Home insurance insurance quote

Understanding the value of a home insurance quote is essential for homeowners seeking financial protection and peace of mind.

A home insurance quote provides an estimate of the cost to insure a property, factoring in elements such as location, home size, construction type, and coverage needs. Comparing quotes helps individuals find policies that offer comprehensive protection at competitive rates. Insurance providers evaluate risks like natural disasters, theft, and liability when calculating premiums.

Accurate quotes depend on up-to-date, detailed information, making it crucial to assess personal needs carefully. Securing multiple quotes ensures informed decisions for long-term security.

New York Life Group Disability Insurance Attorney

New York Life Group Disability Insurance AttorneyUnderstanding Home Insurance Quotes: What You Need to Know

Obtaining a home insurance quote is a crucial step in protecting your property and ensuring financial security against unexpected events such as fires, theft, or natural disasters. A home insurance quote is an estimate of how much it will cost to insure your home, based on various factors including the home's location, size, age, construction type, and the level of coverage you choose.

Insurance providers analyze these details to assess risk and calculate a premium that reflects the likelihood and potential cost of claims. It’s important to gather multiple quotes from different insurers to compare costs and coverage options, as rates can vary significantly.

Accurate information during the quoting process ensures you receive a reliable estimate and avoids surprises when claims arise. Additionally, many insurers offer online tools that allow you to customize your coverage and instantly receive a quote, making the process more convenient and transparent.

Factors That Influence Your Home Insurance Quote

Several key elements affect the price of your home insurance quote, and understanding them can help you find cost-effective coverage. The location of your home plays a major role—properties in areas prone to hurricanes, wildfires, or high crime rates typically face higher premiums.

Famers Life Insurance

Famers Life InsuranceThe age and condition of the home also matter; older homes may require more expensive coverage due to outdated electrical or plumbing systems. Other factors include the construction materials, square footage, presence of safety features like smoke detectors or security systems, and your credit score, which insurers often use as a predictor of risk.

Additionally, your claims history and the coverage limits you select—such as dwelling coverage, personal property, and liability—will directly influence the final quote. By addressing risk factors proactively, such as reinforcing your roof or upgrading wiring, you may qualify for lower rates.

How to Get an Accurate Home Insurance Quote Online

To receive an accurate home insurance quote online, start by gathering essential information about your property, including its square footage, year built, roof type, and any recent renovations. Most insurers require details about security systems, heating and cooling systems, and whether your home has risk factors like wood-burning stoves or swimming pools.

When using online quote tools, provide precise answers to ensure the estimate reflects your actual insurance needs. It’s also helpful to list the value of your personal belongings to determine appropriate personal property coverage.

Fidelity Life Insurance Login Pay Bill

Fidelity Life Insurance Login Pay BillBe aware that while online quotes offer speed and convenience, they may not account for every nuance—some insurers may adjust your rate after an inspection or underwriting review. Comparing at least three quotes helps identify the best balance of coverage, cost, and customer service.

Common Mistakes to Avoid When Shopping for Home Insurance Quotes

Many homeowners make avoidable errors when seeking a home insurance quote, which can result in inadequate coverage or inflated premiums. One common mistake is underestimating the rebuild cost of your home by confusing it with market value; insurance is meant to cover reconstruction, not property appreciation.

Another issue is failing to update coverage after home improvements, leaving newly added square footage or upgraded materials unprotected. Some shoppers also focus solely on premium price, ignoring policy details like deductibles, exclusions, and limits, which can lead to surprises during a claim.

Additionally, not disclosing certain risks—like renting out part of your home or keeping high-value items without scheduling them—can void coverage. To avoid these pitfalls, ask questions, review policy documents carefully, and consider consulting an insurance agent for personalized advice.

Highest Offer Life Insurance Policy Settlement

Highest Offer Life Insurance Policy Settlement| Factor | Impact on Quote | Tips to Reduce Cost |

|---|---|---|

| Home Location | High-risk areas increase premiums | Choose insurers with regional discounts or bundling options |

| Credit Score | Affects eligibility and rates | Maintain a good credit history |

| Security Features | Can reduce premiums | Install deadbolts, smoke detectors, and monitored alarm systems |

| Deductible Amount | Higher deductible = lower premium | Select a deductible you can afford in case of a claim |

| Claims History | More claims = higher rates | Avoid filing small claims to maintain a clean record |

How to Get an Accurate Home Insurance Quote: A Step-by-Step Guide

Which providers offer the most affordable home insurance quotes?

