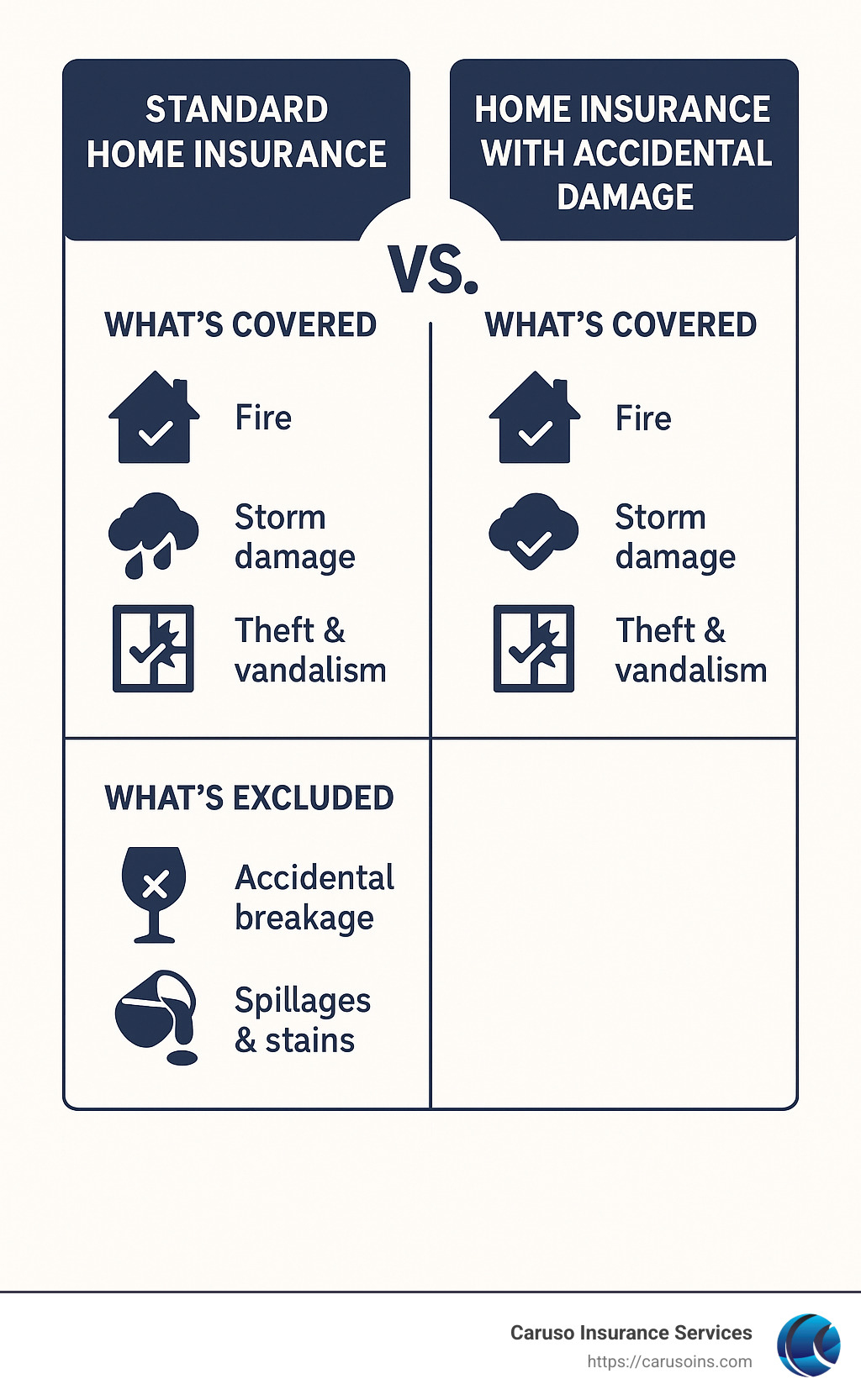

Does home insurance cover accidental damage

Accidental damage is an unfortunate reality in everyday life, whether it’s spilling water on a laptop, tripping and cracking a window, or knocking over a valuable piece of furniture.

While these incidents happen to everyone, they can lead to costly repairs or replacements. Home insurance is designed to protect homeowners from financial loss due to unexpected events, but coverage varies significantly between policies.

