Premium Life Insurance Quote

Securing the right life insurance policy is a critical step in safeguarding your family’s financial future, and a premium life insurance quote offers access to comprehensive coverage tailored to individual needs.

These quotes reflect high-value policies designed for those seeking extended benefits, higher payouts, and added riders for enhanced protection. Factors such as age, health, lifestyle, and coverage duration influence the final premium, ensuring a personalized approach.

Obtaining an accurate quote allows individuals to compare options from top insurers, evaluate policy features, and make informed decisions that align with long-term financial goals and peace of mind.

Questions To Ask Before Buying Life Insurance

Questions To Ask Before Buying Life InsuranceSecuring the right life insurance policy begins with obtaining an accurate and competitive premium life insurance quote.

A premium quote represents the amount you'll pay periodically—monthly, quarterly, or annually—for coverage under a life insurance policy. These quotes are not one-size-fits-all; they're calculated based on a range of personal factors such as age, health history, lifestyle choices, occupation, and the type and amount of coverage desired.

Insurers use sophisticated underwriting processes to assess risk and determine your premium. Understanding how these quotes are generated empowers you to make informed decisions, compare offers effectively, and ultimately choose a policy that aligns with your financial goals and family protection needs.

Your premium life insurance quote is influenced by several key elements that insurers evaluate during the underwriting process. Age is a primary factor—generally, the younger you are when you apply, the lower your premiums will be, as younger individuals pose less risk of immediate claims.

Ramsey Solutions Term Life Insurance

Ramsey Solutions Term Life InsuranceHealth conditions such as diabetes, heart disease, or high blood pressure can increase your rate, as can lifestyle factors like smoking or excessive alcohol consumption. Your occupation and hobbies also matter; for instance, someone working in a high-risk job or participating in extreme sports may face higher premiums.

Additionally, the coverage amount, policy type (term or permanent), and whether you choose additional riders like accidental death or waiver of premium will impact the final quote. Accurate disclosure during the application ensures a fair and reliable quote.

When requesting a premium life insurance quote, one of the most significant decisions you'll make is choosing between term and permanent life insurance. Term life insurance provides coverage for a specified period—typically 10, 20, or 30 years—and generally offers the lowest premiums because it is purely protection-based with no cash value component.

In contrast, permanent life insurance, including whole and universal life policies, provides lifelong coverage and includes a savings or investment element that builds cash value over time. Because of these additional benefits, permanent policies come with significantly higher premiums.

Sun Life Insurance Phone

Sun Life Insurance PhoneYour financial goals will determine which type is more suitable: term is ideal for temporary needs like mortgage protection or income replacement, while permanent insurance suits long-term estate planning or legacy goals.

To get the most value from your premium life insurance quote, it's essential to compare multiple offers from reputable insurers. Begin by assessing your coverage needs based on debts, income, dependents, and future expenses.

Use online comparison tools or consult with an independent insurance agent who can access quotes from various carriers. When reviewing quotes, ensure they are based on the same coverage amount, term length, and policy features to allow for accurate comparisons.

Pay close attention to the insurer’s financial strength ratings from agencies like A.M. Best or Standard & Poor’s, as these reflect their ability to pay claims. Also, consider customer service reputation and the ease of policy management. Small differences in premiums can add up over time, so thorough evaluation ensures both affordability and reliability.

Term And Whole Life Insurance Difference

Term And Whole Life Insurance Difference| Feature | Term Life Insurance | Permanent Life Insurance |

|---|---|---|

| Coverage Duration | Fixed term (e.g., 10–30 years) | Lifelong |

| Premium Cost | Lower initial premiums | Higher, ongoing premiums |

| Cash Value | No cash value component | Yes, accumulates over time |

| Best For | Temporary financial protection | Wealth transfer, savings component |

| Policy Flexibility | Fixed premium and term | Adjustable premiums and benefits (in some types) |

%20(1).png)

The average monthly premium for a $1,000,000 life insurance policy varies significantly based on multiple factors such as age, health, gender, lifestyle, type of policy, and the insurance provider.

For a healthy 35-year-old non-smoker, a 20-year term life insurance policy with a $1,000,000 death benefit typically costs between $40 and $60 per month. Individuals at higher risk due to medical conditions, smoking, or extreme occupations can expect to pay substantially more—sometimes over $200 per month.

Permanent life insurance policies, such as whole life or universal life, which provide lifelong coverage and accumulate cash value, generally have much higher premiums, potentially ranging from $300 to over $1,000 monthly depending on age and other criteria.

