New York Life Group Disability Insurance Attorney

Navigating the complexities of New York Life group disability insurance claims can be overwhelming, especially when benefits are delayed or denied.

Many policyholders are unaware of their rights and the legal options available to challenge unfair decisions. A knowledgeable New York Life group disability insurance attorney plays a crucial role in guiding individuals through the appeals process, ensuring proper documentation, and advocating for timely and fair benefits.

These legal professionals specialize in disability insurance law and understand the tactics insurers may use to minimize payouts. With expert legal representation, claimants can significantly improve their chances of securing the financial support they deserve during times of medical hardship.

Business Owners Insurance Quote Charlotte

Business Owners Insurance Quote CharlotteWhat to Know About a New York Life Group Disability Insurance Attorney

A New York Life group disability insurance attorney specializes in helping individuals who are part of group disability insurance policies issued by New York Life, one of the largest and most established life and disability insurance providers in the United States.

These attorneys focus on representing policyholders when their disability claims have been denied, delayed, or underpaid. Since group disability policies are often governed by federal laws like the Employee Retirement Income Security Act (ERISA), navigating the claims and appeals process can be complex and legally demanding.

A knowledgeable attorney can guide claimants through the required administrative procedures, gather medical and employment evidence, and file appeals or lawsuits when necessary. Their expertise is particularly important because mistakes during the application or appeal phase can result in a permanent loss of benefits.

The Role of an Attorney in New York Life Disability Claims

A New York Life group disability insurance attorney plays a critical role in protecting the rights of policyholders who are unable to work due to a disabling medical condition.

Best Life Insurance Companies That Pay Outfinance

Best Life Insurance Companies That Pay OutfinanceThese legal professionals understand the intricacies of group long-term or short-term disability plans offered through employers and underwritten by New York Life. They assist clients by reviewing the terms of the insurance policy, ensuring that all documentation—including medical records and employer statements—is properly submitted, and interpreting complex definitions of disability defined in the policy.

When a claim is denied, the attorney prepares and files a formal appeal, which is a mandatory step under ERISA before taking legal action. Their intervention significantly increases the likelihood of a successful claim resolution by holding the insurer accountable and advocating for fair treatment based on the policyholder’s contractual rights.

Why ERISA Matters in New York Life Disability Cases

Most group disability insurance plans, including those offered by New York Life through an employer, are governed by the Employee Retirement Income Security Act (ERISA).

This federal law sets standards for claims processing, appeals, and legal recourse, but it also imposes strict rules that must be followed precisely. For instance, claimants typically have only 180 days to appeal a denial, and all legal arguments must be based on the administrative record created during the claim and appeal phases—meaning new evidence cannot be introduced in court.

Best Life Insurance For 40 Year Old

Best Life Insurance For 40 Year OldAn experienced New York Life group disability insurance attorney understands these ERISA-specific requirements and ensures that clients do not miss deadlines or compromise their right to sue. Because ERISA regulations heavily favor insurance companies procedurally, professional legal guidance becomes essential to level the playing field and protect the claimant's interests.

Common Reasons for New York Life Disability Claim Denials

Even with comprehensive group coverage through New York Life, many disability claims are initially denied for various reasons, often related to technicalities or insufficient documentation.

Common causes include failure to meet the policy’s strict definition of disability, gaps in medical treatment, lack of objective medical evidence, or failure to exhaust administrative appeals. Insurers may also argue that the disabling condition is not severe enough to prevent the individual from performing any occupation, especially after a transition period.

A skilled attorney can analyze the denial letter, identify the insurer’s rationale, and address the specific deficiencies in a powerful appeal. By ensuring that all medical documentation aligns with policy requirements and by clearly demonstrating functional limitations, legal representation can reverse unjust denials and secure the financial support the claimant deserves.

| Aspect | Details |

|---|---|

| Governing Law | Most group disability claims involving New York Life are regulated by ERISA, a federal law that standardizes employee benefit plans. |

| Appeal Deadline | Under ERISA, policyholders typically have 180 days from the denial date to file a formal appeal. |

| Legal Representation | Hiring a disability insurance attorney increases the chances of approval by ensuring compliance with complex procedures. |

| Common Denial Reasons | Insufficient medical evidence, failure to meet the definition of disability, or procedural errors during filing. |

| Coverage Type | Group policies are typically offered through employers and may include short-term or long-term disability benefits. |

Comprehensive Guide to New York Life Group Disability Insurance Claims and Legal Representation

How long does long-term disability coverage last under New York Life group insurance policies?