Many standard home insurance plans cover specific perils like fire, theft, or storm damage, but accidental damage often requires additional coverage. Understanding what your policy includes—and where gaps may exist—is essential for full protection.

Philadelphia American Life Insurance Provider Phone Number For Claims

Philadelphia American Life Insurance Provider Phone Number For ClaimsDoes Home Insurance Cover Accidental Damage?

Standard home insurance policies typically do not automatically cover accidental damage to your property or personal belongings. Most basic homeowners insurance plans focus on protection against named perils such as fire, theft, vandalism, and natural disasters.

However, accidental incidents—like spilling water and damaging hardwood floors, dropping a television, or drilling into a wall and hitting a pipe—are generally excluded unless you’ve specifically added an accidental damage endorsement or rider to your policy.

This optional coverage can extend protection to sudden and unintentional mishaps that aren't caused by negligence or lack of maintenance. It's important to carefully review your policy documents and speak with your insurer to determine whether your plan includes this add-on and what types of accidents are covered.

What Is Considered Accidental Damage in Home Insurance?

Accidental damage refers to sudden, unexpected, and unintentional events that cause harm to your home or its contents.

Who Are The Best Life Insurance Companies

Who Are The Best Life Insurance CompaniesExamples include a child accidentally breaking a window with a ball, a DIY project gone wrong resulting in damaged walls or flooring, or knocking over and destroying an expensive appliance. It does not include gradual wear and tear, damage from neglect, or issues stemming from poor maintenance—such as a leaky roof that worsens over time.

Insurers define accidental damage narrowly, so the incident must be immediate and clearly unintentional. Even then, coverage is usually only available if you've purchased additional protection, as most standard policies do not include it by default.

How to Add Accidental Damage Coverage to Your Policy

To gain protection against accidental damage, you must typically add a specific endorsement or opt for a more comprehensive policy that includes this feature.

This addition, often referred to as an accidental damage rider, can be applied to both dwelling coverage and personal property. The cost varies depending on the insurer, the value of your home and possessions, and the level of coverage you desire. When shopping for home insurance, ask your provider whether accidental damage is included or available as an add-on.

Whole Life Dividend Paying Insurance

Whole Life Dividend Paying InsuranceSome premium-level policies include this protection automatically, while in other cases, a modest increase in your premium can significantly expand your coverage. Always document the terms, exclusions, and limits of this coverage before finalizing your policy.

Common Examples of Covered and Non-Covered Accidents

While coverage depends on the specific policy and insurer, certain types of accidental damage are more likely to be included when the rider is active. For example, accidentally cracking a countertop while moving furniture or short-circuiting electronics due to a power surge might be covered.

On the other hand, damage from long-term exposure, improper installation, or incidents involving lack of supervision (such as leaving a bath overflowing unattended for hours) are typically excluded. To clarify what incidents are protected, the following table outlines common scenarios and their usual coverage status under an accidental damage endorsement.

| Incident | Coverage Status | Notes |

|---|---|---|

| Spilling wine on a carpet causing permanent stain | Covered (with rider) | Only if accidental damage endorsement is active; may require proof of sudden incident |

| Drilling into a wall and damaging electrical wiring | Covered (with rider) | Typically covered if done by homeowner and not part of a professional renovation |

| Appliance failure due to normal wear over time | Not covered | Considered maintenance issue, not accidental damage |

| Child breaking a large window with a toy | Covered (with rider) | Sudden and unintentional damage is key factor |

| Water damage from a leaking pipe over several weeks | Not covered | Gradual damage and lack of maintenance are excluded |

Does Home Insurance Cover Accidental Damage? A Comprehensive Guide

Does homeowners insurance typically cover accidental damage claims?

Homeowners insurance typically does not cover accidental damage caused by the policyholder or household members under standard policy terms.

1199 Life Insurance Phone Number

1199 Life Insurance Phone NumberMost basic home insurance policies are designed to protect against sudden, accidental, and unforeseen perils such as fire, windstorms, theft, or water damage from burst pipes. However, general wear and tear, intentional damage, or accidents that result from negligence—such as spilling paint on hardwood floors or breaking an appliance—are usually excluded.

Some insurance companies may offer optional endorsements or additional coverage for accidental damage, particularly to personal property, but this is not included in standard policies. Policyholders should carefully review their declarations page and consult with their insurance provider to understand the full scope of what is and isn't covered.

What Types of Accidents Are Usually Covered by Homeowners Insurance?

