How to choose home insurance with best claims process

Choosing home insurance is about more than just finding the lowest premium—it’s about ensuring reliable protection when disaster strikes.

Among the most critical factors is the claims process, which can significantly impact your recovery after damage or loss. A smooth, efficient claims experience provides peace of mind during stressful times. When evaluating home insurance providers, consider their reputation for fast claims handling, customer support availability, digital tools for filing claims, and transparency in communication.

Look for insurers with clear guidelines, minimal paperwork, and positive customer reviews regarding claim settlements. The right policy doesn’t just cover your home—it stands by you when you need it most, making claims resolution swift and stress-free.

How to ensure personal items are covered by home insurance

How to ensure personal items are covered by home insuranceHow to Choose Home Insurance with the Best Claims Process

Choosing home insurance with a superior claims process requires careful consideration of multiple factors beyond just the premium cost. A policy might offer low rates, but if the insurer is slow, unresponsive, or difficult to work with when you file a claim, it defeats the purpose of having coverage.

The ideal home insurance provides fast claims settlement, clear communication, and strong customer support throughout the process. Look for insurers with 24/7 claims reporting, direct repair networks, and transparent documentation requirements. Reading customer reviews, checking third-party ratings from organizations like AM Best or J.D.

Power, and asking about average claim resolution time can give you a realistic picture of how smoothly claims are handled. Ultimately, the best policy is one that delivers reliable financial protection when you need it most.

Check Insurance Company Ratings and Customer Reviews

Evaluating an insurer’s reputation through independent ratings and verified customer feedback is one of the most reliable ways to predict claim-handling performance. Organizations like A.M. Best, Standard & Poor’s, and J.D.

How to make a home insurance claim with youi

How to make a home insurance claim with youiPower assess insurers based on financial strength, customer satisfaction, and claims handling efficiency. High ratings suggest that a company is likely to pay claims promptly and operate with stability. Additionally, online reviews on platforms like the Better Business Bureau (BBB) or consumer forums reveal real-world experiences with adjuster responsiveness, ease of filing claims, and payout fairness.

Pay close attention to patterns—if multiple customers complain about delays or poor communication during claims, it could be a red flag. A financially stable insurer with consistently positive feedback is more likely to deliver a smooth claims experience when disaster strikes.

