Auto Insurance In Miami

Auto insurance in Miami is essential for all drivers navigating the city’s busy streets and unpredictable traffic patterns. With high population density, frequent accidents, and increased risks of weather-related damages, having reliable coverage is more than a legal requirement—it's a financial safeguard.

Miami’s unique urban environment, combined with its coastal location, leads to higher premiums compared to other parts of Florida. Drivers must consider factors like theft rates, flood risks, and uninsured motorists when choosing a policy. Understanding the available options, from liability to comprehensive plans, helps ensure adequate protection on the road.

Understanding Auto Insurance in Miami: What Drivers Need to Know

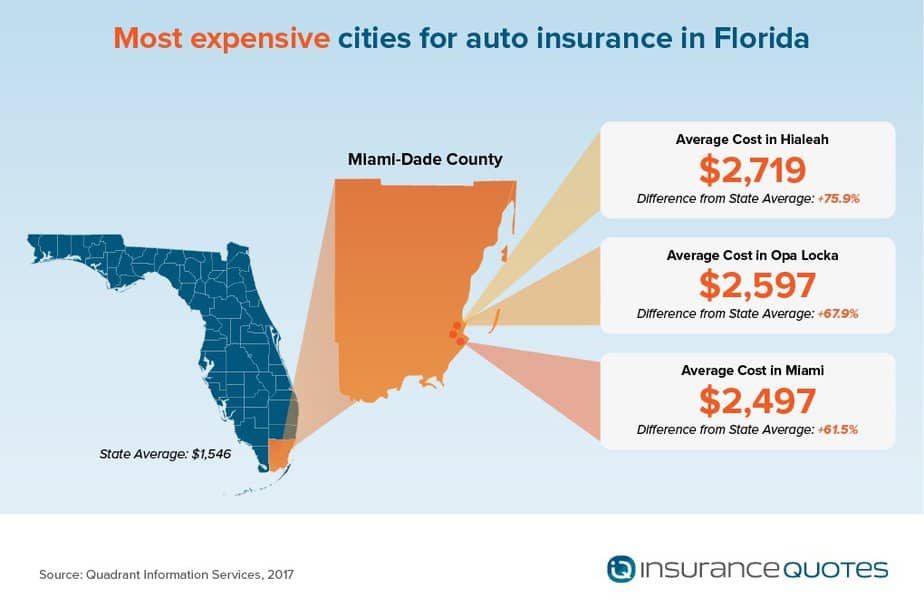

Miami's unique urban environment, combined with high population density, frequent tropical weather, and heavy tourist traffic, creates a complex landscape for auto insurance. Drivers in Miami face some of the highest car insurance premiums in Florida due to elevated risks such as accidents, theft, and hurricane-related damages.

When should adult child at home get own car insurance

When should adult child at home get own car insuranceState law mandates minimum coverage, including personal injury protection (PIP) and property damage liability (PDL), but many drivers opt for additional coverage to protect against uninsured motorists, flooding, and comprehensive risks. Understanding the local factors that influence policy pricing—such as ZIP code, driving record, and vehicle type—is essential for securing adequate and cost-effective insurance in Miami.

Factors That Influence Auto Insurance Rates in Miami

Auto insurance premiums in Miami are significantly affected by a combination of demographic, environmental, and behavioral factors.

The city consistently reports high rates of uninsured drivers, frequent accidents, and insurance fraud, all of which contribute to increased costs for policyholders. Urban congestion leads to more collisions, while Miami’s susceptibility to hurricanes and flooding raises the likelihood of vehicle damage, prompting insurers to adjust premiums accordingly.

Additionally, areas with higher vehicle theft rates—like Miami-Dade County—often see elevated comprehensive coverage costs. Insurers also consider individual metrics such as credit score, driving history, and commute distance, making it crucial for drivers to compare quotes and maintain clean records to secure better rates.

Who offers the best unoccupied home insurance in the uk

Who offers the best unoccupied home insurance in the ukRequired Coverage and Legal Compliance

Florida operates under a no-fault insurance system, which means that drivers must carry Personal Injury Protection (PIP) and Property Damage Liability (PDL) regardless of who causes an accident. In Miami, the state-mandated minimums are $10,000 in PIP coverage and $10,000 in PDL coverage.

PIP covers medical expenses and lost wages for the driver and passengers, no matter who is at fault, while PDL covers damage the insured causes to another person’s property. Failure to maintain these minimums can result in penalties such as license suspension, vehicle registration revocation, and fines.

