Flood insurance for home

Flood insurance for homeowners is an essential safeguard often overlooked until disaster strikes. Unlike standard homeowners' insurance, typical policies exclude flood damage, leaving many vulnerable when rising waters hit.

Whether living in a high-risk flood zone or a moderate-to-low-risk area, unexpected flooding can result from storms, hurricanes, or even gradual water accumulation. Federally backed flood insurance, primarily offered through the National Flood Insurance Program (NFIP), provides financial protection for both property structures and personal belongings.

Understanding coverage limits, policy options, and the real risks involved helps homeowners make informed decisions. Investing in flood insurance isn’t just about compliance—it’s a crucial step in protecting one’s home and financial future.

Pail Revere Life Insurance Polocys

Pail Revere Life Insurance PolocysUnderstanding Flood Insurance for Homeowners: What You Need to Know

Flood insurance is a crucial yet often overlooked aspect of protecting your home and financial well-being. Unlike standard homeowners insurance, which typically excludes coverage for flood damage, a separate flood insurance policy is required to safeguard your property from rising water due to storms, hurricanes, overflowing rivers, or other flood events.

This type of insurance is particularly important for homeowners in high-risk flood zones, although flooding can occur anywhere due to extreme weather or infrastructure failures.

The National Flood Insurance Program (NFIP), administered by the Federal Emergency Management Agency (FEMA), is the primary source for flood coverage in the United States, although private insurers also offer alternative policies. Understanding the terms, coverage limits, and claims process can help you make informed decisions and avoid costly surprises after a flood event.

What Does Flood Insurance Cover?

Flood insurance typically provides two types of coverage: building property and personal property. Building property coverage protects the structure of your home, including the foundation, electrical and plumbing systems, built-in appliances, and wall-to-wall carpeting. It also covers debris removal and essential structural elements like staircases and cabinets.

Pls Provide Top 5 Life Insurance Companies Rewarding Healthy Behaviors

Pls Provide Top 5 Life Insurance Companies Rewarding Healthy BehaviorsOn the other hand, personal property coverage addresses your belongings—such as clothing, furniture, electronics, and certain valuables—up to the policy’s specified limits. However, there are exclusions: flood insurance generally does not cover damage caused by moisture, mold, or mildew that could have been avoided, currency, precious metals, or vehicles.

Additionally, basements are covered only for structural elements and essential equipment, not for finished walls or stored personal items. Knowing exactly what is and isn’t covered helps homeowners set realistic expectations and consider supplemental protection if needed.

Who Needs Flood Insurance?

