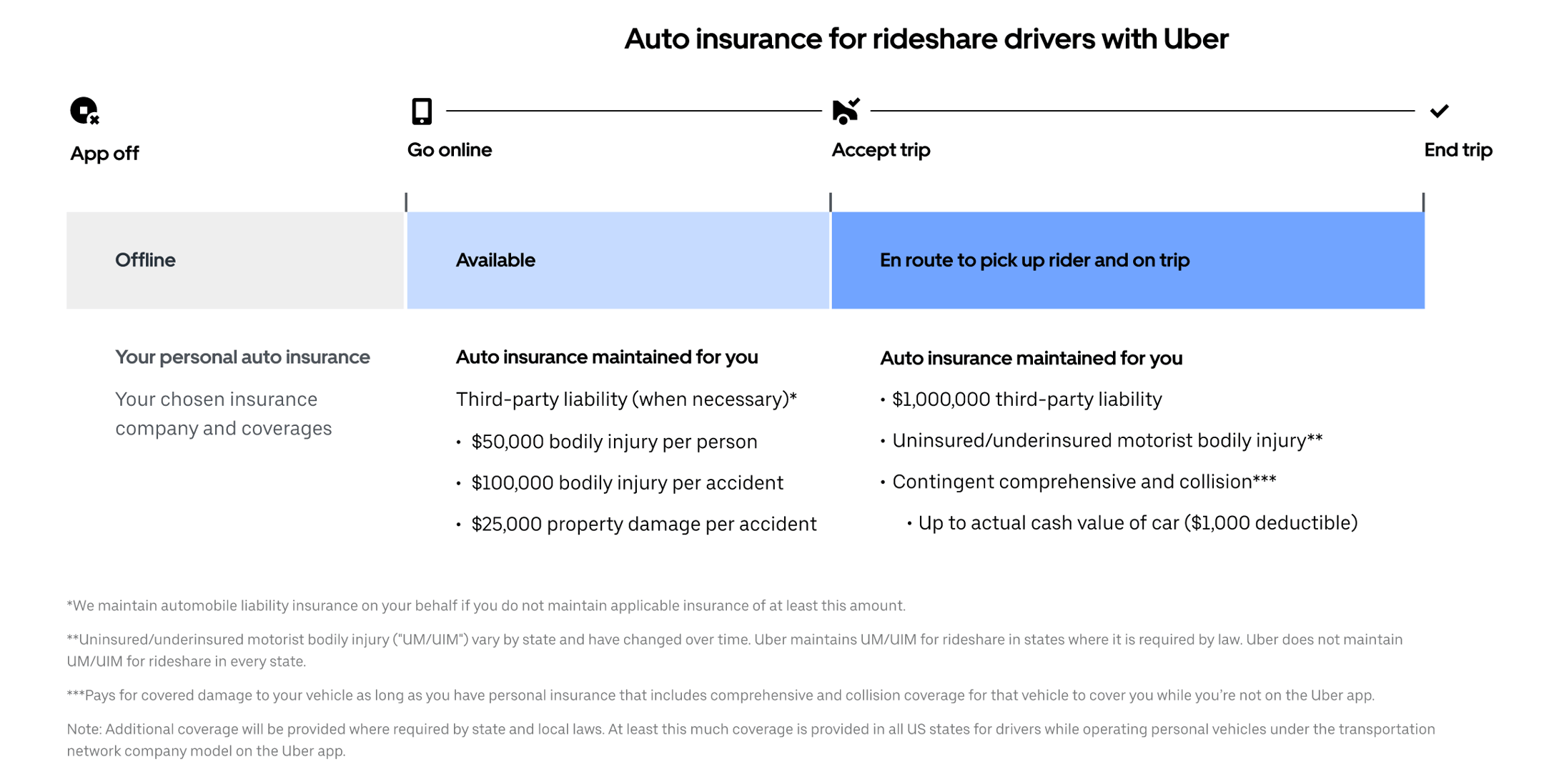

Understanding the Three Stages of Uber's Insurance Coverage

Uber provides insurance coverage that varies depending on the stage of the rideshare process, divided into three distinct periods. In Period 1, when the Uber app is on but you haven’t accepted a trip, Uber offers limited liability coverage (typically up to $50,000 per person, $100,000 per accident for bodily injury, and $25,000 for property damage), which may not fully replace your personal insurance.

