Dog breeds not covered by home insurance

Some dog breeds face restrictions when it comes to home insurance coverage due to perceived liability risks. While many insurers welcome pets, certain breeds—often those associated with strength or aggression, such as Pit Bulls, Rottweilers, and German Shepherds—are frequently excluded from standard policies.

These exclusions stem from concerns over potential dog bites or property damage, even if individual temperaments vary. As a result, owners of these dogs may struggle to find affordable insurance or face outright denial.

Understanding which breeds are commonly blacklisted and why can help pet owners navigate coverage options, advocate for fair treatment, and ensure their homes and pets remain protected despite breed-related biases in the insurance industry.

Whole Life Dividend Paying Insurance

Whole Life Dividend Paying InsuranceDog Breeds Not Covered by Home Insurance: What Homeowners Need to Know

Many homeowners insurance policies include liability coverage for dog-related incidents, such as bites or property damage.

However, certain breeds are commonly excluded from coverage due to their perceived risk of aggression or likelihood of causing costly claims. Insurers often rely on breed-specific legislation and historical claims data when determining which dogs are considered high risk.

As a result, owners of specific breeds may find it difficult to secure standard home insurance or may be required to pay significantly higher premiums. Understanding which breeds are typically excluded and the rationale behind these policies can help pet owners make informed decisions and find alternative insurance solutions.

Commonly Restricted Dog Breeds

Insurance companies often flag specific breeds as high risk based on incident reports and generalizations about behavior, even if individual dogs are well-trained and non-aggressive.

1199 Life Insurance Phone Number

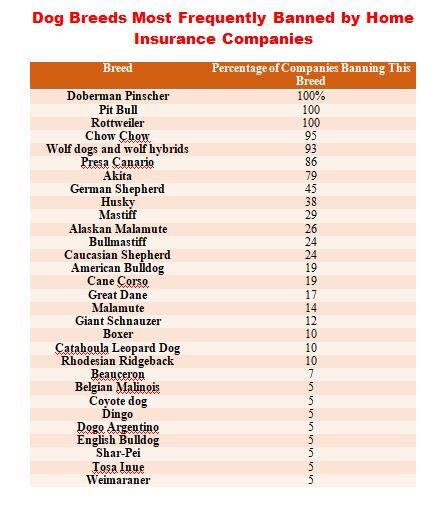

1199 Life Insurance Phone NumberAmong the most commonly restricted breeds are Pit Bulls, Rottweilers, German Shepherds, Doberman Pinschers, Chow Chows, and Akitas. Some insurers also include younger mixed-breed dogs that resemble these breeds in appearance, adding complexity for pet owners.

While breed-specific restrictions vary by insurer and state regulations, the underlying concern is the potential for serious injury or legal liability stemming from dog bites. It's important for dog owners to disclose their pet’s breed accurately during the application process to avoid policy cancellation or claim denial.

How Insurance Companies Assess Risk

Insurers evaluate risk using a combination of claims history, breed-specific data, and regional laws. For example, if a particular breed is statistically overrepresented in dog bite liability claims in a given area, insurers may classify it as high risk.

Some companies also consider the dog’s size, strength, and training history, although most rely primarily on breed alone. Additionally, insurers may consult databases from organizations like the Centers for Disease Control and Prevention (CDC) or insurance industry reports when shaping their underwriting guidelines.

Allstate Life Insurance Forms

Allstate Life Insurance FormsHomeowners in states without breed-specific legislation may still face denials due to internal insurer policies, underscoring the importance of shopping around and asking detailed questions about pet coverage.

Alternatives for Homeowners with Restricted Breeds

If your dog breed is excluded from standard homeowners insurance, several alternatives can help you maintain adequate coverage. Specialized insurance providers, such as Amica, Farmers, or USAA, may offer policies that don’t use breed as a disqualifier, instead focusing on a dog’s behavior and history.

Another option is purchasing standalone umbrella liability insurance, which can extend protection beyond the limits of a standard policy. Additionally, some companies offer separate dog liability insurance to cover veterinary bills or third-party injuries.

Renters with restricted breeds may benefit from renters insurance that includes personal liability, though breed restrictions can still apply. Proactively researching insurers and disclosing accurate information ensures better protection without compromising your pet ownership.

Allstate Life Insurance Sale

Allstate Life Insurance Sale| Dog Breed | Commonly Restricted? | Reason for Restriction | Potential Insurance Alternatives |

|---|---|---|---|

| Pit Bull | Yes | High representation in dog bite claims | Umbrella policy, breed-friendly insurers |

| Rottweiler | Yes | Perceived aggression and strength | Behavior-based insurance, liability riders |

| German Shepherd | Sometimes | Use in law enforcement raises perceived risk | Insurers with case-by-case evaluations |

| Doberman Pinscher | Yes | Historical association with guard roles | Renters insurance, specialized providers |

| Chow Chow / Akita | Yes | Territorial behavior and independence | Umbrella coverage, full disclosure to insurer |

Dog Breeds Typically Excluded from Home Insurance Coverage

Which dog breeds are typically excluded from home insurance coverage?

