How to prepare for a successful home insurance claim

Preparing for a successful home insurance claim starts long before disaster strikes. Homeowners who take proactive steps significantly increase their chances of a smooth and fair settlement process.

Documentation is key—keeping detailed records of possessions, property conditions, and maintenance can make a critical difference. Understanding your policy, knowing what is covered, and maintaining open communication with your insurer are equally important.

A well-prepared claim reduces delays and disputes. By organizing vital information and taking preventive measures, you safeguard not only your property but also your financial security when filing a claim.

Manufactured home insurance in stuart

Manufactured home insurance in stuartHow to Prepare for a Successful Home Insurance Claim

Preparing for a successful home insurance claim starts long before disaster strikes. Taking proactive steps can significantly streamline the process, ensure faster payouts, and reduce stress during an already difficult time.

The foundation of a strong claim lies in thorough documentation, clear understanding of your policy, and prompt communication with your insurer. By organizing your important documents, maintaining a detailed home inventory, and knowing your coverage limits and exclusions, you position yourself to file a comprehensive and credible claim.

Additionally, understanding the steps to take immediately after damage occurs—such as mitigating further loss and contacting your provider—can make a critical difference in the outcome of your claim.

Document Your Home and Belongings

One of the most important steps in preparing for a potential insurance claim is creating a comprehensive record of your home and personal property.

Metairie home insurance

Metairie home insuranceUse a smartphone or camera to take high-quality photos and videos of each room, capturing furniture, electronics, appliances, and valuable items from multiple angles. Store these files securely in the cloud or an external hard drive along with purchase receipts, appraisals, and serial numbers whenever possible. This visual evidence is crucial for proving ownership and establishing the value of damaged or lost items.

Without proper documentation, insurers may dispute the extent of your losses, leading to reduced settlements or even claim denials. A well-maintained home inventory not only supports your claim but also helps determine the appropriate amount of coverage you need.

