Find An Agent Commercial Auto Insurance In Vermont

Finding the right commercial auto insurance in Vermont requires partnering with a knowledgeable agent who understands state regulations and industry risks. With strict liability requirements and varying coverage needs across businesses, selecting an experienced agent is crucial.

A qualified professional can assess your fleet's unique demands, offer tailored policies, and help reduce premiums through proper risk management. Whether you operate a trucking company, delivery service, or local contracting business, the right agent will provide comprehensive protection against accidents, damages, and liability claims. In Vermont’s competitive insurance market, access to an agent with strong carrier relationships ensures better options and faster claims support.

How to Find a Trusted Commercial Auto Insurance Agent in Vermont

Finding the right commercial auto insurance agent in Vermont is a crucial step for businesses that rely on vehicles for operations. Whether you operate a delivery service, construction company, or transportation business, having adequate coverage reduces risk and protects your assets.

Auto Insurance For Kia

Auto Insurance For KiaA knowledgeable agent will understand Vermont’s specific regulations, provide tailored policy options, and assist in claims processes when needed. To ensure you're working with a qualified professional, it’s best to seek agents who are licensed in Vermont, have experience with commercial fleets, and carry strong client reviews.

Many insurance providers have local offices across the state, including in cities like Burlington, Montpelier, and Rutland, making it easier to find personalized service. Additionally, using online directories like the Vermont Department of Financial Regulation’s licensed agent search tool can help verify credentials and streamline your search.

Understanding Commercial Auto Insurance Requirements in Vermont

In Vermont, commercial auto insurance is mandatory for any vehicle used for business purposes, and the coverage requirements exceed personal auto policies in both scope and liability limits.

The minimum liability coverage required by the state is $25,000 for bodily injury per person, $50,000 per accident, and $10,000 for property damage, but businesses often need higher limits depending on fleet size and vehicle use. Policies typically include coverage for liability, physical damage (comprehensive and collision), uninsured/underinsured motorists, and medical payments.

Auto Insurance Hickory Nc 28602

Auto Insurance Hickory Nc 28602Commercial policies may also offer additional protections such as cargo insurance, garage keeper’s coverage, and Hired and Non-Owned Auto (HNOA) insurance for employees using personal vehicles for work. An experienced agent can help determine which coverages are essential based on your industry and operations, ensuring full compliance with Vermont law and minimizing financial exposure.

| Coverage Type | Description | Importance |

|---|---|---|

| Liability Insurance | Covers injuries and damages caused to others in an accident where your business is at fault. | Required by Vermont law; protects against costly lawsuits. |

| Physical Damage Coverage | Includes collision and comprehensive coverage for business-owned vehicles. | Protects your investment in company vehicles from theft, weather, or accidents. |

| Hired & Non-Owned Auto (HNOA) | Provides liability coverage for employees driving rental or personal vehicles for business. | Often overlooked but essential for full risk management. |

Where to Find Licensed Commercial Auto Insurance Agents in Vermont

To find licensed commercial auto insurance agents in Vermont, start by checking the Vermont Department of Financial Regulation (DFR) website, which offers a searchable database to verify agents’ credentials and licensing status.

Many national insurance providers, such as Nationwide, State Farm, and The Hartford, have local agents throughout Vermont who specialize in commercial policies. Additionally, independent insurance agencies often represent multiple carriers, giving you access to broader options and competitive pricing.

Business associations like the Chambers of Commerce in cities like South Burlington or St. Johnsbury may also provide referrals based on member feedback. Online platforms such as the Independent Insurance Agents & Brokers of America (IIABA) or Insurify can help narrow your search by location and business type, allowing you to compare agents based on expertise, customer service, and industry focus.

Auto Insurance Hurst

Auto Insurance HurstKey Questions to Ask When Choosing an Insurance Agent

When evaluating potential commercial auto insurance agents in Vermont, it’s vital to ask the right questions to ensure they understand your business needs. Begin by asking about their experience with businesses in your industry, as an agent familiar with construction or logistics, for example, will be better equipped to customize coverage.

Inquire whether they represent multiple insurance carriers or are captive to one, as this affects your ability to compare quotes. Also ask about their claims support process, especially response times and assistance during emergencies.

Transparency about fees, policy renewal terms, and available discounts (like safe driver programs or fleet safety training) is another indicator of a reliable agent. Finally, request client references or read online reviews to assess satisfaction and service quality. Selecting an agent who communicates clearly and proactively will make managing your insurance significantly smoother.