Certain dog breeds are often excluded from home insurance coverage due to their perceived risk of aggression or likelihood of causing injury. Insurance companies assess these risks based on historical claims data, breed-specific legislation, and incident reports.

As a result, homeowners with certain breeds may face difficulties obtaining coverage, higher premiums, or outright denial of liability protection. While policies vary by insurer and region, there are consistent patterns in which breeds are typically flagged.

Breeds Commonly Excluded by Home Insurance Providers

- Pit Bull Terrier – Frequently at the top of exclusion lists, pit bulls are often associated with severe dog bites and liability claims, leading most major insurers to decline coverage or impose strict restrictions.

- Rottweiler – Known for their strength and guarding instincts, Rottweilers are considered high-risk by many insurers, especially if not properly trained or socialized from an early age.

- German Shepherd – Despite their common use in police and service roles, their size and protective nature result in some insurers categorizing them as higher risk, particularly if they have a history of aggression.

Why Insurers Exclude Certain Dog Breeds

- Claims History – Data shows that certain breeds are disproportionately involved in dog bite incidents resulting in serious injury, prompting insurers to adjust policies based on risk assessment.

- Legal and Regulatory Pressures – Some municipalities have breed-specific legislation (BSL) that restricts ownership of certain dogs, and insurers often align their policies with local laws to mitigate legal exposure.

- Liability Costs – Medical expenses, legal fees, and settlements from dog bite claims can be substantial; insurers exclude breeds associated with higher claim costs to manage financial risk.

- Shop Around – Not all insurance companies use the same breed restrictions; some insurers evaluate dogs based on individual behavior rather than breed alone, making it possible to find coverage with specialized providers.

- Provide Proof of Training and Behavior – Offering documentation of obedience training, good behavior, and a history free of incidents can increase the chances of approval with more flexible insurers.

- Consider Umbrella Liability Insurance – If standard homeowners insurance excludes a dog, purchasing a separate umbrella policy may offer additional liability protection that covers dog-related incidents.

Which dog breeds are excluded from home insurance coverage?

Dog Breeds Commonly Excluded by Home Insurance Providers

- Pit Bull Terriers are among the most frequently excluded breeds due to their reputation for aggression and higher likelihood of biting incidents, which increases liability risk for insurers.

- German Shepherds, while often used in police and service roles, are sometimes restricted because of their strength and potential for aggressive behavior if not properly trained.

- Rottweilers are also commonly blacklisted due to their powerful build and history of involvement in dog attacks, leading insurers to classify them as high-risk breeds.

Why Insurers Restrict Certain Dog Breeds

- Insurance companies evaluate dog breeds based on statistical data regarding dog bites and liability claims, using this information to identify breeds that pose greater financial risk.

- The primary concern is third-party liability; if a dog injures someone on the homeowner’s property, the insurance policy may be required to cover medical expenses and legal fees.

- To minimize the potential for costly claims, insurers adopt breed-specific restrictions, even if individual dogs are well-behaved, relying instead on broader breed-based risk assessments.

How Breed Restrictions Affect Homeowners and Alternatives Available

- Homeowners with restricted breeds may be denied coverage altogether or required to remove the dog from the property to qualify for a policy.

- Some insurance companies offer coverage if the dog is spayed or neutered, has completed obedience training, or is muzzled in public spaces, reducing perceived risk.

- Specialty pet liability insurers and policies from companies that do not use breed-specific criteria can provide alternatives, though they may come with higher premiums or limited coverage options.

Which dog breeds are typically excluded from renters insurance coverage?

Commonly Excluded Dog Breeds in Renters Insurance Policies

- Many renters insurance companies maintain lists of dog breeds they consider high-risk and thus exclude from coverage. These typically include breeds historically associated with aggression or strength, such as Pit Bulls, which encompass several variations including the American Pit Bull Terrier and American Staffordshire Terrier. Insurance providers often categorize these dogs as posing a higher liability risk due to public perception and historical incident reports.

- Rottweilers are another frequently excluded breed because of their size, power, and protective instincts. While many Rottweilers are well-trained and friendly, insurers assess risk based on general breed characteristics rather than individual temperament. As a result, policyholders with Rottweilers may find it difficult to obtain coverage from standard providers.

- German Shepherds, although commonly used in police and service work, are also sometimes restricted. Their strong guarding instincts and large build contribute to their classification as potentially high-risk. Other breeds that often appear on exclusion lists include Doberman Pinschers, Chow Chows, and Akitas, each noted for their loyalty and protective nature, which insurers may interpret as a liability concern.

