Home insurance claim requirements

Filing a home insurance claim requires careful attention to detail and adherence to specific procedural requirements.

Understanding what is needed can streamline the process and improve the likelihood of a successful outcome. Typically, policyholders must promptly report the incident, provide documentation of damages, and submit relevant evidence such as photos, receipts, or police reports.

Insurance companies often require a detailed inventory of affected items and may conduct their own assessment. Familiarity with your policy’s terms, coverage limits, and deductible is crucial. Meeting all home insurance claim requirements helps ensure timely processing and fair compensation for losses.

How to compare home insurance policies easily

How to compare home insurance policies easilyUnderstanding Home Insurance Claim Requirements

Filing a home insurance claim involves a series of specific steps and documentation that policyholders must follow to ensure a smooth and successful process. Knowing what insurers require can significantly reduce delays and potential claim denials.

Typically, the process begins immediately after a covered loss, such as fire, theft, or severe weather damage. Homeowners must promptly notify their insurance company, provide a detailed account of the incident, and supply evidence supporting the claim.

Requirements often include proof of ownership, repair estimates, police reports (if applicable), and thorough documentation of damages through photos or videos. Insurers may also send an adjuster to inspect the property and verify the claim’s validity. Complying with all procedural and evidentiary requirements set forth in the policy is essential to receiving fair and timely compensation.

Documenting the Damage

When filing a home insurance claim, one of the most critical steps is thoroughly documenting the damage. Insurers require visual and written proof to validate the extent and cause of the loss.

How to ensure personal items are covered by home insurance

How to ensure personal items are covered by home insuranceHomeowners should take clear, timestamped photographs and videos of all affected areas and damaged belongings before any cleanup or repairs begin. This visual evidence should capture wide-angle views as well as close-ups of specific damage. In addition to media, creating a detailed inventory of damaged or lost items—with descriptions, purchase dates, and estimated values—can strengthen the claim.

Using a home inventory list created prior to the incident can be invaluable. Failure to properly document damages may lead to underpayment or denial, so it's crucial to be comprehensive and systematic.

Notifying Your Insurance Company Promptly

Timely notification is a fundamental home insurance claim requirement. Most policies stipulate that policyholders must report a loss “as soon as possible” or “promptly” after the incident occurs.

Delays in reporting can lead to complications, including suspicion of fraud or questions about the claim’s legitimacy. Contacting the insurer immediately via phone, online portal, or mobile app initiates the claims process and assigns a claims representative.

How to make a home insurance claim with youi

How to make a home insurance claim with youiDuring this initial communication, be prepared to provide basic information such as the policy number, date and cause of loss, a description of damages, and whether anyone was injured. Some insurers have specific time windows—such as 24 to 72 hours—for reporting certain types of claims. Adhering to these timelines helps maintain policy compliance and expedites the overall processing.

Providing Proof of Loss and Supporting Documents

Insurance companies require a formal Proof of Loss document in many cases, particularly for larger claims, which serves as a sworn statement detailing the items damaged or lost and their estimated value.

This form must typically be submitted within a specified period, such as 60 days after the loss. Alongside the Proof of Loss, insurers expect supporting documentation, including receipts, appraisals, repair estimates from licensed contractors, and official reports (e.g., police reports for theft or fire department reports for fires).

Bank or credit card statements can also substantiate ownership and value. Lack of proper documentation is one of the leading reasons for claim denials or reduced settlements. Ensuring that all requested paperwork is accurate, complete, and submitted on time is essential for a favorable outcome.

| Required Document | Purpose | When It's Needed |

|---|---|---|

| Photographs/Videos of Damage | Provides visual evidence of the extent and nature of property damage | Immediately after loss, before cleanup |

| Home Inventory List | Details personal belongings and their value for reimbursement | After loss, during claims submission |

| Proof of Loss Form | Sworn statement summarizing the claim and damages | Within 60 days, if required by insurer |

| Repair Estimates | Shows cost of repairs from licensed professionals | During claim assessment process |

| Police or Fire Reports | Verifies incident occurrence and official response | For theft, vandalism, or fire-related claims |

Essential Requirements for Filing a Home Insurance Claim

What should you avoid saying during a home insurance claim to meet claim requirements?