Term Life Insurance Quotes Gilbert

Term Life Insurance Quotes Gilbert- Age plays a critical role in determining premiums; younger applicants benefit from lower rates since the risk of mortality is lower. A 30-year-old might pay half of what a 50-year-old pays for the same coverage amount and policy term.

- Health status is evaluated through medical underwriting, including factors like blood pressure, cholesterol levels, BMI, and pre-existing conditions. Applicants with excellent health are categorized in the preferred risk class, securing the lowest available rates.

- Lifestyle choices such as tobacco use, alcohol consumption, and participation in high-risk activities (e.g., skydiving or scuba diving) can significantly increase premiums. Insurers may require additional underwriting or impose exclusions for risky behaviors.

- Term life insurance offers coverage for a specific period, such as 10, 20, or 30 years, and is generally the most affordable option for securing a $1,000,000 death benefit. Premiums remain fixed throughout the term and are ideal for income replacement during working years.

- Whole life insurance, a type of permanent coverage, provides lifelong protection and includes a cash value component that grows over time. Due to the extended coverage period and additional features, premiums are considerably higher—often five to ten times more than comparable term policies.

- Universal life insurance offers more flexibility than whole life, allowing adjustments to premiums and death benefits. However, the complexity and investment component result in higher fees and monthly costs compared to term insurance, even for the same $1,000,000 coverage amount.

How Insurance Providers Calculate Monthly Rates

- Insurers use actuarial tables and underwriting guidelines to assess an applicant's life expectancy. These data-driven models analyze mortality risk based on demographic and medical information to determine the likelihood of a claim.

- Applicants are assigned to risk classes such as preferred plus, preferred, standard, or substandard. Those in higher risk classes due to health or lifestyle may face increased premiums or require a medical exam to qualify for coverage.

- Premiums are also impacted by the insurer's operational costs, profit margins, and market competition. Shopping around and comparing quotes from multiple insurers can lead to substantial savings, even for the same $1,000,000 policy amount.

The average premium cost for a $500,000 life insurance policy varies significantly based on several key factors such as age, health status, gender, lifestyle habits, and the type of policy selected.

For a healthy 35-year-old non-smoker, a 20-year term life insurance policy with a $500,000 death benefit typically ranges from $25 to $40 per month. Premiums increase with age; for example, a 50-year-old in good health might pay between $75 and $120 monthly for the same coverage.

Permanent life insurance policies, such as whole life, are considerably more expensive due to their lifelong coverage and cash value component, often costing several hundred dollars per month for a $500,000 policy. Insurers also consider risk factors like family medical history, occupation, and hobbies when calculating premiums.

- Age: Premiums rise with age because the risk of mortality increases over time. A 25-year-old will pay significantly less than a 60-year-old for the same $500,000 coverage due to longer life expectancy and lower health risks.

- Health and Medical History: Individuals with pre-existing conditions such as diabetes, heart disease, or obesity are typically charged higher premiums. Routine medical exams and health screenings during underwriting directly impact pricing.

- Lifestyle Choices: Smoking, excessive alcohol consumption, and participation in high-risk activities like skydiving or scuba diving can lead to higher premiums. Insurers view these behaviors as increasing the likelihood of a claim.

- Term Life Insurance: This type of policy provides coverage for a specific period, such as 10, 20, or 30 years. Premiums are generally lower and fixed during the term. For a $500,000 policy, young, healthy individuals may pay under $30 monthly, making it an affordable option for temporary financial protection.

- Whole Life Insurance: As a form of permanent coverage, whole life policies last a lifetime and include a savings component known as cash value. Premiums are much higher—often five to ten times more than term life for the same face amount—because the policy is guaranteed to pay out and accumulates value over time.

- Universal Life Insurance: This flexible permanent policy allows adjustments in premium payments and death benefits. While potentially less expensive than whole life, it still costs significantly more than term insurance due to lifelong coverage and investment features.

How Gender and Occupation Affect $500,000 Life Insurance Rates

- Gender: On average, women pay lower premiums than men for the same $500,000 policy because statistical data shows they tend to live longer. For instance, a 40-year-old woman might pay 15–25% less than a man of the same age and health profile.

- Occupational Risk: Individuals working in hazardous environments—such as construction, mining, or firefighting—may face higher premiums or additional underwriting scrutiny. Insurers assess job-related risks that could increase the probability of injury or death.