Although Florida does not require bodily injury liability (BIL) coverage, many drivers choose to add it voluntarily due to the high risk of costly lawsuits following serious accidents in busy metropolitan areas like Miami.

Optional Coverages to Consider for Miami Drivers

Given Miami’s specific risks, drivers should strongly consider adding optional coverages to their policies for enhanced protection. Comprehensive coverage safeguards against non-collision incidents such as theft, vandalism, and hurricane-related flooding, which are common in coastal regions.

Wichita home insurance cost

Wichita home insurance costUninsured/Underinsured Motorist Coverage (UM/UIM) is also highly recommended due to the city’s high number of drivers operating without adequate insurance. Collision coverage helps pay for repairs after accidents, regardless of fault, and is especially valuable for owners of newer or high-value vehicles.

Additionally, rental reimbursement and roadside assistance can be practical additions, considering Miami’s traffic congestion and vehicle breakdown risks during hot, humid conditions. These optional protections may increase premiums slightly but offer substantial financial security in emergency situations.

| Coverage Type | State Minimum (Florida) | Recommended for Miami Drivers | Key Benefits |

|---|---|---|---|

| Personal Injury Protection (PIP) | $10,000 | Yes | Covers medical expenses and lost wages regardless of fault |

| Property Damage Liability (PDL) | $10,000 | Yes | Pays for damage to others' property caused by the insured |

| Uninsured/Underinsured Motorist (UM/UIM) | Not required | Highly Recommended | Protects if hit by a driver with no or insufficient insurance |

| Comprehensive Coverage | Not required | Highly Recommended | Covers theft, flood damage, and natural disasters common in Miami |

| Collision Coverage | Not required | Recommended for newer vehicles | Covers repair or replacement after accidents |

Comprehensive Guide to Auto Insurance in Miami: Coverage Options and Local Requirements

Why is auto insurance in Miami more expensive than in other cities?

Frequent Accidents and High Traffic Density

Auto insurance in Miami is significantly higher due to the region's extremely high volume of traffic and the frequency of car accidents.

As one of the most densely populated urban areas in Florida, Miami experiences constant congestion on major roadways such as I-95 and the Palmetto Expressway. This persistent flow of vehicles increases the probability of collisions, including fender benders, rear-end crashes, and more serious multi-vehicle incidents.

Insurance companies use historical accident data to determine risk, and Miami consistently ranks among the top U.S. cities for traffic congestion and accident rates. As a result, insurers charge higher premiums to offset the increased likelihood of claims.

- Heavy daily commuter traffic from residents and tourists contributes to accident-prone conditions on Miami roads.

- Intersections such as those around Brickell and Downtown Miami are particularly notorious for crashes.

- Higher accident frequency leads insurers to anticipate more claims, driving up premiums citywide.

High Rates of Insurance Fraud

Miami is widely recognized not only within Florida but across the nation for having one of the highest rates of auto insurance fraud. Fraudulent activities such as staged accidents, exaggerated injuries, and false claims dramatically impact insurance costs for honest policyholders. These deceptive practices increase the overall amount insurers must pay out annually, leading them to raise rates to maintain financial stability.

The presence of organized fraud rings operating in South Florida allows for complex scams that are difficult to detect, forcing insurance companies to account for these elevated risks when pricing policies. Regulatory and law enforcement efforts have been ongoing, but the financial damage has already been integrated into pricing models.

- Staged crashes involving multiple vehicles are common, with fraudsters deliberately causing collisions to claim medical and property damages.

- Medical clinics and lawyers sometimes collaborate in fraudulent schemes to inflate injury claims.

- Insurers factor in the regional fraud rate when setting Miami-specific premiums, making coverage more expensive for all drivers.

Urban Theft, Vandalism, and Weather Risks

Miami's metropolitan environment presents a higher exposure to vehicle theft, vandalism, and damage caused by extreme weather events. As a coastal city, it faces regular threats from hurricanes, tropical storms, and flooding, which can lead to widespread auto damage and subsequent insurance claims.

Additionally, certain neighborhoods experience higher rates of car theft and property crimes, increasing the cost of comprehensive coverage. Unlike rural or suburban areas, urban centers like Miami concentrate more insured vehicles in smaller geographic zones, magnifying the insurer's exposure during disasters or crime spikes. These combined environmental and criminal risks make Miami a high-cost zone for insuring vehicles.

