Home insurance flood cover

Flood damage can strike unexpectedly, leaving homeowners facing costly repairs and emotional distress. Standard home insurance policies typically exclude flood coverage, leaving many unprotected when natural disasters occur.

Home insurance flood cover provides essential protection by helping to repair or replace property damaged by flooding from external sources, such as heavy rain, overflowing rivers, or storm surges. This specialized coverage can include structural repairs, replacement of personal belongings, and additional living expenses during displacement.

Understanding the risks and securing appropriate flood insurance is crucial, especially for homes in high-risk areas. With climate change increasing flood frequency, proactive protection has never been more important.

Most Reputable Buyers For Life Insurance Policies

Most Reputable Buyers For Life Insurance PoliciesFlood Coverage in Home Insurance: What You Need to Know

Standard home insurance policies typically do not include protection against flood damage, leaving many homeowners vulnerable to significant financial loss during flood events. Flood coverage is generally offered as a separate policy through the National Flood Insurance Program (NFIP) in the United States or via private insurers.

This specialized coverage is essential for properties located in high-risk flood zones, although it can also benefit homes in moderate- to low-risk areas, as flooding can result from heavy rainfall, drainage issues, or nearby body of water overflow.

Understanding the limitations of standard home insurance, knowing when and how to obtain flood insurance, and evaluating the true cost of being uninsured are key steps in ensuring comprehensive protection for your home and belongings.

What Does Flood Insurance Cover?

Flood insurance provides financial protection for both the structure of your home and your personal belongings in the event of flood-related damage.

National Union Life And Limb Insurance Company

National Union Life And Limb Insurance CompanyStructural coverage typically includes essential components such as the foundation, walls, flooring, electrical systems, plumbing, and built-in appliances. Contents coverage, which may be offered as a separate component, protects personal property like furniture, clothing, and electronics.

It's important to note that not all water damage qualifies as flood damage—sewage backup or burst pipes may fall under standard home insurance, whereas flooding caused by overflowing rivers, storm surges, or heavy rainfall that inundates two or more acres and affects two or more properties qualifies under flood policies. Understanding these distinctions ensures you have the right type of protection for different types of water-related disasters.

Who Needs Flood Insurance and Where Is It Required?

Flood insurance is strongly recommended for homeowners in high-risk flood areas, particularly those located within Special Flood Hazard Areas (SFHAs) designated by the Federal Emergency Management Agency (FEMA).

Lenders often require flood insurance as a condition for mortgages on properties in these zones. However, nearly 25% of all flood insurance claims come from low- to moderate-risk areas, illustrating that flooding can occur anywhere due to extreme weather, inadequate drainage, or infrastructure failure.

New York Life Group Disability Insurance Attorney

New York Life Group Disability Insurance AttorneyEven if you're not in a high-risk zone, considering flood insurance can be a prudent financial decision, especially with the increasing frequency of severe weather events linked to climate change. Evaluating your property’s flood risk through FEMA flood maps and understanding your local vulnerability helps determine the necessity of coverage.

How to Purchase and Afford Flood Insurance

Obtaining flood insurance is typically done through the NFIP, a federal program administered by FEMA, or through private insurance providers that may offer more comprehensive or flexible plans.

To buy an NFIP policy, homeowners work with an authorized insurance agent, and policies usually have a 30-day waiting period before taking effect, emphasizing the need for proactive planning before flood threats emerge. Premiums are based on several factors, including flood zone designation, elevation of the home, property age, and the amount of coverage selected.

While costs can vary significantly—ranging from a few hundred to several thousand dollars annually—many policyholders find the expense manageable compared to the potentially devastating cost of unrepaired flood damage. Some communities participating in FEMA’s Community Rating System (CRS) may qualify for discounted premiums, further improving affordability.

Famers Life Insurance

Famers Life Insurance| Feature | Standard Home Insurance | Flood Insurance (NFIP) |

|---|---|---|

| Covers flooding from rivers or storms | No | Yes |

| Covers basement flooding | Limited | Yes, with restrictions on contents |

| Covers water damage from burst pipes | Yes | No |

| Waiting period before coverage starts | None | 30 days (NFIP) |

| Maximum building coverage (NFIP) | N/A | Up to $250,000 for residential properties |

Flood Coverage in Home Insurance: A Comprehensive Guide

Does standard home insurance include flood coverage?

