Do You Need Special Insurance To Be A Delivery Driver

Driving for food or package delivery services has become a popular way to earn income, but many wonder if standard auto insurance is enough. The reality is that using a personal vehicle for delivery work can create coverage gaps. Most personal insurance policies exclude commercial activities, and regular use for deliveries may violate your policy terms.

Without proper coverage, drivers risk denied claims or canceled policies. Specialized insurance, such as hired and non-owned auto insurance or ride-share and delivery endorsements, may be necessary. Understanding the risks and requirements is essential for any delivery driver seeking financial protection on the road.

Do You Need Special Insurance To Be A Delivery Driver?

Yes, if you're working as a delivery driver—whether for platforms like Uber Eats, DoorDash, Grubhub, or Amazon Flex—you typically need special insurance coverage beyond a standard personal auto policy. Most standard car insurance policies are designed for personal use and explicitly exclude coverage for commercial activities, including food or package delivery.

Do You Need Special Insurance For Lyft

Do You Need Special Insurance For LyftEngaging in these delivery services transforms your vehicle into a commercial asset, and if you're involved in an accident while making deliveries, your personal insurer may deny the claim due to the commercial nature of the activity. This creates a significant financial risk, which is why understanding and obtaining the right insurance is crucial for delivery drivers.

Understanding the Gap in Personal Auto Insurance

Standard personal auto insurance policies operate under the assumption that the vehicle is primarily used for commuting, errands, and other non-commercial purposes.

When you begin driving for delivery apps, you’re effectively using your car for business, which is often categorized by insurers as “courier” or “ridesharing/commercial delivery” use. Most policies contain clauses indicating that coverage does not extend to vehicles used “for hire” or for commercial purposes.

Therefore, if an accident occurs while you're logged into a delivery app, en route to pick up food, or delivering an order, your personal insurer could refuse to pay damages, leaving you responsible for repair costs, medical bills, and legal liabilities. This lapse in coverage is known as the “insurance gap” and highlights the urgent need for supplemental or specialized insurance when working as a delivery driver.

Do You Need Special Insurance For Shipt

Do You Need Special Insurance For ShiptTypes of Insurance Available for Delivery Drivers

Delivery drivers have several insurance options to close the coverage gap. First, some delivery platforms offer limited liability and collision coverage during specific periods of active delivery—for instance, once you've accepted a delivery request and until the drop-off is complete.

However, this coverage varies by company and often only activates during “Period 2” and “Period 3” of the delivery process (when a delivery is accepted). For comprehensive protection, many drivers opt for non-owner commercial auto insurance or rideshare/delivery endorsements added to their existing personal policy.

Some insurers now offer hybrid policies specifically tailored for gig workers, combining personal and commercial coverage. For drivers who use their vehicle extensively for deliveries, a full commercial auto insurance policy may be the best (though more expensive) option, providing broad protection regardless of the delivery app in use.

When and How to Purchase Delivery Driver Insurance

It's essential to purchase appropriate insurance before you begin driving for delivery services—do not wait until after an accident. Start by reviewing your current personal auto policy to understand what is and isn't covered.

Do You Need Special Insurance For Turo

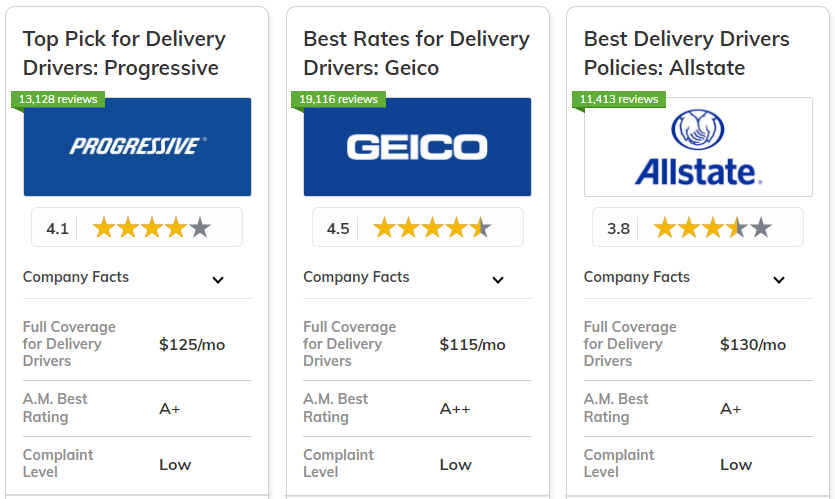

Do You Need Special Insurance For TuroThen contact your insurance provider to ask about rideshare endorsements or gig economy add-ons. If your insurer doesn't offer such options, consider switching to a company that does, like State Farm, GEICO, or Progressive, all of which provide specific solutions for delivery drivers.

