Whole Life Dividend Paying Insurance

Whole life dividend-paying insurance is a type of permanent life insurance that provides lifelong coverage while offering the potential for cash value accumulation and annual dividends. Unlike term life insurance, which covers a specific period, whole life remains in force for the policyholder’s entire life as long as premiums are paid.

Policies issued by mutual insurance companies may distribute dividends based on the company’s financial performance, though these are not guaranteed. Policyholders can use dividends to increase coverage, reduce premiums, or accumulate cash value. This financial tool combines protection, savings, and potential growth, making it a strategic component in long-term financial planning for many individuals.

Understanding Whole Life Dividend Paying Insurance: A Comprehensive Overview

Whole Life Dividend Paying Insurance is a type of permanent life insurance that provides lifelong coverage, accumulates cash value, and may pay annual dividends to policyholders. Unlike term life insurance, which covers a specific period, whole life insurance remains in force for the insured’s entire life, provided premiums are paid.

Whole Term Life Insurance Rates

Whole Term Life Insurance RatesThe distinguishing feature of dividend-paying whole life insurance is that it is issued by mutual insurance companies, which are owned by policyholders. When these companies perform profitably, they may return a portion of earnings to policyholders in the form of non-guaranteed dividends. These dividends can be used in several ways: to reduce premiums, purchase additional paid-up insurance, accumulate interest, or be taken as cash.

The cash value grows at a guaranteed rate and can be accessed via policy loans, offering financial flexibility over time. Whole life insurance offers predictable premiums and serves not only as a death benefit vehicle but also as a long-term wealth-building and estate planning tool.

How Dividend-Paying Whole Life Insurance Works

Dividend-paying whole life insurance operates on a foundation of fixed premiums, guaranteed death benefits, and cash value accumulation.

The insurance company invests the premiums collected, and if the company’s financial performance—through investment returns, mortality experience, and operational efficiency—exceeds expectations, it may declare annual dividends. It is crucial to understand that these dividends are not guaranteed and can vary from year to year or even be omitted. Policyholders have several options for using dividends: they can reduce out-of-pocket premium costs, increase the death benefit by purchasing paid-up additions, or let dividends accumulate at interest within the policy.

20 Year Term Life Insurance Quote

20 Year Term Life Insurance QuoteThe policy’s cash value grows on a tax-deferred basis, and loans against this value (if not repaid) reduce the death benefit. Over time, this structure supports both financial protection and long-term savings, making it appealing to individuals seeking stability.

Benefits of Choosing a Dividend-Paying Policy

One of the primary advantages of a dividend-paying whole life insurance policy is its potential for lifetime value growth and financial security. Because it’s a permanent insurance product, it never expires as long as premiums are paid, offering peace of mind to policyholders.

Dividends, while not guaranteed, have historically been paid consistently by well-established mutual insurers, contributing to enhanced cash value over time. The ability to use dividends to buy paid-up additional insurance compounds growth, effectively increasing both the death benefit and cash value without additional premium payments.

Other key benefits include tax-advantaged growth, as cash value accumulates without current income taxation, and accessibility of funds through loans or withdrawals. For estate planning purposes, the death benefit is generally income-tax-free to beneficiaries, making it an effective tool for wealth transfer and legacy planning.

Best Child Life Insurance Plans

Best Child Life Insurance PlansKey Considerations Before Purchasing a Policy

Before purchasing a dividend-paying whole life insurance policy, it’s essential to evaluate several financial and personal factors. These policies are typically more expensive than term life insurance due to the cash value component and lifetime guarantees. Buyers must consider whether they can afford the higher premiums over the long term.