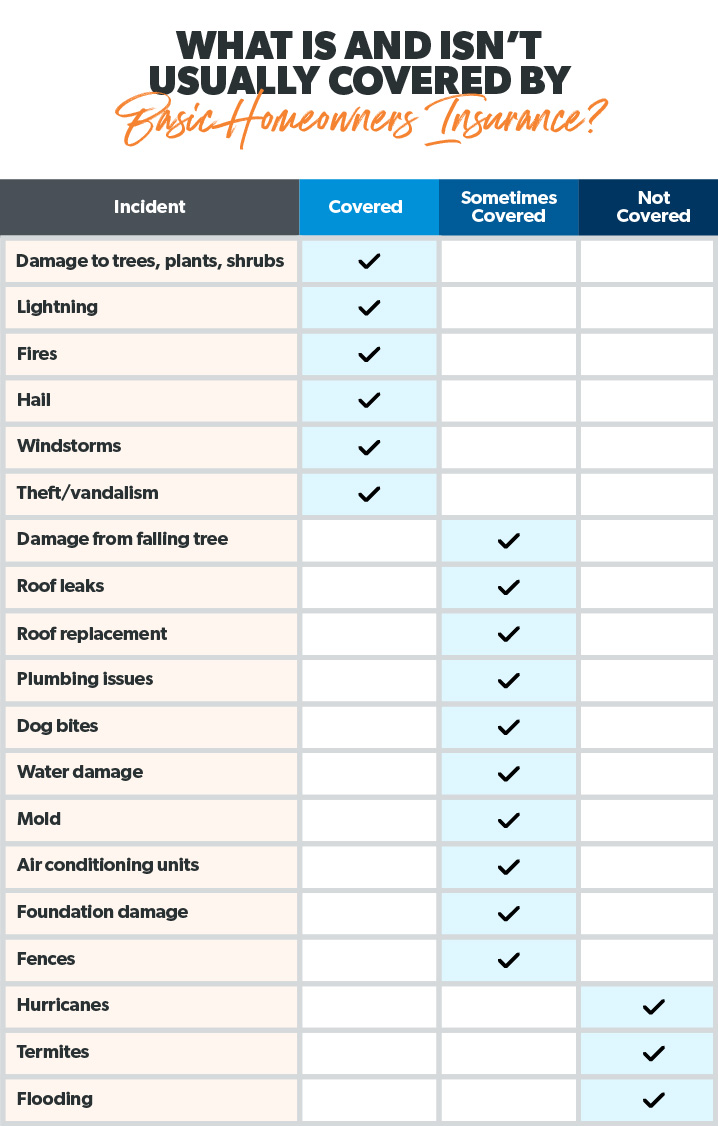

No, standard home insurance does not include flood coverage. Most homeowners insurance policies are designed to protect against sudden and accidental damages such as fire, theft, or windstorms, but they explicitly exclude damage caused by flooding.

Floods are typically defined as an overflow of water that covers land that is normally dry, and this type of risk requires a separate insurance policy. Homeowners in flood-prone areas or those who want added protection must purchase flood insurance through the National Flood Insurance Program (NFIP) or a private insurer.

What Types of Damage Are Covered by Standard Home Insurance?

- Standard home insurance typically covers structural damage to the dwelling from events like lightning strikes, fire, windstorms, hail, or vandalism.

- It also includes protection for personal property, such as furniture, electronics, and clothing, when damaged or destroyed by covered perils.

- Additional living expenses are covered if the home becomes uninhabitable due to a covered event, allowing for temporary housing and meals.

What Is Considered Flood Damage?

- Flood damage includes water that enters a home due to overflowing rivers, heavy rainfall causing ground saturation, or storm surges from hurricanes.

- Damage resulting from water that seeps through basement walls or comes up through drains during a flood event is also classified as flood-related.

- It's important to note that water damage from internal sources, like a burst pipe inside the home, is not considered flooding and is usually covered under standard policies.

How Can Homeowners Obtain Flood Coverage?

- Homeowners can purchase a standalone flood insurance policy through the National Flood Insurance Program, which is administered by FEMA.

- Some private insurers also offer flood insurance with broader coverage options or higher limits than the NFIP provides.

- To obtain coverage, applicants must determine their flood zone using FEMA maps, complete an application, and wait through a typical 30-day waiting period before the policy takes effect.

What is excluded from flood coverage in home insurance policies?

Standard Home Insurance Does Not Cover Flood Damage

Most standard homeowners insurance policies explicitly exclude damage caused by flooding. This means that if rising water from heavy rain, overflowing rivers, storm surges, or broken levees enters your home, the resulting damage is typically not covered under a regular policy.

