Does Condo Insurance Cover Special Assessments

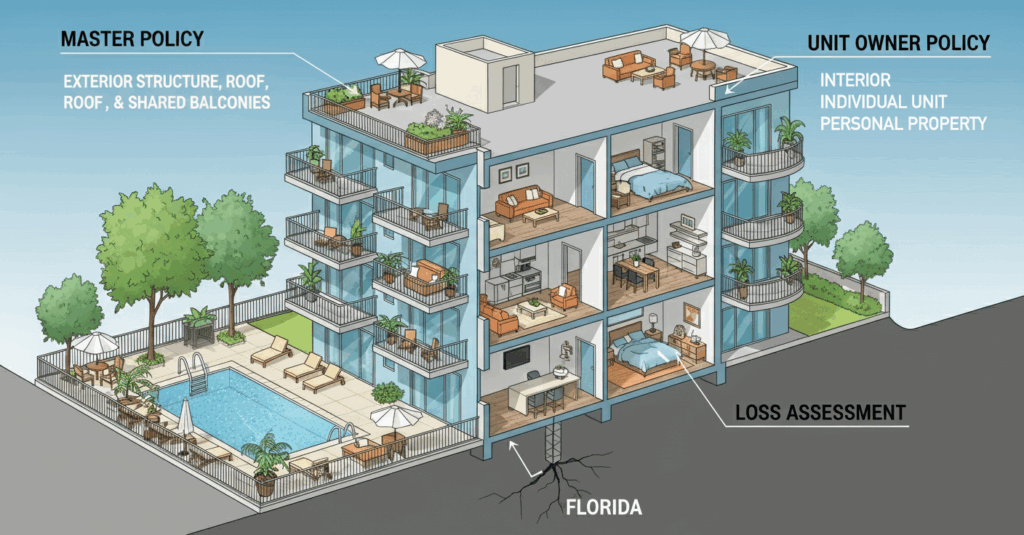

Condo insurance typically covers a unit owner’s private space and personal belongings, but many homeowners are unaware of how it intersects with special assessments imposed by homeowners’ associations (HOAs).

These assessments can arise unexpectedly due to major repairs, natural disasters, or legal liabilities affecting common areas. While the HOA’s master policy covers shared spaces, gaps may leave individual owners financially vulnerable.

This raises a critical question: does standard condo insurance cover special assessments? The answer depends on the cause and specific policy wording. Understanding coverage options, such as loss assessment coverage endorsements, is essential for protecting against unforeseen financial responsibility in shared property ownership.

Do I Need Special Insurance To Drive In Canada

Do I Need Special Insurance To Drive In CanadaDoes Condo Insurance Cover Special Assessments?

Condo insurance is designed to protect unit owners from financial losses related to property damage, liability, and additional living expenses, but its coverage limits and inclusions can vary significantly depending on the policy and location. One frequently misunderstood area is whether standard condo insurance policies cover special assessments imposed by a homeowners' association (HOA) or condo board.

A special assessment is an unexpected fee levied on unit owners to cover a major repair or capital improvement not included in the association's normal operating budget—such as roof replacement, elevator repairs, or hurricane damage. While basic condo insurance (often called an HO-6 policy) typically covers personal property and interior unit damage, it does not automatically extend to special assessments.

However, many insurers offer an optional add-on known as loss assessment coverage or special assessment coverage, which can help reimburse owners for their share of such unexpected fees—usually up to a specified policy limit. Understanding the distinction between what the HOA master policy covers and what the individual unit owner must pay is essential for avoiding surprise costs.

What Are Special Assessments in a Condo Association?

Special assessments are fees imposed by a condominium association when the reserve fund and regular dues are insufficient to cover major unexpected repairs or large-scale improvements, such as structural repairs, fire damage restoration, or major system upgrades.

Do I Need Special Insurance To Rent My House

Do I Need Special Insurance To Rent My HouseUnlike regular monthly fees, which fund ongoing maintenance and operations, special assessments are one-time or infrequent charges distributed among unit owners based on their ownership percentage or unit size. These assessments can range from a few hundred to tens of thousands of dollars depending on the scope of the project and the financial health of the association.