Duration of Long-Term Disability Coverage Under New York Life Group Policies

- New York Life group long-term disability (LTD) insurance typically provides benefits for a defined period, which can vary based on the specific policy terms established by the employer or plan sponsor. Coverage duration is generally structured around a benefit period, which may extend for a set number of years or up to a certain age.

- Common benefit periods offered include coverage up to age 65, up to age 67, or for a fixed duration such as 5 or 10 years from the date disability benefits begin. The exact length depends on the plan design and the terms outlined in the group policy contract.

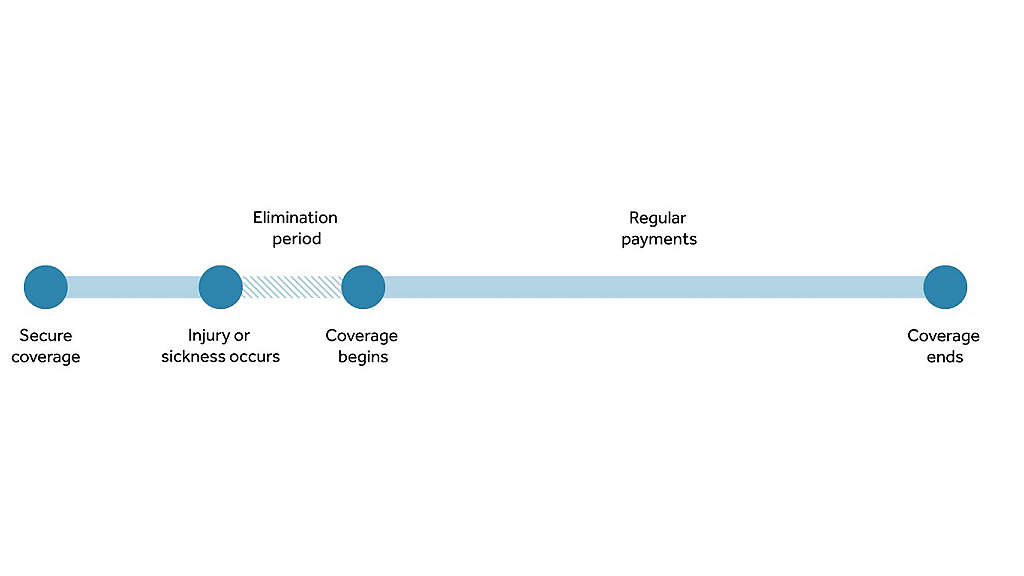

- It is important to note that eligibility for benefits also depends on satisfying the policy's definition of disability and the elimination period, which is typically 90 to 180 days of continuous disability before benefits are payable. Once the elimination period is met, the long-term benefit period begins and continues as long as the insured remains disabled per policy terms.

Factors That Influence the Length of LTD Benefits

- The length of long-term disability coverage under a New York Life group policy is heavily influenced by the plan document selected by the employer. Employers may offer different options, such as shorter benefit periods for lower-paid employees and longer periods for higher-paid or executive-level employees.

- Another major factor is the definition of disability used in the policy. During the first 24 months of benefit payments, disability is often defined as being unable to perform the material duties of one’s own occupation. After this period, the definition typically changes to any occupation for which the individual is reasonably suited by education, training, or experience, which can affect the continuation of benefits.

- Additional influences include whether the policyholder complies with medical review requirements, provides ongoing proof of disability, and adheres to the policy’s reporting mandates. Failure to meet these ongoing conditions can result in early termination of benefits regardless of the stated benefit period.

Options for Extending or Customizing LTD Coverage

- Some New York Life group LTD policies allow for optional riders or enhancements that can extend the benefit period or improve coverage terms. For example, a cost-of-living adjustment (COLA) rider may increase benefits over time, and a future increase option may allow for higher coverage as the employee’s income grows.

- Employees may also have the opportunity to purchase supplemental individual long-term disability insurance alongside their group coverage to extend protection beyond the limits or duration of the group policy. These individual policies can provide benefits that last until retirement age even if the group policy ends earlier.