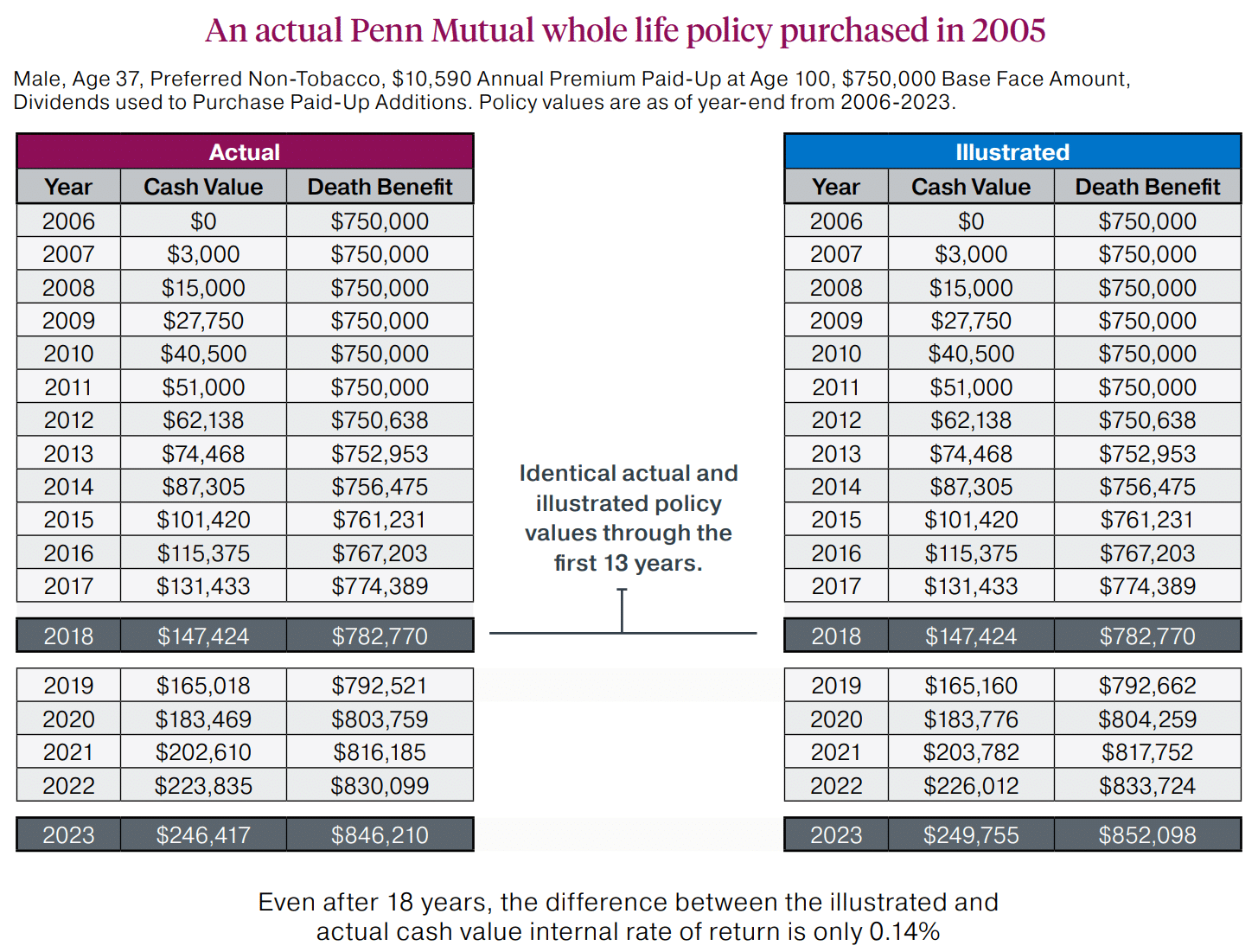

It’s also important to assess the financial strength of the insurance company, as the ability to pay dividends depends on the insurer’s performance and stability. Policy illustrations should be reviewed carefully—they often show projected dividends and values based on current assumptions, but these are not guaranteed.