Look for Policies with Fast and Transparent Claim Reporting

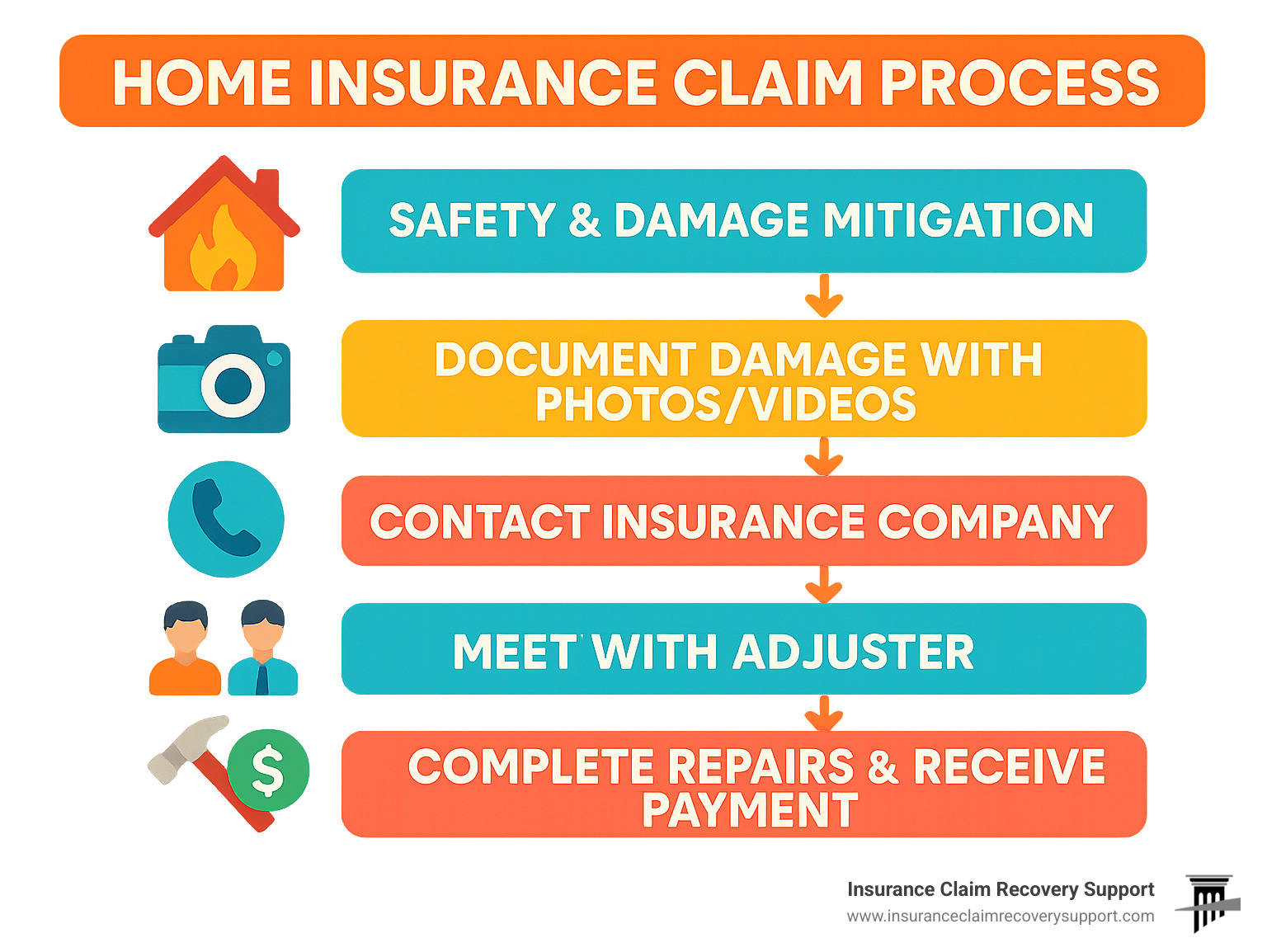

A seamless claims process starts with how easily you can initiate a claim. The best home insurance providers offer multiple reporting options, including a 24/7 claims hotline, mobile apps, online portals, and live chat support.

Immediate reporting can speed up assessment and repairs, minimizing further damage. Transparency is equally important: the insurer should clearly outline what documentation is needed—such as photos, police reports, or repair estimates—and provide real-time updates via email or text.

How can the location of a home affect insurance costs

How can the location of a home affect insurance costsPolicies that integrate with digital claims platforms often streamline the process, allowing you to upload evidence, track claim status, and receive damage assessments quickly. Avoid insurers that require excessive paperwork or have vague claim procedures, as these are signs of a slow and frustrating experience during critical times.

Verify Additional Support Services and Repair Networks

Beyond claim payouts, top-tier home insurers often provide valuable value-added services that simplify recovery after a loss.

These include partnerships with preferred repair contractors, emergency service coordination (like water extraction or locksmiths), and temporary living expense coverage. Some insurers offer guaranteed repair timelines or inflation guard coverage to ensure your home is fully restored even if costs rise.

Assess whether the insurer manages the repair process directly or reimburses you after you handle it yourself—direct repair coordination typically leads to a faster, less stressful resolution. Confirm whether these services are included at no extra cost and whether they are available locally. Having access to a trusted network of professionals enhances the efficiency and quality of your claim resolution.

| Feature | Why It Matters | What to Look For |

|---|---|---|

| Claims Resolution Time | Policies with faster resolution minimize financial strain and speed up recovery. | Insurers that resolve claims in under 14 days on average. |

| 24/7 Claims Hotline | Immediate access ensures timely reporting, especially after emergencies. | Dedicated phone lines with live agents available at all hours. |

| Customer Satisfaction Score | High scores reflect positive real-world claims experiences. | J.D. Power rankings above “Above Average” in claims satisfaction. |

| Direct Repair Network | Reduces hassle and accelerates restoration after damage. | In-network contractors vetted and paid directly by the insurer. |

| Online Claims Tracker | Keeps you informed and reduces anxiety during the claims process. | Mobile app or portal with real-time status updates and document uploads. |

How to Choose Home Insurance with the Best Claims Process: A Comprehensive Guide

What is the 80/20 rule in home insurance claims and how does it impact coverage choice?