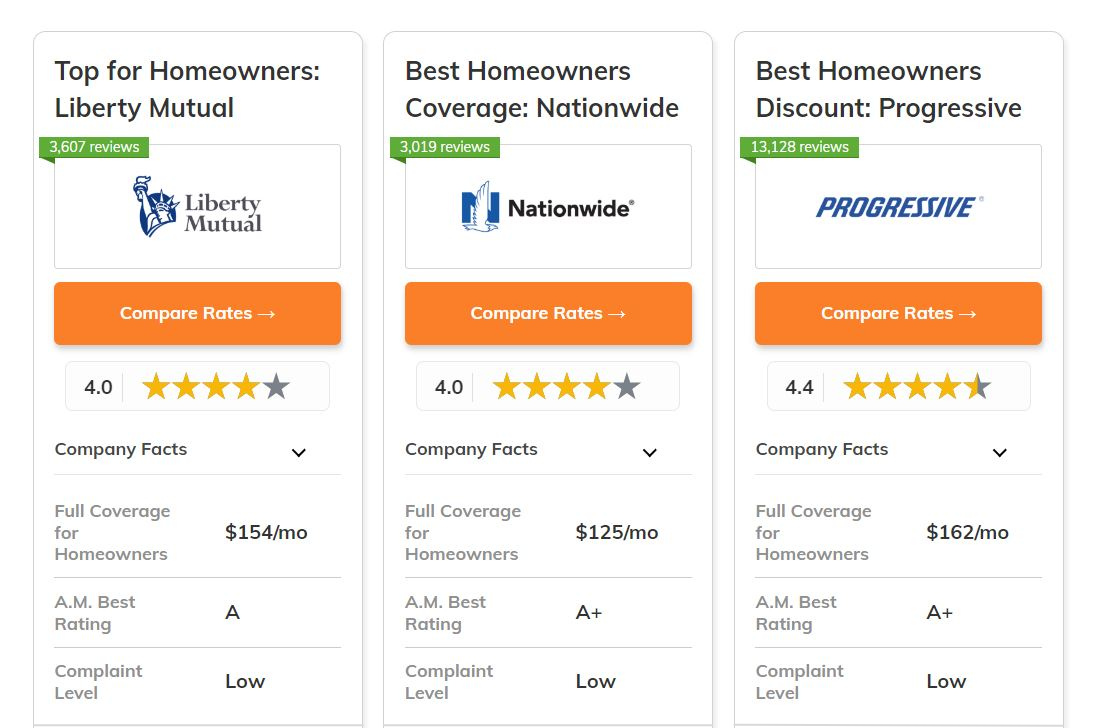

Top Budget-Friendly Home Insurance Providers

Several insurance companies consistently rank among the most affordable options for homeowners insurance. These providers balance low premiums with reliable coverage and customer service.

Key players include Nationwide, Allstate, and Farmers Insurance, which often offer competitive base rates. Additionally, regional carriers like State Farm and USAA (available to military families and veterans) are known for strong pricing, especially in areas prone to fewer natural disasters.

The affordability of each provider can vary significantly based on location, home value, and personal risk factors, so it’s crucial to compare multiple quotes. Digital-first insurers like Lemonade and Hippo are also emerging as cost-effective alternatives, particularly for tech-savvy homeowners who prefer online management.

How Do You Qualify For Life Insurance

How Do You Qualify For Life Insurance- Nationwide offers multiple discount programs, including claims-free and home safety discounts, which can reduce premiums by up to 30%.

- Allstate’s Digital Wallet and automation tools allow customers to adjust policies in real time, often unlocking lower rates based on updated home data.

- Farmers Insurance provides a “Circle of Safety” discount bundle that combines home, auto, and other policies for greater savings.

Factors That Influence Home Insurance Affordability

The cost of home insurance is shaped by a combination of personal, geographic, and structural factors. Providers evaluate your home’s age, construction type, claims history, and proximity to fire stations and hydrants.

Location plays a major role—homes in areas with high crime or frequent severe weather (like hurricanes or wildfires) typically cost more to insure. Insurers also consider your credit-based insurance score, which correlates with claims likelihood.

Moreover, increasing your deductible can lower your monthly premium, though it raises out-of-pocket costs in case of a claim. Bundling home and auto insurance is one of the most effective ways to access discounted rates across multiple policies.

- Homes constructed with fire-resistant materials or upgraded plumbing and electrical systems often qualify for lower premiums due to reduced risk.

- Installing security systems, smoke detectors, and storm shutters can yield discounts of 5% to 20% from insurers like State Farm and Liberty Mutual.

- Insurers such as USAA and Amica reward long-term customers with loyalty discounts, which accumulate over time for consistent policyholders.