How to Find a Commercial Auto Insurance Agent in Vermont

What is the most affordable commercial auto insurance in Vermont, and how can I find a local agent?

Auto Insurance In Miami

Auto Insurance In MiamiTop Affordable Commercial Auto Insurance Providers in Vermont

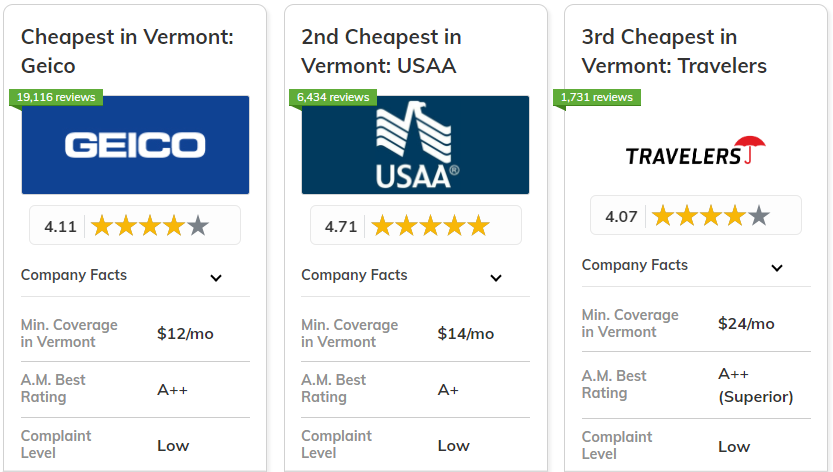

- Progressive Commercial is frequently recognized for offering competitive rates for small businesses and independent contractors in Vermont. They provide customizable policies based on vehicle type, driving history, and annual mileage, which can help lower premiums for low-risk operations.

- GEICO Commercial Insurance is another cost-effective option, especially for businesses with clean driving records and minimal claims history. GEICO leverages its large customer base and online tools to streamline policy pricing and management, often translating into lower costs for Vermont business owners.

- The Hartford is known for its strong reputation in small business insurance and often provides affordable bundled packages that include commercial auto coverage. Their risk assessment model considers business size and industry type, allowing for tailored pricing that can be particularly advantageous for local Vermont enterprises.

How to Compare Commercial Auto Insurance Quotes in Vermont

- Start by collecting quotes from at least three providers either directly through their websites or via online insurance comparison platforms. Ensure that each quote covers the same level of liability, comprehensive, and collision coverage to make an accurate comparison.

- Ask about available discounts such as multi-policy bundling, safe driver incentives, or paperless billing savings. Many insurers in Vermont offer reductions for fleets with GPS tracking or employee driver training programs.

- Review customer feedback and financial stability ratings from sources like A.M. Best or the Better Business Bureau. A cheaper policy may not be worth it if the insurer has a history of slow claims processing or poor service during emergencies.

How to Find a Local Commercial Insurance Agent in Vermont

- Use the Vermont Department of Financial Regulation’s licensed agent database to search for agents authorized to sell commercial auto insurance. You can filter by city, zip code, and agency name to locate professionals near your business location.

- Contact local business associations such as the Vermont Chamber of Commerce or regional Small Business Development Centers (SBDCs). They often maintain lists of recommended insurance providers with experience serving local industries.

- Ask for referrals from other business owners in your network, especially those with similar vehicle usage needs. A recommendation from a trusted peer can connect you with an agent who offers personalized service and a deep understanding of Vermont's regulatory environment.

What Factors Influence Commercial Auto Insurance Costs in Vermont?

Vehicle Type and Usage

- The type of vehicle used for commercial purposes significantly impacts insurance premiums in Vermont. For example, large trucks, delivery vans, or vehicles carrying hazardous materials are considered higher risk and therefore cost more to insure compared to smaller passenger vehicles used for business travel.

- How the vehicle is used—such as delivery, transportation of goods, or client visits—affects exposure to risk. Vehicles that accumulate high annual mileage or operate in densely populated areas face increased chances of accidents, leading to higher insurance costs.

- Specialized equipment installed in the vehicle, such as lifts or refrigeration units, may also raise the cost of coverage due to increased liability and repair expenses in the event of a claim.

Driving Records and Operator Experience

- Insurance providers in Vermont closely examine the driving records of all individuals who operate a commercial vehicle. A history of accidents, traffic violations, or DUI offenses results in significantly higher premiums due to the perceived increase in risk.