- Hurricane season brings a surge in claims related to flood-damaged vehicles, prompting insurers to raise base rates.

- Areas like Liberty City and Overtown report above-average vehicle theft rates, which influence comprehensive premiums.

- Dense urban infrastructure limits safe parking options, increasing exposure to both weather and vandalism-related claims.

What is the most affordable auto insurance provider in Miami, Florida?

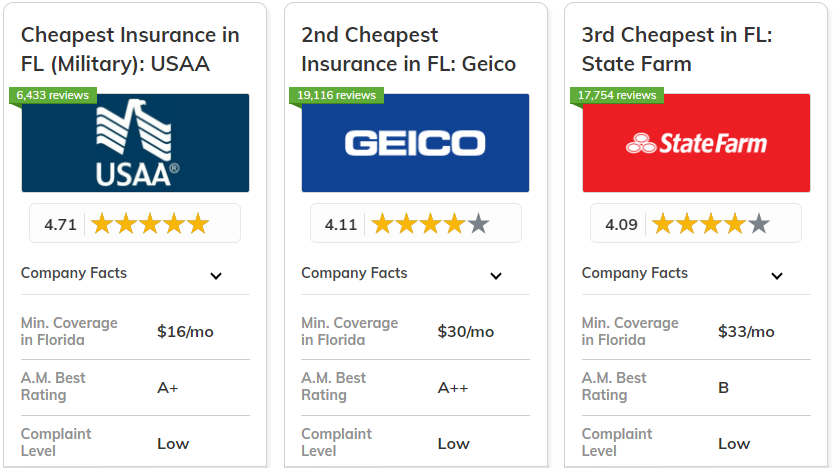

Top Budget-Friendly Auto Insurance Providers in Miami

When searching for the most affordable auto insurance in Miami, Florida, several providers consistently rank at the top for offering competitive rates.

State Farm is often recognized as one of the most affordable options in the area, thanks to its wide range of discounts, strong local agent presence, and personalized service. GEICO is another popular choice, known for its online tools and low base premiums, especially for drivers with clean records.

Additionally, Progressive stands out for its rate comparison tool, which allows customers to benchmark prices across multiple insurers. These companies use diverse pricing models, so affordability can depend heavily on individual factors such as driving history, vehicle type, and coverage levels.

- State Farm frequently offers some of the lowest average rates in Miami, particularly for long-term customers and those bundling home and auto insurance.

- GEICO provides accessible pricing for low-risk drivers and features tools like fuel-efficient vehicle discounts and paperless billing incentives.

- Progressive competes through its Price Comparison tool, enabling users to view side-by-side quotes and select the most economical option tailored to their needs.

Factors That Influence Insurance Costs in Miami

Auto insurance rates in Miami are influenced by various region-specific factors that can either increase or decrease affordability. The city’s high population density and traffic congestion contribute to more frequent accidents and claims, which raises premiums across the board.

Additionally, Miami has a notable rate of insurance fraud, leading insurers to adjust prices accordingly. Personal factors such as age, credit score, and driving record also play a crucial role; younger drivers or those with prior infractions typically pay higher premiums.

Moreover, the type of vehicle insured—especially high-theft or high-performance models—can significantly affect cost. Choosing a higher deductible is one way drivers can lower their monthly premiums, though it increases out-of-pocket expenses in the event of a claim.

- Urban driving conditions in Miami, including congestion and accident frequency, are key reasons for elevated base insurance rates compared to rural areas in Florida.

- Insurance fraud, especially in the form of staged accidents and inflated claims, leads insurers to maintain higher prices to offset risk exposure.

- Personal variables like credit history, years of driving experience, and prior claims or violations are major determinants of individual premium costs.

How to Find the Cheapest Rate for Your Profile

Securing the most affordable auto insurance in Miami requires a customized approach, as the cheapest provider for one person may not be the best for another.

The most effective method is to obtain and compare multiple quotes from top insurers, either directly through their websites or via independent comparison platforms. It's essential to ensure that the coverage limits and deductibles are identical when comparing quotes to make an accurate assessment.

Additionally, taking advantage of available discounts—such as safe driver rewards, multi-policy bundling, and electronic funds transfer savings—can reduce costs significantly. Maintaining a clean driving record and improving your credit score over time are long-term strategies that help secure lower rates.