Homeowners often mistakenly believe that water entering their property from external sources is included, but this is not the case. Flood damage is considered a separate risk and requires a specialized policy.

- Water damage from internal sources, such as burst pipes or leaky appliances, is usually covered under standard home insurance, as these are considered sudden and accidental.

- In contrast, water that enters from the outside due to weather events like hurricanes, prolonged rain, or overflowing bodies of water is classified as flood damage and excluded.

- Even if the flooding is indirectly caused by a covered peril—such as wind damage allowing rain to enter—the flood portion of the damage is not covered.

Basements and Crawl Spaces Have Limited Coverage

Flood insurance policies do offer some protection for basements and crawl spaces, but with significant limitations. Coverage for these areas is generally restricted to structural elements and essential systems, while personal belongings are largely excluded. Homeowners who store furniture, electronics, or other valuables in lower levels may find those items are not protected even under a flood policy.

- Coverage is typically limited to mechanical equipment like furnaces, water heaters, and electrical systems located in basements.

- Finished walls, floors, or built-in cabinetry in basements may receive minimal or no compensation, depending on policy specifics.

- Personal property such as rugs, furniture, clothing, or electronics stored in these areas is often not covered unless the policy includes additional personal contents coverage.

Earth Movement and Secondary Effects Are Not Included

Flood insurance does not cover damage resulting from earth movement, even if it is triggered by flooding. This includes landslides, mudflows, sinkholes, or foundation shifts caused by saturated soil. These perils are considered geologic hazards and fall outside the scope of flood coverage. Separate insurance policies or endorsements may be required to protect against such risks.

- Mudslides or mudflows, despite being water-borne, are not classified as floods under most insurance definitions and therefore are not covered.

- Damage to the foundation or structural integrity of a home caused by soil erosion or shifting due to water saturation is typically excluded.

- Homeowners in areas prone to landslides or subsidence may need geotechnical assessments and additional insurance products to ensure full protection.

How much does home insurance cover for flood damage?

Flood Damage Coverage Under Standard Homeowners Insurance

Standard homeowners insurance policies typically do not cover flood damage. Most common home insurance plans, such as HO-3 or HO-5 policies, specifically exclude losses caused by flooding from external sources like overflowing rivers, storm surges, or heavy rainfall that leads to standing water.

This means if your home sustains damage due to inundation from natural water sources, the repair and recovery costs are not covered under your regular policy.

Homeowners are often surprised by this exclusion, assuming all types of water damage are included. However, damage from burst pipes or appliance leaks is generally covered, as those are considered internal incidents rather than flooding from external forces.

- Flood damage caused by overflowing lakes, rivers, or coastal storms is excluded from standard home insurance.

- Water damage originating from inside the home, such as a leaking pipe or malfunctioning appliance, is usually covered.

- Understanding policy exclusions is crucial, as many homeowners mistakenly believe water-related damage is automatically included.

Obtaining Flood Insurance Through the NFIP

To protect against flood-related losses, homeowners can purchase separate flood insurance through the National Flood Insurance Program (NFIP), administered by the Federal Emergency Management Agency (FEMA). This government-backed program provides up to $250,000 in coverage for the structure of a single-family home and up to $100,000 for personal belongings.

The actual amount disbursed depends on various factors, including the severity of the damage, the home’s elevation, and the terms of the flood policy. It’s important to note that NFIP policies have a 30-day waiting period before they become active, so purchasing insurance after a storm is announced will not provide immediate protection.

- NFIP offers structural coverage up to $250,000 and content coverage up to $100,000 for residential properties.

- Coverage decisions are based on flood zone classification, property elevation, and the extent of the damage.

- There is a mandatory 30-day waiting period after purchasing a policy before it takes effect.

Supplemental Flood Insurance and Private Market Options

In addition to the NFIP, private insurers offer supplemental flood insurance that can provide higher coverage limits and additional protections not included in federal policies. These private plans are particularly useful for homeowners in high-risk flood zones or those with valuable property and possessions that exceed NFIP limits.

Some private policies also cover additional living expenses, loss of use, or damage from sewer backups – aspects not fully addressed by standard NFIP coverage. Premiums vary widely depending on the insurer, location, and property characteristics, so it’s advisable to compare multiple options to find a plan that meets your specific needs.

- Private flood insurance can offer coverage exceeding the NFIP’s $250,000 limit for dwellings.