Understand Your Insurance Policy Coverage

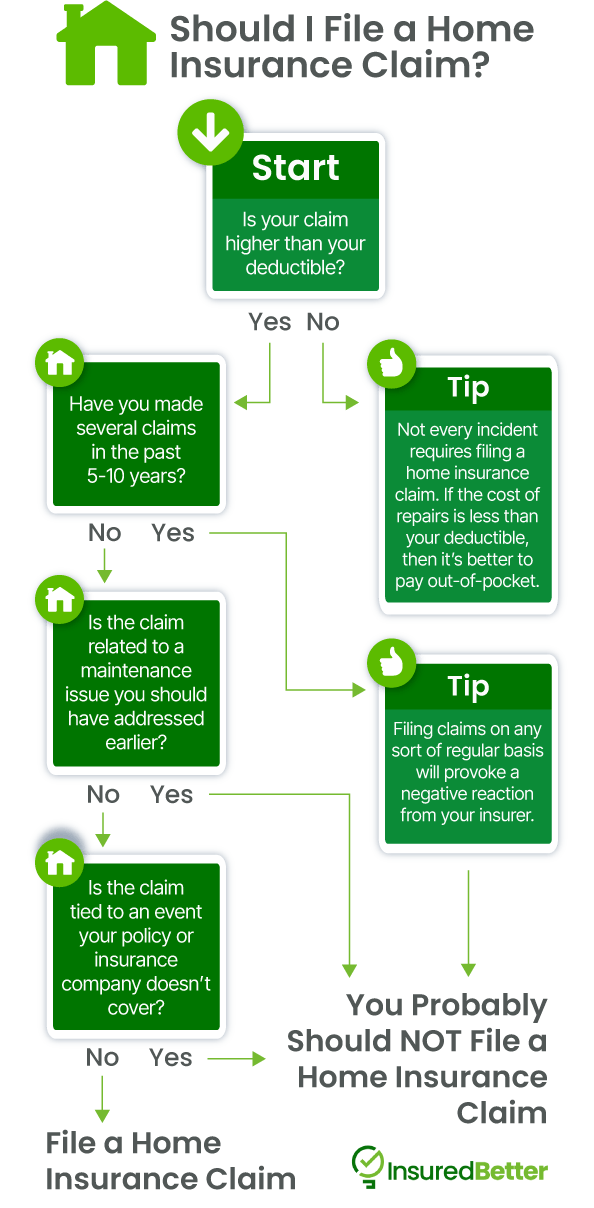

Knowing the details of your home insurance policy is essential to avoid surprises when filing a claim. Carefully review your policy to understand what perils are covered—such as fire, windstorms, or vandalism—and which are excluded, like floods or earthquakes, which often require separate policies.

Pay close attention to your coverage limits, deductibles, and replacement cost versus actual cash value clauses, as these directly affect your payout. For example, a replacement cost policy reimburses you for the cost to replace an item at current prices, while actual cash value accounts for depreciation.

Mobile home insurance in stuart

Mobile home insurance in stuartMisunderstanding these terms can lead to underinsurance or unexpected out-of-pocket expenses. Regularly consult with your insurance agent to clarify terms and update coverage as your home's value or contents change.