- Employers can choose to include provisions such as guaranteed renewable terms or portability options, allowing employees to continue coverage under certain circumstances, like job changes, although long-term disability coverage is typically not portable in the same way as life or health insurance.

What disability insurance options does New York Life provide for group policyholders?

![]()

Short-Term Disability Insurance for Group Policyholders

New York Life offers short-term disability (STD) insurance as part of its group benefits package, designed to provide income protection for employees who are temporarily unable to work due to illness, injury, or childbirth.

This coverage typically begins shortly after the employee becomes disabled—usually after a brief waiting period of 7 to 14 days—and continues for a predetermined duration, generally ranging from a few weeks up to six months, depending on the policy terms. Short-term disability helps maintain financial stability for employees during temporary absences, allowing them to focus on recovery without the added burden of lost wages.

- Provides benefit payments that replace a percentage of the employee's pre-disability income, commonly between 60% to 70%.

- Coverage is typically fully or partially employer-paid, with options for employee contributions through payroll deductions.

- Policies can be customized through New York Life to meet the specific needs of employers, including variation in waiting periods and benefit durations.

Long-Term Disability Insurance for Group Policyholders

Long-term disability (LTD) insurance from New York Life is designed to offer extended financial protection to group policyholders when a disability extends beyond the short-term period. This coverage usually begins after a waiting period that ranges from 90 to 180 days and can provide benefits for several years, up to retirement age in some cases, depending on the policy’s terms.

Long-term disability insurance helps ensure that employees who face serious health issues maintain a consistent income stream, supporting their long-term financial needs during prolonged periods of incapacity.

- Replaces a portion of the employee’s monthly income, generally between 50% and 60%, to help cover everyday expenses during extended disability.

- Benefits may be adjusted based on other income received, such as Social Security disability payments, following policy offset provisions.

- Employers can tailor the plan design, including elimination periods, benefit periods, and coverage caps, in coordination with New York Life’s underwriting team.

Optional Riders and Additional Group Coverage Features

To enhance the flexibility and value of its group disability offerings, New York Life provides optional riders and supplementary features that can be added to both short-term and long-term disability plans.

These enhancements allow employers to build more comprehensive benefit packages that better support employee well-being and retention.

Options such as premium conversion, dependent care disability benefits, and return-to-work programs help differentiate a company’s benefits package while adding meaningful support during challenging times.

- Residual or partial disability riders allow employees to receive benefits when returning to work on a limited basis, ensuring continued support during gradual recovery.

- Waiver of premium riders may be available, which excuse premium payments while the insured is receiving disability benefits.

- Employers can integrate disability coverage with other group benefits like life insurance and wellness programs, enabling a holistic approach to employee protection through New York Life’s integrated platforms.

Frequently Asked Questions

What is a New York Life group disability insurance attorney?

A New York Life group disability insurance attorney is a legal professional specializing in helping policyholders file, appeal, or litigate disability claims under New York Life’s group long-term or short-term disability plans. These attorneys understand ERISA regulations and assist clients in navigating complex claims processes, gathering medical evidence, and challenging wrongful denials to secure rightful benefits.

Why do I need an attorney for my New York Life disability claim?

You may need an attorney for your New York Life disability claim because insurance companies often deny legitimate claims or delay payments. An experienced attorney ensures your application or appeal meets all requirements, compiles essential medical documentation, and represents you effectively under ERISA guidelines. Legal representation significantly increases your chances of approval and helps protect your rights throughout the claims process.

What should I do if New York Life denies my disability claim?

If New York Life denies your disability claim, review the denial letter carefully and begin an appeal immediately, as strict deadlines apply under ERISA. Consult a disability attorney to assess the reasons for denial, strengthen your case with additional medical evidence, and file a comprehensive appeal. Never skip the administrative appeal process, as it’s required before you can sue in federal court.

How much does it cost to hire a New York Life disability attorney?

Most New York Life disability attorneys work on a contingency fee basis, meaning they only get paid if you win your case, typically receiving a percentage (often 30-40%) of your back benefits. Initial consultations are usually free. This fee structure allows access to legal representation without upfront costs and aligns the attorney’s incentives with achieving a successful outcome for your disability claim.

Leave a Reply