Do You Need Special Insurance For Amazon Flex

Do You Need Special Insurance For Amazon FlexDuring Period 2, from accepting a ride to picking up the passenger, and Period 3, when the passenger is in the vehicle, Uber provides more comprehensive coverage, including liability, collision, and comprehensive coverage up to $1 million in some regions. However, this coverage only activates once you've accepted a trip, leaving a coverage gap in Period 1 that personal policies often don't cover—making supplemental insurance critical.

Standard personal auto insurance policies are designed for non-commercial use and typically exclude coverage when the vehicle is being used to transport paying passengers.

If you're involved in an accident while driving for Uber and your insurer determines you were working, they may deny your claim or even cancel your policy. This is because ridesharing increases the frequency and risk of driving, which insurers view as a higher liability.

While Uber’s insurance steps in during active trips, your personal insurer won’t cover damages or injuries that occur when you're logged into the app waiting for a fare—a situation that falls squarely into a gray area. This is why many drivers choose to purchase a rideshare endorsement to extend their personal coverage to include gaps during Period 1.

Do You Need Special Insurance For Food Delivery

Do You Need Special Insurance For Food DeliveryHow to Get the Right Insurance Coverage as an Uber Driver

To ensure full protection, Uber drivers should consider adding a rideshare endorsement to their existing personal auto policy or purchasing a standalone rideshare insurance policy from insurers like GEICO, Progressive, or State Farm, many of which now offer tailored plans.

These policies extend your personal coverage to include all phases of ridesharing, including when you're waiting for a ride request. It’s also essential to inform your insurance provider that you drive for Uber to avoid claim denials.

Comparing quotes and understanding exactly what each policy covers—especially deductibles, liability limits, and coverage periods—can help drivers make informed decisions. Having the right insurance provides not only legal protection but also greater peace of mind while earning.

| Insurance Period | Status in Uber App | Coverage Provided |

|---|---|---|

| Period 1 | App is on, no trip accepted | Limited liability coverage: up to $50K/$100K/$25K (BI/PD); no collision/comprehensive from Uber |

| Period 2 | Trip accepted, en route to passenger | $1M liability, uninsured motorist, collision & comprehensive (subject to deductible) |

| Period 3 | Passenger in car | Full $1M coverage including property damage, bodily injury, and vehicle damage |

Do You Need Special Car Insurance to Drive for Uber? A Complete Guide

What Insurance Coverage Is Required to Drive for Uber?

Personal Auto Insurance: The Starting Point for Uber Drivers

Every Uber driver must begin with a valid personal auto insurance policy that meets their state’s minimum requirements. This coverage is essential even before considering rideshare-specific protections.

Personal auto insurance typically covers accidents that occur when the vehicle is being used for personal purposes, such as commuting to work or running errands. However, it’s important to note that most personal policies explicitly exclude coverage when the vehicle is used for commercial purposes, which includes driving for ride-sharing platforms like Uber.

Failing to inform your insurer about your intention to drive for Uber may result in claim denials if an incident occurs while driving for the platform. Therefore, while personal insurance is a foundational requirement, it alone does not suffice for full protection during rideshare activities.

- Drivers must maintain personal auto insurance that satisfies their state's liability limits.

- Most personal insurance policies exclude coverage during rideshare operations unless specifically endorsed.

- It’s crucial to notify your insurer about your rideshare activities to avoid potential coverage gaps or policy cancellation.

Uber provides a commercial insurance policy that activates at specific stages of a driver’s app engagement, offering much-needed protection during ride-hailing activities.