Admitting Fault or Speculating About Causes

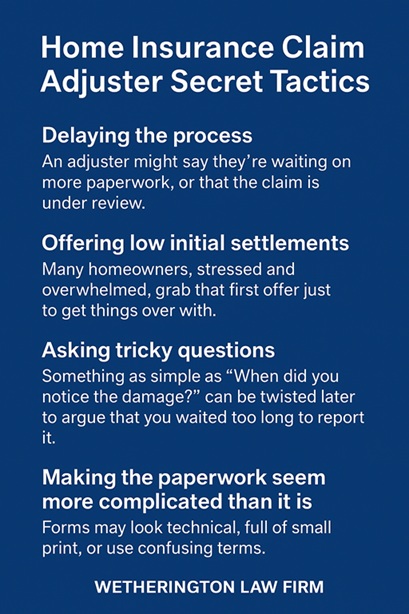

When filing a home insurance claim, it's critical to avoid admitting fault or making assumptions about what caused the damage. Insurance companies rely on professional assessments to determine liability and coverage, so any statements you make could be used to dispute or deny your claim. For example, saying “I think the roof leaked because I didn’t maintain it well” may give the insurer grounds to claim negligence. Instead, stick to objective facts and let the adjuster investigate.

- Do not say you were careless or failed to maintain your property, even casually.

- Avoid guessing how the incident occurred—wait for official findings.

- Refrain from using words like my fault, I should have, or I forgot, as these imply responsibility.

Exaggerating the Damage or Claim Value

Inflating the extent of damage or overstating the value of lost or damaged items can jeopardize your claim and lead to allegations of fraud. Insurance companies often verify claims through documentation, photos, and third-party evaluations. If discrepancies are found, your entire claim may be denied, and you could face legal consequences. It’s best to be honest and provide accurate, itemized information supported by receipts or estimates.

- Do not claim items you didn't own or that were not damaged.

- Avoid estimating costs well above market value just to get a higher payout.

- Submit only documented losses with proof such as photos, purchase records, or appraisals.

Mentioning Previous Undisclosed Claims or Risks

Avoid bringing up past incidents that were not previously reported to your insurer, such as older water leaks, thefts, or prior damage. If those events weren’t covered under previous policies or were not disclosed, mentioning them now could prompt a review of your policy validity or lead to denial based on incomplete information. Additionally, discussing risky behaviors like frequent electrical issues or unpermitted renovations may raise red flags.

- Do not volunteer information about past damage that wasn’t formally claimed.

- Refrain from discussing unreported home modifications that might violate building codes.

- Avoid talking about recurring problems that could suggest ongoing neglect or increased risk.

What are the required steps to file a home insurance claim successfully?

Document the Damage Thoroughly

- Begin by taking clear, high-resolution photographs and videos of all affected areas and damaged items. Capture wide-angle shots to show the overall context and close-ups to highlight specific damages.

- Make a detailed inventory of all damaged or destroyed personal belongings, noting their estimated value, age, and purchase date if possible. Include serial numbers and any available receipts or proof of ownership.

- Preserve damaged items until the insurance adjuster has inspected them. Discarding items prematurely could jeopardize your claim, even if the damage appears total.

Contact Your Insurance Company Promptly

- Notify your insurer as soon as possible after the incident, as most policies require timely reporting. Use the official claims phone number or online portal provided by your insurance carrier.

- Be prepared to provide your policy number, date and cause of loss, address of the property, and a brief description of the damage when filing the initial report.

- Follow any immediate instructions from the insurer, such as securing the property to prevent further damage or scheduling an inspection with a claims adjuster.

Cooperate with the Claims Adjuster and Review the Settlement

- Schedule and attend the inspection with the assigned claims adjuster, ensuring they have full access to all damaged areas and your documented evidence.

- Answer all questions truthfully and provide supporting documents, such as repair estimates, receipts for temporary repairs, and your inventory list.