- Geographic Location: Where you live can also affect premiums due to regional differences in healthcare costs, life expectancy, and state-specific regulations. Urban areas with higher medical costs or crime rates may see slightly increased rates compared to rural locations.

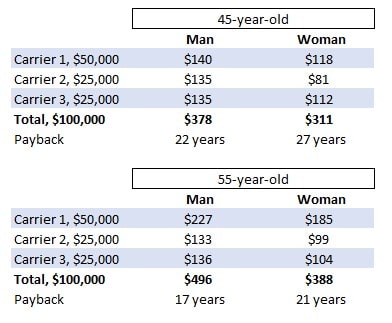

The average premium cost for a $100,000 life insurance policy varies significantly based on multiple factors such as age, health, gender, lifestyle, and the type of policy chosen. Generally, term life insurance policies are more affordable than permanent life insurance options.

For a healthy 35-year-old non-smoker, a 20-year term policy with a $100,000 death benefit might cost between $10 and $20 per month. Rates increase with age and pre-existing medical conditions. For instance, a 50-year-old with similar health might pay $25 to $45 monthly.

Permanent policies, such as whole life, typically have higher premiums—potentially ranging from $50 to over $100 per month for the same coverage—because they include a cash value component and provide lifelong protection.

- Age: Premiums rise with age because insurers perceive older applicants as higher risk. A 25-year-old will pay significantly less than a 60-year-old for the same $100,000 coverage due to longer life expectancy and lower immediate mortality risk.

- Health Status: Individuals with excellent health, normal blood pressure, and no history of chronic illness qualify for the best rates. Conversely, conditions like diabetes, heart disease, or obesity can substantially increase monthly premiums.

- Lifestyle Choices: Habits such as smoking, excessive alcohol consumption, or engaging in high-risk hobbies (e.g., skydiving) lead to higher premiums. Insurers often require medical exams or questionnaires to assess these factors.

- Term Life Insurance: These policies provide coverage for a set period, such as 10, 20, or 30 years. Premiums are typically fixed during the term and are significantly lower than permanent policies. For a $100,000 term policy, a healthy applicant might pay as little as $10 per month.

- Whole Life Insurance: This type of permanent insurance offers lifelong coverage and includes a savings component that grows over time. Premiums are much higher—often three to five times more than term policies—for the same death benefit due to the added cash value feature.

- Universal Life Insurance: Another permanent option, universal life provides flexibility in premium payments and death benefits. While it can sometimes be less expensive than whole life, it still costs more than term insurance and requires careful management to avoid lapsing.

How Gender and Location Affect $100,000 Life Insurance Rates

- Gender: Statistically, women live longer than men, leading to lower life insurance premiums for female applicants. A $100,000 term policy for a 40-year-old woman might cost $12 per month, compared to $15 for a man of the same age and health profile.

- Geographic Location: Premiums can vary by state or country due to local regulations, mortality rates, and cost of living. For example, individuals in states with higher average healthcare costs or increased incidence of certain health conditions may face slightly elevated rates.

- Insurer Pricing Models: Each insurance company uses its own underwriting guidelines and risk assessment models. One insurer might offer a $100,000 policy for $13 per month to a specific applicant, while another charges $18, even for similar health and demographics. Shopping around is essential to find the most competitive rate.

Frequently Asked Questions

A Premium Life Insurance Quote is an estimate of how much you’ll pay for a life insurance policy based on your age, health, lifestyle, and coverage needs. It helps you compare different plans and providers to find the best value. Premiums can be fixed or vary depending on the policy type, ensuring financial protection for your loved ones.

Insurers calculate a Premium Life Insurance Quote using factors like your age, medical history, occupation, lifestyle habits (such as smoking), and the amount of coverage desired. Actuarial data determines the risk level, which influences the premium cost. Accurate information ensures a fair and realistic quote, helping you select a policy that fits your budget and protection goals.

Yes, you can get a Premium Life Insurance Quote online through insurer websites or comparison platforms. These tools provide quick, convenient estimates by collecting basic personal and financial information. While online quotes are helpful for initial research, speaking with a licensed agent ensures you understand all policy details and receive the most accurate pricing.

A Premium Life Insurance Quote typically includes the base cost of coverage but may not reflect all potential fees or riders. Additional costs like optional benefits, medical exams, or underwriting charges might not be included. Always review the full policy details to understand total expenses and ensure the quote aligns with your long-term financial protection needs.

Leave a Reply