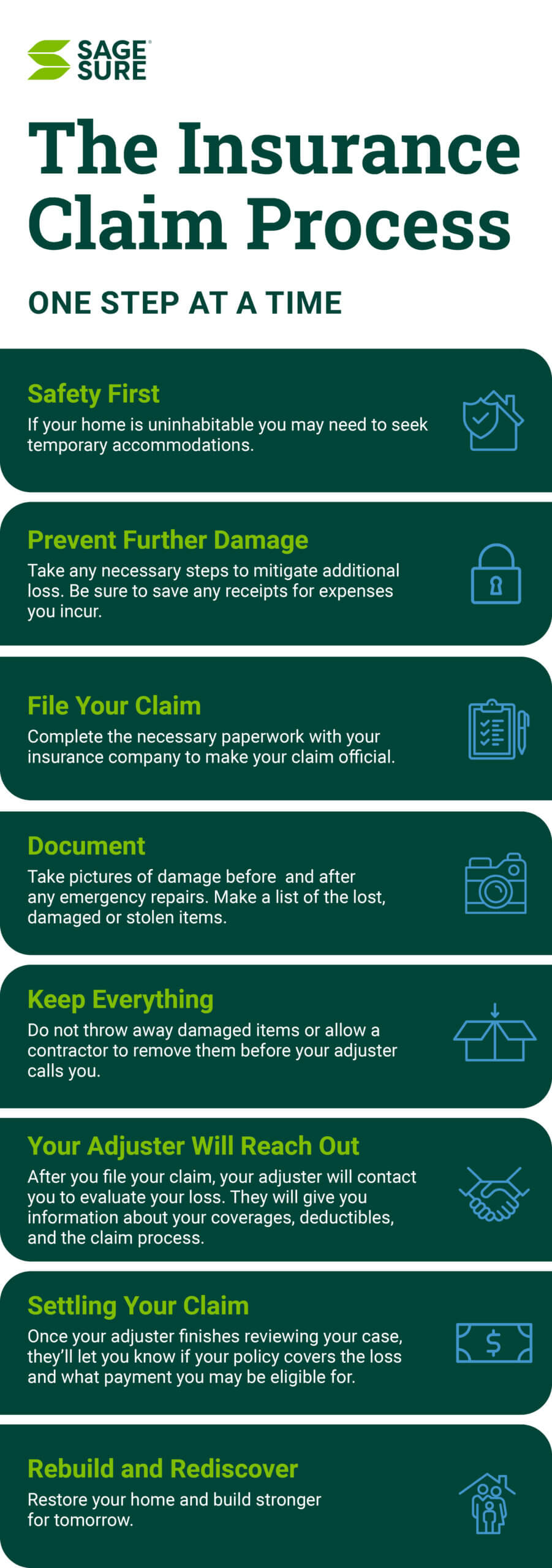

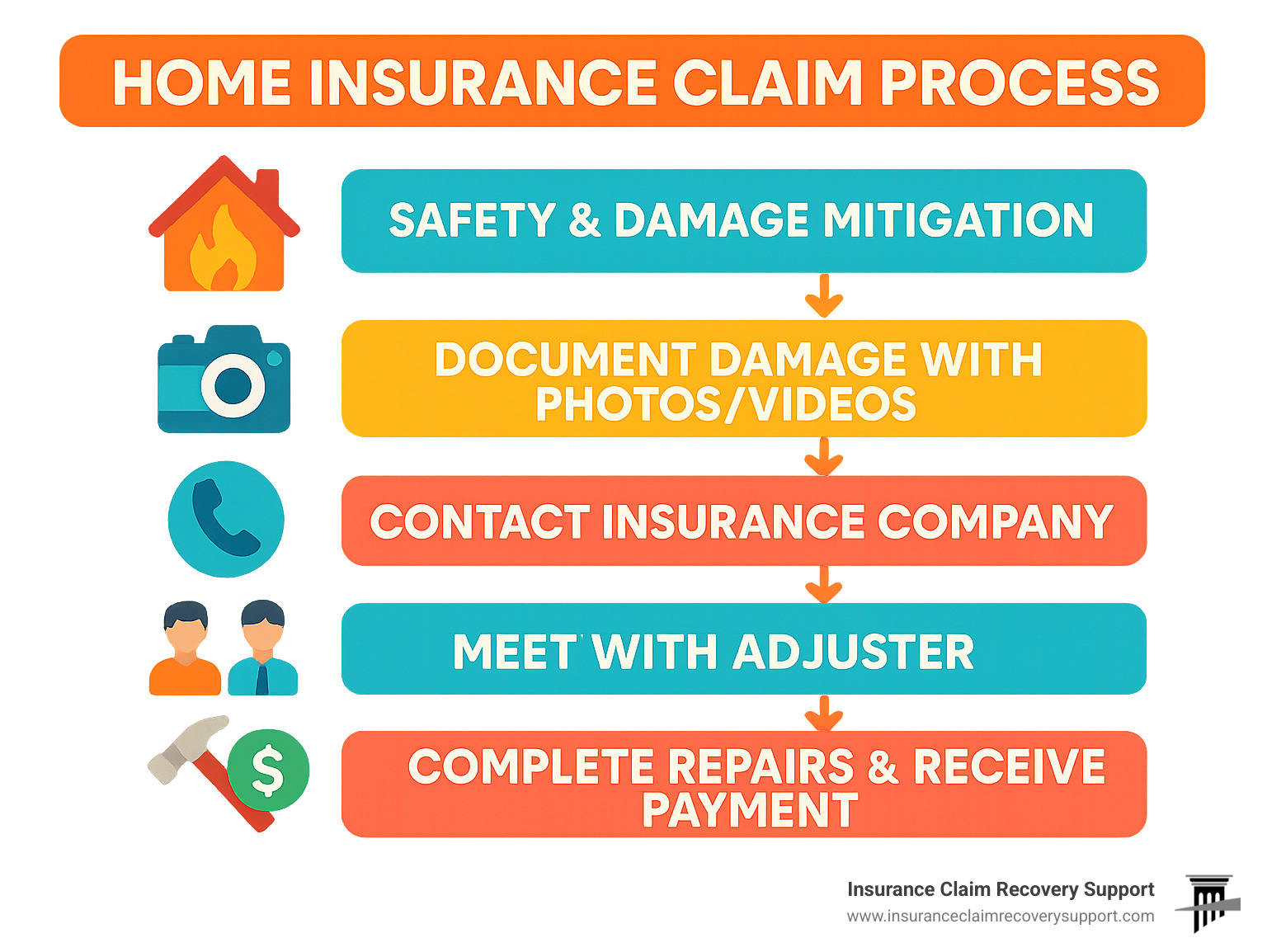

Take Immediate Action After Damage Occurs

After experiencing property damage, taking swift and appropriate steps can protect both your home and your claim’s success.