Make sure you understand the coverage periods—some policies only activate when you're actively fulfilling a delivery, not when you're logged in but without an assignment. Accurately reporting your vehicle usage is vital to avoid policy cancellation or claim denial.

| Insurance Type | Coverage Scope | Best For |

|---|---|---|

| Personal Auto Insurance | Limited or no coverage during delivery activities | General commuting, not for delivery work |

| Rideshare/On-Demand Delivery Endorsement | Bridges gaps during active delivery periods | Part-time or occasional delivery drivers |

| Commercial Auto Insurance | Full coverage for business use of vehicle | Full-time delivery drivers or business owners |

| Platform-Provided Insurance (e.g., DoorDash, Uber) | Secondary liability and collision during active delivery | Supplemental protection in combination with personal policy |

Do You Need Special Insurance To Be A Delivery Driver: A Complete Guide

What Insurance Coverage Is Required for Delivery Drivers?

Personal Auto Insurance Limitations for Delivery Drivers

- Most personal auto insurance policies explicitly exclude coverage when a vehicle is used for commercial purposes, which includes food or goods delivery. Drivers who use their personal vehicles for delivery work may find their claims denied if an accident occurs while on a delivery job, as insurers consider this a higher-risk activity than typical personal use.

- Insurance companies often define delivery driving as business use, which typically requires a commercial policy. Even occasional deliveries can void standard coverage, especially if the driver is being compensated, whether through wages, per-delivery fees, or tips.

- Drivers may not realize their personal coverage is insufficient until after an accident. When claims are denied, they could face significant out-of-pocket expenses for vehicle repairs, medical bills, or third-party liability, making it critical to understand the limitations of personal policies.

Commercial Auto Insurance Requirements

- Commercial auto insurance is specifically designed for vehicles used in business operations, including delivery services. This type of policy provides coverage for liability, collision, comprehensive damage, and medical payments when vehicles are used for work-related deliveries.

- The exact requirements for commercial coverage depend on the nature of the delivery job. For instance, delivery drivers employed directly by a company—such as couriers or truck drivers—usually require a commercial policy under the employer’s insurance plan, with the driver listed as an authorized operator.

- Independent contractors using their own vehicles, such as gig economy drivers for food delivery platforms, may need hired and non-owned auto insurance (HNOA), which covers them when using a personal vehicle for business purposes not owned by their employer. This gap-filler coverage is often necessary when commercial policies are not owned by the driver or employer.

Platform-Provided Insurance and Gaps in Coverage

- Many delivery platforms, like Uber Eats, DoorDash, or Instacart, offer contingent insurance coverage that activates during specific periods of a delivery, such as after accepting a delivery request and before dropping off the order. However, this coverage is secondary, meaning it only applies after a driver’s personal insurance pays out first, and may not cover the entire cost of a claim.

- There are significant coverage gaps in platform policies, particularly during the logged-in but not on a delivery phase, where protection may be limited or nonexistent. Drivers who assume they’re fully covered by the delivery app can be at risk if an accident occurs during these periods.

- It is essential for delivery drivers to review the exact terms of the platform’s insurance policy, understand when coverage begins and ends, and consider supplemental insurance such as a commercial endorsement or non-owner policy to fill potential gaps, especially if their personal insurer does not cover business use under any circumstances.

What Insurance Do Delivery Drivers Need?

Do You Need Special Insurance To Deliver Food

Do You Need Special Insurance To Deliver FoodCommercial Auto Insurance for Delivery Drivers

- Delivery drivers are required to have commercial auto insurance when using their vehicle to deliver goods as part of a job, because personal auto policies typically do not cover vehicles used for business purposes. This type of insurance is essential as it provides liability coverage for bodily injury and property damage that may occur during deliveries.

- Commercial auto insurance also offers protection for damage to the insured vehicle itself, especially if it is used frequently on the road under varying conditions, which increases wear and risk. Policies can be customized based on the type of delivery service, vehicle size, and the areas where the driver operates.

- Many delivery companies either require proof of commercial insurance or provide it directly to drivers, especially in cases where the driver is considered an employee. However, independent contractors or gig workers must obtain their own commercial coverage to remain compliant and protected.

Non-Owned and Hired Auto Insurance Coverage

- Non-owned auto insurance is designed for delivery drivers who use someone else’s vehicle or their personal car for work-related deliveries but are not the registered owners. This coverage extends liability protection when the driver is at fault in an accident while performing delivery duties.

- Hired auto insurance applies when a delivery driver rents or leases a vehicle specifically for deliveries, such as a van or scooter. This policy covers both liability and physical damage to the rented vehicle during the rental period, and is often required by rental agencies.

- These types of policies are particularly important for gig economy drivers working with platforms like Uber Eats, DoorDash, or Instacart, where personal auto insurance may have gaps during active delivery periods. Non-owned and hired auto coverage helps fill those protection gaps when the driver is logged into the app and en route to a delivery.