- Compare quotes from at least three to five insurers to understand the competitive landscape and identify potential savings based on your risk profile.

- Check for available discounts, such as defensive driving course completion, low annual mileage, or affiliation-based programs (e.g., alumni or employer groups).

- Review your policy annually and consider adjusting coverage levels or switching providers if life circumstances change, such as improved credit or a safer vehicle purchase.

Is $200 Monthly Considered Expensive for Auto Insurance in Miami?

Factors That Influence Auto Insurance Rates in Miami

- Miami's high population density and heavy traffic congestion significantly contribute to the increased likelihood of accidents, which in turn drives up insurance premiums. Areas with more vehicles on the road tend to experience more collisions and claims, prompting insurers to adjust rates to reflect this elevated risk.

- The prevalence of insurance fraud in South Florida, particularly staged accidents and inflated claims, is another key factor pushing auto insurance costs higher. Insurers account for these fraudulent activities by charging higher premiums across the board to mitigate financial losses.

- Additionally, the cost of living in Miami influences repair and medical expenses, both of which are factored into insurance calculations. Higher labor and material costs, combined with expensive healthcare, mean that claims settlements are costlier, leading to more expensive monthly premiums for drivers.

How $200 Monthly Compares to Florida and National Averages

- The average monthly cost of auto insurance in Florida is approximately $180 to $200, placing $200 per month at or slightly above the state average. However, regional differences within Florida are significant, with urban areas like Miami typically exceeding the statewide mean due to higher risks and living costs.

- Nationwide, the average cost of auto insurance is closer to $130 to $150 per month, meaning $200 is notably higher than what most Americans pay. This disparity highlights how location-specific risks in Miami elevate insurance costs compared to less densely populated or lower-risk areas.

- When evaluating whether $200 is expensive, it’s important to consider coverage level. Minimum liability coverage is cheaper, but full coverage (which includes collision and comprehensive protection) often pushes monthly costs toward or beyond $200 in high-risk urban zones like Miami.

Ways Miami Drivers Can Reduce Their Insurance Costs

- Shopping around and comparing quotes from multiple insurers can lead to substantial savings. Rates vary widely between providers due to different risk assessments and underwriting models, so obtaining several quotes helps drivers find competitive pricing even in a high-cost region.

- Taking advantage of available discounts—such as safe driver programs, multi-policy bundling, or low-mileage incentives—can lower monthly premiums. Many insurers offer discounts that are underutilized, and qualifying for even a few can reduce a $200 monthly payment significantly.

- Maintaining a clean driving record and improving credit scores, where applicable, are long-term strategies that gradually reduce insurance costs. Insurers view drivers with fewer infractions and better credit as lower risks, making them eligible for lower rates over time.

Frequently Asked Questions

Why is auto insurance more expensive in Miami compared to other cities?

Auto insurance in Miami tends to be more expensive due to high traffic congestion, frequent accidents, and elevated rates of insurance fraud. The city’s dense population and year-round tourism contribute to increased accident risks.

Additionally, Miami has a high rate of uninsured drivers and vehicle thefts. Insurers factor in these risks when calculating premiums, leading to higher costs for policyholders compared to other regions in Florida or the U.S.

What minimum auto insurance coverage is required in Miami?

In Miami, Florida law requires drivers to carry at least $10,000 in personal injury protection (PIP) and $10,000 in property damage liability (PDL) coverage.

This no-fault insurance system means drivers must first use their own PIP coverage for medical expenses after an accident, regardless of fault. While these are the minimum requirements, experts recommend higher coverage limits to ensure better financial protection in case of severe accidents or lawsuits.

How can I lower my auto insurance rates in Miami?

You can lower your auto insurance rates in Miami by maintaining a clean driving record, taking defensive driving courses, and bundling policies with the same insurer. Installing safety and anti-theft devices in your vehicle may also qualify you for discounts.

Additionally, increasing your deductible can reduce premiums, though it means higher out-of-pocket costs in case of a claim. Regularly comparing quotes from different insurers helps find the most affordable option.

Yes, auto insurance in Miami covers hurricane-related damages, but only if you have comprehensive coverage. Standard liability policies do not cover weather-related damage such as flooding or fallen trees.

Comprehensive coverage protects against non-collision incidents, including hurricanes, storms, and water damage. Since Miami is prone to hurricanes, it’s highly recommended to carry comprehensive coverage to protect your vehicle from natural disasters.

Leave a Reply