- Standard homeowners insurance typically covers accidental damage that results from sudden, external, and identifiable events. For example, if a tree falls on your roof during a storm, the resulting structural damage is covered under the dwelling protection portion of the policy. These are events beyond the homeowner's control and are classified as covered perils.

- Accidental water damage from plumbing failures, such as a sudden burst pipe or malfunctioning water heater, is generally included. However, damage due to long-term leaks or lack of maintenance is typically excluded. The key factor is whether the incident was sudden and accidental rather than gradual or preventable.

- Fire damage caused accidentally—like a kitchen fire from unattended cooking—is usually covered. These are considered unforeseen accidents and fall within the named perils of most policies, providing coverage for repairs, temporary living expenses, and replacement of damaged belongings, up to policy limits.

Why Are Most Accidental Damages Not Covered Under Standard Policies?

- Homeowners insurance is structured to cover catastrophic or unexpected events rather than everyday mishaps. Accidents like dropping a TV, ripping carpet, or chipping a countertop are considered maintenance responsibilities of the homeowner and are often deemed preventable or part of normal use, so they fall outside policy protections.

- Insurers exclude routine accidental damage to prevent misuse of the policy and maintain affordable premiums. If every minor accident were covered, it would significantly increase the cost of coverage for all policyholders. Therefore, coverage is reserved for large-scale risks that could cause financial hardship.

- Policies are written to distinguish between accidental damage caused by external forces (like a hailstorm breaking windows) and self-inflicted or internal accidents (like knocking over a lamp). The former is covered because it aligns with defined perils; the latter is not, as it’s viewed as a personal responsibility.

Can You Add Accidental Damage Coverage to a Homeowners Policy?

- Some insurance providers offer optional endorsements or floaters that extend coverage to include accidental damage, particularly for high-value personal property like electronics, jewelry, or furniture. These endorsements usually come with an additional premium and specific limits on coverage amounts.

- Standalone accidental damage protection is rare in standard homeowners insurance but may be available through specialty insurers or as part of a broader home warranty plan. These plans often cover repairs or replacements for incidents like shattered screens or damaged flooring.

- Policyholders interested in such coverage should consult their insurer about riders or supplemental policies. It’s important to review terms carefully, as even added coverage may exclude certain types of damage, impose deductibles, or limit the number of claims per year.

Does home insurance include accidental damage coverage, and is it worth adding?

What Is Accidental Damage Coverage in Home Insurance?

- Accidental damage coverage in home insurance refers to protection against sudden and unintentional incidents that harm your home or personal belongings. Examples include spilling a drink on a laptop, dropping a TV, or drilling through a water pipe while hanging a shelf.

- Standard home insurance policies typically cover major perils like fire, theft, or storm damage but often exclude everyday accidents unless explicitly added. This means that if you accidentally break a window or damage a fixed appliance, the repair might not be covered without specific accidental damage endorsement.

- This type of coverage can usually be added as an optional extension to your policy, either for the structure of the home, your personal possessions, or both. It is commonly offered by insurers in the UK and other regions, though availability and terms can vary significantly in the U.S. market.

Does Standard Home Insurance Include Accidental Damage?

- Generally, most standard home insurance policies in the United States do not include accidental damage coverage for personal property or the dwelling by default. They focus on more significant insured events such as fires, vandalism, or natural disasters, leaving smaller but costly mishaps uncovered.

- In contrast, some multi-peril home insurance policies, particularly in countries like the UK, may include limited accidental damage cover for fixed installations like built-in cabinets, plumbing, or flooring. However, this still might not extend to movable personal items such as electronics or furniture.

- Homeowners who want protection for everyday accidents usually need to pay an additional premium to add an accidental damage rider or endorsement. Without this add-on, claims for events like knocking a hole in the wall or cracking a countertop during renovation are likely to be denied.

Is It Worth Adding Accidental Damage Coverage to Your Policy?

- The value of adding accidental damage coverage depends on your lifestyle, living situation, and risk tolerance. Families with young children, pets, or frequent home improvement activities may benefit from the extra protection, as such environments increase the likelihood of accidental incidents.

- For those living in high-value homes with expensive fixtures or electronics, the cost of replacing or repairing an item accidentally damaged can outweigh the additional premium over time. In these cases, accidental damage coverage might offer worthwhile financial security.