This coverage fills the gap left by personal insurance policies when drivers are using their vehicles for commercial purposes. Uber’s insurance coverage is divided into different periods: Period 1 covers the time when the app is on but no ride has been accepted; Period 2 begins when a ride is accepted but before picking up the passenger; and Period 3 covers the time from passenger pickup until drop-off.

Each period offers specific levels of liability, uninsured motorist, and collision and comprehensive coverage. For example, during Periods 2 and 3, Uber provides up to $1 million in liability coverage, which significantly exceeds most personal policies. While this commercial coverage is provided at no extra cost to drivers, understanding its limitations and activation criteria is essential for comprehensive protection.

- Uber’s insurance activates in three distinct periods based on app status and trip progress.

- During Period 1, contingent liability coverage is provided, but collision and comprehensive coverage may not apply unless specific conditions are met.

- Periods 2 and 3 include $1 million in liability coverage, collision, and comprehensive protection, subject to a deductible.

Gig Worker Insurance Add-Ons: Bridging Coverage Gaps

To ensure continuous protection, many Uber drivers choose to purchase a rideshare-endorsed or gig economy insurance add-on from their personal insurance provider. These endorsements are specifically designed to close the protection gaps that occur between personal insurance and Uber’s commercial policy, especially during Period 1 when the driver is waiting for a ride request.

Without such an endorsement, drivers may find themselves financially exposed if an accident occurs while the app is on but no ride has been accepted. These add-ons typically extend personal coverage to include periods of rideshare activity and may include higher limits and broader protections than standard personal policies.

While not always required by law, obtaining such coverage is considered a best practice for financial and legal protection. Drivers should compare options from multiple insurers to find a policy that balances affordability with comprehensive coverage.

- Rideshare endorsements extend personal insurance to cover Period 1, when the Uber app is active but no ride is accepted.

- These add-ons often require a small premium increase but prevent coverage lapses that could lead to out-of-pocket expenses.

- Drivers should verify that the endorsement is compatible with Uber’s commercial policy and provides seamless transition between coverages.

What type of car insurance is required to drive for Uber?

Personal Auto Insurance for Pre-Trip Period

- When you are using your vehicle for personal reasons or signed into the Uber app but before accepting a ride request, your personal auto insurance policy is responsible for coverage. This phase is known as Period 0 in ride-share insurance terminology.

- Most standard personal car insurance policies do not cover commercial activities, so if an accident occurs while you are logged into the Uber app, your insurer might deny the claim, leaving you financially exposed.

- It’s essential to notify your insurance provider that you drive for Uber, as some companies offer ride-share endorsements or add-on coverage to extend protection during this phase.

Uber’s Interim Coverage During Idle Time (Period 1)

- Once you log into the Uber app and are available to accept trips—but before you’ve accepted a ride request—Uber provides limited liability coverage. This is known as Period 1.

- During this phase, Uber supplies $50,000 in bodily injury coverage per person, $100,000 per accident, and $25,000 for property damage (50/100/25), which may not be sufficient in moderate to serious accidents.

- In addition, Uber includes contingent collision and comprehensive coverage during this period, but your personal deductible may apply, and gaps in protection can still exist depending on your location and vehicle value.

Commercial Insurance Coverage While on a Trip (Periods 2 and 3)

- After you accept a ride request (Period 2) or when you are en route to pick up or transporting a passenger (Period 3), Uber provides comprehensive commercial insurance coverage.

- This includes $1 million in liability coverage, which applies to both bodily injury and property damage, as well as collision and comprehensive coverage with a $1,000 deductible for eligible incidents.

- Uber’s primary commercial policy acts as the main source of coverage during these periods, reducing reliance on personal insurance. However, drivers must ensure they meet all vehicle requirements and compliance standards set by Uber to remain eligible for this protection.

Do Uber drivers need additional insurance beyond personal coverage?

What Happens to Personal Insurance When Driving for Uber?

When drivers use their personal vehicles to provide rides through Uber, their standard personal auto insurance may not offer full coverage during all phases of a trip.