- The experience level of drivers plays an essential role as well. Drivers with extensive experience and clean records are typically offered lower rates, as they are statistically less likely to be involved in accidents.

- Companies that implement driver training programs and regular performance reviews are often viewed more favorably by insurers, which may lead to reduced premiums through experience modification credits or safety discounts.

Business Location and Coverage Requirements

- The geographic location of a business within Vermont influences insurance costs due to differences in traffic density, accident rates, and weather conditions. Businesses operating in urban centers like Burlington face higher premiums than those in rural areas with less congestion and lower collision frequencies.

- State-mandated minimum coverage limits play a foundational role in determining base premiums. However, most commercial policies exceed these minimums, and the selected limits for liability, collision, and comprehensive coverage directly affect the overall cost.

- Additional coverages such as cargo insurance, uninsured motorist protection, or garage liability may be necessary depending on the nature of the business, leading to an increase in the total policy cost based on coverage scope and industry-specific risks.

What is the leading commercial auto insurance provider in Vermont?

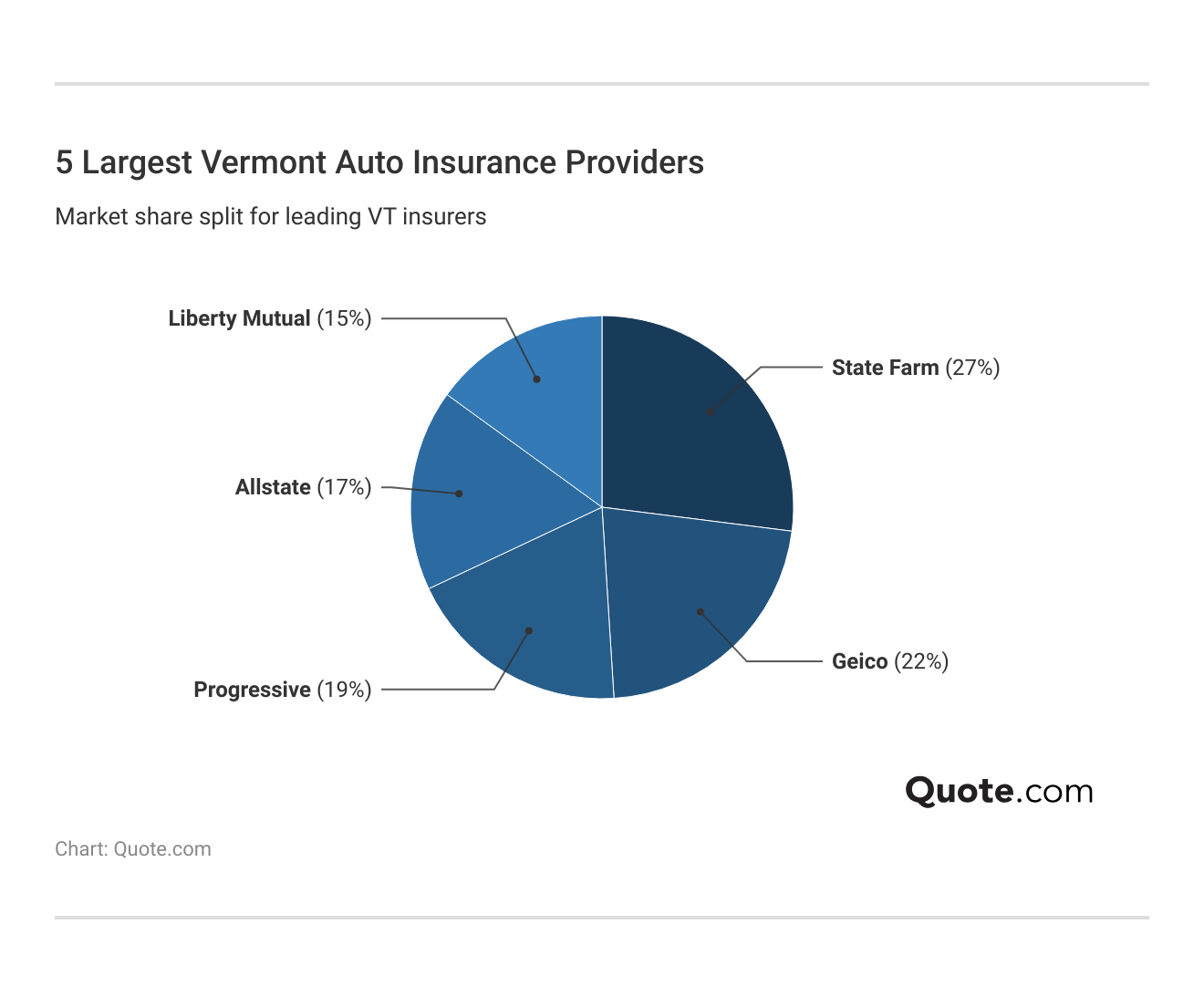

The leading commercial auto insurance provider in Vermont is State Farm. With a strong presence across the United States, State Farm consistently ranks at the top in terms of market share and customer base in the commercial auto insurance sector within the state.

Its extensive network of local agents, competitive pricing, and comprehensive coverage options make it a preferred choice for small and mid-sized businesses operating commercial vehicles. State Farm offers customizable policies that can include liability, collision, comprehensive, medical payments, and uninsured motorist coverage, tailored to meet the specific needs of diverse industries.

Factors That Contribute to State Farm's Market Leadership in Vermont

- State Farm's widespread agent network ensures local, personalized service for Vermont businesses, allowing policyholders to receive face-to-face support and tailored advice based on regional driving conditions and regulatory requirements.

- The company leverages advanced data analytics and risk assessment tools to offer competitive premiums, making its commercial auto policies accessible to a broad range of business types, including delivery services, contractors, and transportation providers.

- State Farm consistently receives high customer satisfaction ratings due to its efficient claims processing, digital tools for policy management, and responsiveness during emergencies, which contribute to its strong reputation in Vermont’s insurance market.

Alternatives to State Farm for Commercial Auto Insurance in Vermont

- Progressive Commercial is a major competitor, known for its specialized offerings for high-risk drivers and a wide variety of business classifications, along with tools like online quoting and fleet management services that appeal to growing businesses.