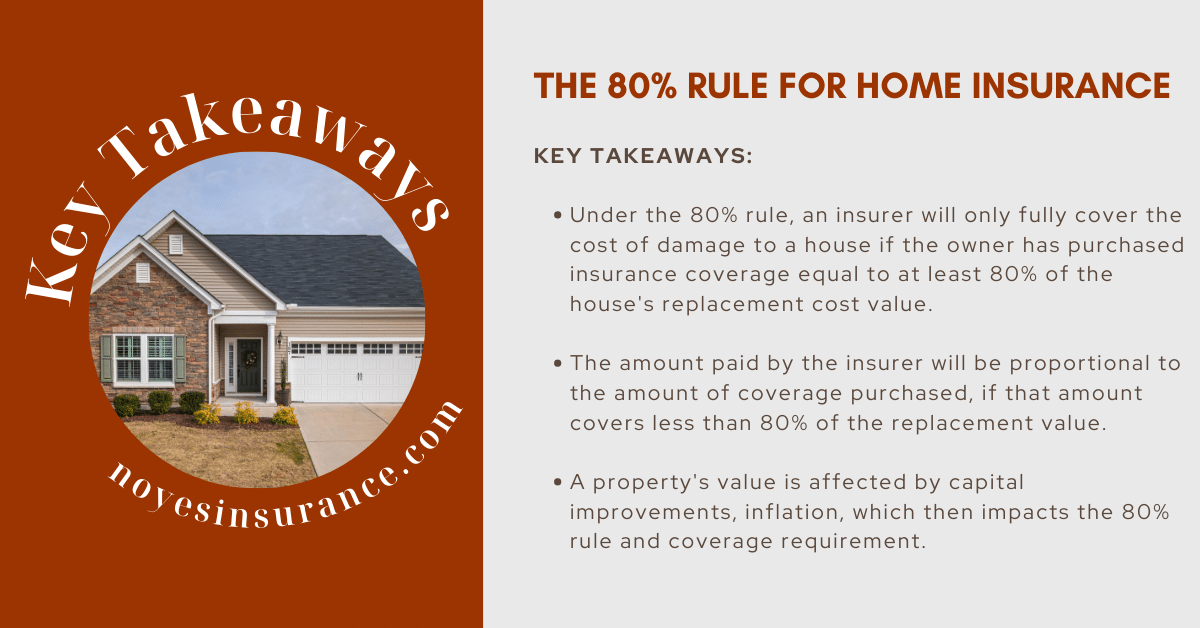

The 80/20 rule in home insurance, often referred to as the 80% rule, is a guideline used by insurers to determine the minimum amount of dwelling coverage a homeowner should carry to ensure full reimbursement for certain types of partial losses. Specifically, it states that insurers will only provide full replacement cost coverage for a loss if the homeowner has insured their property for at least 80% of its current replacement cost.

If the insured amount falls below this threshold, the homeowner may be subject to coinsurance penalties, meaning they will have to pay a larger portion of the claim out of pocket. This rule strongly influences how policyholders select coverage limits, pushing them to accurately estimate the cost of rebuilding their home rather than relying solely on market value or purchase price.

Understanding the Mechanics of the 80% Rule

- The 80% rule requires policyholders to insure their home for at least 80% of its replacement cost to qualify for full payouts on partial losses, such as roof damage or fire affecting only part of the house.

- If a homeowner insures for less than 80%, the insurance company applies a proportional penalty, meaning the claim reimbursement is reduced based on the percentage of underinsurance.

- For example, if a home’s replacement cost is $300,000, the homeowner should carry at least $240,000 in dwelling coverage; falling below this amount could result in out-of-pocket costs even with a covered claim.

How the 80/20 Rule Affects Coverage Decisions

- Homeowners must regularly reassess their dwelling coverage to account for inflation, construction cost increases, and home improvements that affect replacement value.

- Choosing a lower coverage amount to save on premiums can backfire when a claim occurs, as the 80% threshold may not be met, leading to substantial out-of-pocket expenses.

- Insurance agents often recommend guaranteed or extended replacement cost coverage to bypass strict adherence to the 80% rule, offering more predictable protection.