Most personal insurance policies are designed for private, non-commercial use, so when a driver activates the Uber app and begins working, they are technically engaging in commercial activity. Many personal insurers will deny claims or reduce coverage if they discover the vehicle was being used for ride-sharing at the time of an accident.

This leaves a significant gap in protection, especially during periods when the driver is logged into the app but hasn’t accepted a ride yet. To avoid financial risk, drivers need to understand exactly when their personal policy stops providing coverage and what alternatives are available.

- Personal insurance typically covers only personal use of the vehicle, not commercial ridesharing activities.

- Insurers may investigate and deny claims if the vehicle was being used for ride-hailing during an accident.

- There are specific periods during Uber driving—such as when the app is on but no ride is active—where personal policies may not apply.

Does Uber Provide Insurance for Its Drivers?

Yes, Uber does offer some level of insurance coverage, but it varies depending on the stage of the driver’s activity within the app. The company provides contingent liability and, in some cases, collision and comprehensive coverage. However, this coverage is secondary or primary depending on the phase: waiting for a ride request, en route to pick up a passenger, or actively transporting a passenger.

While Uber’s insurance helps fill the gap left by personal policies, it may not cover everything, such as the driver’s deductible or damage to personal property. Additionally, coverage limits and availability differ by state and country, so drivers must review Uber's insurance details carefully to understand what is and isn’t included.

- Uber provides insurance coverage that kicks in during specific periods of driving, such as after accepting a trip.

- During periods when the app is active but no ride is accepted, Uber’s coverage may be limited or secondary.

- Uber’s insurance may not cover deductibles, personal injury, or personal vehicle damage in all cases.

What Are the Options for Additional Insurance Coverage?

Uber drivers have several options to obtain proper insurance coverage beyond their personal policy. One common solution is to purchase a rideshare-specific endorsement or a commercial policy that bridges the gap between personal and Uber’s coverage. Many major insurance companies now offer rideshare insurance add-ons, which extend protection during all phases of using the Uber app.

Another option is to secure a full commercial auto policy, though it tends to be more expensive. Drivers should compare policies based on coverage limits, deductibles, and cost to ensure continuous protection and compliance with both local regulations and Uber’s requirements.

- Drivers can add a rideshare endorsement to their personal policy, which extends coverage during app use.

- Commercial auto insurance policies offer comprehensive protection but come with higher premiums.

- Comparing different policies helps drivers find affordable coverage that meets both legal and platform requirements.

Frequently Asked Questions

Do You Need Special Car Insurance To Drive For Uber?

Yes, you need special car insurance to drive for Uber. Personal auto insurance typically doesn't cover you when driving for ride-sharing. Uber provides some insurance coverage during specific periods, like when you have a ride request or are transporting passengers. However, coverage gaps exist, especially when the app is on but you don't have a passenger. Uber drivers should consider a rideshare-endorsed policy for full protection.

What Does Uber’s Insurance Cover?

Uber’s insurance provides liability, uninsured motorist, and contingent comprehensive and collision coverage. It applies in two main periods: when you’ve accepted a trip and are en route to pick up a passenger, and while transporting a passenger. However, when the app is on but you haven’t accepted a ride, coverage is limited. Personal insurance may not apply during this time, so a rideshare-specific policy helps fill coverage gaps.

Can I Use My Personal Car Insurance for Uber Driving?

You should not rely solely on personal car insurance when driving for Uber. Most personal auto policies exclude coverage when you're using your vehicle for commercial purposes, such as ride-sharing. If you're in an accident while driving for Uber, your insurer might deny the claim. To avoid this, obtain a rideshare-endorsed policy or confirm with your insurer that your coverage applies during all driving periods.

When Am I Covered by Uber’s Insurance?

You’re covered by Uber’s insurance primarily when you’ve accepted a trip request and are either en route to pick up a passenger or actively transporting them. During this time, Uber provides liability and other protections. However, when the app is on but you’re waiting for a ride request, coverage is minimal. This period often requires a rideshare insurance add-on or endorsement to stay properly protected.

Leave a Reply