How Insurance Companies Determine Breed Restrictions

- Insurance companies typically base breed exclusions on data from previous liability claims, breed-specific legislation, and reports from canine organizations. Actuarial data helps insurers assess which breeds are statistically more likely to be involved in dog bite incidents, even if such data is controversial or not fully representative of individual behavior.

- Some insurers rely on third-party databases that track dog bite claims across regions, allowing them to identify patterns and adjust their underwriting guidelines accordingly. For example, if a particular breed is disproportionately represented in bite-related lawsuits in urban areas, insurers may broadly exclude that breed from renter policies in similar environments.

- It’s important to note that visual breed identification is often inaccurate, yet many policies still apply restrictions based solely on reported breed. Even mixed-breed dogs that resemble a restricted breed—such as a Boxer-Pit Bull mix—may be denied coverage, regardless of actual ancestry or temperament.

Alternatives for Renters with Restricted Breeds

- Some specialty insurance providers offer coverage for renters with excluded breeds, though at higher premiums. Companies like Lemonade, State Farm, or USAA may have more flexible underwriting practices or evaluate dogs on a case-by-case basis, considering factors such as training, behavior, and whether the dog has a history of aggression.

- Landlords may require tenants to carry liability coverage specifically for pets, which can be added as a standalone policy or through a personal liability umbrella policy. These options can provide financial protection even if standard renters insurance denies coverage due to breed restrictions.

- Renters can also mitigate risks by enrolling their dogs in obedience training, providing certification of good behavior, or using safety measures like secure enclosures and muzzles when appropriate. Documenting these efforts may help in negotiations with insurers or landlords and improve chances of securing acceptable coverage.

Which dog breeds are excluded from home insurance coverage?

Dog Breeds Commonly Excluded by Home Insurance Providers

- Pit Bull Terriers are among the most frequently excluded breeds due to their reputation for aggression and involvement in dog bite incidents, leading insurers to classify them as high-risk.

- German Shepherds, despite their intelligence and common use in law enforcement, are sometimes restricted because of their size, strength, and occasional tendency toward protective behavior that may result in liability concerns.

- Rottweilers are also commonly excluded due to their powerful build and history of being involved in serious dog attacks, which increases perceived risk from an insurance standpoint.

Why Insurance Companies Exclude Certain Dog Breeds

- Insurers base breed exclusions on statistical data and historical claims information, where certain breeds have been disproportionately involved in dog bite lawsuits and medical payouts.

- Insurance companies aim to minimize liability exposure; by excluding breeds considered dangerous, they reduce the likelihood of costly injury claims related to dog attacks.

- Public perception and media portrayal of specific breeds contribute to insurers' risk assessments, even when individual dog behavior varies significantly within a breed.

Alternatives and Options for Owners of Excluded Breeds

- Some specialty insurance providers offer coverage for excluded breeds, often at higher premiums or with specific conditions such as obedience training or secure fencing.

- Homeowners may consider writing liability riders or endorsements that specifically cover dog-related incidents, though availability varies by state and insurer.

- Responsible ownership practices—like proper training, socialization, and containment—can sometimes help negotiate coverage or reduce premiums with more flexible insurance companies.

Frequently Asked Questions

Why are some dog breeds not covered by home insurance?

Some dog breeds are excluded from home insurance due to their perceived risk of aggression or likelihood of causing injury. Insurers assess breed-specific data on dog bite claims and liability costs. Breeds like Pit Bulls, Rottweilers, and German Shepherds are often flagged. These policies aim to reduce the insurer’s financial risk. Coverage varies by provider, so it's important to check individual policy details before purchasing.

Which dog breeds are commonly excluded from home insurance?

Commonly excluded breeds include Pit Bulls, Rottweilers, Doberman Pinschers, German Shepherds, Akitas, and Chows. Some insurers also restrict Wolf hybrids and certain mastiff types. The exact list varies by insurance company and region. These breeds are often associated with higher bite claim rates. Always confirm exclusions with your provider, as policies differ significantly across states and insurers.

Can I get home insurance if I own a restricted dog breed?

Yes, you can still get home insurance if you own a restricted breed, but it may require shopping around. Some insurers specialize in high-risk policies or don’t use breed lists. Others evaluate dogs by behavior, size, or past incidents instead. Renters with excluded breeds might consider liability-only policies. Always disclose your pet honestly to avoid claim denials later.

How can I reduce liability risks with a high-risk dog breed?

To reduce liability risks, properly train and socialize your dog from an early age. Use secure fencing and keep your dog on a leash in public. Consider liability insurance specifically for pets, or homeowners policies that don’t discriminate by breed. Document vaccinations, training, and good behavior. These steps can improve safety, reduce incident risks, and make insurance approval more likely.

Leave a Reply