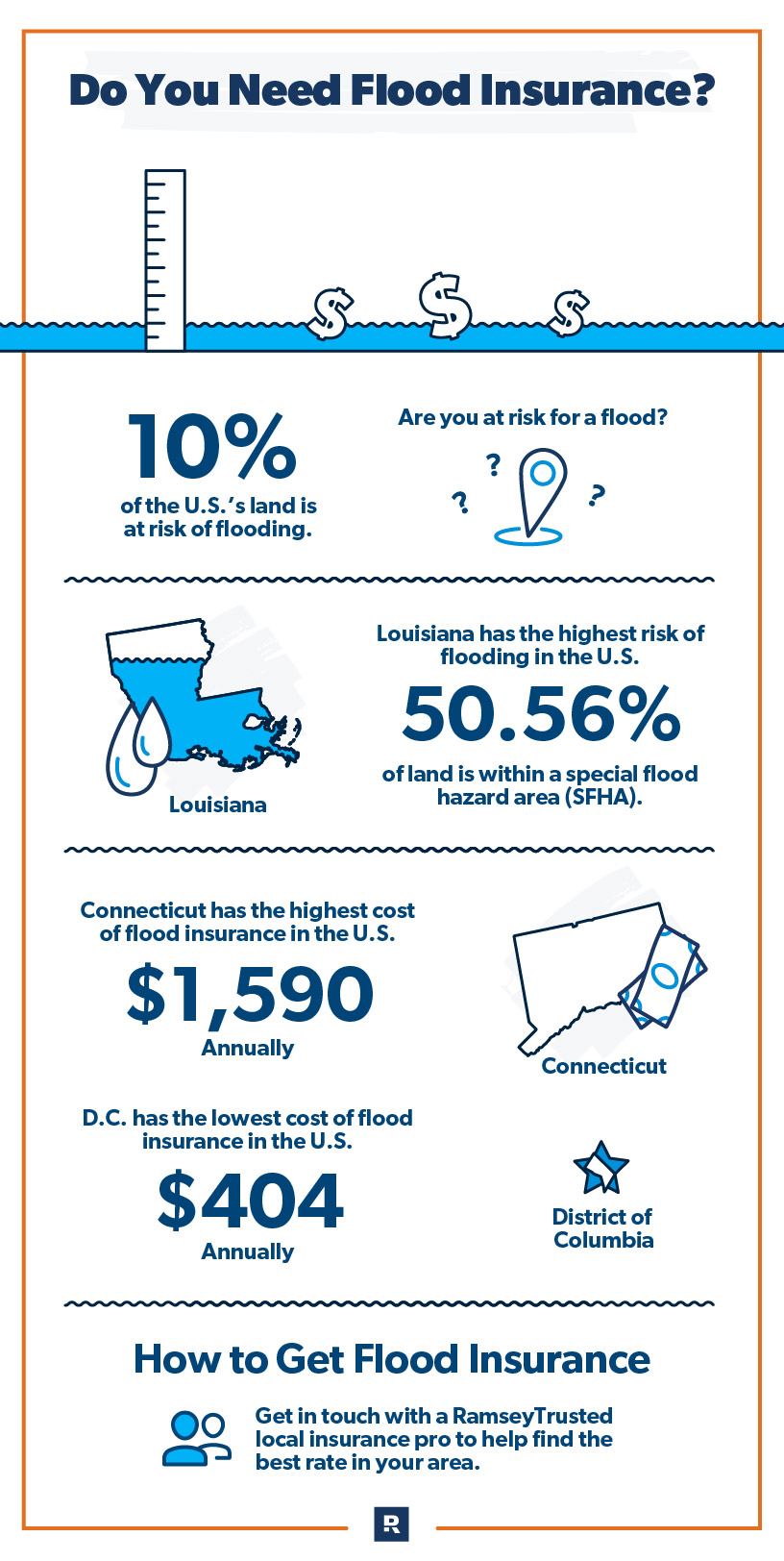

While flood insurance is often mandatory for homeowners with mortgages in high-risk flood areas—specifically those designated as Special Flood Hazard Areas (SFHAs) by FEMA—any homeowner can benefit from having a policy. Over 20% of flood claims come from properties outside high-risk zones, underscoring that flooding is not just a coastal or riverfront issue.

Climate change, urban development, and aging infrastructure are increasing flood risks even in traditionally low-risk regions. Renters, too, should consider coverage—while they won’t need building coverage, a flood insurance policy can protect their personal belongings.

Premium Life Insurance Quote

Premium Life Insurance QuoteEven if your lender doesn’t require it, purchasing flood insurance is a smart financial decision, especially if you live near bodies of water or in areas prone to heavy rainfall. The cost is often far less than the cost of repairs after a single flood event.

How to Obtain and Afford Flood Insurance

Obtaining flood insurance is typically done through the National Flood Insurance Program (NFIP) via an authorized insurance agent, although private insurers now offer competitive alternatives, especially for those seeking higher coverage limits or better terms.

The process usually begins with determining your property’s flood risk using a FEMA Flood Map, which can be accessed online. Premiums are based on several factors, including your home’s location, flood zone classification, elevation, age of the structure, and chosen coverage amount. Most NFIP policies have a 30-day waiting period before they become effective, so it’s wise not to wait until a storm approaches.

To make coverage more affordable, consider mitigation efforts such as elevating your home, installing flood barriers, or choosing a higher deductible. Some communities participate in FEMA’s Community Rating System (CRS), which offers premium discounts for areas engaged in floodplain management.