- Some private policies include additional protections like loss of use or basement flooding, which NFIP may exclude.

- It’s beneficial to shop around and compare premiums, coverage terms, and exclusions among private insurers.

What does the 80% rule mean for flood coverage in home insurance?

The 80% rule in the context of flood coverage for home insurance is often misunderstood because it does not directly apply to flood insurance policies issued through the National Flood Insurance Program (NFIP).

Instead, the 80% rule is primarily associated with standard homeowners insurance and refers to the coinsurance clause that requires homeowners to insure their dwelling for at least 80% of its replacement cost to receive full compensation for a partial loss. However, when discussing flood risks and coverage, a similar principle can indirectly affect how much protection a homeowner receives.

In flood insurance, full coverage is generally only provided if the policyholder insures for the full replacement value or up to the NFIP coverage limits, whichever is lower. Failing to carry sufficient coverage may result in the insured receiving a reduced claim payout, especially in cases of substantial damage. Understanding this concept is essential for homeowners in flood-prone areas to avoid being underinsured.

How the 80% Rule Applies to Standard Home Insurance

- The 80% rule in traditional home insurance means that insurers require policyholders to insure their home for at least 80% of its current replacement cost to qualify for full reimbursement in the event of a covered loss that is not total.

- If a homeowner insures for less than 80% of the replacement value, the insurance company applies a coinsurance penalty, meaning the payout for a claim is reduced proportionally based on the amount of underinsurance.

- For example, if a home’s replacement cost is $300,000 and the homeowner only carries $200,000 in coverage (which is about 67%), they are below the 80% threshold; therefore, if a $50,000 covered loss occurs, the payout may be reduced significantly, potentially leaving the homeowner to pay more out of pocket.

Why the 80% Rule Doesn’t Directly Affect NFIP Flood Insurance

- The National Flood Insurance Program does not enforce a coinsurance clause like the 80% rule found in standard home policies, which means there is no automatic penalty for underinsuring the structure.

- However, to receive the maximum structural coverage available under the NFIP—up to $250,000 for the dwelling—the homeowner must carry coverage equal to at least 80% of the structure’s replacement cost or the maximum available limit, whichever is less, especially if they are required by a mortgage lender.

- Without meeting this threshold, if a substantial flood loss occurs, the homeowner may find that the claim reimbursement is inadequate to cover repair or rebuild expenses, effectively creating a financial gap despite having a policy.

How Homeowners Can Avoid Coverage Gaps in Flood-Prone Areas

- Homeowners should get a current replacement cost estimate for their homes and ensure their flood insurance coverage meets or exceeds 80% of that value, even if the NFIP does not enforce it strictly.

- They can supplement an NFIP policy with private flood insurance to exceed the program’s limits, which helps cover full rebuild costs and accounts for inflation or increased construction expenses after a flood event.

- Regularly reviewing and updating policies, especially after home improvements or changes in local flood risks, ensures that coverage keeps pace with current rebuilding costs and maintains adequate financial protection against flood damage.

Frequently Asked Questions

What does home insurance flood cover typically include?

Home insurance flood cover typically includes damage to the structure of your home and personal belongings caused by flooding from natural sources like heavy rain, overflowing rivers, or storm surges. It may cover repairs to walls, floors, and built-in appliances, as well as cleanup costs like mold remediation. However, standard policies often exclude flood damage, so a separate flood insurance policy is usually required for full protection.

Is flood damage covered under a standard homeowners insurance policy?

No, flood damage is generally not covered under a standard homeowners insurance policy. Most policies exclude damage caused by surface water, overflowing bodies of water, or sewer backups due to flooding. To be protected, you typically need to purchase a separate flood insurance policy through the National Flood Insurance Program (NFIP) or a private insurer, especially if you live in a high-risk flood area.

How can I purchase flood insurance for my home?

You can purchase flood insurance through the National Flood Insurance Program (NFIP), which is administered by FEMA, or through private insurance companies. Contact your current home insurance provider to see if they offer flood coverage, or visit the NFIP website to find an approved agent. Policies usually require a 30-day waiting period before coverage takes effect, so plan ahead.

What factors affect the cost of flood insurance coverage?

The cost of flood insurance depends on several factors, including your property's location, flood zone rating, elevation, home age, and construction type. Properties in high-risk flood areas typically have higher premiums. Other factors include the coverage amount, deductible selected, and whether the building meets current floodplain management standards. Working with an agent can help you understand and compare your options.

Leave a Reply