- GEICO Commercial provides cost-effective solutions for small businesses, with quick online applications and strong customer service, making it a popular alternative, especially for companies seeking straightforward coverage at competitive rates.

- The Hartford ranks highly among insurers serving small businesses, offering integrated packages that combine commercial auto with other liability protections, as well as risk management resources beneficial for safety-conscious companies in Vermont.

Regulatory and Market Conditions Influencing Commercial Auto Insurance in Vermont

- Vermont’s Department of Financial Regulation closely oversees insurance providers, ensuring compliance with state laws, which encourages transparency and stability, helping established national carriers like State Farm operate effectively within the state.

- Winter weather conditions and rural road networks in Vermont increase certain driving risks, leading insurers to emphasize safety programs and driver training incentives—features that State Farm has integrated into its commercial offerings.

- The relatively small number of commercial vehicle registrations in Vermont compared to larger states means insurers focus on building strong client relationships rather than competing solely on volume, benefiting providers with a local service model like State Farm.

Frequently Asked Questions

How can I find a reliable commercial auto insurance agent in Vermont?

To find a reliable commercial auto insurance agent in Vermont, start by searching online through state-licensed insurance directories or the Vermont Department of Financial Regulation website. Look for agents with positive reviews, proper licensing, and experience in commercial policies. Ask for referrals from other business owners and request personalized quotes to compare coverage and service quality.

What should I look for in a commercial auto insurance agent?

Choose a commercial auto insurance agent with strong industry experience, excellent customer reviews, and valid Vermont licensing. Ensure they represent multiple insurers to offer competitive rates and tailored policies. Effective communication, responsiveness, and knowledge of local regulations are key. Ask about their claims support and whether they specialize in your business type to ensure they meet your specific needs.

Do I need commercial auto insurance for my business vehicles in Vermont?

Yes, Vermont law requires businesses to have commercial auto insurance for vehicles used for work purposes. Personal policies don’t cover business-related accidents or liabilities. Commercial insurance protects against property damage, bodily injury, and medical payments. It also covers legal expenses and offers higher liability limits, ensuring your business remains compliant and protected from financial risks.

Can I compare commercial auto insurance quotes online in Vermont?

Yes, you can compare commercial auto insurance quotes online in Vermont through licensed insurance portals or by contacting multiple agents directly. Online tools allow side-by-side comparisons of coverage options, premiums, and deductibles. However, it's wise to consult an agent to ensure all business-specific risks are accurately assessed and included in the quotes for comprehensive protection.

Leave a Reply