Sayings About Life Insurance

Sayings About Life Insurance| Insurance Feature | NFIP Standard Coverage | Private Market Options |

|---|---|---|

| Building Coverage Limit | Up to $250,000 | Often up to $500,000 or more |

| Personal Property Limit | Up to $100,000 | Higher limits available |

| Waiting Period | 30 days (standard) | May offer shorter periods |

| Coverage for Valuables | Limited (e.g., $2,500 for art) | Better coverage for high-value items |

| Premium Discounts | Available through CRS communities | Variants based on risk mitigation |

Comprehensive Guide to Flood Insurance for Homeowners

What is the average cost of home flood insurance?

Factors That Influence Flood Insurance Costs

- One of the primary factors affecting the average cost of home flood insurance is the property's location and flood risk zone. Homes situated in high-risk flood areas, such as near rivers, coastlines, or in designated Special Flood Hazard Areas (SFHAs), typically incur higher premiums compared to those in moderate- to low-risk zones.

- The elevation of the home relative to the base flood elevation (BFE) also plays a significant role. Structures built above the BFE are considered less at risk and may qualify for lower rates, while homes with living spaces below the BFE face substantially increased premiums.

- Additional factors include the age of the building, the design and structure type, the amount of coverage selected (building and/or contents), and the deductible chosen. Older homes or those with basements in flood-prone areas often face higher costs due to increased vulnerability.

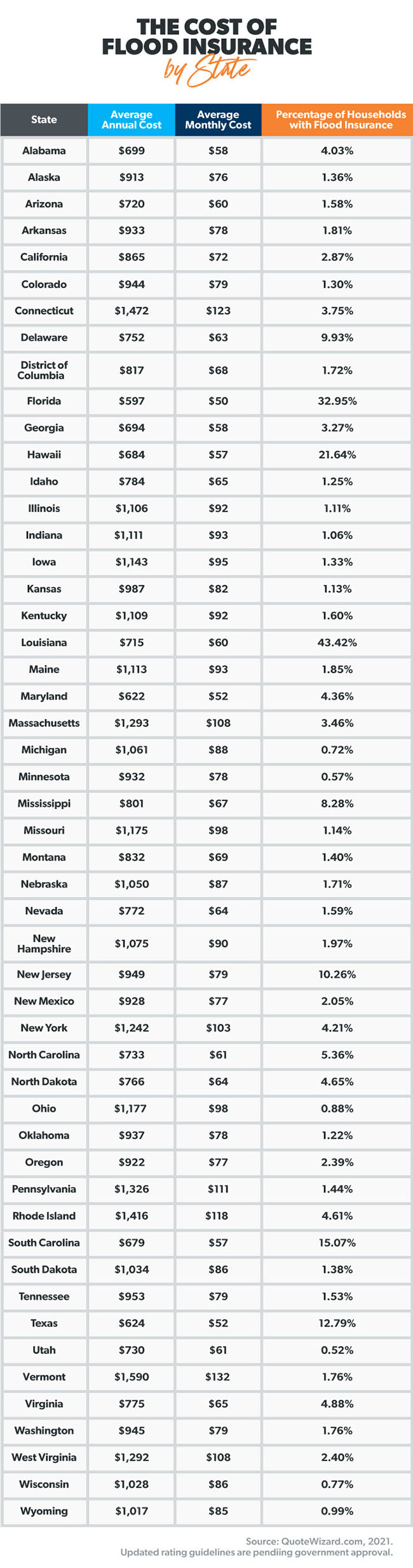

- The average cost of a flood insurance policy through the National Flood Insurance Program (NFIP) in the United States is approximately $700 to $1,300 per year. However, this average can vary significantly depending on individual circumstances and location.

- In low-risk areas, such as those classified as Zone X, premiums can be as low as $130 to $450 annually. These policies are often available under the Preferred Risk Policy (PRP), which offers discounted rates for properties not in high-risk zones.

- In contrast, properties in high-risk zones (like Zone A or Zone V) may see annual premiums exceeding $2,000, especially if the structure is below the base flood elevation or has previously experienced flood damage. Coverage limits under the NFIP max out at $250,000 for building property and $100,000 for personal contents.

Private Market Flood Insurance Options and Pricing

- In recent years, private flood insurance has become a viable alternative to NFIP policies, with several insurers offering competitive rates and broader coverage options. These policies can sometimes be cheaper than NFIP plans, particularly for homes in moderate-risk areas or for those seeking higher coverage limits.