Additionally, policy loans and withdrawals can significantly impact the death benefit and may trigger taxable events if the policy lapses. Prospective buyers should consult with a licensed financial advisor to determine if this product aligns with their long-term financial goals, risk tolerance, and estate strategies.

| Feature | Description | Benefit to Policyholder |

|---|---|---|

| Guaranteed Death Benefit | A fixed amount paid to beneficiaries upon the insured’s death, assuming premiums are paid. | Provides financial security and supports legacy or estate planning goals. |

| Dividends (Non-Guaranteed) | Annual returns from mutual insurers based on company performance; not guaranteed. | Can enhance cash value, reduce premiums, or increase coverage over time. |

| Cash Value Accumulation | Builds over time on a tax-deferred basis; grows through guaranteed interest and dividend additions. | Offers access to funds via loans and adds a savings component to the policy. |

| Premium Stability | Premiums remain fixed for the life of the policy and do not increase with age. | Protects against rising insurance costs as the policyholder ages. |

| Policy Loans | Allows borrowing against the cash value; interest is charged but loans are not subject to credit checks. | Provides liquidity during emergencies or for other financial needs. |

Comprehensive Guide to Whole Life Dividend Paying Insurance

What are the benefits of dividend-paying whole life insurance?

Steady Cash Value Growth and Tax-Advantaged Savings

- Dividend-paying whole life insurance offers a guaranteed cash value that grows over time at a steady rate, providing a reliable financial resource for policyholders.

- The accumulation of cash value occurs on a tax-deferred basis, meaning policyholders do not pay taxes on the growth as long as the funds remain within the policy.

- Policyholders can access this accumulated cash value through tax-free policy loans, which can be used for emergencies, supplemental retirement income, or major expenses, without triggering taxable events if structured properly.

Potential for Annual Dividends and Enhanced Returns

- Policyholders of dividend-paying whole life insurance are eligible to receive annual dividends, which are not guaranteed but have been consistently paid by many mutual insurance companies over long periods.

- These dividends can be used in multiple ways: to reduce premiums, purchase additional paid-up insurance, accumulate at interest, or be taken as cash, offering flexibility in financial planning.

- When dividends are used to buy paid-up additions, they compound over time, increasing both the death benefit and the cash value of the policy, thereby enhancing long-term growth.

Lifetime Coverage and Financial Predictability

- Unlike term insurance, dividend-paying whole life insurance provides coverage for the entire life of the insured, as long as premiums are paid, ensuring a guaranteed death benefit for beneficiaries.

- Premiums are fixed and do not increase with age, allowing policyholders to lock in costs and plan their budgets with certainty over decades.

- The policy's structure includes defined benefits and predictable performance, making it a stable component of an overall financial strategy, especially useful in estate planning and wealth transfer.

Why does Dave Ramsey oppose dividend-paying whole life insurance?

High Fees and Commissions in Whole Life Insurance

- Dave Ramsey opposes dividend-paying whole life insurance largely due to the excessive fees and commissions associated with these policies. A significant portion of the premiums paid in the early years goes toward agent commissions, administrative costs, and policy setup rather than building cash value.

- These high costs create a challenging environment for investors to see meaningful returns, especially in the first decade of the policy. Ramsey often emphasizes that it can take 10 to 20 years just to break even on the total amount paid into the policy.

- He argues that such inefficiencies make whole life insurance a poor financial vehicle compared to lower-cost alternatives like term life insurance combined with separate, disciplined investing in mutual funds or index funds.

Misleading Promises of Guaranteed Returns

- Dave Ramsey is skeptical of the way insurance companies market dividend-paying whole life policies, often highlighting guaranteed growth and tax advantages. He contends that dividends are not guaranteed and can be reduced or eliminated by the insurer based on performance.

- Many policyholders are led to believe their cash value will grow predictably over time, but in reality, returns are often lower than projected, especially when compared to historical stock market returns over the long term.

- Ramsey warns that the complexity of these policies can be used to obscure underwhelming performance, leading consumers to overestimate their financial benefit and remain locked into expensive contracts.

Better Alternatives for Wealth Building

- Ramsey strongly advocates for a buy term and invest the difference strategy, where individuals purchase affordable term life insurance and invest the money they save in growth-oriented assets like mutual funds or retirement accounts.

- This approach provides sufficient death benefit protection while allowing for greater flexibility and higher potential returns, aligning with Ramsey's principles of debt-free living and aggressive wealth accumulation.