First, ensure safety by evacuating if necessary and contacting emergency services. Then, take action to prevent further damage—such as covering broken windows, turning off water, or drying wet areas—as most policies require you to mitigate losses. Notify your insurance company as soon as possible, as delays can jeopardize your claim.

Avoid making permanent repairs until an adjuster has inspected the damage, but temporary fixes like boarding up a roof are encouraged. Keep all receipts related to emergency repairs and relocation expenses, as these may be reimbursable under your policy’s loss of use or additional living expenses coverage.

| Action | Why It Matters | Key Tips |

|---|---|---|

| Create a home inventory | Provides proof of ownership and value for lost or damaged items | Update annually; include photos, receipts, and model numbers |

| Review policy details | Helps avoid claim denials due to coverage gaps or exclusions | Ask your insurer about umbrella coverage or endorsements |

| Report claims promptly | Meets policy requirements and speeds up the adjustment process | Use your insurer’s app or portal for faster communication |

| Mitigate further damage | Fulfills your duty to minimize loss under the policy | Keep all repair receipts for reimbursement |

How to Prepare for a Successful Home Insurance Claim: A Step-by-Step Guide

What should you avoid saying during a home insurance claim to ensure a smooth process?

Admitting Fault or Speculating About the Cause

- Avoid stating that you are unsure how the damage occurred or admitting that you may have contributed to the incident. Insurance companies investigate claims closely, and any suggestion of negligence or liability on your part could be used to reduce or deny the payout.

- Instead of saying things like I might have left the faucet running or It could have been my fault, stick to observable facts. Describe the damage without assigning blame or guessing at causes.

- Speculation, even casual, can be recorded and cited in claim reviews. It's better to let the adjuster determine the cause based on evidence rather than offer personal theories that might imply fault.

Providing Unverified or Exaggerated Information

- Never exaggerate the extent of the damage or claim that items were present if they were not. For example, do not say you lost expensive electronics if they weren't actually in the home at the time of the incident.

- Insurers often verify claims through documentation such as receipts, photos, or prior inventories. Inaccurate claims can lead to denial or even accusations of fraud, which can jeopardize future coverage.

- Stick to accurate, measurable details. If you're uncertain about the value of a lost item, say you'll provide documentation later rather than estimating a high value on the spot.

Making Emotional or Defiant Statements

- Refrain from making statements like This is completely unfair or You have to pay for everything, as they can damage the rapport with the claims adjuster and suggest you are being unreasonable.

- Insurance adjusters are trained to assess claims objectively. Emotional outbursts or aggressive language may prompt a more thorough or skeptical review of your claim.

- Keep your communication calm and factual. Focus on cooperation and providing clear evidence rather than expressing frustration or demanding outcomes.

What Are the Key Steps to Understanding the 3 D's in Home Insurance Claims?

Defining the 3 D's: Damage, Determination, and Documentation

- Damage refers to the physical harm sustained by your property due to a covered event such as fire, storm, or vandalism. Understanding what constitutes insurable damage is the first critical step in the claims process, as not all types of wear and tear are eligible for compensation.

- Determination involves the insurance company’s evaluation of whether the cause of damage is covered under your policy. This step includes reviewing policy terms, exclusions, and conditions to decide if the loss qualifies for a payout.

- Documentation is the systematic collection and submission of evidence supporting your claim. This includes photos, videos, repair estimates, receipts, and a detailed inventory of lost or damaged items, all of which help substantiate the extent and value of the loss.

How to Properly Assess and Report Damage

- Inspect your property thoroughly after a loss, noting all visible damage to structures, fixtures, and personal belongings. Make sure to check less obvious areas such as attics, basements, and behind walls where hidden damage may exist.

- Take clear, timestamped photographs and videos from multiple angles to create an accurate visual record. These media files will serve as crucial evidence during the adjuster’s review and help prevent disputes.