Practical Implications During a Claim Settlement

- When a claim is filed, insurers evaluate the extent of damage and compare the insured amount to the 80% benchmark of the home’s rebuild cost at the time of loss.

- If underinsured, the payout is calculated using a coinsurance formula that reduces the claim amount proportionally—for example, paying only 75% of the repair cost if only 60% of the required coverage was in place.

- Homeowners may be surprised by the gap between expected and actual payouts, emphasizing the need for accurate valuation and sufficient coverage limits from the outset.

Which home insurance provider has the most reliable claims payout process?

Top Home Insurance Providers Known for Reliable Claims Payouts

- State Farm consistently ranks among the top home insurance providers for claims satisfaction. According to surveys conducted by J.D. Power, State Farm scores above the national average in customer satisfaction with the claims process. Customers report timely initial contact from adjusters, clear instructions during documentation, and prompt settlement resolution.

- Amica Mutual is frequently highlighted for its outstanding claims service and financial stability. It holds an A+ rating from the Better Business Bureau (BBB) and an A+ (Superior) rating from AM Best, which underscores its ability to meet policyholder obligations. Amica emphasizes a personalized claims experience, assigning a single representative to guide customers from start to finish.

- USAA, available exclusively to military members, veterans, and their families, is renowned for its efficient and empathetic claims handling. USAA has received the highest scores in multiple J.D. Power studies, particularly in categories involving claims settlement fairness and ease of process. Their digital tools also support faster photo uploads and virtual estimates, speeding up repair timelines.

Factors That Influence Claims Payout Reliability

- Financial strength ratings from agencies like AM Best, Moody’s, and Standard & Poor’s play a critical role in determining a company’s ability to pay claims, especially after large-scale disasters. Insurers with higher ratings are more likely to have the reserves needed to fulfill all claims promptly.

- Customer service responsiveness, including how quickly a company assigns an adjuster and responds to communication, directly affects the reliability of the claims experience. Providers with 24/7 claims support and mobile claim filing options tend to resolve issues faster.

- The clarity of policy terms and exclusions also impacts payout reliability. Some insurers streamline the process by offering straightforward language and transparent coverage details, which reduces disputes over whether a loss is covered.

How to Evaluate Claims Performance Before Choosing a Provider

- Review third-party customer satisfaction rankings, such as those from J.D. Power’s U.S. Home Insurance Study or the American Customer Satisfaction Index (ACSI). These reports assess real customer experiences with the claims process, including ease of filing, fairness of settlement, and overall satisfaction.

- Check complaint indices published by state insurance departments and the National Association of Insurance Commissioners (NAIC). A significantly higher-than-average complaint ratio may indicate issues with claims handling or delayed payouts.

- Look into the insurer’s history of handling catastrophe claims. Companies that maintain fast response times and avoid prolonged delays after hurricanes, wildfires, or floods are generally more reliable when large numbers of claims are filed simultaneously.

What factors should I consider when selecting home insurance for a reliable and efficient claims experience?

Claims Processing Reputation and Customer Service

When selecting home insurance, evaluating an insurer’s claims processing reputation is critical for a smooth experience after a loss. A company known for prompt, fair, and hassle-free claims handling can significantly reduce stress during difficult times.

Research customer reviews, ratings from organizations like J.D. Power or the Better Business Bureau, and complaint indices from state insurance departments to gauge satisfaction levels. A responsive and supportive customer service team, available through multiple channels like phone, email, or mobile apps, ensures you can file and follow up on claims efficiently.

- Look for insurers with high customer satisfaction scores specifically related to claims handling.

- Check third-party ratings and consumer feedback regarding responsiveness and transparency during the claims process.

- Ensure the insurer offers 24/7 claims reporting and dedicated claims representatives for personalized support.

Speed of Claim Settlement and Payout Efficiency

The timeline from claim filing to receiving payment can vary significantly between providers, impacting your ability to repair or rebuild promptly.

Insurers with streamlined digital tools, automated evaluation systems, and experienced adjusters tend to settle claims faster. Some companies offer guaranteed timeframes for claims processing or advance payments for urgent repairs. Understanding these policies helps you choose a provider that aligns with your need for timely financial support after an incident.

- Compare average claim settlement times reported by insurers or revealed in consumer surveys.

- Select companies that provide direct deposit options and quick payout mechanisms to reduce waiting periods.