- He believes that whole life insurance combines insurance and investment in a way that does neither job well, and that separating the two allows for more control, transparency, and efficiency in financial planning.

How to generate $1,000 monthly in passive income with dividend-paying whole life insurance?

Understanding Dividend-Paying Whole Life Insurance as a Passive Income Tool

- Dividend-paying whole life insurance is a type of permanent life insurance that provides lifelong coverage and builds cash value over time. Insurance companies that are mutual (owned by policyholders) may distribute a portion of their profits to policyholders in the form of dividends. These dividends are not guaranteed but have been paid consistently by many well-established insurers for decades.

- Policyholders can choose how to use these dividends: they can be taken as cash, used to reduce premiums, left to accumulate interest, or most relevantly, reinvested to purchase paid-up additional insurance. This last option increases both the death benefit and the cash value of the policy over time, creating a compounding effect.

- Because dividends are derived from the insurer’s performance and not directly tied to market fluctuations, they can provide a relatively stable and predictable supplemental income stream when structured properly. Over time, the cumulative effect of reinvesting dividends can grow the policy's value enough to support withdrawals or policy loans, which can be used as a source of tax-advantaged income.

Steps to Structure a Policy for $1,000 Monthly Passive Income

- To generate $1,000 monthly in passive income (or $12,000 annually) using dividend-paying whole life insurance, you first need to determine the size of the policy required. This depends on dividend performance, your age, health, and how long you plan to let the policy grow. A financial professional can help project the necessary premium and death benefit based on current dividend scales.

- Begin by funding the policy with maximum allowable premiums during the early years, taking advantage of paid-up additions. These additions boost cash value accumulation and increase future dividends. Overfunding within the IRS guidelines helps avoid creating a modified endowment contract (MEC), which would result in less favorable tax treatment.

- After the policy has matured—typically after 10–15 years of consistent premium payments and dividend reinvestment—you can start accessing the cash value through policy loans. These loans are generally income tax-free as long as the policy remains in force. By structuring withdrawals carefully, you can take out approximately $1,000 per month without depleting the principal, allowing the remaining cash value to continue earning dividends.

Key Considerations and Long-Term Planning

- It is essential to work with a knowledgeable advisor who understands infinite banking or similar concepts where whole life insurance is used as a personal financial system. Not all whole life policies are created equal—dividend performance varies significantly between insurance companies. Research and compare historical dividend payouts, financial strength ratings, and expense ratios before selecting a carrier.

- Patience is critical. Whole life insurance is not a short-term investment. The cash value grows slowly in the early years due to front-loaded expenses and costs of insurance. However, after 10 to 15 years, the growth accelerates as the cash value compounds and dividends increase. Expect to wait at least a decade before accessing $1,000 monthly without jeopardizing the policy’s longevity.

- Monitor the policy regularly and adjust over time. Life changes such as shifts in income, health, or financial goals may require modifications. Also, while dividends are not guaranteed, choosing a company with a long history of increasing or stable dividends improves the likelihood of achieving your income target. Properly maintained, a well-structured whole life policy can provide a reliable, tax-efficient stream of passive income for decades.

What is the cash value growth of a $100,000 dividend-paying whole life insurance policy?

Understanding Cash Value Accumulation in a $100,000 Dividend-Paying Whole Life Policy

The cash value growth in a $100,000 dividend-paying whole life insurance policy refers to the portion of the premium payments that accumulates over time on a tax-deferred basis.

This growth is influenced by several variables including the insurer’s performance, dividend payouts, interest crediting rates, and policy expenses. Unlike term policies, whole life insurance includes a savings component where each premium paid contributes to both the death benefit and the cash value.

Dividends, which are not guaranteed, are typically based on the insurer's surplus earnings and can be used to purchase additional paid-up insurance, reduce premiums, or be taken in cash. Over time, the cash value grows predictably according to a schedule outlined in the policy illustration but may increase above that schedule if dividends perform better than projected.

- The cash value grows through a combination of guaranteed and non-guaranteed elements, with guaranteed interest rates set by the insurer and additional growth coming from annual dividends.