- Contact your insurer promptly to report the damage and initiate the claim. Provide a concise description of the incident, the type of damage observed, and any immediate steps you’ve taken to mitigate further loss, such as boarding up broken windows or turning off water supplies.

- Cooperate fully with the insurance adjuster assigned to your case by granting access to your property and answering questions honestly. The adjuster will assess the damage, determine the cause, and verify coverage based on your policy details.

- Review your insurance policy carefully to understand coverage limits, deductibles, and exclusions. This knowledge helps you evaluate whether the insurer’s determination aligns with your contract and allows you to challenge decisions if necessary.

- Keep detailed records of all communications with your insurance company, including emails, letters, and phone calls. Having a paper trail ensures transparency and can support your position if disputes arise during the determination phase.

What steps ensure a successful home insurance claim process?

Document the Damage Thoroughly

- As soon as it is safe to do so, take clear, high-resolution photos and videos of all damaged areas, including structural elements, personal belongings, and any relevant surroundings. This visual evidence serves as crucial proof for your claim.

- Create a detailed inventory of damaged or lost items, noting their approximate value, age, and condition prior to the incident. If you have receipts, manuals, or prior photographs of these items, include them in your documentation.

- Write a descriptive account of how the damage occurred, including the date, time, and any contributing factors such as weather conditions or accidents. This narrative can help the insurance adjuster understand the context behind the claim.

Contact Your Insurance Company Promptly

- Notify your insurer as soon as possible after the incident, ideally within 24 to 48 hours. Most policies have specific timeframes for filing claims, and early reporting helps prevent delays.

- Use the official claims process outlined in your policy—this may involve calling a hotline, using a mobile app, or submitting a form online. Follow the instructions precisely to ensure your claim is officially registered.

- Provide accurate and consistent information during your initial report. Be ready to share details such as your policy number, a summary of the damage, and whether emergency repairs have been made.

Cooperate with the Claims Adjuster and Track Expenses

- Schedule and prepare for the adjuster’s inspection by ensuring access to all affected areas and having your documentation readily available. Be present during the assessment to clarify any concerns or details about the damage.

- Keep detailed records of all communication with the insurance company, including names, dates, and summaries of conversations. Save emails, claim reference numbers, and any written correspondence.

- Maintain receipts for temporary repairs, lodging, or replacement items if your home is uninhabitable. Most policies cover reasonable expenses, but reimbursement requires proof of payment and necessity.

Frequently Asked Questions

What documents should I gather before filing a home insurance claim?

Gather your insurance policy, recent photos of the damaged area, receipts for repairs or replacements, and a detailed inventory of affected items. Also, include any police or fire reports if applicable. Having these documents ready speeds up the claims process and supports your case. Keep digital and physical copies in a secure location for quick access during emergencies.

How do I report a home insurance claim promptly?

Contact your insurance company as soon as possible after the incident, either through their website, app, or customer service line. Provide essential details like the date, nature of damage, and extent of loss. Prompt reporting helps prevent claim delays and ensures timely inspection. Be honest and clear in your communication. Many insurers offer 24/7 claim reporting to assist homeowners quickly after an incident.

Should I make temporary repairs before the insurance adjuster arrives?

Yes, make only necessary temporary repairs to prevent further damage, like covering broken windows or leaking roofs. Keep all receipts for materials, as insurers may reimburse these costs. Avoid major renovations until the adjuster inspects the property. Document the damage with photos before starting repairs. Taking reasonable steps shows responsibility and helps protect your home, but always wait for approval before permanent fixes.

How can I ensure a smooth claims inspection process?

Be present during the adjuster’s visit and provide access to all affected areas. Share your documentation, including photos and repair estimates. Clearly explain the incident and point out all damages. Ask questions if you don’t understand something. Being cooperative and organized helps the adjuster assess the claim accurately. Prepare a list of damaged items and previous maintenance records to support your claim effectively.

Leave a Reply