They become necessary when the condominium’s master insurance policy has a deductible that the association must pay, or when damages exceed policy coverage limits—both situations triggering a financial obligation passed down to individual owners.

How Does Loss Assessment Coverage Work in Condo Insurance?

Loss assessment coverage is an optional endorsement available on most HO-6 condo insurance policies that specifically addresses an owner’s liability for special assessments resulting from insured perils.

This coverage generally applies when the association assesses unit owners to pay its insurance deductible after a covered loss (e.g., fire, windstorm) or to cover costs exceeding the master policy’s limits. For instance, if a hurricane damages common areas and the master policy’s $10,000 deductible is split among 50 units, each owner might be assessed $200.

Do I Need Special Travel Insurance For A Cruise

Do I Need Special Travel Insurance For A CruiseLoss assessment coverage would reimburse the unit owner up to the limit specified in their policy—often between $1,000 and $10,000. It’s important to note that this coverage only applies to losses caused by perils included in the condo policy, such as fire or vandalism, and does not cover assessments for non-insured reasons like aesthetic upgrades or general repairs.

What Is Not Covered by Loss Assessment Coverage?

While loss assessment coverage provides valuable financial protection, it has notable exclusions that unit owners should be aware of.

This coverage does not apply to assessments for improvements or upgrades to common elements, such as new landscaping, fitness center installations, or aesthetic enhancements. It also does not cover fees related to routine maintenance, budget shortfalls, or financial mismanagement by the association.

Furthermore, assessments resulting from flood or earthquake damage are typically excluded unless the owner has purchased separate flood or earthquake insurance with loss assessment provisions. Policyholders must carefully review their exclusions section to understand the limits and conditions of their coverage. Without proper endorsements, a major event could result in a costly special assessment that the owner must pay out of pocket.

Do I Need Special Travel Insurance If Pregnant

Do I Need Special Travel Insurance If Pregnant| Coverage Type | Covered? | Notes |

|---|---|---|

| Special assessment to pay master policy deductible after fire | Yes (with loss assessment coverage) | Reimbursed up to policy limit if fire is a covered peril |

| Assessment for new clubhouse construction | No | Considered an improvement, not a covered loss |

| Assessment due to flood damage | No (unless flood endorsement added) | Standard policies exclude flood-related losses |

| Assessment after windstorm exceeding master policy limits | Yes (with appropriate coverage) | Only applies if windstorm is covered and endorsement is active |

| Assessment for roof repair after hail damage | Yes (if covered peril and within limits) | Subject to policy terms and deductible conditions |

Does Condo Insurance Cover Special Assessments? A Comprehensive Guide

Does condo insurance typically cover special assessment fees?

Yes, condo insurance typically covers special assessment fees, but only if the policy includes a specific endorsement known as special assessment coverage or loss assessment coverage.

Standard condominium insurance policies, often referred to as HO-6 policies, primarily protect the unit owner’s personal belongings, interior fixtures, and liability. However, when damage to common areas—such as building exteriors, hallways, or shared amenities—triggers a special assessment by the homeowners' association (HOA), the cost for individual unit owners can be significant.

Without this additional coverage, unit owners may be personally liable for their share of these fees. The inclusion of loss assessment coverage helps mitigate that financial risk, typically up to a predetermined limit, such as $1,000 to $10,000, depending on the insurer and policy.

What Are Special Assessment Fees in a Condo Context?

- Special assessment fees are charges imposed by a condominium association when unexpected major repairs or replacements are needed for shared property, such as roofs, elevators, or plumbing systems, and the reserve fund is insufficient.

- These assessments are levied on individual unit owners in proportion to their ownership share, often based on unit size or value, and are legally binding obligations under HOA bylaws.

- Unlike regular monthly maintenance fees, special assessments are one-time or short-term charges that can range from a few hundred to tens of thousands of dollars, depending on the scope of the repairs and the number of units in the building.

What Does Loss Assessment Coverage Include in Condo Insurance?

- Loss assessment coverage, typically available as an endorsement to a standard condo insurance policy, pays for a unit owner’s share of a special assessment if the damage was caused by a covered peril, such as fire, windstorm, vandalism, or water damage from a burst pipe in a common area.