Uninsured and Underinsured Motorist Coverage for Delivery Drivers

- Uninsured motorist coverage protects delivery drivers if they are involved in an accident with a driver who has no auto insurance. Given the amount of time delivery drivers spend on the road, the likelihood of encountering an uninsured motorist increases, making this coverage a critical component of a comprehensive insurance plan.

- Underinsured motorist coverage comes into play when the at-fault driver’s insurance limits are insufficient to cover the full cost of damages or injuries. For delivery drivers, who often drive long hours and through high-traffic areas, this protection ensures they won’t be left with out-of-pocket expenses due to another driver’s inadequate coverage.

- These coverages are especially valuable when a driver’s vehicle is damaged or they suffer injuries that require medical attention. Since personal health and auto insurance may not cover all costs related to work accidents, having uninsured and underinsured motorist protection adds an essential financial safety net during unpredictable road incidents.

Do delivery drivers need specific insurance coverage to work legally?

Why Personal Auto Insurance Is Not Sufficient for Delivery Work

- Most personal auto insurance policies explicitly exclude coverage when the vehicle is used for commercial purposes, such as delivering food, packages, or other goods. This means if an accident occurs while making deliveries, the driver could be left financially responsible for damages and injuries.

- Insurance companies consider delivery driving a higher-risk activity due to increased mileage, frequent stops, and driving during peak hours, which raises the likelihood of accidents. As a result, standard personal policies are not designed to handle these elevated risks.

- Some delivery drivers may falsely assume they are covered under their personal policy, only to discover after an incident that their claim has been denied. This gap in coverage can lead to significant out-of-pocket expenses, legal liabilities, and even the loss of personal assets.

Types of Insurance Required for Delivery Drivers

- Commercial auto insurance is typically required for delivery drivers who use their vehicle primarily for business purposes. This type of policy covers liability, collision, and comprehensive damage specifically in the context of delivery work and is tailored to higher usage levels.

- Rideshare and delivery endorsement policies, sometimes referred to as hired and non-owned auto (HNOA) insurance, are available for drivers working with platforms like Uber Eats, DoorDash, or Amazon Flex. These endorsements extend personal policies during specific delivery periods when the driver is logged into the app and en route to or from a delivery.

- Some delivery companies provide contingent insurance coverage, which applies only after the driver’s personal policy has been exhausted. However, this coverage often has limitations, making it essential for drivers to carry primary commercial or delivery-specific insurance to ensure full protection.

Legal and Platform-Specific Insurance Requirements

- Legally, operating a vehicle for commercial delivery without appropriate insurance can result in fines, suspension of driving privileges, or even criminal charges in case of an uninsured accident. Each state or country has its own set of regulations governing commercial vehicle use and minimum coverage levels.

- Many delivery platforms require proof of insurance that explicitly allows for delivery activities as a condition of use. Drivers may need to provide documentation such as a certificate of insurance to verify they have the necessary coverage before being approved to accept delivery requests.

- Failure to comply with insurance requirements not only poses legal and financial risks but can also lead to deactivation from delivery platforms. Staying compliant ensures uninterrupted work eligibility and protects both the driver and third parties in the event of an accident.

Frequently Asked Questions

Do I need special insurance if I drive for food delivery services like Uber Eats or DoorDash?

Yes, you typically need special insurance for food delivery driving. Personal auto insurance may not cover accidents while delivering, especially when carrying food. Most food delivery companies offer contingent liability coverage, but it only kicks in after your personal policy pays. To stay fully protected, consider obtaining rideshare or delivery-specific insurance, which bridges gaps between personal and commercial policies during active delivery periods.

Does my personal car insurance cover me while I’m working as a delivery driver?

Most personal car insurance policies exclude coverage when you're using your vehicle for commercial purposes like delivery. While some coverage may apply in limited cases, insurers often deny claims if they find you were working. Gaps exist between logging into the app and accepting a delivery. To ensure protection, notify your insurer about your delivery work and consider adding rideshare or delivery endorsement to your policy.

What is delivery driver insurance, and how is it different from regular car insurance?

Delivery driver insurance is a specialized policy or endorsement designed for drivers using their vehicles commercially. Unlike standard personal car insurance, it covers incidents that occur during all stages of delivery work — from logging into the app to dropping off orders. It typically includes higher liability limits and protection for property damage or bodily injury while working, addressing gaps that regular insurance doesn’t cover during commercial use.

Do You Need Special Insurance To Deliver Pizza

Do You Need Special Insurance To Deliver PizzaCan I get delivery insurance if I don’t own a car but rent or lease one?

Yes, you can get delivery insurance even if you rent or lease a vehicle. Many insurers offer non-owner or hired vehicle policies tailored for delivery drivers. These policies provide liability coverage while using a rented or borrowed car for delivery work. However, verify that the coverage meets the requirements of your delivery platform and the vehicle owner. Always disclose your commercial use to avoid claim denials and ensure continuous protection.

Leave a Reply