- Private insurers may use more advanced risk assessment models, taking into account real-time weather data, improved elevation certificates, and modernized flood maps, which can result in more accurate and potentially lower premiums for certain properties.

- Some private policies offer additional benefits not included in standard NFIP coverage, such as coverage for temporary living expenses, cost of increased regulation (e.g., elevation requirements after a flood), or basement improvements. Premiums with private insurers can range from under $500 to several thousand dollars annually, depending on the level of risk and desired coverage.

Is flood insurance for homeowners a worthwhile investment through FEMA?

Understanding FEMA's Role in Flood Insurance

- FEMA, the Federal Emergency Management Agency, does not sell flood insurance directly but manages the National Flood Insurance Program (NFIP), which makes flood coverage accessible to homeowners through approved insurers and agents.

- The NFIP was created to reduce the impact of flooding on private and public structures by providing affordable insurance and encouraging communities to adopt and enforce floodplain management regulations.

- Although FEMA sets the guidelines and rates for policies under the NFIP, actual policies are issued and serviced by private insurance companies, meaning homeowners interact with insurers while the federal framework supports consistency and availability.

When Flood Insurance Through FEMA Is Necessary or Advisable

- Homeowners with mortgages in high-risk flood zones, particularly Special Flood Hazard Areas (SFHAs) as designated by FEMA flood maps, are typically required by lenders to carry flood insurance through the NFIP or a private provider.

- Even in moderate- to low-risk areas, purchasing a flood policy can be a prudent financial decision, as over 20% of flood claims come from outside high-risk zones, and standard homeowners' insurance does not cover flood damage.

- Properties historically affected by heavy rains, proximity to rivers, or those in regions prone to flash flooding benefit significantly from NFIP coverage, as post-disaster federal aid often comes in the form of loans that must be repaid, unlike insurance payouts.

Limitations and Considerations of NFIP Coverage

- NFIP policies come with coverage caps—up to $250,000 for the building and $100,000 for personal property—which may be insufficient for homes in high-value areas or those with extensive contents, prompting some to seek private supplemental policies.

- There is typically a 30-day waiting period from the date of purchase before an NFIP policy goes into effect, meaning last-minute purchases ahead of a storm are not immediately protective.

- Not all types of water damage are covered; for example, damage from sewer backups or seepage may not be included unless directly caused by a flood event as defined by the NFIP, which can lead to misunderstandings during claims.

Frequently Asked Questions

What does flood insurance for a home typically cover?

Flood insurance typically covers structural components and essential systems of a home, including the foundation, walls, floors, electrical and plumbing systems, and built-in appliances. It also protects personal belongings like furniture, clothing, and electronics up to a specified limit. However, it generally excludes damage from water seepage, mold, or belongings in basements. Coverage is subject to policy terms and limits set by the National Flood Insurance Program or private insurers.

Is flood insurance required for all homeowners?

Flood insurance is not required for all homeowners, but it is mandatory for properties located in high-risk flood zones with government-backed mortgages. Even in low-risk areas, lenders may recommend or require coverage. Homeowners in any area can purchase flood insurance voluntarily, as floods can occur unexpectedly. Relying solely on federal disaster assistance is risky since it’s not guaranteed and often comes in the form of loans that must be repaid.

How much does flood insurance cost on average?

The average cost of flood insurance in the U.S. is around $700 to $1,300 per year, but prices vary widely based on location, flood risk, home elevation, and coverage amount. Properties in high-risk zones cost more to insure. Premiums may be lower through the National Flood Insurance Program, though private insurers offer competitive rates. Deductibles apply, and cost-saving measures include elevating utilities or improving drainage. Shopping around helps find the best value.

Can renters purchase flood insurance for their belongings?

Yes, renters can and should purchase flood insurance to protect their personal belongings. While the building owner’s policy covers the structure, it does not cover renters’ possessions. Renters’ flood insurance covers items like furniture, clothing, electronics, and other personal property damaged by flooding. Coverage limits are typically lower than homeowner policies but offer essential financial protection. It's an affordable way to safeguard valuables in flood-prone areas.

Leave a Reply