- Look for policies that allow partial or emergency payments while the full assessment is ongoing.

Clarity of Policy Terms and Support During the Claims Process

A clear, well-documented policy reduces confusion and disputes when filing a claim. Insurers that provide detailed explanations of coverage limits, exclusions, and required documentation make the claims process more predictable.

Additionally, access to adjusters who guide you through each step, help complete forms, and communicate regularly improves efficiency. Some carriers also offer online tracking portals so you can monitor your claim's status in real time, fostering transparency and trust.

- Choose insurers that use plain-language policy documents and offer pre-claim consultations if needed.

- Verify whether the provider assigns a single point of contact or claims handler for continuity.

- Ensure digital tools like mobile apps or online dashboards are available for uploading documents and receiving updates.

What phrases should you avoid during a home insurance claim to ensure a smooth process?

Admitting Fault or Speculating About the Cause

- Avoid saying anything that sounds like you’re taking responsibility for the damage, such as “It was my fault I left the faucet running” or “I probably should have repaired the roof earlier.” Even if true, admitting fault can give the insurer grounds to reduce or deny your claim.

- Do not speculate about how the incident occurred if you’re unsure. Phrases like “I think the electrician did something wrong” or “Maybe the pipe froze because I turned the heat down” introduce uncertainty that can delay investigation and lead to disputes.

- Stick to the facts you can verify. Instead of guessing, say, “I discovered water coming from the ceiling this morning,” or “I noticed smoke coming from the kitchen outlet when I turned on the toaster.”

Downplaying or Exaggerating the Damage

- Never understate the severity of the damage to seem cooperative, such as “It’s not that bad” or “We can probably just paint over it.” Doing so may result in insufficient coverage for necessary repairs.

- Equally problematic is overstating the damage with statements like “Everything is ruined” or “The whole house is unsafe.” Exaggerations can trigger suspicion of fraud and lead to a more aggressive investigation.

- Provide a detailed, honest account. Describe visible damage objectively: “The first floor has three inches of standing water,” or “The fire damaged the kitchen cabinets and scorched the wall.” Let assessors make their own conclusions.

Mentioning Prior Unreported Damage or Neglect

- Do not volunteer information about past damage that wasn’t repaired or previously reported, such as “The basement’s been leaking for months,” or “We’ve had mold issues since last winter.” This may be interpreted as negligence and jeopardize your claim.

- Avoid discussing delayed maintenance, even casually. Phrases like “I’ve been meaning to fix that gutter for years” or “We’ve ignored the crack in the foundation” can be used to argue that you failed to protect your property.

- Limits your comments to the current incident. If the insurer asks specific questions about prior issues, answer truthfully but briefly—do not offer unsolicited details that could complicate your case.

Frequently Asked Questions

What factors should I consider when evaluating an insurance company’s claims process?

Look for insurers with high customer satisfaction ratings, fast claim settlement times, and 24/7 claims reporting. Check third-party reviews and claim denial rates. A transparent, user-friendly online claims portal and availability of mobile apps also improve the experience. Ensure the insurer offers direct repair programs and clear communication throughout the process to minimize delays and frustration during critical times.

How can I find out if an insurance company pays claims fairly and promptly?

Review ratings from AM Best, J.D. Power, and the National Association of Insurance Commissioners (NAIC). Examine customer feedback on claim handling and response times. Compare how quickly companies acknowledge claims, assign adjusters, and issue payments. Avoid insurers with unusually high complaint index scores. Ask your agent for statistics on average claim resolution time and payout ratios to assess reliability and fairness.

Does the type of home insurance policy affect the claims process?

Yes, policy type impacts coverage limits, deductibles, and exclusions, all of which influence claim outcomes. A replacement cost policy typically offers faster, more predictable payouts than actual cash value. Specialized policies for floods or earthquakes require separate claims. Always understand your policy’s terms to avoid claim denials and ensure you’re covered for common risks in your area.

Are online insurance providers reliable when it comes to claims handling?

Many online insurers offer efficient, tech-driven claims processes with instant uploads and quick approvals. However, reliability varies by company. Research customer reviews and financial strength ratings to ensure stability. Some digital insurers partner with local agents or contractors to support complex claims. Choose a provider balancing innovation with proven customer service to ensure smooth support when filing a claim.

Leave a Reply