How to Compare and Secure the Lowest Quotes

To find the most affordable home insurance, it's essential to compare quotes from at least five different providers. Online comparison tools from sites like NerdWallet, Insurify, and The Zebra allow side-by-side evaluation of coverage and pricing.

When reviewing quotes, make sure the policies offer similar coverage limits and deductibles to ensure accurate comparisons. Adjusting coverage levels or eliminating unnecessary add-ons (such as equipment breakdown protection) can also reduce costs.

Many insurers offer price-match guarantees or loyalty bonuses if you find a lower rate elsewhere. Additionally, periodically reassessing your policy—especially after home improvements or credit score increases—can lead to better rates.

- Request quotes online from major insurers including Progressive, Nationwide, and Travelers, ensuring all use identical coverage parameters.

- Use independent insurance agents who have access to multiple carriers and can negotiate tailored deals based on your risk profile.

- Ask about seasonal promotions or new customer discounts—some insurers reduce rates by up to 15% for signing up during specific campaigns.

What is the most affordable home insurance provider for an online quote?

The most affordable home insurance provider for an online quote varies depending on location, home value, credit history, and coverage needs, but companies like Progressive, Allstate, and Nationwide frequently offer competitive rates through their online platforms.

Progressive is often recognized for its strong comparison tool, which allows customers to evaluate quotes not only from Progressive but from other insurers as well, helping identify the lowest available price. Allstate provides customizable policies with optional discounts for bundling, safety features, and loyalty, which can significantly reduce premiums. Nationwide tends to offer low average rates for standard home insurance, particularly for customers with strong credit and a claim-free history.

It’s essential to input accurate information when requesting online quotes, as minor variations can influence the final cost. Additionally, local and regional insurers may offer even lower prices in specific areas, so using independent comparison sites like Insurify, NerdWallet, or The Zebra can help uncover less-known but economical options.

Factors That Influence Home Insurance Quote Accuracy Online

- Personal information such as credit score, claims history, and occupation can have a direct impact on the quoted premium, as most insurers use risk-based pricing models that assess likelihood of future claims.

- The physical characteristics of the home, including age, construction type, roof condition, and location-specific risks like flood zones or wildfire areas, are critical data points used to calculate accurate quotes.

- Desired coverage levels—such as dwelling coverage, personal property limits, and liability protection—affect the final price, and providing detailed, realistic figures ensures that the quote reflects actual insurance needs rather than an under- or over-estimated policy.

How to Compare Multiple Online Home Insurance Quotes Effectively

- Use aggregator websites like Bankrate, Policygenius, or QuoteWizard that pull rates from multiple insurers, enabling side-by-side comparisons based on identical coverage parameters and home details.

- Ensure each quote includes the same coverage limits, deductible amounts, and additional protections like personal liability or water backup coverage to maintain consistency in evaluation.

- Review customer satisfaction ratings and financial strength from organizations like J.D. Power or AM Best to balance affordability with reliability, as a lower premium from a company with poor claims service may cost more in the long run.

Discounts That Can Lower Your Online Home Insurance Rate

- Many insurers offer multi-policy discounts when bundling home and auto insurance, with savings that can range from 10% to 25%, making bundling a key strategy to reduce overall insurance costs.

- Installing safety and security features such as monitored alarm systems, deadbolts, smoke detectors, or storm shutters can result in substantial discounts, often between 5% and 20%, depending on the device and insurer.

- Loyalty programs and paperless billing options may also lead to reduced rates, and some companies reward claim-free years with incremental discounts, further improving affordability over time.

What is the average cost of a home insurance quote?

The average cost of a home insurance quote varies significantly depending on location, home value, coverage needs, and individual risk factors.

Nationwide in the United States, the average annual cost of homeowners insurance is approximately $1,700 to $1,900, according to data from the Insurance Information Institute and other insurance analytics firms. However, this figure can be much lower or higher based on regional risks such as hurricanes, wildfires, or tornadoes.

Insurance quotes are not one-size-fits-all; they are personalized estimates based on the structure of the home, chosen deductible, coverage limits, and the homeowner’s claims history. It's important to note that a quote is not a fixed price—it's an estimate that can change after underwriting review.

Factors That Influence Home Insurance Quotes

- Geographic location plays a major role—homes in areas prone to natural disasters such as floods, earthquakes, or hurricanes typically face higher premiums due to increased risk of claims.

- The age, size, and construction materials of the home affect pricing; older homes or those built with wood may cost more to insure than newer, fire-resistant structures.

- Personal factors such as credit score, claims history, and insurance score also impact the quote, as insurers use them to assess the likelihood of future claims.

Types of Coverage and Their Impact on the Quote

- Standard home insurance policies typically include dwelling coverage, personal property protection, liability insurance, and additional living expenses, each contributing to the overall cost of the quote.