- Dividends are not guaranteed but historically have contributed significantly to cash value increases in policies from strong mutual insurers.

- Policyholders can access the cash value through withdrawals or loans, although borrowing may reduce the death benefit and cash surrender value.

Factors That Influence Cash Value Growth Over Time

Several key factors impact how quickly and substantially the cash value in a $100,000 dividend-paying whole life policy accumulates.

Premium payments are initially used to cover administrative and mortality costs, so early cash value growth is typically modest. As the policy ages, a greater portion of each premium goes toward building cash value. The insurer’s dividend scale, which reflects its claims experience, investment returns, and operating costs, also plays a major role.

Higher dividends allow for the purchase of paid-up additions, which in turn generate more dividends and compound growth. Additionally, the policy’s design—such as whether it's a 10-pay, 20-pay, or lifetime pay—will affect the funding pattern and, consequently, the growth trajectory of the cash value.

- The method and duration of premium payments affect how quickly cash value builds, with shorter pay periods often leading to faster accumulation.

- Insurer financial strength and consistent dividend performance can enhance long-term cash value growth beyond minimum guarantees.

- Policy loans and withdrawals impact the compounding effect since borrowed amounts may reduce dividend earnings and overall cash value growth.

Illustrating Projected vs. Actual Cash Value Performance

Insurance companies provide policy illustrations that project the expected cash value growth of a $100,000 dividend-paying whole life policy based on guaranteed and non-guaranteed assumptions.

These illustrations typically include a low-end scenario using only guaranteed values and a higher projection incorporating non-guaranteed dividends. Over decades, actual performance may vary depending on how well the insurer meets its dividend payouts.

If dividends remain consistent with historical levels, the cash value can grow significantly—sometimes doubling or more over a 30- to 40-year period. However, it's essential to understand that changes in dividend scales, fee structures, or economic conditions may result in actual growth differing from initial projections.

- Policy illustrations show both guaranteed and non-guaranteed growth scenarios, with the latter being dependent on the insurer's future financial performance.

- Historical dividend performance of mutual life insurers provides insight into how closely projected cash values may align with actual outcomes.

- Reviewing dividend history and insurer stability helps policyholders assess the likelihood that projected cash value growth will be realized over the long term.

Frequently Asked Questions

What is Whole Life Dividend Paying Insurance?

Whole Life Dividend Paying Insurance is a permanent life insurance policy that offers lifelong coverage and builds cash value over time. Policyholders may receive dividends, which are portions of the insurer’s profits, though they are not guaranteed. These dividends can be used to reduce premiums, purchase additional coverage, or accumulate cash value. The policy combines death benefit protection with potential financial growth, making it a long-term financial planning tool.

How do dividends work in Whole Life Insurance?

Dividends in Whole Life Insurance are returns of excess premiums based on the insurer’s performance, including mortality, expenses, and investment results. While not guaranteed, they are typically paid annually. Policyholders can choose how to use them—such as receiving cash, reducing premiums, or buying paid-up additions. These options enhance the policy’s value over time. Dividends do not equate to investment income and are generally not taxed if kept within the policy.

Is the cash value in Whole Life Dividend Paying Insurance accessible?

Yes, the cash value in Whole Life Dividend Paying Insurance grows tax-deferred and can be accessed during the policyholder’s lifetime. You can withdraw funds or take loans against the cash value, which may affect the death benefit if not repaid. Withdrawals up to the amount of premiums paid are typically tax-free. The cash value serves as a financial resource for emergencies, retirement, or other needs, adding flexibility to the policy as a wealth-building tool.

Can I lose money with Whole Life Dividend Paying Insurance?

Generally, you won’t lose money in a Whole Life Dividend Paying Insurance policy if managed properly. Premiums are fixed, and the cash value is guaranteed not to decrease. However, early surrender may result in surrender charges and loss of benefits. Loans exceeding the cash value can reduce or eliminate the death benefit. While dividends are not guaranteed, the core value of the policy remains protected, making it a low-risk, long-term financial instrument.

Leave a Reply