- Review the adjuster's assessment and settlement offer carefully. If you disagree with the valuation, submit additional evidence or request a reassessment before accepting the payment.

What documentation is required for a home insurance claim involving property damage?

Photographic and Video Evidence of the Damage

Providing visual documentation is one of the most critical steps when filing a home insurance claim for property damage. Insurers rely heavily on clear images or videos to assess the extent and nature of the damage. It is essential to capture photos and videos from multiple angles, showing both close-ups of affected areas and wider shots that illustrate the overall condition.

This step should be completed before any repairs or cleanup begins to ensure the insurer sees the original state of the damage. Visual records help prevent disputes about the claim’s validity and support faster processing.

- Take high-resolution photos of all damaged areas, including structural components like walls, roofs, and floors.

- Record short video clips panning across damaged rooms or exteriors to give context and show the full scope of destruction.

- Photograph any associated hazards or causes, such as broken windows, fallen trees, or water leaks, to link the damage to a specific event.

Incident Report and Written Description

Alongside visual records, a detailed written account of the incident strengthens your claim and helps the insurance adjuster understand the sequence of events. This documentation should include the date, time, and specific circumstances leading to the damage.

Whether the cause was a storm, fire, burst pipe, or vandalism, a clear narrative supports consistency in your claim. If law enforcement or emergency services were involved, including reference numbers or names of responding officers adds credibility. A well-prepared description reduces the likelihood of delays due to missing or unclear information.

- Write a chronological summary of the event, noting when the damage occurred and when it was discovered.

- Include environmental or external factors such as weather conditions, neighborhood incidents, or prior maintenance issues.

- Attach copies of police reports, fire department records, or service technician notes if applicable to substantiate your account.

Receipts, Repair Estimates, and Inventory Records

Financial documentation plays a major role in determining the reimbursement amount for your claim. Insurers often require proof of ownership and valuation of damaged personal property and structural elements.

Keeping receipts for major appliances, electronics, or home improvements helps establish their worth. Additionally, obtaining written estimates from licensed contractors for repair costs provides a benchmark for the insurer’s assessment. A home inventory—preferably updated annually—listing your belongings with descriptions and values is extremely helpful, especially in cases of total loss or extensive damage.

- Gather receipts or purchase records for high-value items that were damaged, such as furniture, electronics, or flooring.

- Obtain at least two written repair or replacement estimates from certified professionals for structural repairs.

- Submit a detailed home inventory list that includes item descriptions, purchase dates, estimated values, and corresponding photos.

Frequently Asked Questions

What documents are needed to file a home insurance claim?

To file a home insurance claim, you typically need a completed claim form, photo or video evidence of the damage, a detailed inventory of damaged items, repair estimates, and police reports if applicable. Your policy number and contact information are also required. Providing thorough documentation helps speed up the claims process and supports accurate assessment of your losses by the insurance company.

How soon should I report a home insurance claim after damage occurs?

You should report a home insurance claim as soon as possible after damage occurs, ideally within 24 to 48 hours. Prompt reporting helps prevent further damage and fulfills policy requirements. Delays may lead to complications or denial of the claim. Contact your insurer immediately, provide initial details, and begin documenting the damage. Most policies require timely notification to ensure coverage is properly applied.

Do I need an adjuster’s report for my home insurance claim?

Yes, most home insurance claims require an adjuster’s report. After filing, your insurer will assign an adjuster to inspect the damage and verify the claim details. The adjuster assesses the extent of loss, determines coverage, and helps calculate compensation. Cooperate fully with the adjuster, provide all requested documents, and keep your own records of the inspection to ensure a fair evaluation.

Can I start repairs before the insurance claim is approved?

You can begin emergency repairs to prevent further damage, but avoid major renovations before the insurance company inspects the property. Making significant changes can interfere with the claims process and may result in denied coverage. Take photos before any repairs, keep all receipts, and consult your insurer first. Following proper procedure ensures your expenses are considered during claim settlement.

Leave a Reply