- Optional coverages such as scheduled personal property, identity theft protection, or equipment breakdown can increase the quote but offer enhanced protection for specific needs.

- High coverage limits or lower deductibles will raise the premium because the insurer assumes greater financial responsibility in the event of a claim.

How to Obtain Accurate and Competitive Home Insurance Quotes

- Comparing multiple quotes from different insurers is essential, as pricing models and customer profiles vary widely between companies, leading to significant differences in premiums.

- Providing precise and complete information about the home—such as the roof’s age, security systems, and prior claims—helps ensure the quote reflects the actual risk and avoids surprises later.

- Reviewing available discounts, such as bundling home and auto insurance, installing smart home devices, or maintaining a claim-free history, can reduce the quoted price substantially.

What home insurance company offers the lowest quotes in Louisiana?

Determining the home insurance company that offers the lowest quotes in Louisiana can vary based on location, home characteristics, and individual risk profiles.

However, data from sources like the National Association of Insurance Commissioners (NAIC) and third-party comparison sites consistently show that Allstate, State Farm, and USAA frequently provide some of the most competitive rates across different regions of the state. USAA, available exclusively to military members and their families, often ranks among the cheapest options due to its strong customer loyalty programs and bundled discounts.

State Farm tends to offer lower premiums in suburban and rural areas, while Allstate may provide competitive pricing with added flexibility in coverage options. It is essential to obtain personalized quotes because rates can differ significantly even between adjacent neighborhoods due to flood zones, crime rates, and construction materials.

Factors Influencing Home Insurance Rates in Louisiana

- Location within Louisiana plays a crucial role, as coastal areas like New Orleans have higher risks of hurricanes and flooding, leading to increased premiums compared to inland regions such as Shreveport or Baton Rouge.

- The age and condition of the home affect pricing, with older homes or those with outdated electrical, plumbing, or roofing systems generally incurring higher costs due to increased risk of claims.

- Insurance companies use credit-based insurance scores in Louisiana, meaning individuals with higher credit scores often qualify for lower rates, assuming all other factors are equal.

Top Competitors for Low-Cost Home Insurance in Louisiana

- Allstate provides customizable policies and frequent discounts, such as bundling home and auto insurance, installing security systems, or remaining claims-free, all of which can significantly reduce premiums.

- State Farm, with an extensive network of local agents, offers personalized service and competitive base rates, especially in rural parishes where its agent presence is strong.

- USAA consistently ranks high for affordability among eligible customers, offering robust coverage options and superior customer satisfaction ratings, which often translate into long-term savings through loyalty discounts.

How to Get the Most Accurate Quote for Your Louisiana Home

- Use online comparison tools from reputable websites such as NerdWallet, Bankrate, or Insurify, which allow side-by-side comparisons of multiple insurers based on your specific ZIP code and home details.

- Contact local independent agents who represent more than one insurance company, giving them the ability to shop around and find tailored options that better match your needs and budget.

- Ensure your home’s risk profile is up to date—installing storm shutters, reinforced roofing, or a monitored alarm system may qualify you for additional discounts that lower your annual premium.

Frequently Asked Questions

What is a home insurance quote?

A home insurance quote is an estimate of how much you'll pay for homeowners insurance based on your property's characteristics, location, coverage needs, and personal factors like credit score. Insurers use this information to calculate your premium. Quotes are typically free and don’t obligate you to buy. Getting multiple quotes helps compare prices and coverage options to find the best policy for your needs.

How do I get a home insurance quote online?

To get a home insurance quote online, visit an insurer’s website or use a comparison platform. Provide details about your home, such as its size, age, location, construction type, and desired coverage. You may also need personal information like your claims history. After submitting the form, you’ll receive estimated premiums from one or more providers. Review each quote carefully to ensure coverage meets your needs before making a decision.

Why do home insurance quotes vary between companies?

Home insurance quotes differ between companies because each insurer uses its own pricing models, risk assessments, discounts, and underwriting guidelines. Factors like your home’s location, claim history, and credit score may be weighted differently. Some insurers specialize in certain regions or home types. Additionally, available discounts and customer service offerings can impact pricing. Comparing multiple quotes ensures you find both competitive rates and reliable coverage tailored to your situation.

Does getting a home insurance quote affect my credit score?

Getting a home insurance quote does not hurt your credit score. Insurers perform a soft credit check, which doesn’t impact your score. Soft inquiries are only visible to you and are used to assess risk and pricing. You can shop around and compare multiple quotes without worrying about credit consequences. However, if you later purchase a policy, the insurer may conduct another soft check, which also has no effect on your credit.

Leave a Reply