- This coverage usually applies only when the master insurance policy held by the HOA does not fully cover the damage, leaving a shortfall that is passed on to unit owners through the special assessment.

- It's important to note that this coverage has limits, which can vary widely; standard policies might cap this at $1,000 or $2,500, but higher limits can often be purchased for an additional premium.

When Is Special Assessment Coverage Not Applicable?

- Loss assessment coverage generally does not apply if the special assessment is for non-insured events, such as routine maintenance, aesthetic upgrades, or improvements that enhance property value, since these are not considered accidental damages.

- Additionally, if the assessment stems from liability claims or lawsuits against the association—such as a slip-and-fall incident not caused by a covered peril—this coverage may not respond unless liability is explicitly included in the endorsement.

- Some policies also exclude assessments related to ordinance or law issues, such as mandatory building code upgrades after a fire, so it’s essential to review the policy language carefully and potentially request expanded coverage if needed.

Can Condo Insurance Help Prevent Special Assessment Costs?

What Are Special Assessment Costs in a Condo Association?

- Special assessment costs are unexpected fees imposed by a condominium association to cover expenses that exceed the available reserve funds, often due to major repairs or emergencies like roof damage, plumbing failures, or fire restoration.

- These assessments are typically levied when insurance claims do not cover the full cost of repairs or when damage occurs due to uncovered perils, requiring unit owners to pay their share based on ownership percentage.

- Unlike regular monthly dues, special assessments are not budgeted in advance, making them a financial burden for owners who are unprepared for large, sudden payments.

How Does Condo Insurance Cover Special Assessments?

- Many condo insurance policies, specifically under the loss assessment or special assessment coverage provision, help reimburse unit owners for their portion of a special assessment levied by the HOA for certain covered events.

- This coverage generally applies when the assessment stems from damage to common areas caused by a peril insured under the master policy, such as fire, vandalism, or water damage from a burst pipe.

- However, the extent of coverage is subject to policy limits—often between $1,000 and $10,000—so it may not cover the entire assessment if repair costs are very high.

When Does Condo Insurance Not Prevent Special Assessment Costs?

- Condo insurance typically does not cover assessments related to non-insured events, such as improvements to common areas, financial mismanagement by the HOA, or earthquake or flood damage if those perils are excluded from the master policy and not added as endorsements.

- Limited coverage amounts mean that if a special assessment exceeds the loss assessment limit in your policy, you must pay the remaining balance out of pocket.

- Failing to carry adequate insurance or misunderstanding the scope of coverage can leave owners vulnerable, especially when the HOA does not maintain sufficient reserves or comprehensive master insurance.

What Does Loss Assessment Coverage Include for Condo Owners?

What Is Loss Assessment Coverage for Condo Owners?

- Loss assessment coverage is a type of insurance protection typically included in a condo owner's HO-6 policy, designed to help pay for assessments levied by the condominium association after a loss covered under the master insurance policy.

- This coverage becomes necessary when the association's master policy has insufficient limits or a high deductible, leaving unit owners responsible for contributing to the cost of repairs or liability claims.

- For example, if a fire damages common areas like hallways or lobbies and the master policy deductible is $25,000, the condo association may divide that cost among all unit owners. Loss assessment coverage helps pay the individual owner's portion of that assessment.

What Types of Losses Are Covered Under Loss Assessment?

- This coverage generally applies to losses involving common areas such as roofs, elevators, fitness centers, parking garages, and exterior walls when damage results from covered perils like fire, windstorms, vandalism, or water damage from a burst pipe.

- It also extends to third-party liability claims. If someone slips and falls in a shared space and the association is found liable, an assessment may be issued to cover legal expenses or settlements, and loss assessment coverage can help pay the unit owner's share.

- However, not all assessments are covered. Routine maintenance fees, special assessments for upgrades like a new roof or landscaping, or financial mismanagement by the association are typically excluded from this type of insurance protection.

How Much Coverage Should Condo Owners Have?

- Most standard condo insurance policies offer $1,000 to $2,000 in loss assessment coverage by default, but this amount may be insufficient depending on the size of the building and the master policy's deductible.