- However, if you're cautious, live alone, or have a lower-value property, the added cost may not justify the benefit. Carefully evaluate your claim history, the cost of the endorsement, and the coverage limits before adding it—especially since some policies impose per-incident caps or exclude certain high-risk items.

What accidental damages are typically excluded from home insurance coverage?

Allstate Life Insurance Forms

Allstate Life Insurance FormsFlood and Water Damage from External Sources

Home insurance policies typically exclude damage caused by flooding or water entering the home from outside sources. This category includes rising water from rivers, storm surges, overflowing lakes, and municipal water system failures.

Standard policies are designed to cover sudden and accidental internal water damage—like a burst pipe—but not water that enters gradually or due to natural events beyond the homeowner’s control. As a result, homeowners in flood-prone areas often need to purchase separate flood insurance through government programs or private insurers.

- Flooding from natural disasters such as hurricanes or heavy rainfall is nearly always excluded from standard home insurance.

- Surface water runoff, especially due to poor drainage or landscaping issues, is not covered as it’s considered preventable or external.

- Damage from sewer or drain backups may require a separate endorsement or rider, as they are not automatically included.

Damage from Termites, Pests, and Wear and Tear

Most accidental damage exclusions in home insurance involve issues stemming from lack of maintenance or gradual deterioration. Infestations by termites, rodents, or other pests are routinely excluded because they are viewed as preventable through regular home upkeep.

Similarly, damage caused by long-term wear and tear—such as roofing degradation, rusting pipes, or wood rot—is not considered “accidental” and thus falls outside the scope of coverage. Insurers expect homeowners to inspect and maintain their property to prevent such issues.

- Termite damage, though extensive, is not covered because it develops slowly and can be mitigated with routine inspections.

- Rodent infestations that chew through wires or insulation are considered maintenance-related and excluded from accidental coverage.

- Structural weakening due to mold, dry rot, or prolonged moisture exposure is seen as neglect, not a sudden accident.

Earth Movements Such as Earthquakes and Landslides

Standard home insurance policies do not cover damage caused by earthquakes, landslides, sinkholes, or other earth movements. These events are classified as high-risk and fall under separate specialized policies.

Earthquakes, in particular, can cause significant structural damage, but because of their unpredictable nature and potential for widespread loss, they require an additional earthquake insurance policy. Similarly, homes built on unstable terrain may face landslide risks that are not covered unless specifically insured.

- Earthquake damage, including cracked foundations and collapsed walls, requires a standalone policy for coverage.

- Landslide or mudflow damage is often conflated with flood damage and is excluded unless covered under specific geologic hazard add-ons.

- Sinkholes, especially common in certain geological regions, are typically excluded and necessitate extra coverage through endorsement or specialty insurers.

Frequently Asked Questions

Does standard home insurance cover accidental damage?

Standard home insurance typically covers major perils like fire, theft, and storms, but accidental damage is often not included automatically. Basic policies usually exclude incidents like spilling paint, breaking a window, or damaging flooring. Accidental damage coverage is generally available as an optional add-on. Check your policy details or speak with your insurer to confirm what’s included and whether you need to purchase additional protection for such events.

What types of accidental damage are covered by home insurance?

If you’ve added accidental damage coverage to your policy, it may cover events like breaking a window, damaging walls, or accidentally flooding a room. Common inclusions are cracked screens, fallen TVs, or holes in walls. However, coverage varies by insurer—some exclude wear and tear or damage caused by negligence. Always review your policy wording to understand exactly what incidents are protected and any applicable exclusions or limits on claims.

Is accidental damage to personal belongings covered under home insurance?

With accidental damage coverage, personal belongings like laptops, furniture, and electronics may be protected if they're damaged due to unexpected incidents, such as dropping a phone or spilling liquid on a laptop. This usually applies to items both inside and sometimes outside the home, depending on the policy. Standard contents insurance without this add-on typically won’t cover such accidents. Confirm coverage limits and exclusions with your provider.

How do I add accidental damage coverage to my home insurance?

You can usually add accidental damage coverage as an optional extra when purchasing or renewing your home insurance policy. It may increase your premium, but it provides protection for unexpected accidents like broken appliances or damaged fixtures. Contact your insurer or broker to discuss adding this coverage. Be sure to compare quotes, understand the terms, and verify which areas of your home and belongings are included under the accidental damage protection.

Leave a Reply