- Experts recommend reviewing the association’s master policy to understand the deductible and overall coverage limits, then purchasing additional loss assessment coverage—often up to $25,000 or more—if needed.

- Condo owners should also confirm with their insurer whether their policy covers the full amount of an assessment or if there are sub-limits or exclusions, especially for flood or earthquake-related damage, which often require separate policies.

Can You Deduct Special Assessment Fees for Condos on Your Taxes?

What Are Special Assessment Fees for Condos?

- Special assessment fees are one-time or occasional charges imposed by a condominium association to cover major repairs, improvements, or unexpected expenses that exceed the regular budget or reserve funds. These fees are different from regular monthly condo dues, which cover ongoing expenses like landscaping, maintenance, and insurance.

- Examples of projects that may trigger special assessments include roof replacements, elevator repairs, exterior painting, structural repairs, or upgrades to common areas such as pools and lobbies. Because these costs can be significant, assessments may run into thousands of dollars per unit owner.

- Homeowners are typically required to pay these assessments regardless of whether they personally use or approve of the project. The responsibility to pay arises from ownership of the unit and membership in the homeowners' association (HOA), which governs the condo community.

Are Special Assessment Fees Tax Deductible for Homeowners?

- In most cases, special assessment fees are not deductible on your federal income taxes if you use the condo as a personal residence. The IRS generally treats these fees as capital expenses that increase the basis of your property rather than as deductible operating expenses like mortgage interest or property taxes.

- If the assessment is used for improvements that add value to the property—such as a new roof or structural upgrades—it may be added to the home's cost basis. This adjustment can reduce capital gains tax when you eventually sell the condo, but it does not provide an immediate tax deduction.

- There are limited circumstances where part of an assessment may be deductible. For instance, if a portion of the fee pays for repairs deemed ordinary and necessary for rental properties, landlords may be able to claim deductions. However, this applies only to investment properties, not primary residences.

When Can Special Assessments Be Considered Deductible?

- Deductibility can apply if the condo is used exclusively as a rental or investment property. In such cases, special assessments for maintenance or repairs (not improvements) may be treated as deductible maintenance expenses under IRS guidelines for rental income properties.

- The key distinction is between repairs and improvements. Repairs that maintain the property in good operating condition—such as fixing a broken pipe in a common area—may be deductible in the year paid if the unit is rented out. In contrast, improvements that prolong the life or increase the value of the property must be capitalized and depreciated over time.

- It is essential to keep detailed records and invoices associated with the special assessment, including the association’s resolution and how funds were allocated. This documentation helps support any deduction claimed and ensures compliance if the IRS ever questions the filing.

Frequently Asked Questions

Does condo insurance cover special assessments?

Yes, many condo insurance policies include coverage for special assessments through an endorsement called Loss Assessment Coverage. This protection helps pay your share of unexpected fees levied by the homeowners' association for repairs after a covered loss, such as water damage or fire. Standard coverage typically ranges from $1,000 to $5,000, but you can often increase it based on your needs and risk exposure.

What is a special assessment in a condominium?

A special assessment is an extra fee charged by a condominium association to cover unexpected repair or maintenance costs not included in the regular budget.

These can result from events like roof damage, elevator repairs, or legal expenses. When the association’s reserve fund is insufficient, owners are required to pay their share. Condo insurance with loss assessment coverage may help cover these costs if they result from a covered peril.

How does loss assessment coverage work in condo insurance?

Loss assessment coverage in condo insurance helps pay your portion of a special assessment when the condominium association collects funds for a covered loss, such as fire, vandalism, or water damage.

If your policy includes this coverage—usually up to $1,000–$5,000—it activates when the association assesses owners. It doesn't cover assessments for improvements or non-covered perils, so reviewing your policy details is essential to understand limitations and extensions.

Should I increase my loss assessment coverage limit?

You should consider increasing your loss assessment coverage limit if your condo association has high property liabilities or inadequate reserves. Standard limits (e.g., $1,000–$2,500) may fall short if a major incident leads to large special assessments.

Raising coverage to $10,000 or more provides stronger protection at a relatively low premium increase. Consult your insurer, review association financials, and evaluate local risks to determine an appropriate limit for your situation.

Leave a Reply